There has been widening of NVCC-compliant sub-debt:

Investors who leaped into Basel-compliant bonds issued by Canadian banks to great fanfare are likely regretting their haste. A year on, the reward for taking on the risk of bailing out a bank has become much richer.

Relative yields of the bonds have widened 25 basis points this year, the worst performance among Canadian five-year corporate bonds, according to RBC Dominion Securities research. The debt is designed to convert to equity if a bank gets into financial distress, in line with new Basel rules to prevent another financial crisis. The first issue of the debt, called contingent capital bonds, in Canada was by Royal Bank of Canada in July, 2014.

…

Toronto-Dominion Bank was the most recent issuer, pricing $1.5-billion of 10-year notes on June 18 at a yield of 166 basis points more than the equivalent government benchmark. By comparison, investors demand about 108 basis points to hold senior-ranking bank debt, according to Merrill Lynch.

Google rallied a few days ago; today it was Amazon’s turn:

Amazon.com Inc. reported a surprise second-quarter profit on top of sales that beat analysts’ estimates, showing investors — as it has done before — that the Web retailer can make money when it puts the brakes on investments.

Shares in Amazon jumped as much as 19 percent after it reported Thursday that revenue rose 20 percent to $23.2 billion, helped by a fast-growing cloud-computing business and initiatives to lure more customers. Net income was $92 million, or 19 cents a share. Analysts projected, on average, a loss of 14 cents on sales of $22.4 billion.

…

Shares surged after the close of trading in New York, helping to push Amazon’s market capitalization to about $267 billion, more than Wal-Mart Stores Inc., the world’s largest retailer. The stock declined 1.3 percent to $482.18 at the close, leaving it up 55 percent this year.

And even the Canadian economy is forecast to grow:

The Canadian economy is already bouncing back from a slump in the first half of the year, but it remains vulnerable to further falls in oil prices and any renewed weakness in export demand from the United States, a Reuters poll found.

After the economy contracted in the first three months of the year, the second quarter also got off to a weak start, suggesting Canada, a major oil exporter, may have been in recession in the first half of 2015.

But economists, none of whom predicted such an outcome when polled on the outlook six months ago, forecast gross domestic product is already re-accelerating to a 1.7-per-cent rate, followed by 2.2 per cent in the fourth quarter.

A Reuters poll taken last week after the Bank of Canada shocked markets for a second time this year with an interest rate cut to dull the sting from falling oil prices found that the new rate of 0.5 per cent will likely be the floor.

It was a good, if mixed, day for the Canadian preferred share market, with PerpetualDiscounts gaining 18bp, FixedResets up 30bp and DeemedRetractibles off 1bp. The Performance Highlights table is dominated by winners. Volume was low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

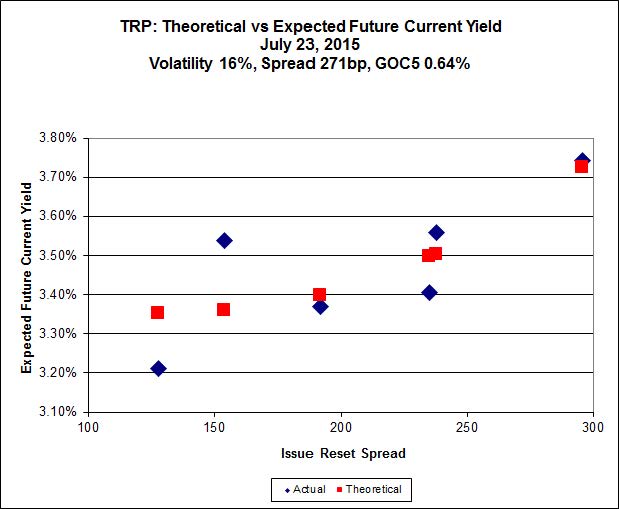

Here’s TRP:

Click for Big

TRP.PR.B, which resets 2020-6-30 at +128, is bid at 14.95 to be $0.63 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.82 cheap at its bid price of 15.40.

Click for Big

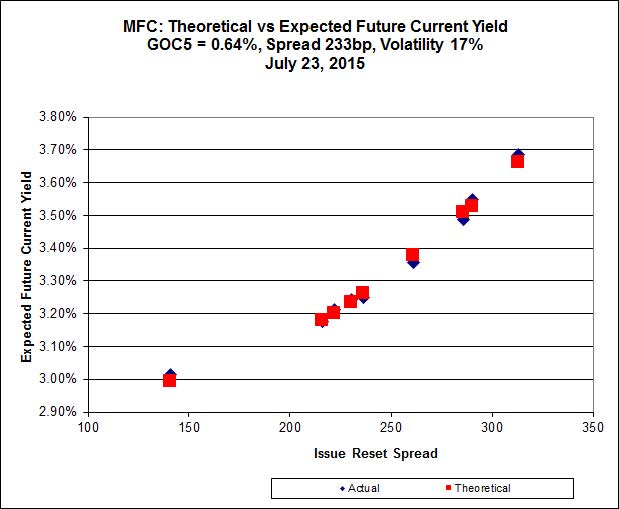

Another good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 25.10 to be $0.16 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.58 to be $0.15 cheap.

Click for Big

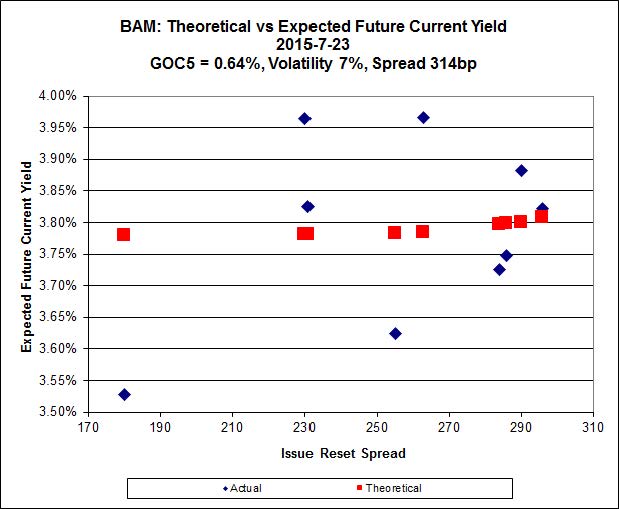

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 20.61 to be $1.00 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 17.29 and appears to be $1.15 rich.

Click for Big

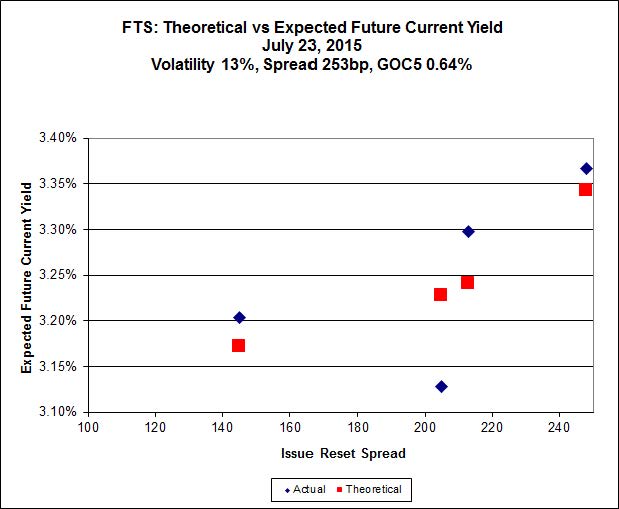

FTS.PR.K, with a spread of +205bp, and bid at 21.50, looks $0.66 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 21.00 and is $0.37 cheap.

Click for Big

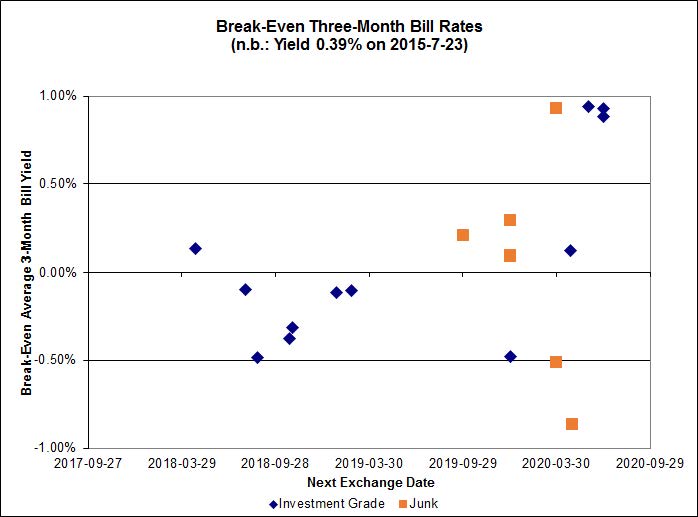

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of 0.09%, with no outliers. There are no junk outliers.

Click for Big

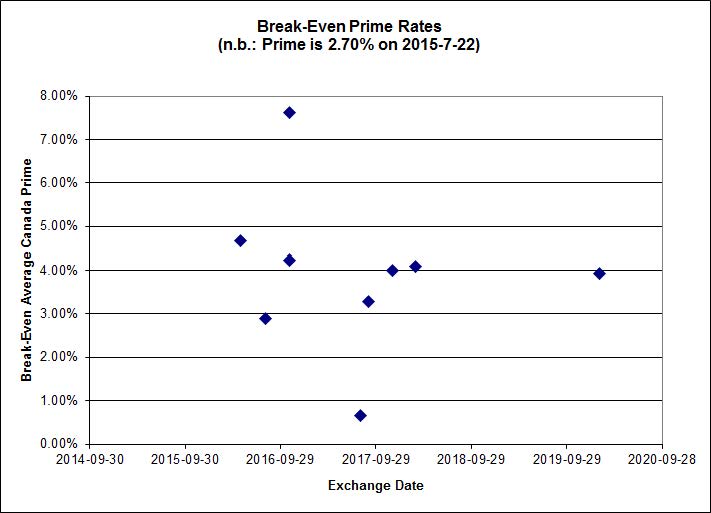

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5415 % | 2,113.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.5415 % | 3,696.0 |

| Floater | 3.47 % | 3.52 % | 60,973 | 18.47 | 3 | 1.5415 % | 2,247.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1743 % | 2,774.8 |

| SplitShare | 4.59 % | 4.90 % | 64,083 | 3.18 | 3 | 0.1743 % | 3,251.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1743 % | 2,537.3 |

| Perpetual-Premium | 5.53 % | 5.01 % | 70,613 | 2.27 | 13 | -0.0835 % | 2,507.8 |

| Perpetual-Discount | 5.31 % | 5.27 % | 93,990 | 14.96 | 23 | 0.1834 % | 2,677.7 |

| FixedReset | 4.61 % | 3.75 % | 210,688 | 16.22 | 88 | 0.2961 % | 2,283.3 |

| Deemed-Retractible | 5.04 % | 4.84 % | 110,502 | 3.30 | 34 | -0.0106 % | 2,614.5 |

| FloatingReset | 2.36 % | 3.06 % | 43,901 | 6.06 | 10 | 0.0877 % | 2,285.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PF.D | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.78 Evaluated at bid price : 24.02 Bid-YTW : 3.57 % |

| PWF.PR.K | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 23.69 Evaluated at bid price : 23.99 Bid-YTW : 5.17 % |

| NA.PR.S | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.69 Evaluated at bid price : 23.61 Bid-YTW : 3.40 % |

| BMO.PR.S | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.47 Evaluated at bid price : 23.20 Bid-YTW : 3.45 % |

| MFC.PR.K | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 4.75 % |

| BAM.PF.D | Perpetual-Discount | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 21.34 Evaluated at bid price : 21.65 Bid-YTW : 5.70 % |

| BAM.PR.Z | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.83 Evaluated at bid price : 23.55 Bid-YTW : 4.03 % |

| HSE.PR.C | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.13 Evaluated at bid price : 22.70 Bid-YTW : 4.40 % |

| BAM.PR.M | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 20.92 Evaluated at bid price : 20.92 Bid-YTW : 5.74 % |

| ENB.PF.A | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.78 % |

| ELF.PR.G | Perpetual-Discount | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.28 Evaluated at bid price : 22.55 Bid-YTW : 5.29 % |

| CM.PR.Q | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.93 Evaluated at bid price : 24.37 Bid-YTW : 3.51 % |

| BAM.PF.F | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.52 Evaluated at bid price : 23.35 Bid-YTW : 4.00 % |

| BAM.PR.K | Floater | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 3.52 % |

| HSE.PR.E | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.80 Evaluated at bid price : 24.00 Bid-YTW : 4.47 % |

| RY.PR.H | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.03 Evaluated at bid price : 22.50 Bid-YTW : 3.45 % |

| IFC.PR.A | FixedReset | 1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.43 Bid-YTW : 6.87 % |

| ENB.PR.J | FixedReset | 2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 18.95 Evaluated at bid price : 18.95 Bid-YTW : 4.68 % |

| BAM.PR.C | Floater | 3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 3.52 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.H | FixedReset | 117,185 | Desjardins crossed 80,900 at 22.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 22.03 Evaluated at bid price : 22.50 Bid-YTW : 3.45 % |

| RY.PR.O | Perpetual-Discount | 108,168 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 24.22 Evaluated at bid price : 24.59 Bid-YTW : 4.99 % |

| BNS.PR.Z | FixedReset | 93,414 | RBC crossed 50,000 at 22.70. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.69 Bid-YTW : 3.85 % |

| PWF.PR.T | FixedReset | 75,700 | Desjardins crossed 75,000 at 24.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 23.16 Evaluated at bid price : 24.60 Bid-YTW : 3.20 % |

| BMO.PR.Y | FixedReset | 60,300 | Scotia crossed 40,000 at 24.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 23.00 Evaluated at bid price : 24.56 Bid-YTW : 3.49 % |

| TD.PF.F | Perpetual-Discount | 52,135 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-23 Maturity Price : 24.30 Evaluated at bid price : 24.67 Bid-YTW : 4.98 % |

| There were 20 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.O | Perpetual-Premium | Quote: 25.85 – 26.19 Spot Rate : 0.3400 Average : 0.2144 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 21.00 – 21.50 Spot Rate : 0.5000 Average : 0.3811 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 22.01 – 22.50 Spot Rate : 0.4900 Average : 0.3727 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 22.05 – 22.65 Spot Rate : 0.6000 Average : 0.4865 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 24.10 – 24.50 Spot Rate : 0.4000 Average : 0.2868 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 24.00 – 24.59 Spot Rate : 0.5900 Average : 0.4768 YTW SCENARIO |