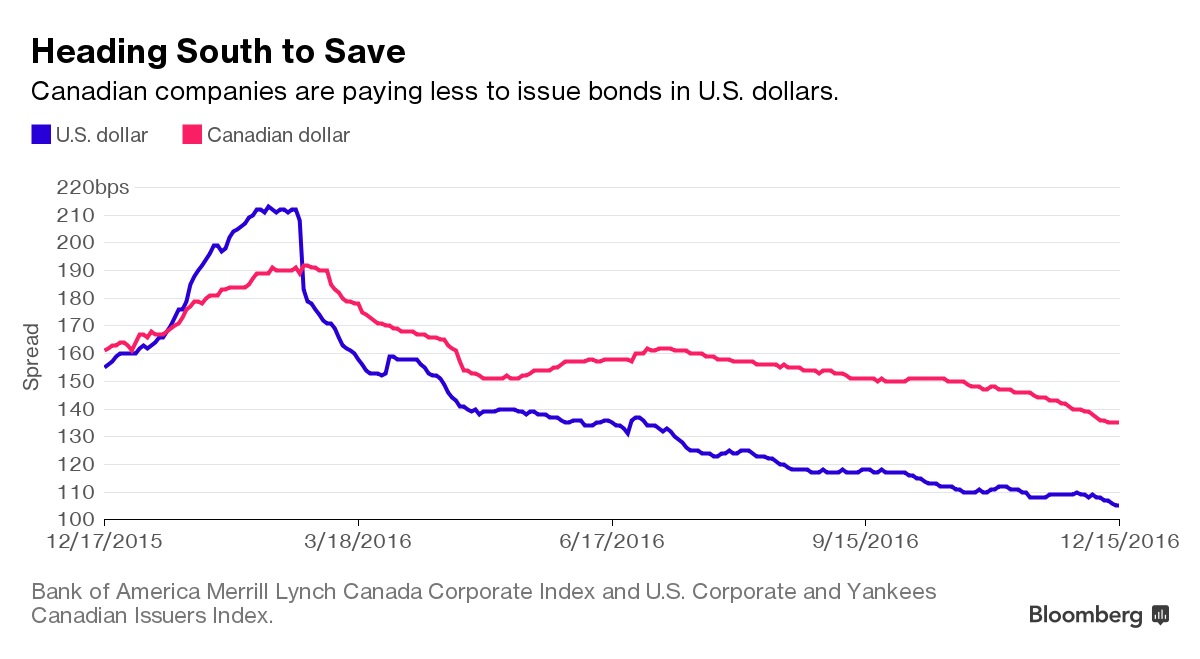

There’s a lot of Canadian bond issuance south of the border:

Canadian companies have issued about $69 billion of debt in U.S. markets this year, up 12 percent from a year ago. That compares with about C$93 billion in the domestic market, a similar amount — $70 billion — when adjusted for currency, and a 3 percent decline from 2015. The move south is being driven by the lure of lower borrowing costs in America’s far larger market, where the high-quality debt of Canadian companies is being lapped up.

The downside for Canadian investors is that deals done south of the border are frequently sold to U.S. investors first. Canadians must wait until those U.S. bond buyers start to sell their notes in the secondary market, which can mean losing out when prices of newly issued bonds rise. Companies meanwhile are chasing the best terms, regardless of geography.

Click for Big

It would be most interesting to learn just how much of this effect was due to the crowding out of Canadian investment capital by our bloated banking sector.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0222 % | 1,802.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0222 % | 3,293.5 |

| Floater | 4.20 % | 4.25 % | 55,800 | 16.92 | 4 | -0.0222 % | 1,898.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0330 % | 2,929.8 |

| SplitShare | 4.82 % | 4.68 % | 62,895 | 4.28 | 6 | -0.0330 % | 3,498.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0330 % | 2,729.9 |

| Perpetual-Premium | 5.48 % | 5.55 % | 88,075 | 14.40 | 23 | -0.3622 % | 2,641.0 |

| Perpetual-Discount | 5.53 % | 5.53 % | 103,495 | 14.54 | 15 | -0.2282 % | 2,720.1 |

| FixedReset | 4.78 % | 4.67 % | 241,261 | 6.75 | 96 | -0.1512 % | 2,139.1 |

| Deemed-Retractible | 5.19 % | 4.74 % | 142,914 | 4.54 | 32 | -0.2415 % | 2,742.1 |

| FloatingReset | 2.84 % | 3.97 % | 45,699 | 4.79 | 12 | -0.3220 % | 2,309.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CU.PR.C | FixedReset | -2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 19.74 Evaluated at bid price : 19.74 Bid-YTW : 4.57 % |

| TRP.PR.F | FloatingReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 15.05 Evaluated at bid price : 15.05 Bid-YTW : 3.98 % |

| BMO.PR.S | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 19.57 Evaluated at bid price : 19.57 Bid-YTW : 4.60 % |

| CCS.PR.C | Deemed-Retractible | -1.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 6.63 % |

| BMO.PR.Y | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 4.58 % |

| SLF.PR.H | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.16 Bid-YTW : 8.45 % |

| BAM.PR.X | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 5.06 % |

| SLF.PR.J | FloatingReset | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.91 % |

| MFC.PR.F | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.03 Bid-YTW : 10.53 % |

| RY.PR.O | Perpetual-Premium | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 23.66 Evaluated at bid price : 24.02 Bid-YTW : 5.13 % |

| BMO.PR.T | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 4.60 % |

| BMO.PR.Z | Perpetual-Premium | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 24.15 Evaluated at bid price : 24.55 Bid-YTW : 5.12 % |

| BAM.PR.N | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 20.67 Evaluated at bid price : 20.67 Bid-YTW : 5.78 % |

| MFC.PR.O | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 26.31 Bid-YTW : 4.34 % |

| MFC.PR.C | Deemed-Retractible | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.23 Bid-YTW : 7.01 % |

| TRP.PR.H | FloatingReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 11.65 Evaluated at bid price : 11.65 Bid-YTW : 3.77 % |

| BAM.PR.R | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 16.79 Evaluated at bid price : 16.79 Bid-YTW : 5.02 % |

| BNS.PR.Z | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.88 Bid-YTW : 6.02 % |

| BMO.PR.Q | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.57 Bid-YTW : 5.96 % |

| PWF.PR.T | FixedReset | 2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 20.57 Evaluated at bid price : 20.57 Bid-YTW : 4.46 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.K | FixedReset | 127,256 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.17 Bid-YTW : 4.87 % |

| TD.PF.H | FixedReset | 89,843 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.54 Bid-YTW : 4.56 % |

| BAM.PF.I | FixedReset | 87,694 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 4.70 % |

| TD.PF.B | FixedReset | 82,319 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 4.63 % |

| RY.PR.H | FixedReset | 79,167 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-12-20 Maturity Price : 19.16 Evaluated at bid price : 19.16 Bid-YTW : 4.61 % |

| MFC.PR.R | FixedReset | 76,860 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-03-19 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 4.98 % |

| There were 83 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.F | FloatingReset | Quote: 15.05 – 15.38 Spot Rate : 0.3300 Average : 0.2168 YTW SCENARIO |

| BAM.PR.R | FixedReset | Quote: 16.79 – 17.22 Spot Rate : 0.4300 Average : 0.3198 YTW SCENARIO |

| SLF.PR.B | Deemed-Retractible | Quote: 22.38 – 22.62 Spot Rate : 0.2400 Average : 0.1552 YTW SCENARIO |

| POW.PR.G | Perpetual-Premium | Quote: 25.00 – 25.30 Spot Rate : 0.3000 Average : 0.2178 YTW SCENARIO |

| BNS.PR.D | FloatingReset | Quote: 19.80 – 20.09 Spot Rate : 0.2900 Average : 0.2198 YTW SCENARIO |

| BMO.PR.Y | FixedReset | Quote: 21.30 – 21.54 Spot Rate : 0.2400 Average : 0.1748 YTW SCENARIO |

“Canadians must wait until those U.S. bond buyers start to sell their notes in the secondary market”

But as retail investors, we can’t access bonds in Canada either, other than in the secondary market. PLEASE correct me if I am wrong about this. I have been searching for a way to access new issue bonds for the past few years, but I gave been unsuccessful.

I have been searching for a way to access new issue bonds for the past few years, but I gave been unsuccessful.

Most discount brokers offer a small selection of new issues to their clients; full-service brokers offer more.

However, this isn’t a business the brokers really like doing, because the commissions aren’t very high.

I have beenwith a full service broker for 2 years. He has never told me about a new issue bond that I couldn’t get from my discount broker. And all the ‘new’ issues I have seen in the past year (4) have been provincial reissues. Are there no alternatives?

Which brokerage house? How much are you willing to invest in a single new issue? What has your guy told you when you’ve complained?

TD

We never spoke about minimum purchase amount

He said “sorry, but that’s all we have.”

The best full-service broker for new issues is RBC-Dominion.