As Novartis AG’s chief executive, [Joe] Jimenez is barreling down untested paths at the frontier of biology and digital technology to prepare for a future in which the use of smartphones and other digital devices to monitor health will be the key to getting paid.

…

Projects and products include pills and inhalers with sensors that tell on patients who miss a dose; clinical tests that rely on Microsoft’s Kinect, the motion-sensing technology used with Xboxes, to measure walking speed and balance in people with multiple sclerosis; and Google contact lenses that focus automatically and can deduce diabetics’ blood-sugar levels from their tears — a gamble that Jimenez says could transform eyesight.

Equities have no direction this month:

Stringing together gains in the American stock market has become next to impossible.

Knocked down 1.5 percent Wednesday, the Standard & Poor’s 500 Index has now gone 26 days without posting gains in back-to-back sessions, the longest stretch since 1994, data compiled by Bloomberg show. Losses in biotechnology and chip companies dragged U.S. stocks to a third day of declines, interrupting another run at a record for the Nasdaq Composite Index as investors sold the year’s best-performing equities.

The Fed is concerned about the mechanics of a rate hike:

In the past, the Fed increased the cost of overnight bank borrowing by raising the funds rate. The trillions of dollars in excess reserves that exist, compared with a few billion at the start of 2007, have obviated the need for banks to borrow daily and forced U.S. monetary authorities to come up with ways to influence market rates directly.

It has been evident since 2008, when the Fed gained the ability to pay interest on excess reserves, that the new rate wasn’t anchoring borrowing costs as envisioned. Government-sponsored agencies including regional Federal Home Loan Banks, primary providers of cash in the overnight market, aren’t able to receive such interest, which has enabled the funds rate to drift below IOER [Interest On Excess Reserves], now at 0.25 percent.

To make matters worse, widespread negative yields abroad, and heightened regulation on banks and money funds, have sapped the supply of safe short-term assets and buoyed demand. That further casts doubt on whether a tightening of policy will be smooth.

Strategists have expressed concern that, when the Fed starts to tighten policy by raising IOER, other market rates may not follow, leaving monetary conditions too accommodative. While banks receiving interest on surplus reserves have dimmed their desire to dump excess cash into the money markets, the funds rate has still consistently traded below the IOER. The reverse repo program thus far has helped provide a floor for the funds rate.

Problems with the Effective Fed Funds rate became apparent during the Credit Crunch, as discussed at Effective Fed Funds Rate Continues to Confuse, Effective Fed Funds Rate: A Technical Explanation? and Effective Fed Funds and Interest on Excess Reserves.

There will be a secondary offering of Capital Power common:

Capital Power Corporation (TSX: CPX) (“Capital Power”) and EPCOR Utilities Inc. (“EPCOR”) announced today that Capital Power and EPCOR have entered into an agreement with a syndicate of underwriters, co-led by CIBC and TD Securities Inc., as bookrunners, for a secondary offering by EPCOR Power Development Corporation (“EPDC”), a subsidiary of EPCOR, on a bought deal basis, of 9,000,000 common shares of Capital Power at an offering price of $23.85 per common share. Capital Power will not receive any of the proceeds ($215 million, before giving effect to the over-allotment option) from the sale of common shares by EPDC.

The underwriters have also been granted an option to purchase up to an additional 450,000 common shares at the issue price to cover over-allotments, if any. If exercised, EPDC will receive additional gross proceeds of approximately $10.7 million. The over-allotment option is exercisable, in whole or in part, by the underwriters at any time up to 30 days after the closing of the offering. Capital Power will not receive any proceeds from the exercise of the over-allotment option.

Capital Power doesn’t appear to be hard up for cash. They’ve suspended their DRIP:

Effective for the expected June 30, 2015 dividend, Capital Power will be suspending its Dividend Reinvestment Plan (DRIP) for its common shares until further notice. Shareholders participating in the DRIP will begin receiving cash dividends on the expected July 31, 2015 payment date. If the Company elects to reinstate the DRIP in the future, shareholders that were enrolled in the DRIP at suspension and remained enrolled at reinstatement, will automatically resume participation in the DRIP.

Capital Power is the proud issuer of CPX.PR.A, CPX.PR.C and CPX.PR.E, all FixedResets.

Loblaw Companies Limited, proud issuer of L.PR.A, was confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating, Medium-Term Notes rating and Debentures rating of Loblaw Companies Limited (Loblaw or the Company) at BBB, its Cumulative Redeemable Second Preferred Shares, Series A rating at Pfd-3 and its Short-Term Issuer Rating at R-2 (middle), all with Stable trends. DBRS also confirmed the Senior Unsecured Debt rating of Shoppers Drug Mart Corporation (Shoppers) at BBB with a Stable trend, based on guarantee by Loblaw. The confirmation primarily reflects Loblaw’s continued deleveraging efforts, which should result in credit metrics considered acceptable for the current rating by the end of 2015, as well as, its solid operating performance in 2014.

…

DBRS expects that Loblaw’s financial leverage should continue to decline as the Company uses free cash flow to repay debt pursuant to its deleveraging plan following the acquisition of Shoppers. Cash flow from operations should track operating income over the medium term, while capital expenditures (capex) should remain in the current $1.2 billion to $1.4 billion per year with a shifting focus toward retail investments. The cash outlay related to dividends is expected to remain above the $400 million level. DBRS, therefore, continues to believe that Loblaw will generate free cash flow in the $700 million per year range. Loblaw is expected to use free cash flow in the near term primarily for debt repayment. DBRS forecasts that lease-adjusted debt-to-EBITDAR attributable to the retail operations should return below 3.50 times (x) by the end of 2015, a level considered acceptable for the current rating. Over the longer term, DBRS expects that Loblaw will begin using free cash flow to complete share repurchases. Should operating performance remain solid and credit metrics improve further toward the Company’s stated target (i.e., lease-adjusted debt-to-EBITDAR of 3.25x) as a result of growing operating income and/or continuing debt repayment, a positive rating action would likely result.

George Weston Limited, proud issuer of WN.PR.A, WN.PR.C, WN.PR.D and WN.PR.E (all Straight Perpetuals) was confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Medium-Term Notes and Debentures rating of George Weston Limited (Weston or the Company) at BBB, its Short-Term Issuer Rating at R-2 (high) and its Preferred Shares rating at Pfd-3, all with Stable trends. The confirmations reflect the confirmation of the ratings of Loblaw Companies Limited (Loblaw; see separate press release) as well as Weston’s stable balance-sheet debt levels despite pressure on the Weston Foods bakery business from higher commodity costs.

…

Weston’s financial profile is expected to remain relatively stable going forward based on the Company’s ownership in Loblaw, its cash-on-hand, and its stable balance-sheet debt levels. Weston announced a strategic plan in 2015, which includes expansionary capex of approximately $300 million in 2015 and approximately $170 million in 2016 to increase capacity (including two new facilities in the United States) and innovation in key growth areas. As a result of the increase in capex, Weston Foods is expected to incur a free cash flow deficit through the end of 2016. DBRS believes the Company will use a portion of its cash-on-hand to fund such investments, while maintaining at least $1 billion of cash-on-hand and short-term investments through the end of Loblaw’s deleveraging plans expected to be completed at the end of 2015. Over the longer-term DBRS expects the Company will continue to use cash-on-hand and free cash-flow generated to invest in growth (organic and/or acquisitions) and/or to increase returns to shareholders. Weston’s ownership interest in Loblaw could return above the 50% level in the medium term as Loblaw is expected to use free cash flow to complete share repurchases once it completes its deleveraging plan. DBRS notes that a positive rating action at Loblaw would not necessarily result in a corresponding rating action at Weston.

It was a modestly negative day for the Canadian preferred share market, with PerpetualDiscounts down 7bp, FixedResets losing 14bp and DeemedRetractibles off 4bp. The Performance Highlights table is notable for a large contingent of Enbridge FixedReset losers. Volume was high.

PerpetualDiscounts now yield 4.99%, equivalent to 6.49% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.6% so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 290bp, a widening from the 280bp reported March 18.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

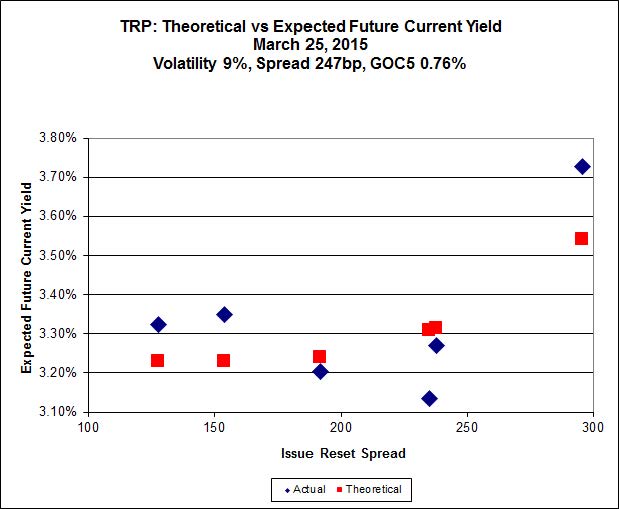

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.80 to be $1.29 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.32 cheap at its bid price of 24.95.

Click for Big

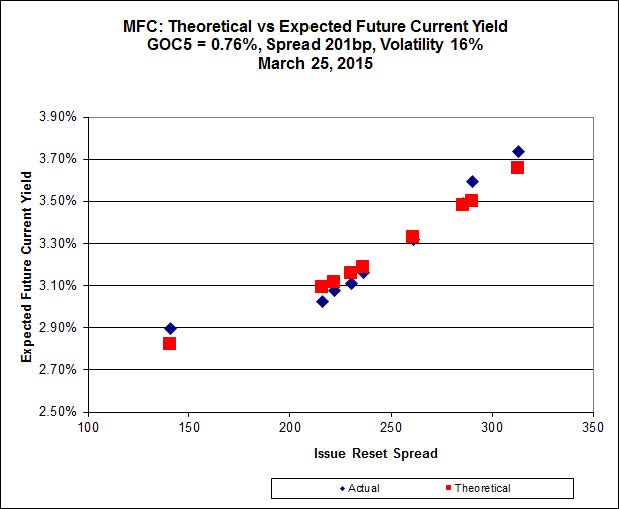

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.15 to be $0.52 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.47 to be $0.67 cheap.

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.21 to be $0.67 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.14 and appears to be $0.64 rich.

Click for Big

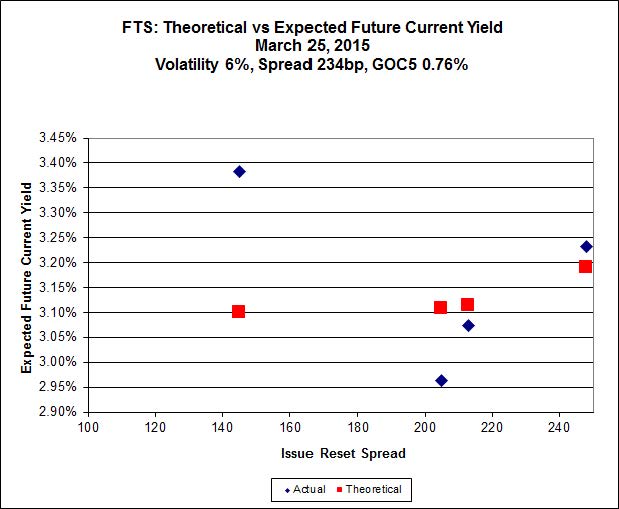

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.33, looks $1.49 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.71 and is $1.10 rich.

Click for Big

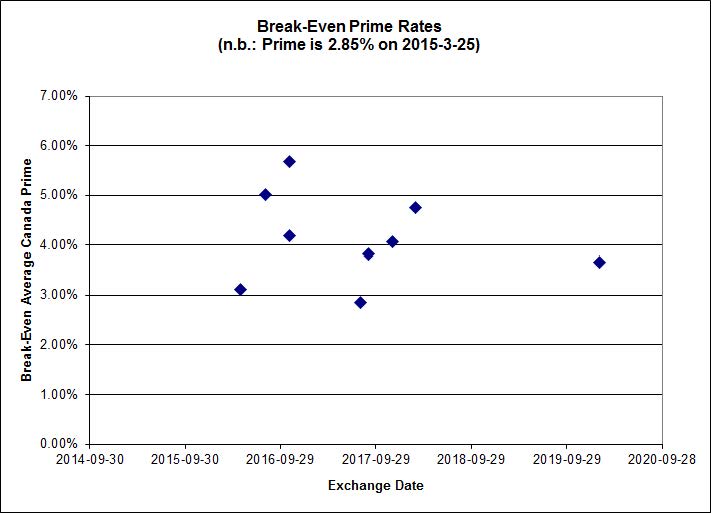

Investment-grade pairs predict an average over the next five years of a little under 0.10% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.51%. The DC.PR.B / DC.PR.D pair is still off the charts and now predicts an average bill rate over the next 4 3/4 years of -2.09%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.8864 % | 2,354.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.8864 % | 4,116.5 |

| Floater | 3.22 % | 3.22 % | 61,060 | 19.18 | 3 | 1.8864 % | 2,502.8 |

| OpRet | 4.06 % | 0.48 % | 101,768 | 0.24 | 1 | 0.1190 % | 2,769.1 |

| SplitShare | 4.35 % | 4.26 % | 34,254 | 3.48 | 4 | 0.1700 % | 3,215.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1190 % | 2,532.1 |

| Perpetual-Premium | 5.30 % | 1.77 % | 57,064 | 0.08 | 25 | 0.0027 % | 2,523.5 |

| Perpetual-Discount | 4.97 % | 4.99 % | 163,378 | 15.20 | 9 | -0.0651 % | 2,814.5 |

| FixedReset | 4.38 % | 3.37 % | 239,358 | 16.78 | 85 | -0.1429 % | 2,431.0 |

| Deemed-Retractible | 4.91 % | -0.20 % | 112,356 | 0.17 | 37 | -0.0427 % | 2,657.1 |

| FloatingReset | 2.43 % | 2.82 % | 80,805 | 6.31 | 8 | -0.1118 % | 2,341.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PF.A | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 4.21 % |

| ENB.PF.C | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 21.51 Evaluated at bid price : 21.51 Bid-YTW : 4.25 % |

| MFC.PR.C | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.87 Bid-YTW : 5.13 % |

| ENB.PF.G | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 21.41 Evaluated at bid price : 21.71 Bid-YTW : 4.25 % |

| ENB.PR.J | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 4.13 % |

| ENB.PR.F | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 4.27 % |

| IFC.PR.A | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 4.96 % |

| HSE.PR.A | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 17.13 Evaluated at bid price : 17.13 Bid-YTW : 3.72 % |

| GWO.PR.I | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.09 Bid-YTW : 4.99 % |

| MFC.PR.L | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.15 Bid-YTW : 3.79 % |

| BAM.PR.K | Floater | 4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 15.43 Evaluated at bid price : 15.43 Bid-YTW : 3.23 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.M | FixedReset | 208,600 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 23.00 Evaluated at bid price : 24.65 Bid-YTW : 3.35 % |

| RY.PR.J | FixedReset | 154,275 | Scotia crossed 122,000 at 25.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 23.18 Evaluated at bid price : 25.10 Bid-YTW : 3.37 % |

| ENB.PR.T | FixedReset | 147,624 | RBC crossed 140,000 at 20.47. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 20.31 Evaluated at bid price : 20.31 Bid-YTW : 4.21 % |

| GWO.PR.M | Deemed-Retractible | 79,595 | Scotia crossed 70,000 at 26.22. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-30 Maturity Price : 26.00 Evaluated at bid price : 26.20 Bid-YTW : -3.27 % |

| TD.PF.D | FixedReset | 76,980 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 23.15 Evaluated at bid price : 25.02 Bid-YTW : 3.41 % |

| CM.PR.Q | FixedReset | 74,225 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-25 Maturity Price : 23.10 Evaluated at bid price : 24.88 Bid-YTW : 3.44 % |

| There were 47 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.G | FixedReset | Quote: 23.51 – 23.91 Spot Rate : 0.4000 Average : 0.2391 YTW SCENARIO |

| BNS.PR.M | Deemed-Retractible | Quote: 25.67 – 25.98 Spot Rate : 0.3100 Average : 0.1915 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 24.01 – 24.44 Spot Rate : 0.4300 Average : 0.3202 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 23.87 – 24.24 Spot Rate : 0.3700 Average : 0.2688 YTW SCENARIO |

| ENB.PR.F | FixedReset | Quote: 19.86 – 20.14 Spot Rate : 0.2800 Average : 0.1934 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 24.67 – 24.89 Spot Rate : 0.2200 Average : 0.1371 YTW SCENARIO |