The latest worry is Quantitative Easing effects on European corporate bond liquidity:

The European Central Bank’s addition of three listed companies’ notes to a bond-buying program has sparked concerns about how far it may push into the corporate-bond market and the impact this would have on already tight liquidity.

The inclusion of the listed companies, all Italian utilities less than 30 percent state owned, may mark a first step toward buying bonds from any government-backed company, BNP Paribas SA analysts wrote in a note. That may open as much as 157 billion euros ($174 billion) of securities outstanding to potential ECB buying, including notes from Volkswagen AG, Airbus Group SE and Telekom Austria AG, they said.

“Let’s hope the ECB leaves its additions here, but there are plenty more companies that seem to tick its latest box for inclusion,” said Jeroen Van Den Broek, the head of developed-markets credit strategy and research at ING Bank NV in Amsterdam. “With the ECB buying up what little liquidity there is left in euro-zone investment-grade corporates, it pushes real money managers even further down the curve.”

Liquidity has already plunged in the corporate-bond market, with trading tumbling about 90 percent since 2006, according to Royal Bank of Scotland Group Plc. That slump, predominately caused by banks cutting holdings to preserve capital in response to tougher capital rules, has prompted the Bank for International Settlements to warn about liquidity traps.

The Chinese may be relative newcomers to equity markets but they’ve got the official response to downturns down pat:

Rumor-spreading short sellers and foreign investors with a hidden agenda.

If you believe China’s state-run media, those are some of the key culprits for a stock-market rout that erased $3.2 trillion of value in three weeks — or almost $1 million for each minute of trading on mainland exchanges. The underlying message, that market manipulation is fueling the selloff, was reinforced by securities regulators last week as they pledged to crack down on “vicious” short selling.

The problem with that narrative, though, is that the numbers tell a different story. Short positions on the Shanghai Stock Exchange totaled just 1.95 billion yuan ($314 million) on Thursday, or less than 0.03 percent of the country’s market capitalization, as bears closed out more than half their bets since June 12. Foreign money managers own fewer than 3 percent of Chinese shares, and they’ve been adding to holdings in Shanghai as prices tumble.

There has been lots of credit news lately! Greece … Puerto Rico … Ontario:

- •We are lowering our long-term issuer credit and senior unsecured debt ratings on the Province of Ontario to ‘A+’ from ‘AA-‘.

- •At the same time, we are affirming our ‘A-1+’ short-term and commercial paper ratings on the province.

- •The downgrade reflects our view that Ontario is a sustained and projected underperformer on its budgetary performance and debt burden versus domestic and international peers.

- •The stable outlook reflects our expectation that, under our base-case scenario, Ontario will continue to make slow progress in reducing its after-capital deficit in the next two fiscal years and that it will continue with its stated 10-year capital plan.

RATING ACTION

On July 6, 2015, Standard & Poor’s Ratings Services lowered its long-term issuer credit rating and senior unsecured debt ratings on the Province of Ontario to ‘A+’ from ‘AA-‘. At the same time, Standard & Poor’s affirmed its ‘A-1+’ short-term and commercial paper ratings on the province. The outlook is stable.RATIONALE

The downgrade reflects our view that Ontario is a sustained and projected underperformer on its budgetary performance and debt burden versus domestic and international peers. Although Ontario continues to beat its fiscal targets and expects to close its operating budget gap by fiscal 2018 (year-ended March 31), it will still have to contend with sizable yearly after-capital deficits, given its large net capital spending intentions. Under our base-case scenario, we foresee Ontario’s after-capital deficit remaining above 7% of total adjusted revenues over the next two years. Additional capital revenues from potential asset sales or the cap-and-trade scheme put forward but not articulated in the fiscal 2016 budget could mitigate the province’s medium-term borrowing demands. In the next two years, however, we expect capital funding needs to cause Ontario’s tax-supported debt to peak at 267% of consolidated operating revenues (and its interest payments to remain near 9%of adjusted operating revenues from fiscal years 2015-2017), which we consider very high. While some domestic and international peers display very weak budgetary performances or very high debt burdens similarly, it is the combination of both that sets Ontario apart from the group, leading us to conclude that its credit profile is more consistent with an ‘A+’ rating.

I just hope they’ve accounted for the near-certainty that the millions of tourists coming here for the Pan-Scam Games will be so impressed by our enormous solar power research, engineering and production industry that they place huge orders.

Margaret Wente had a thought-provoking piece in the Globe on the weekend, The world’s nicest, most law-abiding generation:

Social norms have changed a lot since then. The past 50 years have been a watershed for attitudes toward everything from sexism and human rights to littering (now almost a capital offence). By almost any measure you can find, people across the developed world today are the least violent, most law-abiding, hardest-working and most tolerant generation who ever lived.

The biggest measurable change is in violent crime. After peaking in the 1990s, crime rates have plummeted across the developed world, even in the famously violent United States. In Canada, crime rates are now back to where they were in the 1960s. Although theories abound, nobody really knows why.

…

What explains this remarkable progress in conduct and morality? Harvard psychologist Stephen Pinker argues that they are simply the continuation of a long-term evolution in behaviour that began centuries ago. Since medieval times, Northern Europeans have gradually grown less cruel, less violent, and more self-restrained. As society became more complex, it rewarded people who were more diligent, prudent and mild-mannered, and punished people with poor impulse control.

…

This evolution hasn’t stopped. As Simon Kuper suggested in the Financial Times this week, modern society increasingly rewards restraint. Discipline, self-control, compliance and the ability to get along with others are more important than they’ve ever been. Parents increasingly seek to instill those values in their children. They know there’s no frontier to escape to any more. They know that if their kid can’t manage to sit still and behave himself in school for a minimum of 12 to 14 years, that kid will be a loser.

Simon Kuper’s piece in the Financial Times, Why safety now trumps freedom suggests:

Elias’s great work, The Civilizing Process, argued that humans have been getting less violent since medieval times. States forced them to behave, and growing trade encouraged them to. Sadly, Elias’s timing was terrible. His book appeared in German in 1939, just as civilisation was collapsing. But today his argument sounds more credible. We now have evidence — which Elias didn’t — that western homicides have fallen fairly steadily for 700 years.

One disciple of Elias, the Harvard psychologist Steven Pinker, argues that in the 1990s western countries embarked on one of their periodic “civilising processes”. Governments got “tough on crime”. Social norms changed too. The 1960s ethos of “do your own thing, let it all hang out, take a walk on the wild side” lost favour.

…

“Safety” is such a magic word that American campuses now often ban controversial speakers because students must feel “safe” — an attitude that would have baffled 1960s campus activists. Western governments plead security to spy on citizens, and most citizens accept it. They have learnt to love Big Brother.

I suggest that the world’s wimpification stems from technological progress. Since the second war, technology has grown by leaps and bounds, exponentially. We have no idea of what tomorrow might bring, so we seek solace in making our personal lives more predictable.

There are many secondary effects as well; technology has made us immeasurably more productive than we used to be, making it possible to employ far more people as regulators of various sorts, whether these regulators are actually government regulators, police, jail guards, teachers or simply busybodies with time on their hands who achieve a measure of personal satisfaction and social acclaim for telling people they’re not behaving properly.

Increasing technology has, as Ms. Wente states, made school and education more important and has done so at a time when elementary and secondary teaching has become feminized. There are now two types of elementary school teacher: women and reckless idiots. Secondary school has not gone quite so far down that road, but far enough to make a difference. When I was about ten, there was a period when I got into a fist-fight every single day when school let out for lunch, with a guy I loved to hate. We were just kids, as full of piss and vinegar as ten-year-old boys can be. Nowadays we’d be sent for psychiatric evaluation by the horrified female teaching staff.

And we no longer despise informers; we celebrate them as whistle-blowers and see no shame in paying them.

Where will it end? If Wente’s sources are to be believed, it won’t. If my explanation is to be believed, it will end when the populace as a whole becomes inured to technological change and no longer fears innovation. We will see!

Another aspect of all this is that despite (or perhaps due to) all this regimentation and niceness, people are becoming less empathetic:

The research, led by Sara H. Konrath of the University of Michigan at Ann Arbor and published online in August in Personality and Social Psychology Review, found that college students’ self-reported empathy has declined since 1980, with an especially steep drop in the past 10 years. To make matters worse, during this same period students’ self-reported narcissism has reached new heights, according to research by Jean M. Twenge, a psychologist at San Diego State University.

… and that acceptance of social norms masks a hidden agenda:

The study, co-authored by Millennials expert Jean M. Twenge, was really three studies in one. All three are based on surveys that captured the values of millions of American 18-year-olds and college freshman between 1966 and 2009.

The first part looked at life goals. It turns out Millennials and GenX’ers (born between 1962 and 1981) rated being very well off financially, being a leader in the community (which is correlated with a desire for fame), living close to relatives, and having administrative responsibility over others as more important to them than Boomers—born 1946 to 1961—did when they were in their late teens.

Boomers—mostly over the age of 50 now—rated developing a meaningful philosophy of life, finding purpose and meaning, keeping up-to-date with politics, and becoming involved in programs to clean up the environment as more important when they were young than Millennials. Being “very well off financially” was the eighth most important life goal (out of 12) for Boomers; now, it’s consistently ranked most important.

If all this is true, then it suggests we are heading for a new Victorian era, in which social norms are extravagantly and viciously enforced (see my discussion of the Junior Justice League on May 12, amongst other places) while vice and hypocrisy flourish (Mayhew estimated 80,000 prostitutes in London, serving a total population of about 2.8-million; but note that Mayhew included what would now be called lovers and/or mistresses in his count).

It was a good day for the Canadian preferred share market, with PerpetualDiscounts up 17bp, FixedResets gaining 9bp and DeemedRetractibles winning 30bp. The Performance Highlights table has a good length. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

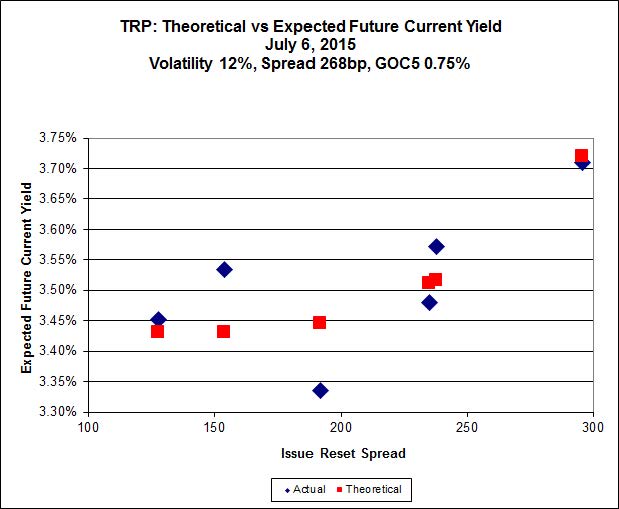

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 20.01 to be $0.64 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.49 cheap at its bid price of 16.20.

Click for Big

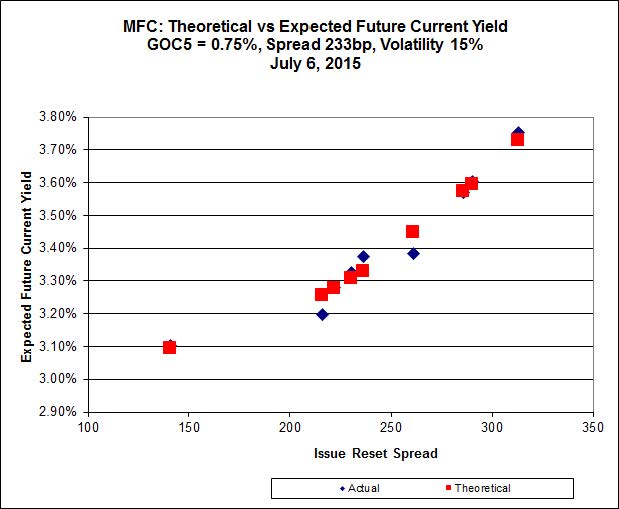

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 24.82 to be $0.45 rich, while MFC.PR.M, resetting at +236bp on 2019-12-19, is bid at 23.05 to be $0.30 cheap.

Click for Big

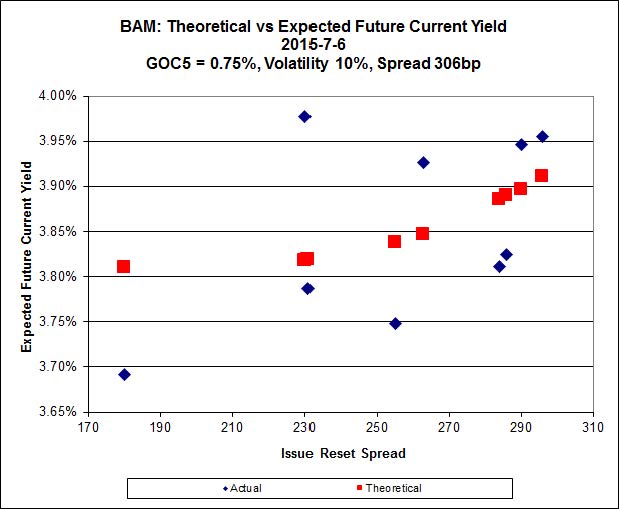

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.17 to be $0.80 cheap. BAM.PR.X, resetting at +180bp 2017-6-30 is bid at 17.27 and appears to be $0.54 rich.

Click for Big

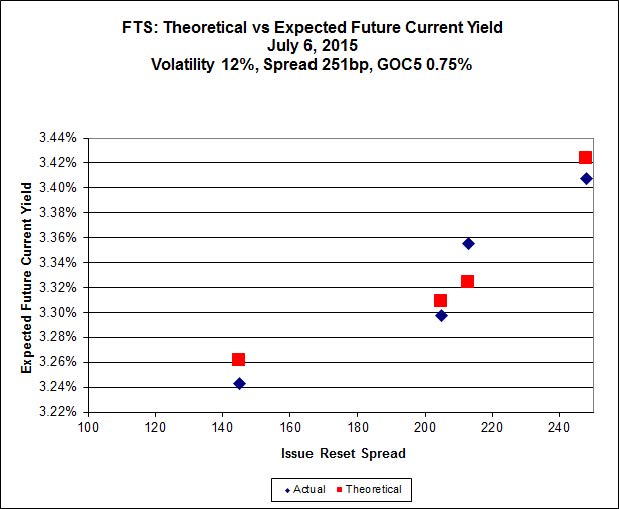

FTS.PR.G, with a spread of +213bp, and bid at 21.46, looks $0.20 cheap and resets 2018-9-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 23.70 and is $0.12 rich.

Click for Big

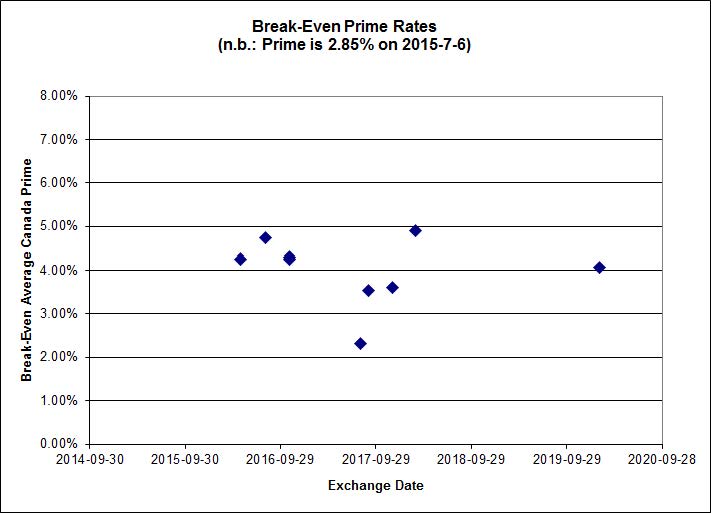

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.39%, including the outlier TRP.PR.A / TRP.PR.F at -0.19%. On the junk side, four of the six pairs are outliers, all with negative break-even yields.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0468 % | 2,214.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0468 % | 3,871.6 |

| Floater | 3.50 % | 3.55 % | 60,443 | 18.44 | 3 | 0.0468 % | 2,353.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0938 % | 2,768.8 |

| SplitShare | 4.59 % | 4.96 % | 64,649 | 3.23 | 3 | -0.0938 % | 3,244.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0938 % | 2,531.8 |

| Perpetual-Premium | 5.47 % | 3.97 % | 65,272 | 0.31 | 13 | -0.0543 % | 2,516.4 |

| Perpetual-Discount | 5.33 % | 5.24 % | 93,915 | 14.86 | 21 | 0.1747 % | 2,685.4 |

| FixedReset | 4.51 % | 3.61 % | 213,946 | 16.33 | 88 | 0.0852 % | 2,330.0 |

| Deemed-Retractible | 5.01 % | 3.15 % | 107,067 | 0.80 | 34 | 0.3050 % | 2,628.6 |

| FloatingReset | 2.48 % | 2.89 % | 53,561 | 6.09 | 10 | -0.2867 % | 2,320.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PF.A | FixedReset | -3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.74 % |

| ENB.PF.C | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 4.69 % |

| TRP.PR.E | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 21.86 Evaluated at bid price : 22.27 Bid-YTW : 3.73 % |

| ENB.PF.E | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 19.82 Evaluated at bid price : 19.82 Bid-YTW : 4.69 % |

| ELF.PR.G | Perpetual-Discount | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 21.80 Evaluated at bid price : 22.05 Bid-YTW : 5.39 % |

| BAM.PR.K | Floater | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 14.06 Evaluated at bid price : 14.06 Bid-YTW : 3.56 % |

| SLF.PR.J | FloatingReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.20 Bid-YTW : 7.07 % |

| MFC.PR.B | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.98 Bid-YTW : 5.82 % |

| SLF.PR.D | Deemed-Retractible | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.74 Bid-YTW : 5.73 % |

| MFC.PR.M | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 4.57 % |

| NA.PR.W | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 22.09 Evaluated at bid price : 22.65 Bid-YTW : 3.48 % |

| MFC.PR.K | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.63 Bid-YTW : 4.55 % |

| FTS.PR.J | Perpetual-Discount | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 23.33 Evaluated at bid price : 23.70 Bid-YTW : 5.05 % |

| IFC.PR.A | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.54 Bid-YTW : 6.12 % |

| BAM.PR.M | Perpetual-Discount | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 5.61 % |

| ENB.PR.F | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 4.71 % |

| SLF.PR.A | Deemed-Retractible | 1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.83 Bid-YTW : 5.42 % |

| MFC.PR.C | Deemed-Retractible | 2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.86 Bid-YTW : 5.73 % |

| MFC.PR.L | FixedReset | 2.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.75 Bid-YTW : 4.57 % |

| TD.PF.D | FixedReset | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 22.96 Evaluated at bid price : 24.45 Bid-YTW : 3.53 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.Z | FixedReset | 111,784 | Scotia bought 83,100 from GMP at 23.43. Nesbitt crossed 23,200 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.40 Bid-YTW : 3.37 % |

| HSE.PR.G | FixedReset | 108,557 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 22.90 Evaluated at bid price : 24.30 Bid-YTW : 4.43 % |

| BNS.PR.B | FloatingReset | 100,924 | RBC crossed 100,000 at 23.95. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 2.86 % |

| BAM.PR.Z | FixedReset | 87,237 | Scotia bought 79,700 from GMP at 23.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 22.77 Evaluated at bid price : 23.45 Bid-YTW : 4.10 % |

| TRP.PR.B | FixedReset | 29,157 | Scotia crossed 25,000 at 14.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-06 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 3.53 % |

| BMO.PR.K | Deemed-Retractible | 26,623 | TD crossed 24,100 at 25.70. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-08-05 Maturity Price : 25.50 Evaluated at bid price : 25.72 Bid-YTW : 1.84 % |

| There were 15 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 22.92 – 23.60 Spot Rate : 0.6800 Average : 0.4198 YTW SCENARIO |

| ENB.PF.A | FixedReset | Quote: 19.50 – 20.10 Spot Rate : 0.6000 Average : 0.3916 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 18.55 – 19.27 Spot Rate : 0.7200 Average : 0.5260 YTW SCENARIO |

| ENB.PF.C | FixedReset | Quote: 19.68 – 20.05 Spot Rate : 0.3700 Average : 0.2364 YTW SCENARIO |

| ENB.PF.E | FixedReset | Quote: 19.82 – 20.17 Spot Rate : 0.3500 Average : 0.2464 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 18.20 – 18.54 Spot Rate : 0.3400 Average : 0.2365 YTW SCENARIO |