Befitting the date, today saw the FOMC spring into action:

Information received since the Federal Open Market Committee met in January indicates that the labor market has continued to strengthen and that economic activity has been rising at a moderate rate. Job gains have been strong in recent months, and the unemployment rate has stayed low. Recent data suggest that growth rates of household spending and business fixed investment have moderated from their strong fourth-quarter readings. On a 12-month basis, both overall inflation and inflation for items other than food and energy have continued to run below 2 percent. Market-based measures of inflation compensation have increased in recent months but remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The economic outlook has strengthened in recent months. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to move up in coming months and to stabilize around the Committee’s 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1-1/2 to 1-3/4 percent.

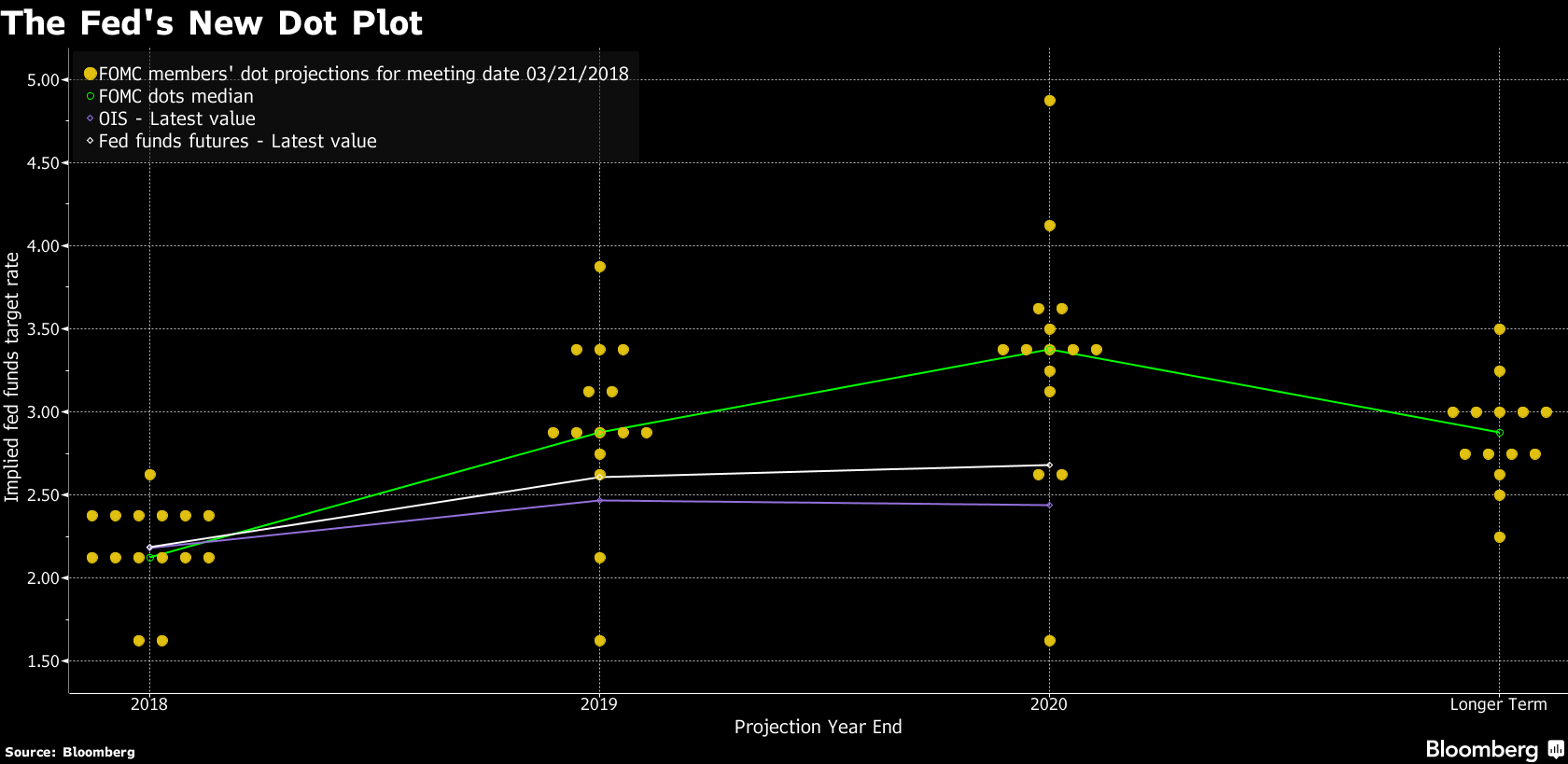

More interesting was the more hawkish dot-plot:

Federal Reserve officials, meeting for the first time under Chairman Jerome Powell, raised the benchmark lending rate a quarter-point and forecast a steeper path of hikes in 2019 and 2020, citing an improving economic outlook. Policy makers continued to project a total of three increases this year.

…

The upward revision in their rate path suggests Fed officials are looking through soft first-quarter economic reports and expect a lift this year and next from tax cuts passed by Republicans in December. Financial conditions have tightened since late January as investors look for signs that the central bank might raise rates at a faster pace, while forecasters predict stronger U.S. growth and tight labor markets.

…

In the forecasts, U.S. central bankers projected a median federal funds rate of 2.9 percent by the end of 2019, implying three rate increases next year, compared with two 2019 moves seen in the last round of forecasts in December. They saw rates at 3.4 percent in 2020, up from 3.1 percent in December, according to the median estimate.The S&P 500 Index of U.S. stocks stayed higher after the release, while the yield on 10-year U.S. Treasury notes rose slightly, to 2.91 percent. The Bloomberg Dollar Spot Index was lower.

In another change to the statement, the Fed said inflation on an annual basis is “expected to move up in coming months,” after saying “move up this year” in the January statement. Price gains are still expected to stabilize around the Fed’s 2 percent target over the medium term, the FOMC said.

Click for big

PerpetualDiscounts now yield 5.46%, equivalent to 7.10% interest at the standard equivalency factor of 1.3x. Long corporates now yield a little under 3.90%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 320bp, a slight (and perhaps spurious) widening from the 315bp reported March 14.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4045 % | 3,079.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4045 % | 5,650.5 |

| Floater | 3.24 % | 3.41 % | 101,943 | 18.75 | 4 | 0.4045 % | 3,256.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0705 % | 3,166.9 |

| SplitShare | 4.69 % | 4.20 % | 56,601 | 3.26 | 5 | 0.0705 % | 3,781.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0705 % | 2,950.8 |

| Perpetual-Premium | 5.60 % | 2.38 % | 77,851 | 0.08 | 11 | -0.1571 % | 2,841.2 |

| Perpetual-Discount | 5.35 % | 5.46 % | 85,467 | 14.64 | 23 | -0.2230 % | 2,936.2 |

| FixedReset | 4.29 % | 4.62 % | 175,590 | 5.88 | 104 | 0.0133 % | 2,510.8 |

| Deemed-Retractible | 5.18 % | 5.76 % | 91,664 | 5.72 | 28 | -0.0847 % | 2,916.0 |

| FloatingReset | 2.91 % | 3.01 % | 35,394 | 3.65 | 10 | 0.7941 % | 2,758.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| W.PR.M | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-15 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 4.67 % |

| CU.PR.C | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 21.50 Evaluated at bid price : 21.77 Bid-YTW : 4.80 % |

| BAM.PR.M | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 5.70 % |

| SLF.PR.J | FloatingReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.82 Bid-YTW : 6.18 % |

| HSE.PR.A | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 17.75 Evaluated at bid price : 17.75 Bid-YTW : 4.94 % |

| PWF.PR.P | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.33 % |

| GWO.PR.M | Deemed-Retractible | 1.29 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-30 Maturity Price : 25.25 Evaluated at bid price : 25.83 Bid-YTW : -15.92 % |

| PWF.PR.Q | FloatingReset | 9.57 % | A reversal of yesterday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 21.42 Evaluated at bid price : 21.76 Bid-YTW : 3.02 % |

| BAM.PR.T | FixedReset | 29.98 % | A reversal of yesterday‘s nonsense. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 4.94 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.K | Floater | 104,712 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 17.64 Evaluated at bid price : 17.64 Bid-YTW : 3.42 % |

| TD.PF.G | FixedReset | 68,469 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 26.52 Bid-YTW : 3.69 % |

| TRP.PR.J | FixedReset | 67,752 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-31 Maturity Price : 25.00 Evaluated at bid price : 26.20 Bid-YTW : 4.03 % |

| CM.PR.Q | FixedReset | 61,400 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 23.21 Evaluated at bid price : 24.28 Bid-YTW : 4.73 % |

| TD.PF.B | FixedReset | 57,682 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-21 Maturity Price : 22.72 Evaluated at bid price : 23.17 Bid-YTW : 4.58 % |

| MFC.PR.G | FixedReset | 56,528 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-12-19 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 4.62 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| W.PR.M | FixedReset | Quote: 25.69 – 26.05 Spot Rate : 0.3600 Average : 0.2086 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 22.83 – 23.16 Spot Rate : 0.3300 Average : 0.2036 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 23.50 – 23.78 Spot Rate : 0.2800 Average : 0.1868 YTW SCENARIO |

| IGM.PR.B | Perpetual-Premium | Quote: 25.55 – 25.80 Spot Rate : 0.2500 Average : 0.1599 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 24.40 – 24.62 Spot Rate : 0.2200 Average : 0.1403 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 24.66 – 24.93 Spot Rate : 0.2700 Average : 0.1932 YTW SCENARIO |