Canadian Imperial Bank of Commerce has announced:

that it has completed the offering of 10 million Non-cumulative Rate Reset Class A Preferred Shares Series 51 (Non-Viability Contingent Capital (NVCC)) (the “Series 51 Shares”) priced at $25.00 per share to raise gross proceeds of $250 million.

The offering was made through a syndicate of underwriters led by CIBC Capital Markets. The Series 51 Shares commence trading on the Toronto Stock Exchange today under the ticker symbol CM.PR.Y.

The Series 51 Shares were issued under a prospectus supplement dated May 27, 2019, to CIBC’s short form base shelf prospectus dated July 11, 2018.

CIBC has designated the Series 51 Shares as eligible to participate in the CIBC Shareholder Investment Plan along with Series 41, 43, 45, 47 and 49. Holders of eligible shares may elect to have dividends on those preferred shares reinvested in common shares if they reside in Canada, or may elect stock dividends if they reside in the U.S. See “CIBC Shareholder Investment Plan” at www.cibc.com for more information.

CM.PR.Y is a FixedReset, 5.15%+362, NVCC, announced May 24. It will be tracked by HIMIPref™ and has been assigned to the FixedReset (Discount) subindex.

The issue traded 1,022,019 shares today in a range of 24.35-65 before closing at 24.37-40. Vital statistics are:

| CM.PR.Y | FixedReset Disc | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2049-06-04 Maturity Price : 22.92 Evaluated at bid price : 24.37 Bid-YTW : 5.10 % |

Given that the PerpetualDiscount index is down 5.64% from its pre-announcement close on May 23, this was actually a pretty good day for the issue!

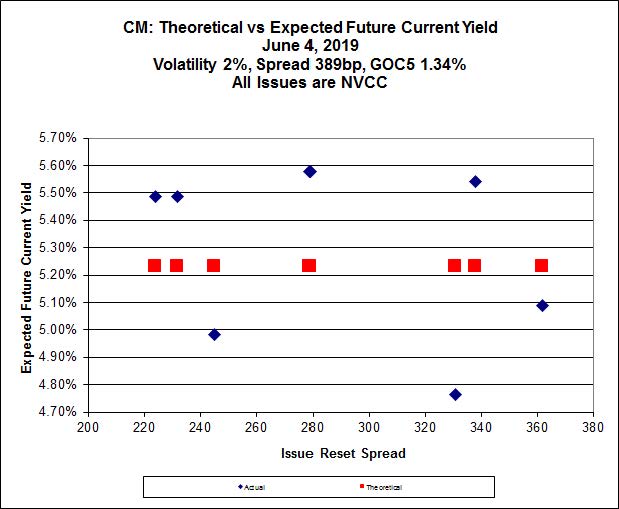

The new issue is somewhat expensive according to Implied Volatility Analysis:

Click for Big

According to this analysis, the fair price of the new issue is 23.71, down from the announcement day fair-value of 24.85, but alert Assiduous Readers will have noticed that the Implied Volatility plot is very peculiar, having three expensive issues and four cheap ones, with nothing in between.

The other two rich issues are:

- CM.PR.S, a FixedReset, 4.50%+245, NVCC-compliant issue that commenced trading 2018-1-18 after being announced 2018-1-10. It is 0.89 rich, being bid at 19.01 compared to a fair value of 18.12.

- CM.PR.T, a FixedReset, 5.20%+331, NVCC-compliant issue that commenced trading 2019-1-22 after being announced 2019-1-14. It is 2.17 rich, being bid at 24.40 compared to a fair value of 22.23. Alert readers will note that is is bid higher than CM.PR.Y despite having an Issue Reset Spread 31bp lower. Sometimes I despair of this market.

The extremely perplexing issue is CM.PR.R, a FixedReset, 4.40%+338, NVCC Compliant issue that commenced trading 2017-6-2 after being announced 2017-5-25. It is bid at 21.30 compared to a fair value of 22.56. Alert readers will note that it is bid much lower than CM.PR.T despite having an Issue Reset Spread 7bp higher.

I confess I don’t know quite what to make of this. It is common – normal, even – for a new issue to remain rich for quite some time, but I am at a loss to explain why CM.PR.S should remain rich after being on the market for sixteen months. CM.PR.R is just silly … but note that its current coupon is low relative to the new issue and it won’t reset until 2022-7-31 … three years, roughly, thirteen coupon payments, but that’s only a total of about $0.60 and doesn’t explain the differential with CM.PR.S anyway.

Fortunately, I don’t have to explain it! All I have to do is avoid buying the new issue and favour other, cheaper, choices for any allocation to CM that I care to make.

Isn’t it a plus that it won’t be resetting anytime soon? I don’t think we have any higher interest rates to look forward to before this year closes.

I was referring to CM.PR.R if it is not clear.

Isn’t it a plus that it [CM.PR.R] won’t be resetting anytime soon? I don’t think we have any higher interest rates to look forward to before this year closes.

Well, the calculations are performed assuming that the same rate is used for all resets of all issues. Once you bring in the question of reset dates, you are first assuming a change (in what direction?) of the long-term equilibrium rate and then you have to map a path towards that equilibrium.

In practical terms, I don’t think it’s a plus, since anything that resets will reset again five years later (assuming it isn’t called).