There was an extremely benign inflation indicator in the States today:

Wholesale prices in the U.S. declined in September by the most since the start of the year as costs fell for gasoline, food and brokerage services.

The 0.5 percent decrease in the producer-price index was the biggest since January and followed no change in August, Labor Department figures showed Wednesday. The median forecast of economists surveyed by Bloomberg called for a 0.2 percent drop. Costs were down 1.1 percent over the past 12 months.

…

Energy expenses decreased 5.9 percent in September, the most since January, after falling 3.3 percent the month before. Food prices dropped 0.8 percent after a 0.3 percent gain. The costs of eggs slumped, while beef and veal prices plunged 7.9 percent, the most since January 2004.

Wholesale prices excluding these two components unexpectedly declined 0.3 percent. The median forecast in the Bloomberg survey called for a 0.1 percent gain. Those costs were up 0.8 percent from September 2014.

Goods prices, which have fallen for three straight months, slumped 1.2 percent in September. The costs of services dropped

0.4 percent, the most since February. More than a quarter of that decrease was due to slumping costs for securities brokerage, dealing and investment advice, the Labor Department said.

After eliminating food, energy and trade services to arrive at a reading that some economists prefer because it excludes one of the report’s most volatile components, wholesale costs also decreased 0.3 percent in September. That was the biggest decline since records began in 2013

“slumping costs for … investment advice”??? This isn’t a slow-down! This is a DEPRESSION!

And retail sales were sluggish:

Consumers in the U.S. tempered purchases at retailers in September, pocketing the savings from lower fuel costs and making for a weak finish to the third quarter.

The 0.1 percent gain followed little change in the prior month that was weaker than previously reported, Commerce Department figures showed Wednesday in Washington. The median forecast of 82 economists surveyed by Bloomberg called for a 0.2 percent advance. More than half of merchant categories showed decreases.

Sluggish sales may raise concern about the staying power of consumer spending, which accounts for about 70 percent of the economy, at a time overseas demand is also cooling. While job gains and cheap fuel may help to underpin purchases, a pickup in wages remains elusive as Federal Reserve policy makers are weighing whether to raise interest rates this year.

Naturally, this led the market to believe that maybe a rate hike isn’t imminent:

First Treasuries traders were banking on September for the Federal Reserve to raise interest rates. Then they turned their focus to December. Now even March is looking like a toss-up.

The drumbeat of weaker-than-forecast global economic data continued Wednesday as September U.S. retail sales fell short of analysts’ expectations. The report came after Fed Governor Daniel Tarullo, who votes on rate decisions, said Tuesday that he doesn’t currently favor an increase in 2015, even though Chair Janet Yellen has said a move would be warranted.

Traders’ bets that the Fed will lift its benchmark by year-end have dropped to less than a one-in-three chance, and aren’t much higher for January. For March, the probability has tumbled to about 50 percent, from 65 percent a month ago. The calculation is based on the assumption that the effective fed funds rate will average 0.375 percent after the first increase.

The uncertainty may be exacerbated by a disagreement regarding a basic tenet of economics:

On Monday, Governor Lael Brainard said that global risks warranted a more cautious stance from the central bank. The next day, fellow Governor Daniel Tarullo indicated that he expects it will be appropriate to keep rates on hold through year end.

The details of their dovish commentary are much more noteworthy, as both appear to disagree with Yellen’s description of what the Fed’s reaction mechanism ought to be.

At the heart of the matter is the extent to which the progress made in achieving one part of the central bank’s mandate (full employment) portends improvement in the other part (price stability, defined as an annual inflation rate of 2 percent).

The relationship between unemployment and inflation is typically understood in terms of the Phillips Curve, which holds that there is an inverse relationship between inflation and unemployment.

Yellen’s previous remarks suggest she thinks a firming labor market will indeed lead to higher levels of inflation.

…

The governors are much more skeptical.

“I do think under these circumstances it’s probably wise not to be counting so much on past correlations—things like the Phillips Curve, which really haven’t been operating very effectively for 10 years now—and instead to really look for some tangible evidence of, for example, pickups in wages or inflation that allow us to make informed decisions based on the evidence,” Tarullo said in an interview with CNBC.

Brainard issued what appeared to be an even more direct rebuttal.

“To be clear, I do not view the improvement in the labor market as a sufficient statistic for judging the outlook for inflation,” she said. “A variety of econometric estimates would suggest that the classic Phillips curve influence of resource utilization on inflation is, at best, very weak at the moment.”

Silver Bullion Trust has fired another round in its battle with Sprott (bolding from original):

Bruce Heagle, Chair of the Special Committee of the Board of Trustees of SBT stated: “Sprott’s recent claims of an “increased offer” are illusory; in reality, nothing has changed. Their supposed “premium consideration” of $0.025 per Unit is immaterial; it represents less than 0.3% of the current value of an SBT Unit, and would be more than offset by the higher annual management fees charged by Sprott. Sprott continues to offer no meaningful premium, would charge significantly higher management fees, strip Unitholders of virtually all their governance rights and expose certain U.S. Unitholders to higher tax risk. Rejecting Sprott’s self-serving, inadequate offer and retaining your SBT Units, characterized by an industry-leading expense ratio, superior bullion security and safeguards, and a sound, tax efficient structure, is the clear choice for long-term bullion investors.”

I’ll be very disappointed when the whole thing is resolved!

Element Financial, whose preferreds were recent added to the HIMIPref™ database, is shifting strategic priorities:

Element Financial Corporation (TSX:EFN) (“Element” or the “Company”), today announced that it has initiated a series of steps that will accelerate the transformation of the Company into North America’s leading fleet management and services enterprise with complementary commercial finance operations. Specifically, the Company has initiated a process to harvest capital from its Canadian commercial & vendor (“C&V”) operations for reinvestment in both organic growth and acquisition opportunities in its core fleet management business. These opportunities include the acquisition of existing fleet management businesses and portfolios as well as fleet services companies that have the potential to drive incremental service fee income for the Company. Concurrently, the Company will optimize the scale and focus of its non-fleet businesses to complement its core fleet management operations.

Some old research done for Parliament illustrates effective marginal tax rates for low income earners:

The “welfare wall” refers to the disincentives to work created by interaction between the system of social assistance and personal income taxation in Canada. Canadians who receive social assistance and subsequently accept low-paying employment face a series of consequences that could potentially make them worse off, including: higher income and payroll taxes; new work-related expenses such as transportation, clothing and childcare; reduced income support in the form of social assistance and income-tested refundable tax credits; and loss of in-kind benefits such as subsidized housing and prescription drugs.

This welfare wall can be demonstrated by estimating an individual’s effective marginal tax rate; that is, the costs associated with the next dollar of earned income. Figure 1 shows that, under the current system of social assistance and taxation in Canada, a single parent with one child who increases his/her earnings from $0 to $10,000 would lose an estimated 78 cents of every additional dollar earned. By comparison, an increase in earnings from $40,000 to $50,000 has an effective marginal tax rate of 41%.

The effective marginal tax rate of 78% on the FIRST $10,000 of earnings is, of course, ridiculous and points out the absurdity of things like the coming Toronto proposal for income-based pricing of bus passes, discussed yesterday, which will only increase the effective marginal rate by withdrawing subsidies as income increases. One suggestion that has some solid thinking behind it is for substantial refundable tax credits to replace social programmes:

The current tax system contains more than $80-billion of tax credits which are non-refundable, which means that low-income Canadians who do not have sufficient taxes owing cannot benefit from them in the same fashion as higher-income taxpayers. While tax filers will be most familiar with the basic personal amount at the top of Schedule 1 of the federal income tax form, other credits for age, eligible dependents, employment and education are also important.

Our recent research paper evaluates the effect of converting these non-refundable credits to refundable credits in the fashion of existing credits such as the Goods and Services Tax Credit and the Working Income Tax Credit and the recently replaced National Child Benefit. A refundable credit simply converts any excess between the credit and taxes owing to a refundable benefit, allowing low-income tax filers to realize the benefits of these tax credits that already accrue to higher-income tax filers.

The paper, titled THE IMPACT OF CONVERTING FEDERAL NON-REFUNDABLE TAX CREDITS INTO REFUNDABLE CREDITS by Wayne Simpson and Harvey Stevens is summarized:

With economic inequality on the rise in Canada, the federal government needs to consider innovative solutions. One possibility for improving the tax-transfer system involves refundable tax credits (RTCs). Making all tax credits refundable wouldn’t require Ottawa to introduce new tax measures; the Canadian tax system already contains a mix of RTCs and NRTCs, so the government could simply continue its practice of designing tax credit programs to be refundable.

Using Statistics Canada’s Social Policy Simulation Database and Model, this paper examines the impacts and cost of converting NRTCs to RTCs, with and without an income exemption equal to 25 percent of the before-tax low-income standard for a census family, the Census Family Low-Income Line.

Under the Option Without Exemption (OW/OE), RTC recipients are taxed at a single rate of 15 percent, regardless of family size, right up to the Line. Under the Option With Exemption (OWE), RTC recipients are taxed at zero percent up to 25 percent of the Line and at a single rate of 20 percent, regardless of family size, up to 100 percent of the Line.

The incremental cost of switching NRTCs to RTCs under the OW/OE is $6.6 billion, as additional benefits are provided to 6.4 million families — slightly less than 37 percent of all families. The cost of the OWE is $7.2 billion, as benefits flow to slightly more families — 6.45 million. However, the percentage of benefits reaching low-income families is much higher under the OWE (69 percent vs. 49 percent). Additionally, the OWE provides an average of nine percent more RTC benefits to low-income tax filers, making it clearly the superior option for poverty reduction. Moreover, the paper shows that alternative conversion schemes that set benefit reduction rates to differ by family size can further increase the benefits to low-income families at a lower overall cost.

Such changes would elicit a labour-supply response in terms of a reduction in hours worked, and while the effect is smaller under the less expensive OW/OE, the difference between the two options is slight.

This paper simulates the conversion of NRTCs to RTCs in comprehensive detail, besides providing practical advice on how such a shift would be funded. It offers valuable food for thought on an issue that is increasingly critical to Canadian society.

“Trigger warnings” have become a popular bone of contention at universities and I’ve decided to experiment with their use myself. So, before you proceed to read about the day’s market action:

Click for Big

Click for BigIt was yet another crummy day for the Canadian preferred share market, with PerpetualDiscounts and FixedResets both down 59bp and DeemedRetractibles losing 80bp. The Performance Highlights table is … well, you know. It’s the Performance Highlights table. It highlights performance. Of particular interest today though, what the amount of churn; some issues did really, really well! Volume was very extremely awfully high – this is like tax-loss selling season! And perhaps it is!

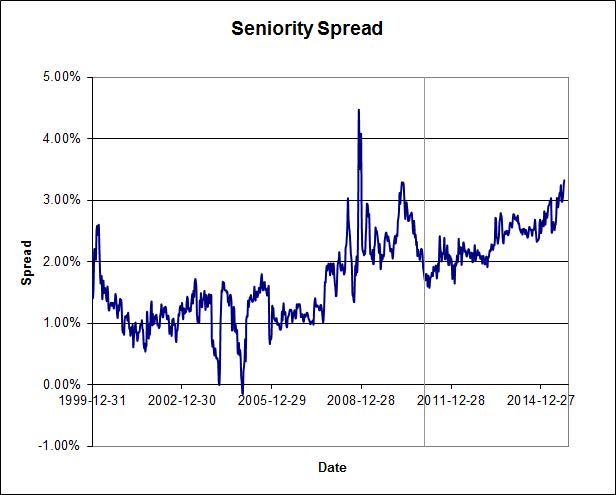

PerpetualDiscounts now yield 5.90%, equivalent to 7.67% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 4.25%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 340bp, a number I didn’t really expect to see ever again, a significant widening from the 330bp reported October 7.

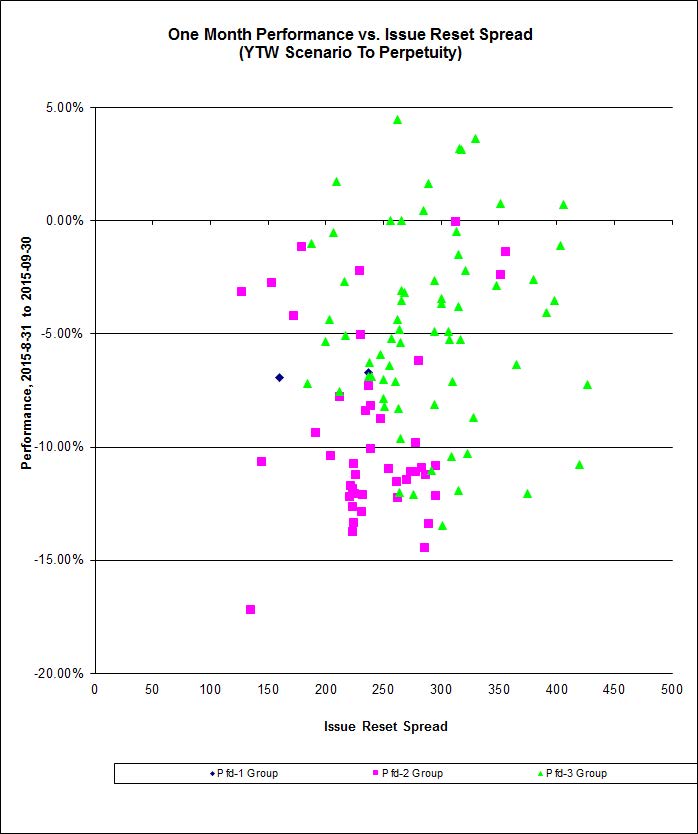

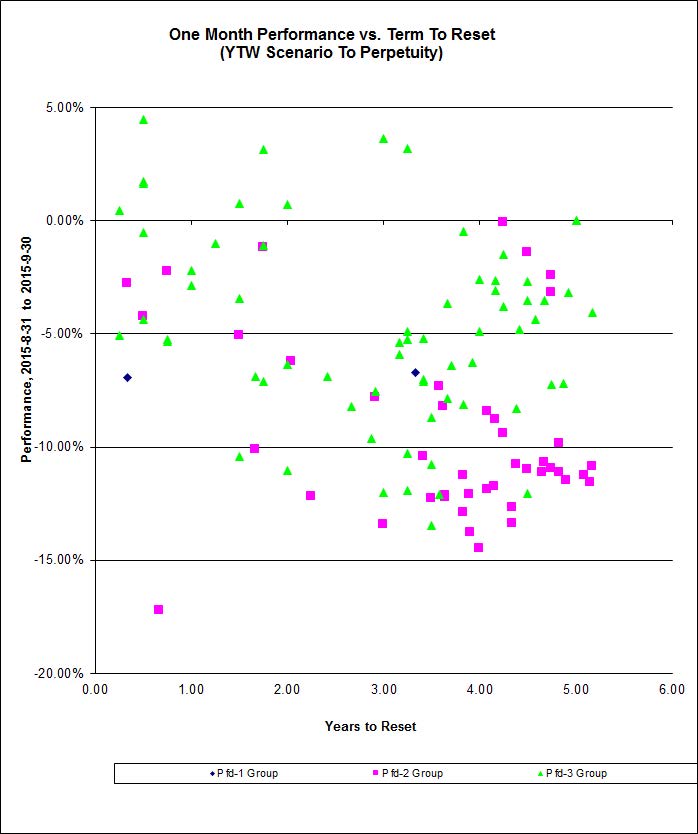

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

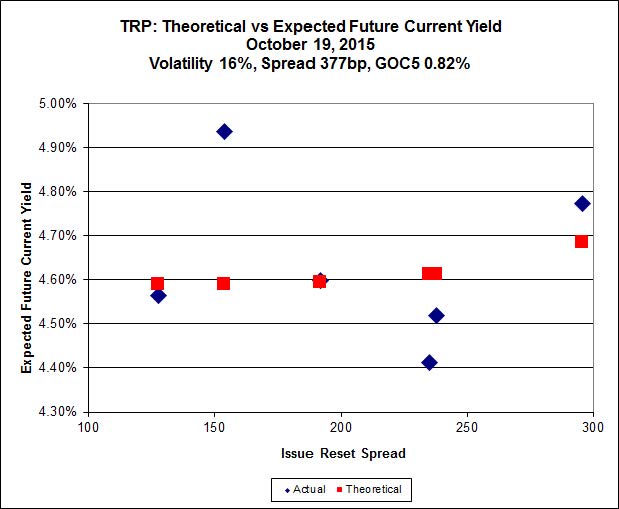

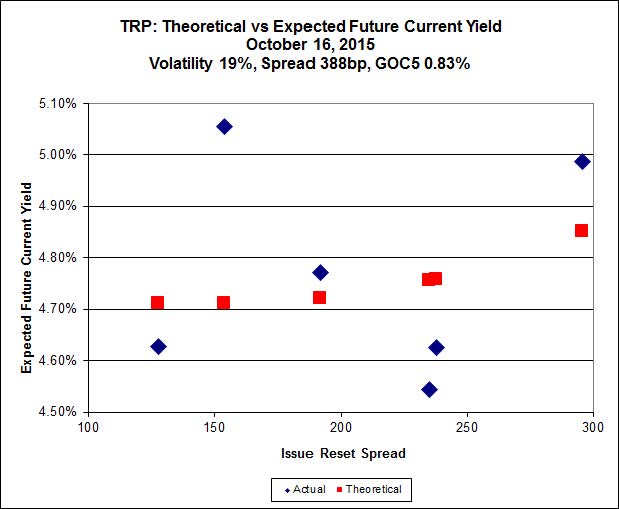

Here’s TRP:

Click for Big

Click for BigImplied Volatility declined today with the normalization of the bid on TRP.PR.D, but remained ridiculously high.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.50 to be $0.63 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.75 cheap at its bid price of 11.33.

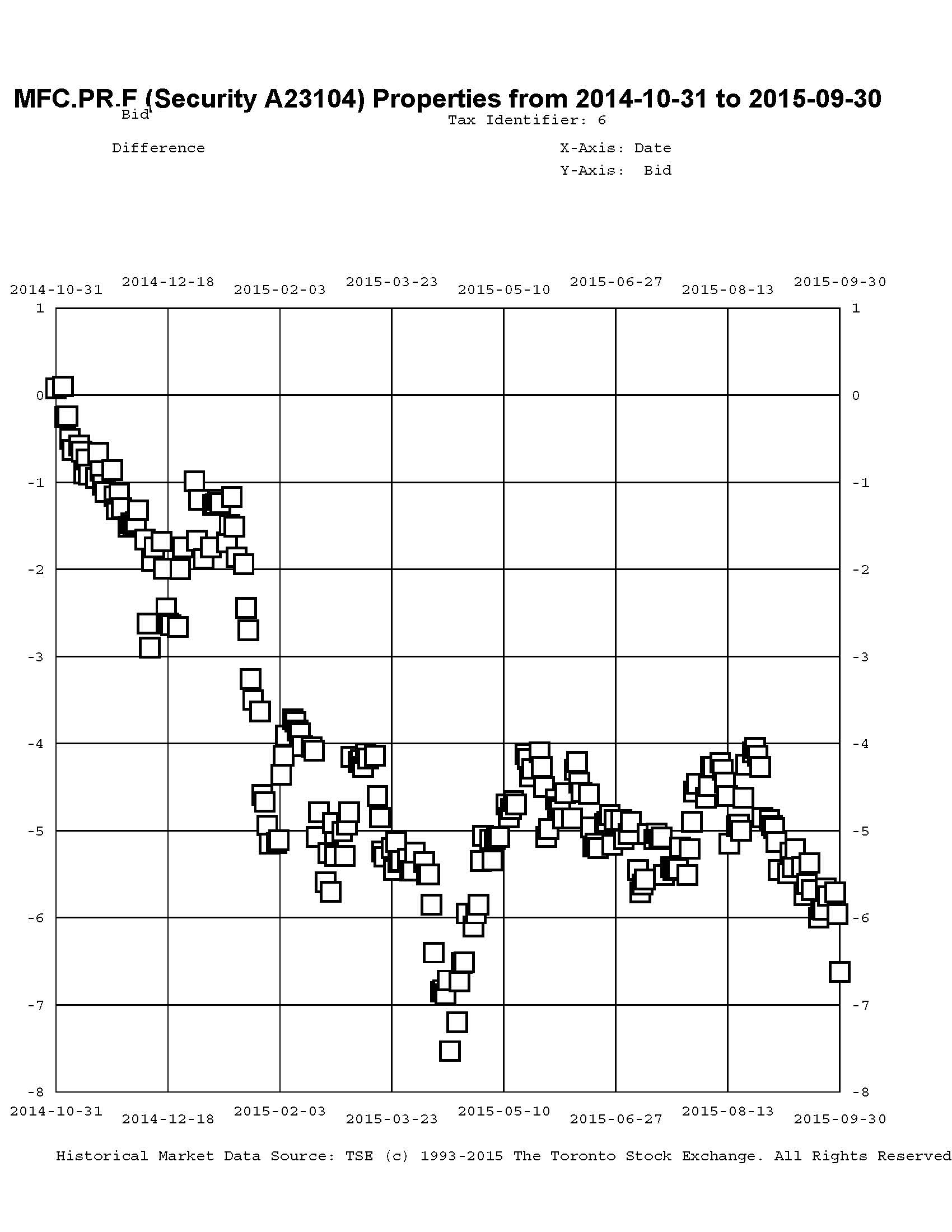

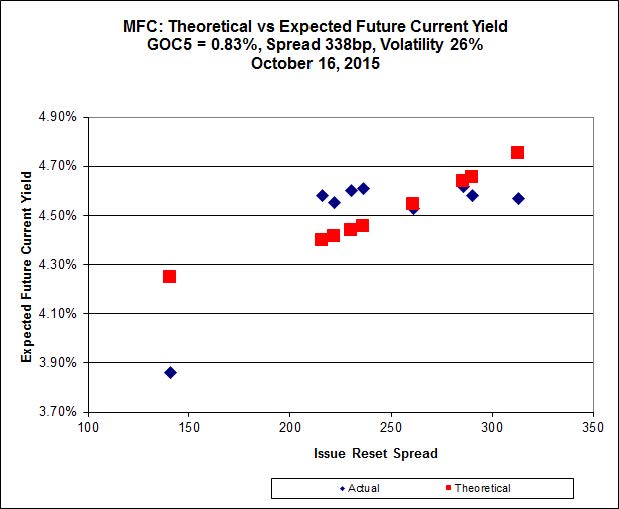

Click for Big

Click for BigImplied Volatility shot upwards today, propelled by excellent relative performance of MFC.PR.F, which is featured on the Performance Highlights table.

Most expensive is MFC.PR.F, resetting at +141bp on 2016-6-19, bid at 14.40 to be 1.04 rich, while MFC.PR.K resetting at +222bp on 2018-9-19, is bid at 15.86 to be 0.96 cheap.

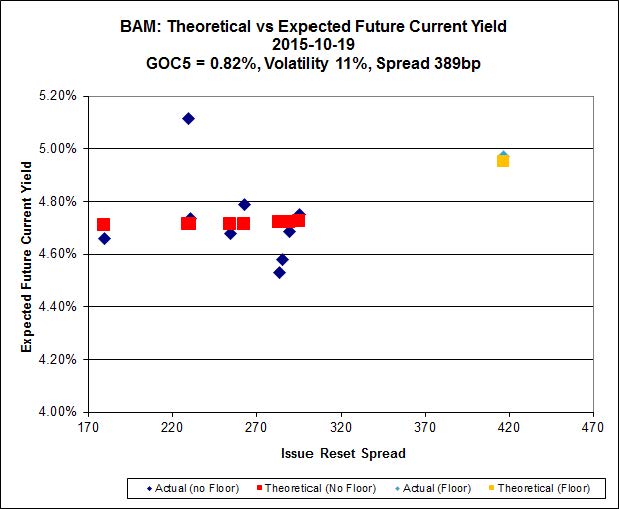

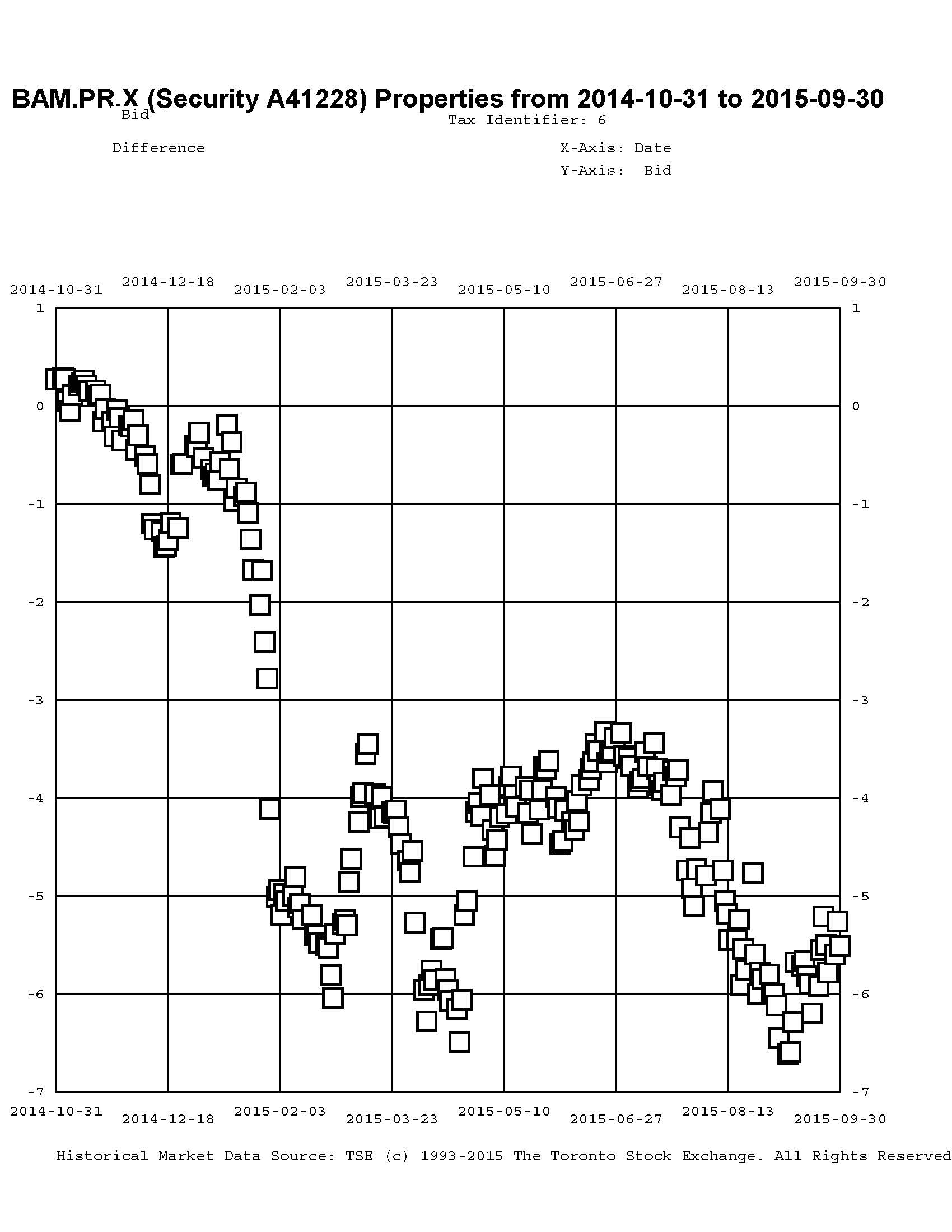

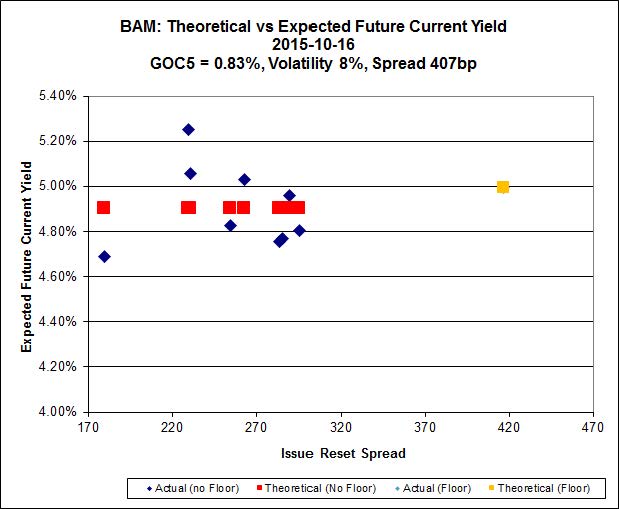

Click for Big

Click for BigThe fit on the BAM issues continues to be horrible!

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.60 to be $0.90 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.19 and appears to be $0.86 rich.

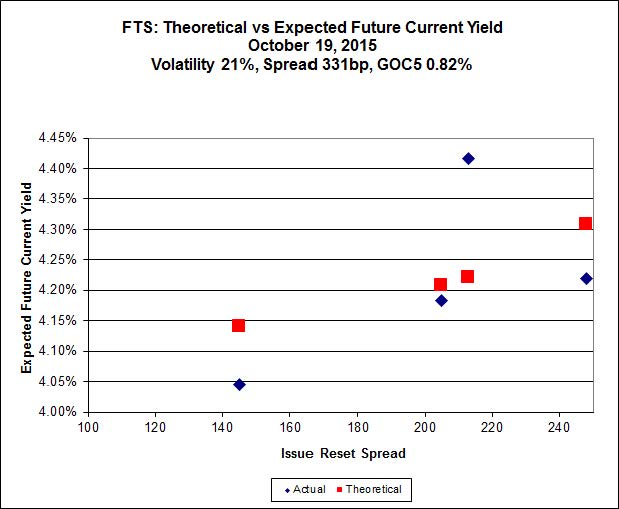

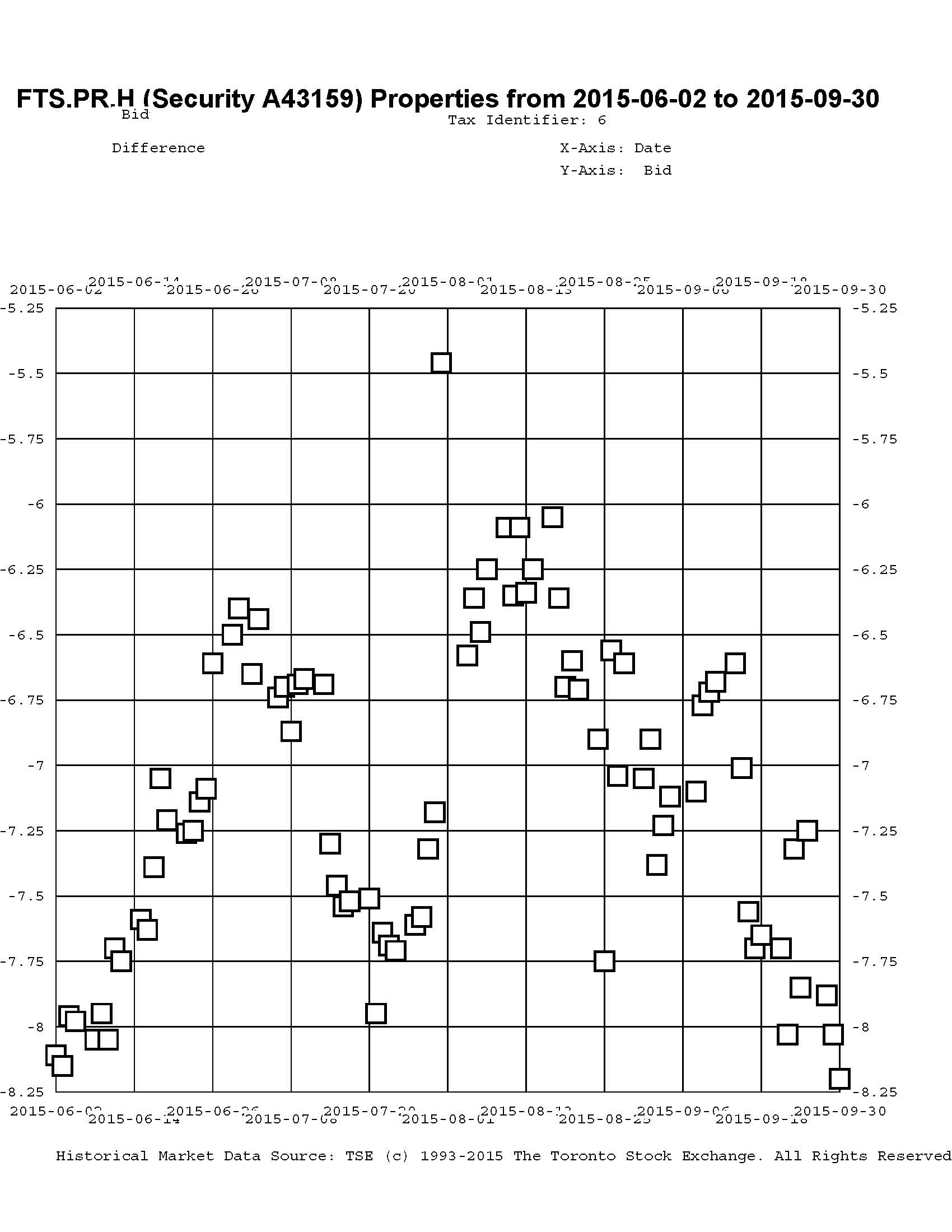

Click for Big

Click for BigImplied Volatility edged up again today to the maximum level I am willing to discuss.

FTS.PR.H, with a spread of +145bp, and bid at 13.70, looks $0.16 expensive and resets 2020-6-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.01 and is $0.42 cheap.

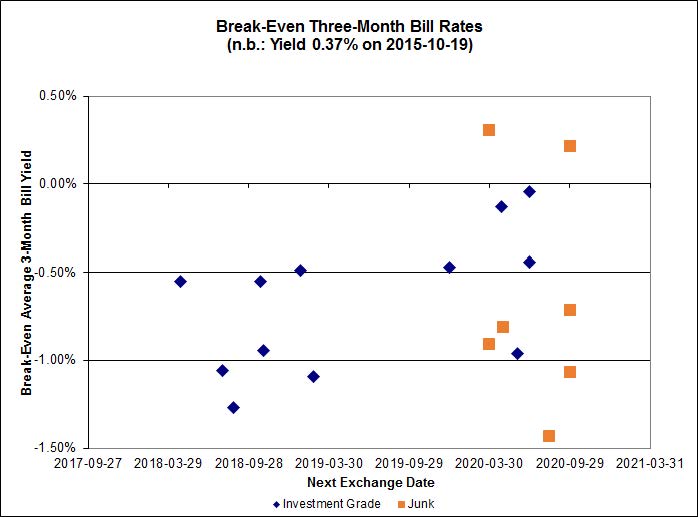

Click for Big

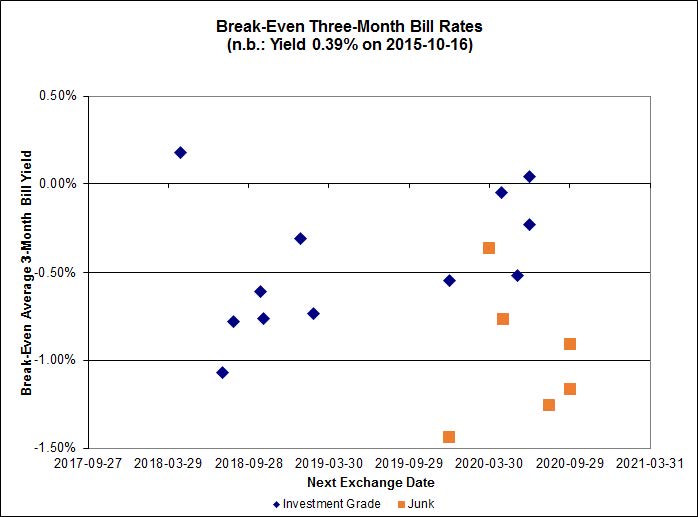

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.51%, with two outliers above 0.00% and none below -2.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -0.82% and other issues averaging -0.07%. There are three junk outliers above 0.00%.

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.3297 % |

1,584.2 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.3297 % |

2,769.8 |

| Floater |

4.69 % |

4.72 % |

63,238 |

16.02 |

3 |

-0.3297 % |

1,684.1 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.2274 % |

2,760.9 |

| SplitShare |

4.34 % |

5.21 % |

74,179 |

2.99 |

5 |

0.2274 % |

3,235.6 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.2274 % |

2,524.6 |

| Perpetual-Premium |

6.00 % |

6.04 % |

61,757 |

13.87 |

5 |

-0.1552 % |

2,426.2 |

| Perpetual-Discount |

5.81 % |

5.90 % |

80,200 |

14.06 |

33 |

-0.5894 % |

2,451.3 |

| FixedReset |

5.49 % |

4.97 % |

197,178 |

14.78 |

76 |

-0.5931 % |

1,856.6 |

| Deemed-Retractible |

5.40 % |

6.16 % |

103,151 |

5.45 |

33 |

-0.7991 % |

2,466.7 |

| FloatingReset |

2.67 % |

4.94 % |

68,311 |

5.81 |

9 |

-0.5949 % |

2,035.9 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| HSB.PR.C |

Deemed-Retractible |

-7.44 % |

Not real. The issue traded a whopping 511 shares today in a range of 24.51-71. The five trades (four of which were timestamped on and after 3:58) so exhausted the market maker that the issue closed at 22.88-24.72 (!). I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.88

Bid-YTW : 6.86 % |

| TRP.PR.A |

FixedReset |

-4.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 14.15

Evaluated at bid price : 14.15

Bid-YTW : 5.17 % |

| BAM.PR.X |

FixedReset |

-3.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 13.52

Evaluated at bid price : 13.52

Bid-YTW : 5.31 % |

| BNS.PR.Q |

FixedReset |

-3.17 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.60

Bid-YTW : 4.88 % |

| RY.PR.H |

FixedReset |

-2.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.23

Evaluated at bid price : 17.23

Bid-YTW : 4.84 % |

| MFC.PR.N |

FixedReset |

-2.78 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.77

Bid-YTW : 8.87 % |

| PWF.PR.T |

FixedReset |

-2.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.35

Evaluated at bid price : 18.35

Bid-YTW : 4.65 % |

| IFC.PR.A |

FixedReset |

-2.53 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.65

Bid-YTW : 10.17 % |

| TRP.PR.F |

FloatingReset |

-2.34 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 12.51

Evaluated at bid price : 12.51

Bid-YTW : 4.65 % |

| BNS.PR.R |

FixedReset |

-2.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.15

Bid-YTW : 4.70 % |

| BAM.PR.R |

FixedReset |

-2.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 14.60

Evaluated at bid price : 14.60

Bid-YTW : 5.60 % |

| BAM.PR.T |

FixedReset |

-2.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 15.30

Evaluated at bid price : 15.30

Bid-YTW : 5.44 % |

| BMO.PR.T |

FixedReset |

-2.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.85

Evaluated at bid price : 16.85

Bid-YTW : 4.93 % |

| PWF.PR.P |

FixedReset |

-2.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 13.48

Evaluated at bid price : 13.48

Bid-YTW : 4.59 % |

| RY.PR.Z |

FixedReset |

-2.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.45

Evaluated at bid price : 17.45

Bid-YTW : 4.74 % |

| BNS.PR.P |

FixedReset |

-1.82 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.20

Bid-YTW : 4.41 % |

| FTS.PR.K |

FixedReset |

-1.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.21

Evaluated at bid price : 16.21

Bid-YTW : 4.87 % |

| BMO.PR.S |

FixedReset |

-1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.69

Evaluated at bid price : 17.69

Bid-YTW : 4.81 % |

| W.PR.H |

Perpetual-Discount |

-1.73 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 22.44

Evaluated at bid price : 22.70

Bid-YTW : 6.09 % |

| GWO.PR.Q |

Deemed-Retractible |

-1.68 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.19

Bid-YTW : 6.88 % |

| TD.PF.B |

FixedReset |

-1.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.87

Evaluated at bid price : 16.87

Bid-YTW : 4.86 % |

| TD.PF.A |

FixedReset |

-1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.94

Evaluated at bid price : 16.94

Bid-YTW : 4.85 % |

| CM.PR.O |

FixedReset |

-1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.11

Evaluated at bid price : 17.11

Bid-YTW : 4.89 % |

| CU.PR.E |

Perpetual-Discount |

-1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 21.02

Evaluated at bid price : 21.02

Bid-YTW : 5.92 % |

| BMO.PR.W |

FixedReset |

-1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.65

Evaluated at bid price : 16.65

Bid-YTW : 4.95 % |

| BIP.PR.A |

FixedReset |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 19.30

Evaluated at bid price : 19.30

Bid-YTW : 5.81 % |

| SLF.PR.I |

FixedReset |

-1.49 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.83

Bid-YTW : 8.25 % |

| CU.PR.G |

Perpetual-Discount |

-1.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 19.62

Evaluated at bid price : 19.62

Bid-YTW : 5.82 % |

| FTS.PR.M |

FixedReset |

-1.44 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.80

Evaluated at bid price : 17.80

Bid-YTW : 5.01 % |

| CU.PR.F |

Perpetual-Discount |

-1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 19.60

Evaluated at bid price : 19.60

Bid-YTW : 5.83 % |

| TRP.PR.C |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 11.33

Evaluated at bid price : 11.33

Bid-YTW : 5.33 % |

| BAM.PF.E |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 5.46 % |

| TRP.PR.B |

FixedReset |

-1.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 10.99

Evaluated at bid price : 10.99

Bid-YTW : 4.92 % |

| BAM.PR.Z |

FixedReset |

-1.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.51

Evaluated at bid price : 18.51

Bid-YTW : 5.40 % |

| TD.PF.D |

FixedReset |

-1.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.55

Evaluated at bid price : 18.55

Bid-YTW : 4.92 % |

| GWO.PR.H |

Deemed-Retractible |

-1.33 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.78

Bid-YTW : 7.47 % |

| GWO.PR.P |

Deemed-Retractible |

-1.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.86

Bid-YTW : 6.73 % |

| IFC.PR.C |

FixedReset |

-1.28 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.79

Bid-YTW : 8.14 % |

| MFC.PR.C |

Deemed-Retractible |

-1.23 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.30

Bid-YTW : 8.13 % |

| CU.PR.C |

FixedReset |

-1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.04

Evaluated at bid price : 18.04

Bid-YTW : 4.67 % |

| SLF.PR.D |

Deemed-Retractible |

-1.19 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.10

Bid-YTW : 8.20 % |

| MFC.PR.I |

FixedReset |

-1.19 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.16

Bid-YTW : 7.50 % |

| POW.PR.B |

Perpetual-Discount |

-1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 22.33

Evaluated at bid price : 22.60

Bid-YTW : 5.95 % |

| GWO.PR.M |

Deemed-Retractible |

-1.17 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.51

Bid-YTW : 6.16 % |

| SLF.PR.J |

FloatingReset |

-1.13 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.15

Bid-YTW : 9.66 % |

| SLF.PR.E |

Deemed-Retractible |

-1.13 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.33

Bid-YTW : 8.09 % |

| TD.PF.F |

Perpetual-Discount |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 21.71

Evaluated at bid price : 22.00

Bid-YTW : 5.57 % |

| MFC.PR.B |

Deemed-Retractible |

-1.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.67

Bid-YTW : 8.05 % |

| BAM.PR.M |

Perpetual-Discount |

-1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 19.82

Evaluated at bid price : 19.82

Bid-YTW : 6.05 % |

| SLF.PR.C |

Deemed-Retractible |

-1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.15

Bid-YTW : 8.16 % |

| BNS.PR.B |

FloatingReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.08

Bid-YTW : 4.94 % |

| MFC.PR.J |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.45

Bid-YTW : 7.71 % |

| VNR.PR.A |

FixedReset |

1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.95

Evaluated at bid price : 17.95

Bid-YTW : 5.25 % |

| TRP.PR.G |

FixedReset |

1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.91

Evaluated at bid price : 17.91

Bid-YTW : 5.40 % |

| HSE.PR.E |

FixedReset |

1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 22.16

Evaluated at bid price : 22.75

Bid-YTW : 4.89 % |

| TRP.PR.D |

FixedReset |

1.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.10

Evaluated at bid price : 16.10

Bid-YTW : 5.28 % |

| MFC.PR.H |

FixedReset |

1.99 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.46

Bid-YTW : 6.85 % |

| GWO.PR.N |

FixedReset |

3.69 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.76

Bid-YTW : 9.72 % |

| RY.PR.I |

FixedReset |

4.77 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.85

Bid-YTW : 4.91 % |

| MFC.PR.F |

FixedReset |

5.19 % |

Wow! The issue traded 26,035 shares in a range of 13.37-14.69 and closed at 14.40-69, 218×30. It caught an enormous bid after about 2:30pm.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.40

Bid-YTW : 9.44 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BAM.PR.N |

Perpetual-Discount |

111,699 |

RBC crossed 104,800 at 19.90.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 19.93

Evaluated at bid price : 19.93

Bid-YTW : 6.02 % |

| RY.PR.J |

FixedReset |

99,357 |

RBC crossed blocks of 14,800 shares, 32,400 and 25,000, all at 18.15.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.24

Evaluated at bid price : 18.24

Bid-YTW : 5.01 % |

| RY.PR.M |

FixedReset |

87,709 |

Anonymous crossed 10,900 at 18.20; RBC crossed 52,400 at 17.85.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 17.90

Evaluated at bid price : 17.90

Bid-YTW : 4.98 % |

| GWO.PR.N |

FixedReset |

66,416 |

Scotia crossed 21,100 at 13.55.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.76

Bid-YTW : 9.72 % |

| TD.PF.D |

FixedReset |

65,381 |

Desjardins crossed 40,000 at 18.68.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 18.55

Evaluated at bid price : 18.55

Bid-YTW : 4.92 % |

| MFC.PR.H |

FixedReset |

57,353 |

Nesbitt crossed 48,200 at 20.33.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.46

Bid-YTW : 6.85 % |

| There were 70 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| HSB.PR.C |

Deemed-Retractible |

Quote: 22.88 – 24.72

Spot Rate : 1.8400

Average : 1.0510

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.88

Bid-YTW : 6.86 % |

| TRP.PR.E |

FixedReset |

Quote: 16.50 – 17.95

Spot Rate : 1.4500

Average : 0.9180

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 16.50

Evaluated at bid price : 16.50

Bid-YTW : 5.24 % |

| MFC.PR.K |

FixedReset |

Quote: 15.86 – 16.60

Spot Rate : 0.7400

Average : 0.5186

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.86

Bid-YTW : 9.43 % |

| W.PR.J |

Perpetual-Discount |

Quote: 23.10 – 23.70

Spot Rate : 0.6000

Average : 0.3896

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 22.82

Evaluated at bid price : 23.10

Bid-YTW : 6.09 % |

| POW.PR.G |

Perpetual-Discount |

Quote: 23.50 – 24.19

Spot Rate : 0.6900

Average : 0.4919

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-10-14

Maturity Price : 23.12

Evaluated at bid price : 23.50

Bid-YTW : 5.98 % |

| TD.PR.S |

FixedReset |

Quote: 23.00 – 23.49

Spot Rate : 0.4900

Average : 0.3163

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.00

Bid-YTW : 4.34 % |