Strange goings-on in FundLand:

Since July, American households — which account for almost all mutual fund investors — have pulled money both from mutual funds that invest in stocks and those that invest in bonds. It’s the first time since 2008 that both asset classes have recorded back-to-back monthly withdrawals, according to a report by Credit Suisse.

Credit Suisse estimates $6.5 billion left equity funds in July as $8.4 billion was pulled from bond funds, citing weekly data from the Investment Company Institute as of Aug. 19. Those outflows were followed up in the first three weeks of August, when investors withdrew $1.6 billion from stocks and $8.1 billion from bonds, said economist Dana Saporta.

Meanwhile, US incomes are ticking up:

Consumer purchases climbed in July as incomes grew, showing the biggest part of the U.S. economy was off to a good start to the quarter.

The 0.3 percent advance matched the prior month’s gain, a Commerce Department report showed Friday in Washington. The median forecast in a Bloomberg survey of 77 economists called for a 0.4 percent increase. Wages rose by the most this year.

…

Total incomes rose 0.4 percent in July for a fourth month, matching the median forecast in the Bloomberg survey. Wages and salaries increased 0.5 percent, the biggest gain since November.Because spending increased less than incomes, the saving rate rose to 4.9 percent from 4.7 percent.

…

The report showed inflation remained tame. The price gauge based on the personal consumption expenditures index increased 0.1 percent from the prior month and was up 0.3 percent from a year earlier.The core price measure, which excludes food and fuel, also rose 0.1 percent from the prior month and was up 1.2 percent from July 2014, the smallest year-to-year gain in four years.

If it doesn’t continue, they’ll blame Canada:

“When Canada hurts, U.S. exporters do, too,” Bricklin Dwyer, an economist at BNP Paribas in New York, wrote in an Aug. 27 note to clients titled “Canada (not China) matters more.”

Economy-watchers and investors have been spooked by fears of a worse-than-expected Chinese slowdown after the nation devalued its currency Aug. 11 in a surprise move. Yet the direct effects on U.S. trade from slowing Chinese growth and the yuan move are probably fairly contained — far more so than the potential fallout from faltering Canadian demand.

Canada counts for 19 percent of total U.S. exports, followed by Mexico at 16 percent, each more than double China’s 7 percent share. And the Canadian dollar is sliding much faster: It has fallen about 12 percent against the U.S. dollar since the start of the year, while China’s yuan has dropped just about 3 percent.

And, too bad for Canada, we have a high domestic sensitivity to FX rate changes:

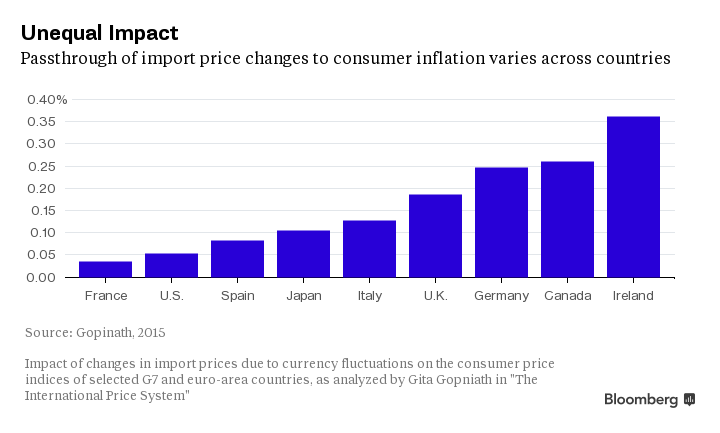

The central banker’s task of keeping inflation just right has become a permanent tussle with the global currency markets. Too weak a currency equals too rapid price gains. Too strong, and disinflation looms.

That’s the well-worn argument under the microscope Friday at the Jackson Hole Symposium, the U.S. Federal Reserve’s annual policy getaway. Gita Gopinath, a scholar at Harvard University, says that it just isn’t that simple.

“The greater the fraction of a country’s imports invoiced in a foreign currency, the greater its inflation sensitivity to exchange rate fluctuations at both short and long horizons,” she says. Because the dollar is by far the dominant currency in world trade, “U.S. inflation is consequently more insulated from exchange rate shocks, while other countries are highly sensitive to it.”

Click for Big

The Ukraine has issued GDP warrants:

The warrants included in a debt deal reached between Ukraine and its biggest creditors on Thursday offer bondholders annual payments for 20 years if economic growth crosses certain thresholds, Finance Minister Natalie Jaresko said at a briefing with journalists late on Thursday.

How are payments determined?

- •No payment will be made if growth is less than 3 percent

- •For growth between 3-4 percent, the payment will be 15 percent of the real GDP growth exceeding 3 percent

- •For growth faster than 4 percent, Ukraine will pay holders 40 percent of the expansion beyond 4 percent, in addition to amount for 3-4 percent growth

And today’s technology news is a pending revolution in bar codes:

The most ubiquitous barcodes allow an eight to 14 digit number to be read by a laser scanner. For example, barcode 4-003994-111000 identifies a box as being a 375 gram pack of Kellogg’s Corn Flakes.

However, that number does not directly capture any other information that might interest a shopper – such as ingredients, allergens or country of origin – nor does it provide a retailer with useful details such as the batch number or sell-by date.

That data is usually printed on the pack, but consumers increasingly want to read it online, or with a smartphone app such as one that measures calories. Retailers want data that can be scanned for tasks such as quickly locating faulty goods for recall or about-to-expire products for mark downs.

GS1, the non-profit organization that assigns the unique numbers in barcodes, has developed a double-layered barcode it calls the “data bar” which can carry some extra details such as expiry date, quantity, batch or lot number.

That has allowed German retailer Metro MEOG.DE to launch PRO Trace, a smartphone app that shows, for example, that a filet of salmon on sale at a store in Berlin on Aug. 25 was caught at the Bremnes Seashore fish farm off the coast of Norway on Aug. 17 and processed in Germany on Aug. 21.

The app also displays a map highlighting the fishing area of the catch and a detailed description of the Atlantic salmon.

Metro says the app helps customers at its cash-and-carry stores such as professional chefs from hotels and restaurants, as they can now embellish their menus with information about the exact origin of pricey delicacies such as wagyu beef.

It was a very strong day for the Canadian preferred share market, with PerpetualDiscounts gaining 12bp, FixedResets winning 81bp and DeemedRetractibles up 50bp. The Performance Highlights table is again very lengthy, but this time there are only a handful of losers. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

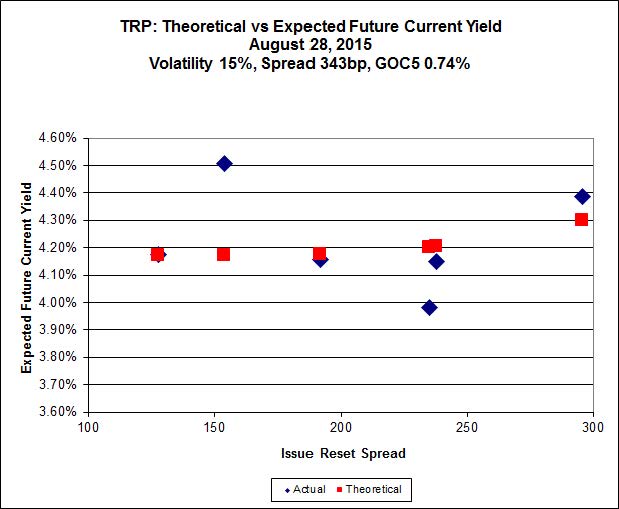

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.40 to be $1.01 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.02 cheap at its bid price of 12.65.

Click for Big

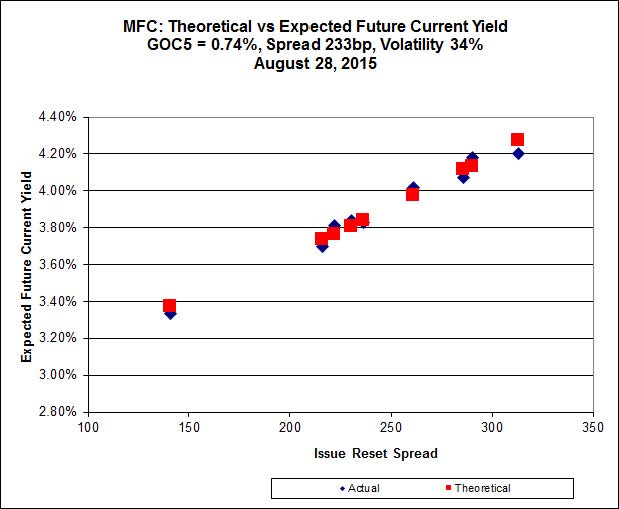

Another good fit today for MFC, with Implied Volatility dropping a bit again today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.01 to be 0.36 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 21.76 to be 0.26 cheap.

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.30 to be $1.75 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.50 and appears to be $1.24 rich.

Click for Big

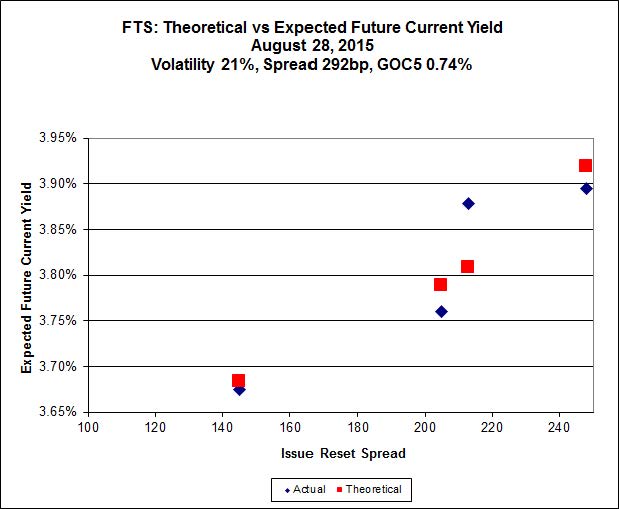

Implied Volatility increased a bit today and remains unreasonably high.

FTS.PR.K, with a spread of +205bp, and bid at 18.55, looks $0.14 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.50 and is $0.34 cheap.

Click for Big

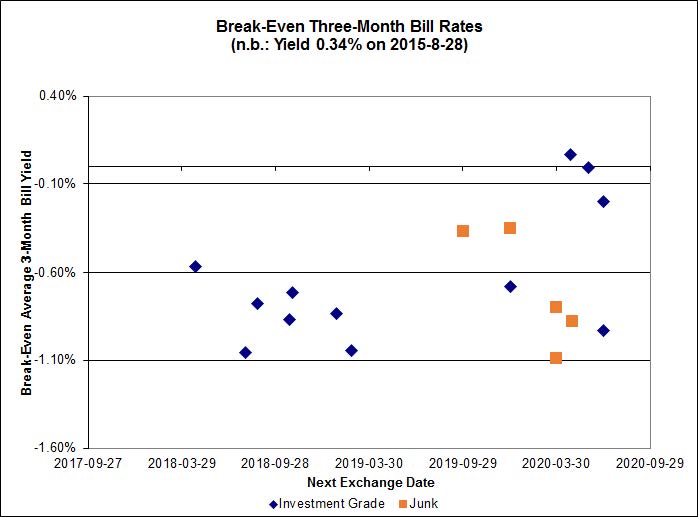

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.63%, with no outliers. Note that the distribution is bimodal, with NVCC non-compliant bank issues averaging -0.84% and the unregulated issues averaging -0.35%. There is one junk outlier below -1.60%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1907 % | 1,631.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1907 % | 2,852.6 |

| Floater | 4.50 % | 4.57 % | 57,945 | 16.21 | 3 | 0.1907 % | 1,734.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0679 % | 2,765.9 |

| SplitShare | 4.65 % | 5.19 % | 57,953 | 3.12 | 3 | -0.0679 % | 3,241.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0679 % | 2,529.1 |

| Perpetual-Premium | 5.74 % | 5.67 % | 62,665 | 14.03 | 9 | -0.1591 % | 2,478.3 |

| Perpetual-Discount | 5.50 % | 5.57 % | 78,408 | 14.56 | 29 | 0.1241 % | 2,567.4 |

| FixedReset | 4.98 % | 4.28 % | 200,504 | 15.76 | 87 | 0.8109 % | 2,122.9 |

| Deemed-Retractible | 5.16 % | 5.32 % | 101,213 | 5.56 | 34 | 0.4990 % | 2,565.6 |

| FloatingReset | 2.38 % | 3.52 % | 47,730 | 5.96 | 9 | 0.4220 % | 2,186.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| HSE.PR.C | FixedReset | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 4.73 % |

| MFC.PR.F | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.11 Bid-YTW : 7.53 % |

| TRP.PR.B | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 12.10 Evaluated at bid price : 12.10 Bid-YTW : 4.03 % |

| PVS.PR.D | SplitShare | -1.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 24.01 Bid-YTW : 5.27 % |

| TD.PR.Y | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.70 Bid-YTW : 3.21 % |

| BAM.PF.B | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 4.41 % |

| RY.PR.N | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 24.23 Evaluated at bid price : 24.60 Bid-YTW : 5.06 % |

| TD.PF.A | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.04 Evaluated at bid price : 21.04 Bid-YTW : 3.67 % |

| MFC.PR.I | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.09 Bid-YTW : 5.26 % |

| PWF.PR.T | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 22.57 Evaluated at bid price : 23.31 Bid-YTW : 3.38 % |

| HSE.PR.G | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.82 Evaluated at bid price : 22.25 Bid-YTW : 4.75 % |

| FTS.PR.K | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 3.92 % |

| PVS.PR.B | SplitShare | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 4.60 % |

| GWO.PR.H | Deemed-Retractible | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.63 Bid-YTW : 6.35 % |

| TD.PF.B | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 3.67 % |

| SLF.PR.A | Deemed-Retractible | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 6.57 % |

| ENB.PR.H | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 5.11 % |

| MFC.PR.C | Deemed-Retractible | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.96 Bid-YTW : 6.85 % |

| NA.PR.S | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 3.87 % |

| ENB.PR.J | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.09 Evaluated at bid price : 17.09 Bid-YTW : 5.03 % |

| RY.PR.M | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.97 Evaluated at bid price : 22.50 Bid-YTW : 3.67 % |

| FTS.PR.H | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 3.64 % |

| BMO.PR.S | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.65 Evaluated at bid price : 21.93 Bid-YTW : 3.56 % |

| GWO.PR.R | Deemed-Retractible | 1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 6.44 % |

| RY.PR.Z | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 3.56 % |

| CM.PR.Q | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 22.29 Evaluated at bid price : 23.01 Bid-YTW : 3.73 % |

| GWO.PR.G | Deemed-Retractible | 1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.93 Bid-YTW : 5.95 % |

| GWO.PR.Q | Deemed-Retractible | 1.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.04 Bid-YTW : 5.84 % |

| BIP.PR.A | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.44 Evaluated at bid price : 21.72 Bid-YTW : 4.88 % |

| ENB.PR.Y | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 5.22 % |

| TD.PF.E | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 22.80 Evaluated at bid price : 24.08 Bid-YTW : 3.60 % |

| HSE.PR.A | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 13.90 Evaluated at bid price : 13.90 Bid-YTW : 4.33 % |

| MFC.PR.M | FixedReset | 2.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.26 Bid-YTW : 6.11 % |

| MFC.PR.N | FixedReset | 2.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.81 Bid-YTW : 6.34 % |

| ENB.PF.A | FixedReset | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 5.16 % |

| ENB.PF.C | FixedReset | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.45 Evaluated at bid price : 17.45 Bid-YTW : 5.10 % |

| TD.PF.C | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.61 % |

| ENB.PR.F | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 15.53 Evaluated at bid price : 15.53 Bid-YTW : 5.28 % |

| TRP.PR.G | FixedReset | 2.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 21.08 Evaluated at bid price : 21.08 Bid-YTW : 4.33 % |

| ENB.PF.E | FixedReset | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.44 Evaluated at bid price : 17.44 Bid-YTW : 5.15 % |

| MFC.PR.K | FixedReset | 2.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.41 Bid-YTW : 6.37 % |

| ENB.PR.B | FixedReset | 2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 14.66 Evaluated at bid price : 14.66 Bid-YTW : 5.33 % |

| TRP.PR.F | FloatingReset | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 14.20 Evaluated at bid price : 14.20 Bid-YTW : 3.98 % |

| ENB.PR.P | FixedReset | 2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 15.85 Evaluated at bid price : 15.85 Bid-YTW : 5.22 % |

| GWO.PR.I | Deemed-Retractible | 3.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.05 Bid-YTW : 6.32 % |

| ENB.PF.G | FixedReset | 3.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.69 Evaluated at bid price : 17.69 Bid-YTW : 5.11 % |

| TRP.PR.A | FixedReset | 3.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.22 % |

| ENB.PR.N | FixedReset | 3.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 16.48 Evaluated at bid price : 16.48 Bid-YTW : 5.18 % |

| HSE.PR.E | FixedReset | 4.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 22.00 Evaluated at bid price : 22.50 Bid-YTW : 4.70 % |

| ENB.PR.D | FixedReset | 4.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 15.12 Evaluated at bid price : 15.12 Bid-YTW : 5.20 % |

| ENB.PR.T | FixedReset | 5.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 16.45 Evaluated at bid price : 16.45 Bid-YTW : 5.04 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.I | FixedReset | 106,543 | TD crossed 100,000 at 22.26. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 4.94 % |

| CM.PR.P | FixedReset | 83,470 | TD crossed 49,800 at 20.80; Scotia crossed 15,000 at 20.81. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 3.71 % |

| TRP.PR.D | FixedReset | 36,364 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.28 % |

| ENB.PR.Y | FixedReset | 31,011 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 5.22 % |

| BAM.PR.T | FixedReset | 28,650 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-08-28 Maturity Price : 17.04 Evaluated at bid price : 17.04 Bid-YTW : 4.60 % |

| MFC.PR.F | FixedReset | 24,347 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.11 Bid-YTW : 7.53 % |

| There were 26 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.K | Floater | Quote: 10.40 – 13.24 Spot Rate : 2.8400 Average : 1.6026 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 21.51 – 22.90 Spot Rate : 1.3900 Average : 0.8039 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 21.08 – 23.00 Spot Rate : 1.9200 Average : 1.3507 YTW SCENARIO |

| RY.PR.M | FixedReset | Quote: 22.50 – 23.50 Spot Rate : 1.0000 Average : 0.6325 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 21.76 – 22.79 Spot Rate : 1.0300 Average : 0.6957 YTW SCENARIO |

| NA.PR.W | FixedReset | Quote: 20.20 – 21.15 Spot Rate : 0.9500 Average : 0.6260 YTW SCENARIO |