The CME’s Department of Selective Enforcement has decided to make a sudden fuss about spoofing and two guys have been scapegoated:

CME Group Inc. said it suspended two traders for placing manipulative trades similar to the ones that catapulted Navinder Singh Sarao into headlines around the world last week.

Heet Khara and Nasim Salim engaged in a practice called “layering,” in which orders are placed with no intention of following through on them, according to CME, the owner of the futures exchange where the two gold and silver traders did business. Khara and Salim are barred from trading on CME markets for 60 days.

However, the trivial nature of the transgression is illustrated by the fact that they only face a 60 day trading ban. Have a nice holiday guys … unless, of course, you hire somebody else to push the buttons with the assistance of your advice. The ZeroHedge blog considers the affair to be scapegoating and window-dressing with a hint of racism.

Anti-Spoofing regulations are unenforceable and spoofing does no direct harm to the interests of fundamental traders (indirect harm, through a thinning of the markets, is possible but I have not seen evidence of this). Anti-spoofing regulations should be repealed; I suspect that consequent private sector development of counter-spoofing tactics will be far more effective than any amount of regulation could ever possibly be.

Holy smokaramaville, but it’s been a week and half for the fixed income markets! Bloomberg notes that it’s been the worst week in almost two months (put that way, it sounds pretty routine, doesn’t it?):

The worst week for U.S. 10-year notes in almost two months got even bleaker as a rout in European bonds continued to diminish investor appetite for relatively higher U.S. yields. The notes also extended an April decline after a report showed U.S. consumer confidence rose last month.

…

Treasury 10-year yields rose eight basis points, or 0.08 percentage point, to 2.11 percent as of 5 p.m. New York time. It touched 2.12 percent, the highest since March 13, based on Bloomberg Bond Trader data. The benchmark 2 percent note due in February 2025 fell 23/32, or $7.19 per $1,000 face amount, to 99.

…

Ten-year yields climbed 20 basis points this week, the most since the week ending March 6, and are up from 1.92 percent at the start of April.U.S. debt extended losses after the University of Michigan said Friday that its final consumer-confidence index for April increased to 95.9 from 93 in March. The median projection in a Bloomberg survey of economists was for 96.

That followed a series of weak first-quarter economic readings that the Fed this week blamed on “transitory” factors including brutal winter weather in much of the U.S. Fed Chair Janet Yellen and her colleagues reiterated in a statement on April 29 after a two-day meeting that they believe growth will pick up to a “moderate pace”.

…

Euro-area debt started selling off early in the week and reached a peak on April 29, when 55 billion euros ($62 billion) was wiped off the value of the region’s government bonds on the day.The extra yield that investors get for holding Treasury 10-year notes instead of similar-maturity German bunds narrowed to 167 basis points on Thursday, the least on a closing basis since April 3.

… and the chart:

Click for Big

This is despite the moderating influence of hedge fund activity:

They don’t think it will last.

Hedge-fund managers and other large speculators who saw the start or this week’s bond rout nevertheless moved in the opposite direction, trimming bearish bets on 10-year notes to the lowest level in 10 weeks.

Net shorts on the securities totaled 98,565 contracts as of April 28, down from 153,366 the week before, according to Commodity Futures Trading Commission data.

It would be most interesting to learn whether hedge-fund activity is generally counterflow. I suspect it is, given that reversion is what quants do best, but I am not aware of any research on this.

And all this affected Canada. According to the BoC, five-year Canadas were trading at 0.71% last Friday, and according to Perimeter they ended this week at 1.04%. That’s a hell of a move for a five year sovereign – although not quite so fast as the descent in January when the overnight rate got cut.

What’s driving it, I think, is that as discussed yesterday, the previously announced European deflation has been cancelled. So markets which were expecting low rates forever are now expecting high rates forever … and this has certainly had an effect in the preferred share market, as previous panic over continued reductions in FixedReset dividends on reset have, at the very least, been moderated.

But we’ll see what next week brings. The market does what it wants to do when it wants to do it. For what it’s worth, I believe that the current situation of 5-year governments trading below inflation to be unsustainable, a very useful word for financial analysis since it doesn’t mean anything. I will opine that I believe the paradox will be resolved by an increase in sovereign yields (rather than a decline in inflation), but I would not dream of predicting just exactly when this might occur.

Still, the violent change in sentiment made it a wild month for FixedResets!

Click for Big

Look at all the fun you had in April and it didn’t cost you anything!

It was an unevenly strong day for the Canadian preferred share market, with PerpetualDiscounts up 30bp, FixedResets winning 64bp and DeemedRetractibles gaining 3bp. The Performance Highlights table is, as one might expect, dominated by winning FixedResets. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

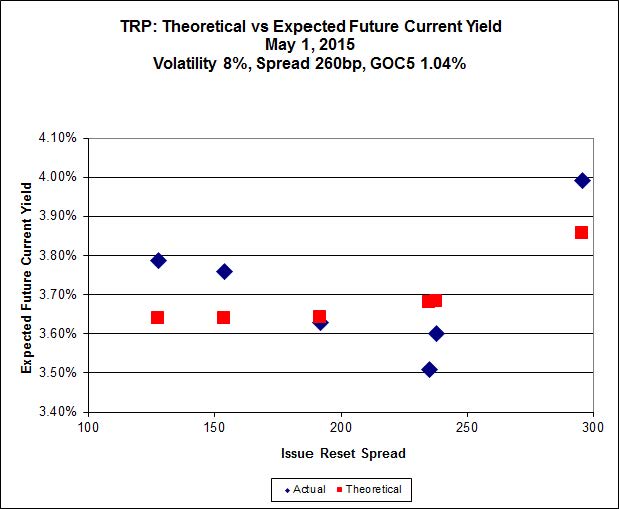

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.15 to be $1.11 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.88 cheap at its bid price of 25.05.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.30 to be $0.40 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.41 to be $0.53 cheap.

Click for Big

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.45 to be $0.61 cheap. BAM.PR.X, resetting at +180bp 2017-6-30 is bid at 18.75 and appears to be $0.82 rich.

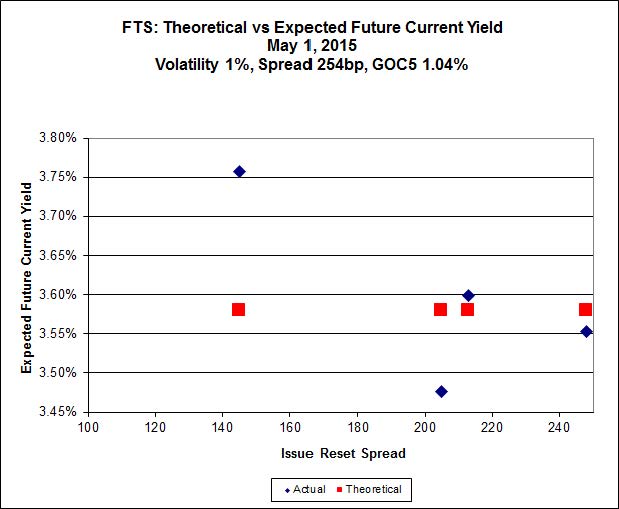

Click for Big

FTS.PR.H, with a spread of +145bp, and bid at 16.57, looks $0.82 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.22 and is $0.64 rich.

Click for Big

Investment-grade pairs now predict an average over the next five years of about 0.25%, but TRP.PR.A / TRP.PR.F is an outlier at -0.33%. The DC.PR.B / DC.PR.D pair retains its customary outlier status, with a breakeven rate of -1.27%. The new data point for BRF.PR.A / BRF.PR.B cannot be considered reliable.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9600 % | 2,296.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9600 % | 4,015.1 |

| Floater | 3.16 % | 3.25 % | 54,172 | 19.09 | 4 | 0.9600 % | 2,441.2 |

| OpRet | 4.42 % | -4.62 % | 37,871 | 0.09 | 2 | -0.0197 % | 2,765.3 |

| SplitShare | 4.57 % | 4.76 % | 68,324 | 3.37 | 3 | -0.2663 % | 3,223.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0197 % | 2,528.6 |

| Perpetual-Premium | 5.45 % | -0.79 % | 68,911 | 0.08 | 18 | 0.0676 % | 2,520.1 |

| Perpetual-Discount | 5.03 % | 4.99 % | 115,903 | 15.41 | 15 | 0.3046 % | 2,785.9 |

| FixedReset | 4.40 % | 3.73 % | 276,479 | 16.74 | 86 | 0.6384 % | 2,409.2 |

| Deemed-Retractible | 4.93 % | 2.99 % | 112,826 | 0.24 | 36 | 0.0343 % | 2,648.1 |

| FloatingReset | 2.59 % | 2.96 % | 71,981 | 6.21 | 7 | -0.1222 % | 2,320.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.B | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.00 Evaluated at bid price : 22.45 Bid-YTW : 4.07 % |

| FTS.PR.K | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 21.85 Evaluated at bid price : 22.22 Bid-YTW : 3.54 % |

| ENB.PR.Y | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.14 Evaluated at bid price : 20.14 Bid-YTW : 4.32 % |

| RY.PR.L | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 25.90 Bid-YTW : 3.19 % |

| TRP.PR.D | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.74 Evaluated at bid price : 23.75 Bid-YTW : 3.51 % |

| ENB.PF.A | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 21.75 Evaluated at bid price : 22.14 Bid-YTW : 4.27 % |

| MFC.PR.J | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.52 Bid-YTW : 3.97 % |

| NA.PR.W | FixedReset | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.83 Evaluated at bid price : 24.10 Bid-YTW : 3.33 % |

| MFC.PR.N | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 4.24 % |

| IAG.PR.G | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 3.82 % |

| BAM.PR.B | Floater | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 15.44 Evaluated at bid price : 15.44 Bid-YTW : 3.25 % |

| BNS.PR.R | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.47 Bid-YTW : 3.04 % |

| ENB.PF.G | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.02 Evaluated at bid price : 22.60 Bid-YTW : 4.22 % |

| PWF.PR.P | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 3.47 % |

| BNS.PR.Z | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 3.55 % |

| TD.PF.C | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.82 Evaluated at bid price : 24.06 Bid-YTW : 3.31 % |

| FTS.PR.F | Perpetual-Discount | 1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 24.57 Evaluated at bid price : 24.80 Bid-YTW : 5.01 % |

| ENB.PR.N | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 4.28 % |

| BAM.PR.K | Floater | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 15.16 Evaluated at bid price : 15.16 Bid-YTW : 3.31 % |

| ENB.PR.H | FixedReset | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 4.30 % |

| BAM.PR.X | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 3.89 % |

| BAM.PF.E | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.35 Evaluated at bid price : 23.13 Bid-YTW : 3.94 % |

| BAM.PR.R | FixedReset | 1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 4.06 % |

| MFC.PR.M | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 4.15 % |

| BAM.PR.T | FixedReset | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 4.03 % |

| ENB.PR.D | FixedReset | 2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.20 % |

| CIU.PR.C | FixedReset | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 16.43 Evaluated at bid price : 16.43 Bid-YTW : 3.59 % |

| HSE.PR.A | FixedReset | 2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 4.05 % |

| MFC.PR.L | FixedReset | 3.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.37 % |

| ENB.PR.B | FixedReset | 3.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.22 % |

| SLF.PR.G | FixedReset | 3.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.75 Bid-YTW : 6.39 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.G | FixedReset | 94,480 | RBC bought two blocks from Nesbitt: 16,700 at 17.00 and 22,600 at 17.20. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.75 Bid-YTW : 6.39 % |

| ENB.PR.B | FixedReset | 80,049 | RBC crossed 19,300 at 19.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.22 % |

| BMO.PR.J | Deemed-Retractible | 78,100 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-05-31 Maturity Price : 25.25 Evaluated at bid price : 25.22 Bid-YTW : 2.35 % |

| TD.PF.C | FixedReset | 59,208 | Desjardins crossed 38,200 at 24.04. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 22.82 Evaluated at bid price : 24.06 Bid-YTW : 3.31 % |

| RY.PR.C | Deemed-Retractible | 41,600 | Nesbitt bought four blocks of 10,000 each from anonymous, all at 25.16. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-11-24 Maturity Price : 25.00 Evaluated at bid price : 25.12 Bid-YTW : 3.22 % |

| CM.PR.Q | FixedReset | 31,700 | Nesbitt crossed 25,000 at 25.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-01 Maturity Price : 23.09 Evaluated at bid price : 24.85 Bid-YTW : 3.59 % |

| There were 23 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CIU.PR.C | FixedReset | Quote: 16.43 – 17.25 Spot Rate : 0.8200 Average : 0.6700 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 24.86 – 25.25 Spot Rate : 0.3900 Average : 0.2449 YTW SCENARIO |

| ENB.PR.P | FixedReset | Quote: 20.73 – 21.09 Spot Rate : 0.3600 Average : 0.2225 YTW SCENARIO |

| ENB.PR.T | FixedReset | Quote: 20.61 – 20.94 Spot Rate : 0.3300 Average : 0.2032 YTW SCENARIO |

| ENB.PF.E | FixedReset | Quote: 22.15 – 22.43 Spot Rate : 0.2800 Average : 0.1814 YTW SCENARIO |

| GWO.PR.H | Deemed-Retractible | Quote: 24.63 – 24.90 Spot Rate : 0.2700 Average : 0.1749 YTW SCENARIO |