Manulife Financial Corporation has announced:

that it has completed its offering of 10 million Non-cumulative Rate Reset Class 1 Shares Series 25 (the “Series 25 Preferred Shares”) at a price of $25 per share to raise gross proceeds of $250 million.

The offering was underwritten by a syndicate of investment dealers co-led by RBC Capital Markets, Scotiabank and TD Securities. The Series 25 Preferred Shares commence trading on the Toronto Stock Exchange today under the ticker symbol MFC.PR.Q.

The Series 25 Preferred Shares were issued under a prospectus supplement dated February 12, 2018 to Manulife’s short form base shelf prospectus dated December 15, 2017.

MFC.PR.Q is a FixedReset, 4.70%+255, announced 2018-2-12. It will be tracked by HIMIPref™ and has been assigned to the FixedReset sub-index.

As this issue is not NVCC compliant and it is an insurance issue, it is analyzed as having a Deemed Retraction, effective 2025-1-31 (this date may change in the future).

The issue traded 798,808 shares today in a range of 24.70-94 before closing at 24.90-94. Vital statistics are:

| MFC.PR.Q | FixedReset | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 4.78 % |

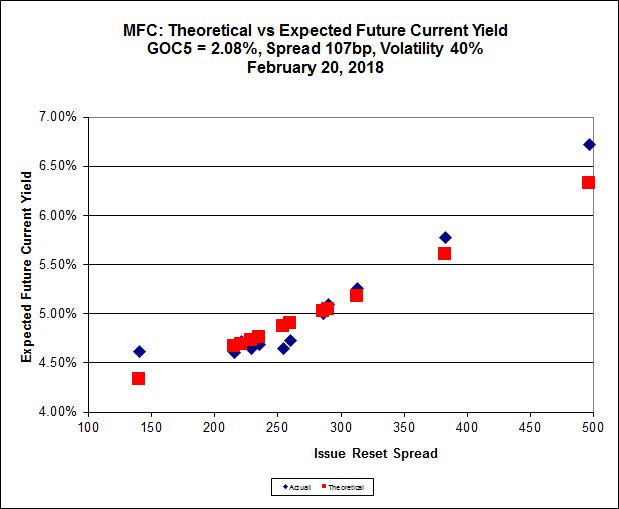

This issue looks quite expensive to me, according to Implied Volatility Analysis:

Click for Big

We see in this chart many of the same features we saw when reviewing the recent BIP.PR.E, BEP.PR.M, CM.PR.S and NA.PR.E: the curve is very steep, with Implied Volatility equal to 40% (a ridiculously large figure).

The ludicrously high figure of Implied Volatility is something I take to mean that the underlying assumption of the Black-Scholes model, that of no directionality of prices, is not accepted by the market; the market seems to be taking the view that since things seem rosy now, they will always be rosy and everything will trade near par in the future.

If the MFC series were an isolated example of this behaviour, I would grin smugly to myself and declare that the implied directionality was a strong indication that the market is starting to take my predictions of Deemed Retraction seriously; but it’s not isolated. In addition, if the market was accounting for future redemption, I would expect the projected yields-to-deemed-retraction to be lower.

In the absence of DeemedRetraction, I balk at ascribing a 100% probability to the ‘all issues will be called, or at least exhibit price stability’ hypothesis. There may still be a few old geezers amongst the Assiduous Readers of this blog who can still (faintly) remember the Great Bear Market of 2014-16, in which quite a few similar assumptions made earlier turned out to be slightly inaccurate. The extra cushion implied by an Issue Reset Spread that is well over the market spread is worth something, even if nothing gets called.

All told, though, I have no hesitation in slapping an ‘Expensive’ label on this issue – according to the Implied Volatility analysis shown above, the theoretical price of the new issue without any accounting for the potential of a DeemedRetraction is 23.76. The two near-par issues, MFC.PR.Q and MFC.PR.J, form a noticeably expensive pothole in the plotted curve.

[…] was issued as a FixedReset, 4.70%+255, that commenced trading 2018-2-20 after being announced 2018-2-12. It is tracked by HIMIPref™ and has been assigned to the […]