Assiduous Readers will remember that there was an 14% Conversion from the FixedReset ALA.PR.G to the FloatingReset ALA.PR.H. I had advised readers not to convert, but to continue holding the ALA.PR.G, which have reset to 3.415%.

ALA.PR.H will pay dividends at a rate of 3-Month Canada Treasury Bills plus 306bp, reset quarterly.

The issue was listed today, but didn’t trade – this is largely due to the banks’ hegemony over the Canadian financial system (approved by both securities regulators and the Competition-haha Board) and their total lack of interest in providing competent service to stinking investor scum such as yourselves. These exchanges do not hit client accounts until the day after the company gives effect to them – however, investors can complain to the exchange-owned CDS and the (mostly) bank-owned brokerages about this lackadaisical attitude toward client assets and see how far it gets them.

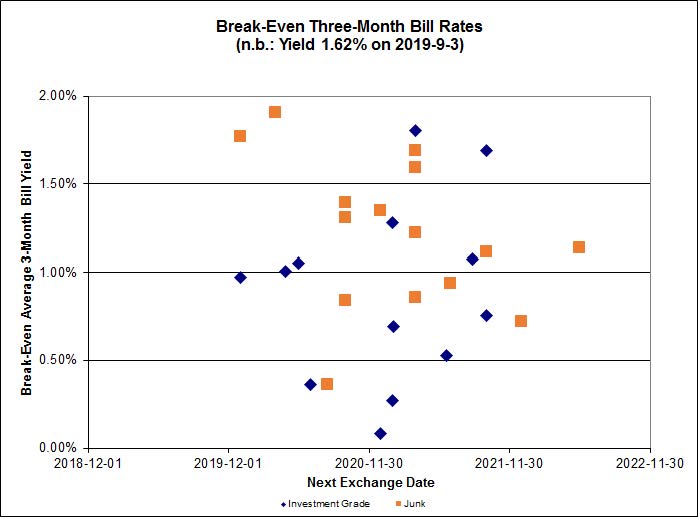

The most logical way to analyze the relative value of ALA.PR.G vs ALA.PR.H through the theory of Preferred Pairs, for which a calculator is available. Briefly, a Strong Pair is defined as a pair of securities that can be interconverted in the future (e.g., ALA.PR.G and the FloatingReset ALA.PR.H). Since they will be interconvertible on this future date, it may be assumed that they will be priced identically on this date (if they aren’t then holders will simply convert en masse to the higher-priced issue). And since they will be priced identically on a given date in the future, any current difference in price must be offset by expectations of an equal and opposite value of dividends to be received in the interim. And since the dividend rate on one element of the pair is both fixed and known, the implied average rate of the other, floating rate, instrument can be determined. Finally, we say, we may compare these average rates and take a view regarding the actual future course of that rate relative to the implied rate, which will provide us with guidance on which element of the pair is likely to outperform the other until the next interconversion date, at which time the process will be repeated.

We can show the break-even rates for each FixedReset / FloatingReset Strong Pair graphically by plotting the implied average 3-month bill rate against the next Exchange Date (which is the date to which the average will be calculated).

Click for Big

The break-even T-Bill yield for the ALA.PR.G / ALA.PR.H pair is now -0.80% (given bid prices of 15.86 and 14.00, respectively; but note that there is no offer for ALA.PR.H and therefore the bid may be regarded with some suspicion even without considering how this relates to other FloatingResets, or other pairs).

Well this jumped up today … Not unhappy 🙂

The TSX reports only two trades today with an identical timestamp … TD buying 200 shares from CIBC at 25.00. Fat-finger error? Market order? I wouldn’t go around spending your winnings just yet!

Ha ha! No, I won’t spend my winnings. I’m kind of sad really because the same seems to be happening here as happened ALA.PR.E when it got taken out. ALA just raised a pile of cash and I think they are going to redeem this one as well.