Pembina Pipeline Corporation has announced:

that it has closed its previously announced public offering of cumulative redeemable minimum rate reset class A preferred shares, Series 21 (the “Series 21 Preferred Shares”) for aggregate gross proceeds of $400 million (the “Offering”).

The Offering was announced on November 28, 2017 when Pembina entered into an agreement with a syndicate of underwriters co-led by RBC Capital Markets, CIBC World Markets and Scotiabank. A total of 16,000,000 Series 21 Preferred Shares, which includes 4,000,000 Series 21 Preferred Shares issued pursuant to the exercise of the underwriters’ option, were sold under the Offering.

The Company intends to use the net proceeds from the Offering to reduce indebtedness of the Company under its credit facilities. The indebtedness of the Company under the credit facilities was incurred in the normal course of business to fund the Company’s capital program, and to fund a portion of the cash consideration payable to former common shareholders of Veresen Inc. (“Veresen”) pursuant to the plan of arrangement with Veresen which closed on October 2, 2017.

The Series 21 Preferred Shares will begin trading on the Toronto Stock Exchange today under the symbol [redacted].

Dividends on the Series 21 Preferred Shares are expected to be $1.225 per share annually, payable quarterly on the 1st day of March, June, September and December, as and when declared by the Board of Directors of Pembina, for the initial fixed rate period to but excluding March 1, 2023. The first dividend, if declared, will be payable March 1, 2018, in the amount of $0.2819 per share.

I have redacted the ticker symbol indicated in the press release because it is inaccurate and would otherwise lead to alarms, confusion and mystifying search results for Assiduous Readers. I must admit, I haven’t seen that kind of error before!

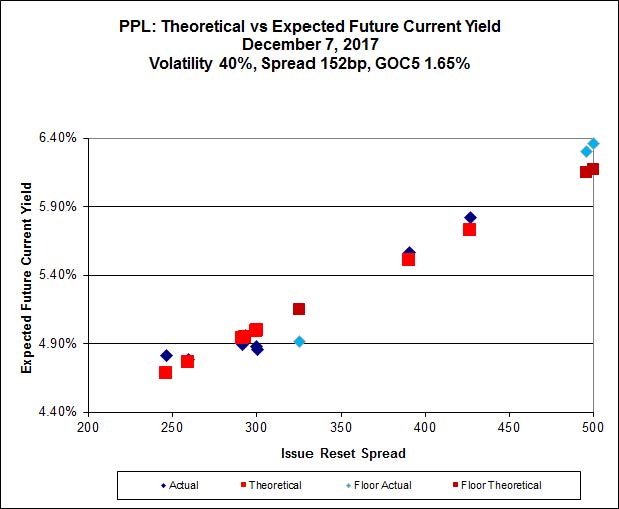

PPL.PF.A is a FixedReset 4.90%+326M490 announced 2017-11-28. It will be tracked by HIMIPref™, but has been relegated to the Scraps subindex on credit concerns.

The issue traded 1,402,627 shares today in a range of 24.85-02 before closing at 24.99-00. Vital statistics are:

| PPL.PF.A | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-07 Maturity Price : 23.14 Evaluated at bid price : 24.99 Bid-YTW : 4.88 % |

It looks expensive to me! According to Implied Volatility analysis:

Click for Big

With the parameters shown, the theoretical value of the new issue is 23.84 – the decline of the market since announcement date has really hurt the valuation of this issue; fair value is now more than fifty cents less than it was then. Critics will be quick to point out that in this calculation there is zero value assigned to the minimum rate guarantee … but I’d say that’s about right!

These straw-men critics I have created will also have to explain why the two other Floor-Rate FixedResets (PPL.PR.K and PPL.PR.M) are cheap according to this analysis. It can be done – just assume that spreads on those two issues are so large that the floor doesn’t matter any more – but one way or another, it’s another example of the asymmetry of returns on issues priced near par working against the investor.

Note also that the Implied Volatility on this series is extraordinarily high, which leads to an expectation that the curve will flatten in the future. As PPL.PF.A is nearer the ‘low spread’ end of the curve than it is to the ‘high spread’ end, such a flattening should lead to underperformance by the issue.

[…] was issued a FixedReset 4.90%+326M490 that commenced trading 2017-12-7 after being announced 2017-11-28. It is tracked by HIMIPref™, but has been relegated to the […]