The OECD is not impressed with Canada’s growth:

In the quarterly update of its global outlook, the Organization for Economic Co-operation and Development cut its forecast for Canadian gross domestic product growth to 1.1 per cent this year, down from 1.5 per cent in its June outlook. For 2016, it reduced its GDP growth projection to 2.1 per cent from 2.3 per cent.

The OECD report underlines Canada’s underperformance this year relative to other major world economies, even as its neighbour and biggest trading partner, the United States, continues to gain momentum. The OECD upgraded its projection for U.S. GDP growth this year to 2.4 per cent, up from 2 per cent in its June report. Among the G7 major industrialized countries, Canada’s forecast 2015 growth is in the middle of the pack, ahead of Japan (0.6 per cent), Italy (0.7 per cent) and France (1.0 per cent). But Canada’s slowdown this year is the worst in G7, and the cut in its OECD forecast is the largest in the group.

Meanwhile, US inflation is moderate:

Prices paid by American households declined in August as cheaper gasoline helped keep inflation below the objective of Federal Reserve policy makers.

The consumer-price index fell 0.1 percent, the first decrease since January, after a 0.1 percent gain in July, Labor Department figures showed Wednesday. The so-called core measure, which strips out often-volatile fuel and food costs, rose 0.1 percent for a second month. Goods prices declined, while services barely rose.

…

The consumer price gauge increased 0.2 percent in the 12 months ended in August, the same as in July.The core CPI measure, which excludes volatile food and fuel costs, rose 1.8 percent from August 2014, matching the prior month’s year-over-year gain.

In the comments to yesterday’s post, Assiduous Reader gimlimike brings to my attention a perpetual Dutch bond issued in 1648. I love perpetuals! If I’m reading the Dutch in the photograph correctly, the bond pays 25 guilders annually on an initial investment of 1,000 guilders, or 2.5%.

A similar bond was auctioned by Christies in 2000 with some interesting historical notes:

The Lekdijk Bovendams was incorporated in 1971 into a larger municipal organization, the Waterschap Kromme Rijn, which took over the payment of annual interest on the handful of extant original bonds. According to a 1978 report of the Waterschap’s Secretary, the corporation had issued a total of 48 bonds in the 17th and 18th century; their denominations ranged from 400 to 8,000 Guilders. Only 4 bonds were issued in the amount of 1200 Guilders. In 1978, only 22 of the 48 issued were still traceable (most in the hands of banks and other institutions, a few in private hands). According to a recent communication from C. Vanema, Archivist of the Streekarchief “Rijnstreek,” where the papers of the Waterschaap are deposited, there are today only five of these early bonds still active. Only one, issued in 1624 and owned since 1938 by the New York Stock Exchange, pre-dates the present bond, and only two of bonds issued in the 17th century are still active.

The good effects of centuries of such care may be observed via Google Maps. Given that one Guilder is 0.453780 Euros, the bond pays 11.34 Euros per year; given that Yale paid 24,000 Euros for it in 2003, the yield is 0.05% and the duration is therefore 2,000.

Yet another candidate has been dropped from the ballot over past indiscretions, and rewarded for his willingness to serve by being publicly vilified. At some point, we’re going to have to learn that not everybody has been a saint since birth; and that those who have been may not necessarily make the best legislators. But it makes us feel better about ourselves to scapegoat those unlucky enough to have been caught … meanwhile, I will continue to quite adequately represented provincially by Cheri DiNovo, who doubtless wouldn’t even be called for an interview in these puritanical times.

It was a negative day for the Canadian preferred share market, with PerpetualDiscounts off 5bp, FixedResets losing 25bp and DeemedRetractibles down 9bp. The Performance Highlights table is dominated by losing FixedResets, mostly of the low-spread variety. Volume was well below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

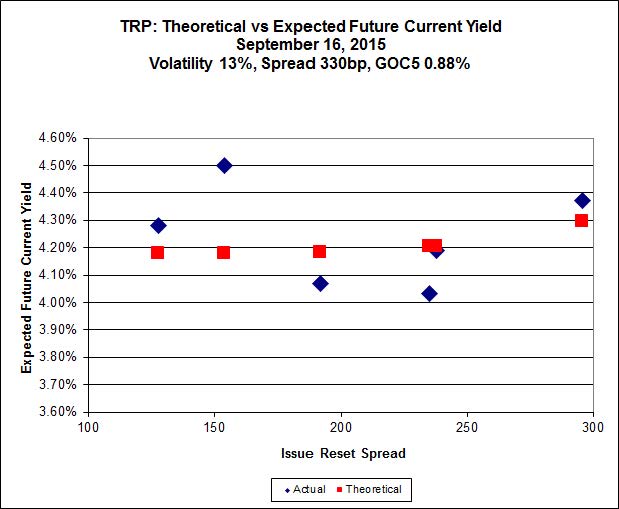

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 20.02 to be $0.89 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.02 cheap at its bid price of 13.45.

Click for Big

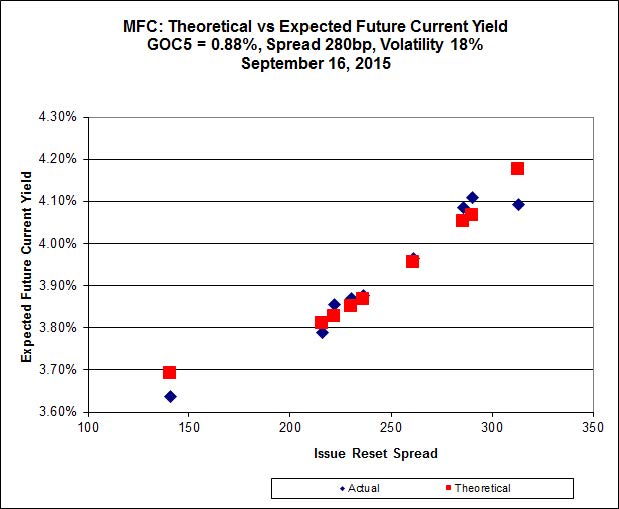

Another good fit today for MFC, with Implied Volatility falling a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.49 to be 0.49 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 23.00 to be 0.23 cheap.

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.80 to be $1.48 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.33 and appears to be $0.95 rich.

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 21.89, looks $0.41 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.73 and is $0.52 cheap.

Click for Big

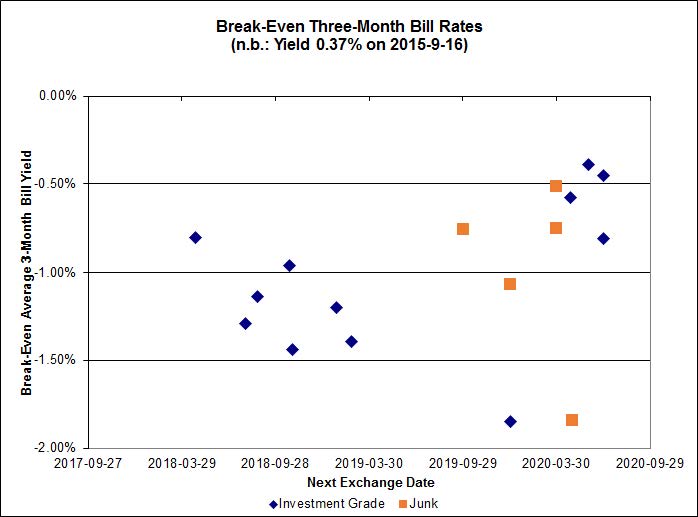

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.03%, with no outliers. The distribution has become bimodal again, with bank NVCC non-compliant issues averaging -1.17% and other issues averaging -0.82%. There are no junk outliers below -2.00%, but one above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1260 % | 1,665.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1260 % | 2,911.8 |

| Floater | 4.46 % | 4.46 % | 57,556 | 16.52 | 3 | 0.1260 % | 1,770.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0135 % | 2,783.2 |

| SplitShare | 4.62 % | 4.99 % | 62,832 | 3.07 | 3 | 0.0135 % | 3,261.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0135 % | 2,544.9 |

| Perpetual-Premium | 5.71 % | 2.47 % | 54,398 | 0.08 | 8 | 0.0494 % | 2,494.0 |

| Perpetual-Discount | 5.45 % | 5.55 % | 69,525 | 14.53 | 30 | -0.0504 % | 2,599.5 |

| FixedReset | 4.73 % | 4.11 % | 180,377 | 16.10 | 74 | -0.2528 % | 2,153.6 |

| Deemed-Retractible | 5.14 % | 4.76 % | 94,987 | 5.50 | 33 | -0.0931 % | 2,586.9 |

| FloatingReset | 2.47 % | 3.97 % | 50,398 | 5.91 | 9 | -0.1851 % | 2,157.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| FTS.PR.H | FixedReset | -3.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 14.61 Evaluated at bid price : 14.61 Bid-YTW : 3.93 % |

| SLF.PR.G | FixedReset | -3.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.45 Bid-YTW : 8.14 % |

| FTS.PR.K | FixedReset | -2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 4.00 % |

| SLF.PR.H | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.62 Bid-YTW : 7.49 % |

| TRP.PR.F | FloatingReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 14.36 Evaluated at bid price : 14.36 Bid-YTW : 3.97 % |

| IFC.PR.C | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 6.22 % |

| BMO.PR.Y | FixedReset | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 22.34 Evaluated at bid price : 23.10 Bid-YTW : 3.87 % |

| BNS.PR.Q | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.63 % |

| W.PR.H | Perpetual-Discount | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 23.59 Evaluated at bid price : 23.86 Bid-YTW : 5.86 % |

| BNS.PR.R | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.64 Bid-YTW : 3.65 % |

| TD.PF.A | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 21.24 Evaluated at bid price : 21.24 Bid-YTW : 3.80 % |

| BMO.PR.T | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 3.79 % |

| TD.PR.S | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 3.27 % |

| FTS.PR.M | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 21.59 Evaluated at bid price : 21.89 Bid-YTW : 3.91 % |

| VNR.PR.A | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 20.21 Evaluated at bid price : 20.21 Bid-YTW : 4.60 % |

| SLF.PR.J | FloatingReset | 3.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.74 Bid-YTW : 8.97 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.E | FixedReset | 31,255 | Scotia crossed 24,000 at 24.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 22.85 Evaluated at bid price : 24.20 Bid-YTW : 3.71 % |

| BAM.PR.B | Floater | 26,982 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-16 Maturity Price : 10.71 Evaluated at bid price : 10.71 Bid-YTW : 4.41 % |

| MFC.PR.J | FixedReset | 23,798 | RBC crossed 21,000 at 22.04. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 5.20 % |

| BNS.PR.Q | FixedReset | 22,175 | RBC crossed 20,300 at 24.32. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 3.63 % |

| BNS.PR.Y | FixedReset | 21,745 | Desjardins crossed 18,200 at 21.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.72 Bid-YTW : 4.22 % |

| PVS.PR.D | SplitShare | 21,130 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 5.09 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.K | FixedReset | Quote: 19.01 – 19.59 Spot Rate : 0.5800 Average : 0.4029 YTW SCENARIO |

| BMO.PR.Y | FixedReset | Quote: 23.10 – 23.55 Spot Rate : 0.4500 Average : 0.2895 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 23.19 – 23.60 Spot Rate : 0.4100 Average : 0.2640 YTW SCENARIO |

| BNS.PR.R | FixedReset | Quote: 24.64 – 25.00 Spot Rate : 0.3600 Average : 0.2261 YTW SCENARIO |

| TD.PF.D | FixedReset | Quote: 23.40 – 23.79 Spot Rate : 0.3900 Average : 0.2660 YTW SCENARIO |

| TD.PF.A | FixedReset | Quote: 21.24 – 21.64 Spot Rate : 0.4000 Average : 0.2827 YTW SCENARIO |