Silver linings were tough to come by in the September jobs data. Payrolls came in at a much-weaker-than-forecast 142,000, while August and July figures were revised down. Wage growth was nonexistent for the month, with average hourly earnings actually falling by a penny on average.

The softness in manufacturing endured, with factory payrolls falling by 9,000 when they were expected to show no change. With dollar appreciation and sluggish overseas growth providing headwinds, it was the biggest back-to-back decline since 2010.

Even service industries, which make up the lion’s share of the economy and are more shielded from global weakness, seem to have shifted into a lower gear. Payroll growth there has slowed for four straight months, the longest such streak since 2001.

Dan Gallagher, whose comments on Dodd-Frank were reported on August 4, has reached the end of the line:

Today is my final day as a Commissioner of the U.S. Securities and Exchange Commission. It has been a privilege and an honor to serve the public during such an important time. I thank my fellow Commissioners and the staff for the time spent working together on critical issues facing investors, issuers, and the markets. After having spent so many years at the SEC in various capacities, departing is certainly bittersweet. As a former SEC staffer, I have particularly enjoyed working so closely again with the Commission’s excellent staff.

I must confess that the more I think about the VW diesel emissions scandal, the less I understand it. A piece in the Globe notes:

Volkswagen’s cheating on emissions tests has soured the European car industry’s heavy bet on diesel, with Renault, Peugeot and Fiat Chrysler potentially facing bigger long-term setbacks than the company that sparked the crisis.

In the face of that perceived injustice, tensions are mounting behind the united facade that European manufacturers present to regulators, some of their representatives say.

It will be recalled that the whistle-blower was an independent environmental agency that tested the VWs in the expectation that everything would be peachy keen; the VWs had been selling really well because they got great fuel economy AND low emissions AND good performance.

I’m not an automotive engineer, but to me that sounds like a ‘Pick Two’ problem. But the implication is that not once, at any of VWs three competitors, did a senior vice president pound the table and scream ‘Dammit, Hans, they’re killing us on sales volume! Why can’t we do that?’ And not once did the senior project engineer confess ‘Honestly, Gunther, I just can’t figure it out. Mind if I buy one and take it apart?’

It just doesn’t make sense to me.

It was a moderately good day for the Canadian preferred share market, with PerpetualDiscounts up 31bp, FixedResets gaining 14bp and DeemedRetractibles off 7bp. These figures mask an awful lot of violent churning with respect to individual issues though, as illustrated by the lengthy Performance Highlights table. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

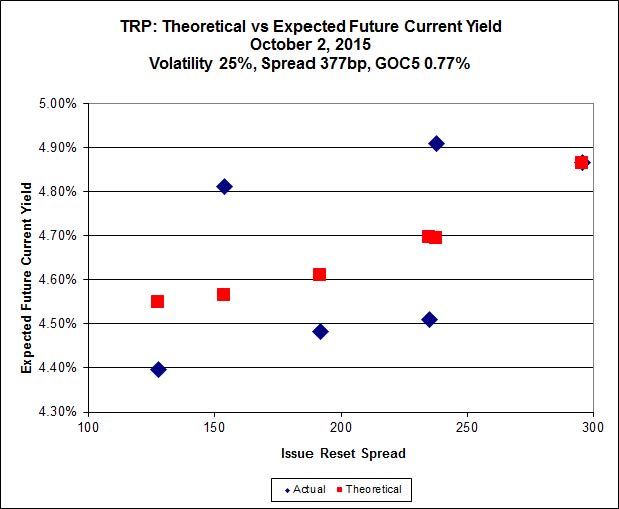

Here’s TRP:

Click for Big

Implied Volatility rocketed today, reaching an unreasonable level.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.30 to be $0.69 rich, while TRP.PR.D (target of a sell programme today; see the Performance Highlights table), resetting 2019-4-30 at +238, is $0.74 cheap at its bid price of 16.04.

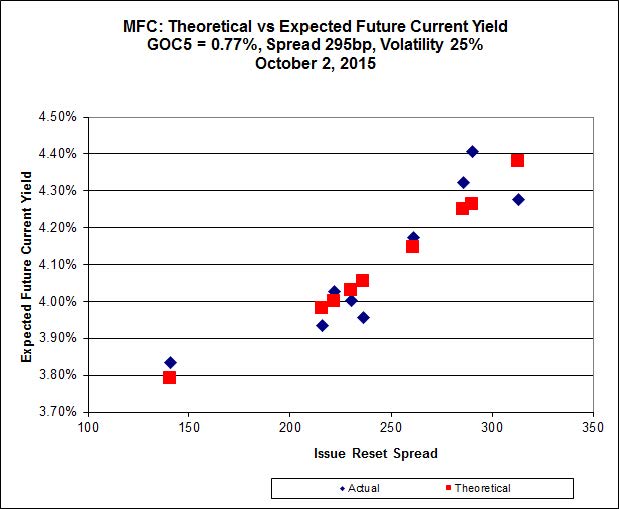

Click for Big

Another good fit today for MFC, with Implied Volatility climbing a bit.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 22.80 to be 0.54 rich, while MFC.PR.G resetting at +280bp on 2016-12-19, is bid at 20.82 to be 0.70 cheap.

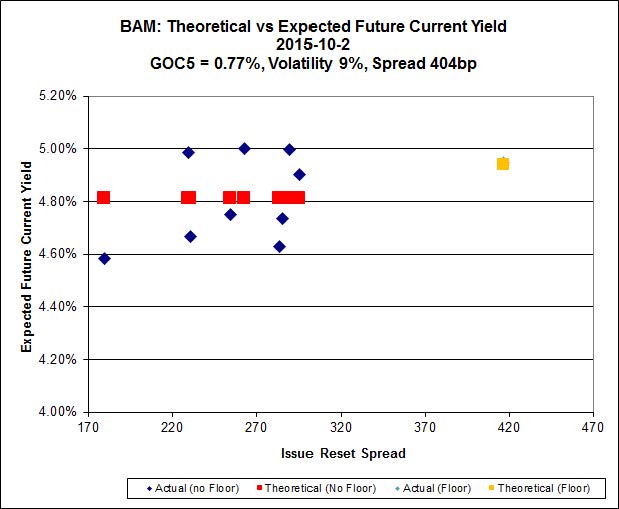

Click for Big

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PF.A, resetting at +290bp on 2018-9-30, bid at 18.36 to be $0.71 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.50 and appears to be $0.74 rich.

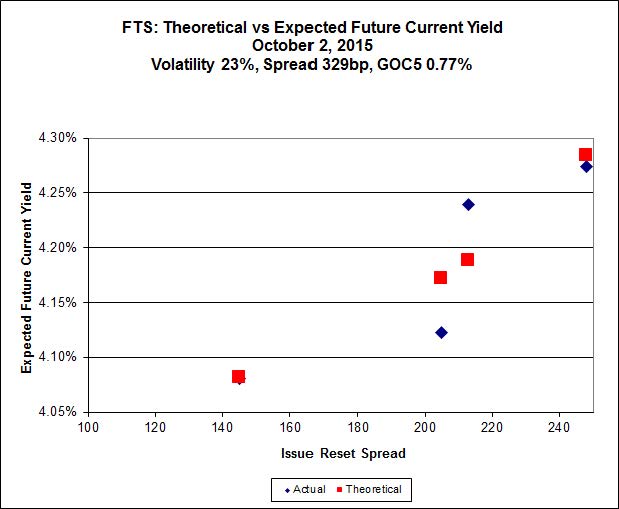

Click for Big

Implied Volatility leaped upwards today, from an unreasonably low to an unreasonably high level, as three of the four issues were featured in the Performance Highlights table – two winners, one loser.

FTS.PR.K, with a spread of +205bp, and bid at 17.10, looks $0.20 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.10 and is $0.21 cheap.

Click for Big

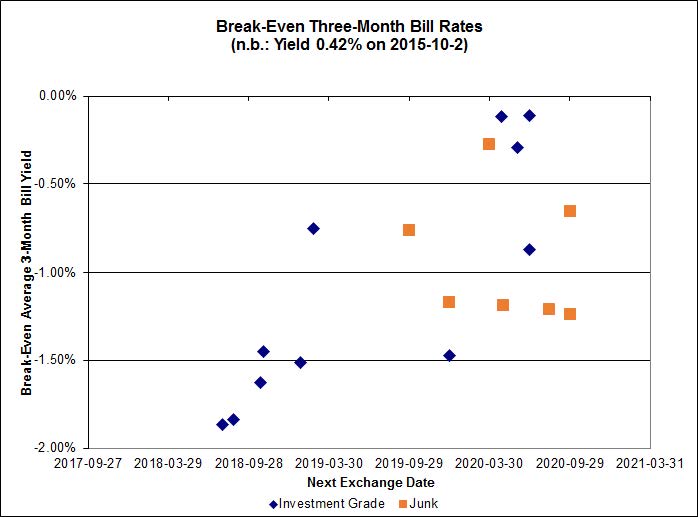

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.20%, with one outlier below -2.00%. The distribution is bimodal, with bank NVCC non-compliant pairs averaging -1.65% and other issues averaging -0.57%. There are three junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4266 % | 1,603.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4266 % | 2,803.7 |

| Floater | 4.63 % | 4.66 % | 63,259 | 16.16 | 3 | 0.4266 % | 1,704.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3078 % | 2,753.4 |

| SplitShare | 4.36 % | 5.00 % | 66,506 | 4.49 | 5 | -0.3078 % | 3,226.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3078 % | 2,517.7 |

| Perpetual-Premium | 5.84 % | 5.85 % | 54,429 | 13.86 | 5 | -0.0159 % | 2,466.2 |

| Perpetual-Discount | 5.70 % | 5.77 % | 74,723 | 14.24 | 33 | 0.3076 % | 2,490.7 |

| FixedReset | 5.18 % | 4.76 % | 186,416 | 15.07 | 76 | 0.1436 % | 1,966.3 |

| Deemed-Retractible | 5.24 % | 5.24 % | 97,799 | 5.50 | 33 | -0.0730 % | 2,538.8 |

| FloatingReset | 2.66 % | 4.64 % | 62,565 | 5.84 | 9 | 0.2205 % | 2,053.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.D | FixedReset | -5.26 % | Not real. The issue traded 47,944 shares today (consolidated exchanges) in a range of 16.43-95 before closing at 16.04-50, 9×2. It looks like there was aggressive selling by a programme run via RBC: twenty-five trades in the last twelve minutes, totalling 7,800 shares – we can’t really blame the market maker for suddenly remembering he had a dentist’s appointment. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 16.04 Evaluated at bid price : 16.04 Bid-YTW : 5.19 % |

| PWF.PR.P | FixedReset | -3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.23 % |

| TD.PF.D | FixedReset | -2.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.54 % |

| TRP.PR.E | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.88 % |

| FTS.PR.F | Perpetual-Discount | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 5.88 % |

| BAM.PR.X | FixedReset | -2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 4.96 % |

| FTS.PR.M | FixedReset | -2.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 4.58 % |

| MFC.PR.N | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.18 Bid-YTW : 6.95 % |

| MFC.PR.G | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.82 Bid-YTW : 6.22 % |

| MFC.PR.C | Deemed-Retractible | -1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 7.22 % |

| BAM.PF.B | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.30 % |

| BMO.PR.T | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 4.38 % |

| RY.PR.I | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 4.34 % |

| BMO.PR.Q | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.81 Bid-YTW : 6.34 % |

| PVS.PR.B | SplitShare | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.45 Bid-YTW : 5.22 % |

| SLF.PR.C | Deemed-Retractible | -1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.30 Bid-YTW : 7.31 % |

| MFC.PR.M | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.78 Bid-YTW : 6.61 % |

| TD.PR.Y | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 3.98 % |

| SLF.PR.A | Deemed-Retractible | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.54 Bid-YTW : 6.82 % |

| BAM.PF.E | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.47 Evaluated at bid price : 17.47 Bid-YTW : 5.20 % |

| BAM.PF.G | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.96 % |

| GWO.PR.G | Deemed-Retractible | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 6.30 % |

| HSE.PR.E | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 21.28 Evaluated at bid price : 21.55 Bid-YTW : 5.11 % |

| TD.PF.F | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 22.66 Evaluated at bid price : 23.00 Bid-YTW : 5.41 % |

| RY.PR.N | Perpetual-Discount | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 22.48 Evaluated at bid price : 22.79 Bid-YTW : 5.51 % |

| BAM.PF.D | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 20.49 Evaluated at bid price : 20.49 Bid-YTW : 6.03 % |

| RY.PR.H | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.28 % |

| MFC.PR.F | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.21 Bid-YTW : 9.47 % |

| BMO.PR.W | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.32 Evaluated at bid price : 18.32 Bid-YTW : 4.38 % |

| BNS.PR.Y | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.49 Bid-YTW : 6.03 % |

| HSE.PR.G | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 21.99 Evaluated at bid price : 22.50 Bid-YTW : 4.86 % |

| BAM.PR.K | Floater | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 4.61 % |

| FTS.PR.G | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.53 % |

| TD.PF.C | FixedReset | 1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 4.38 % |

| NA.PR.Q | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 4.25 % |

| RY.PR.W | Perpetual-Discount | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.27 % |

| TRP.PR.F | FloatingReset | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 12.57 Evaluated at bid price : 12.57 Bid-YTW : 4.64 % |

| W.PR.J | Perpetual-Discount | 1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 22.06 Evaluated at bid price : 22.35 Bid-YTW : 6.28 % |

| W.PR.H | Perpetual-Discount | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 21.98 Evaluated at bid price : 22.21 Bid-YTW : 6.21 % |

| SLF.PR.H | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.69 Bid-YTW : 7.50 % |

| SLF.PR.J | FloatingReset | 1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.20 Bid-YTW : 9.59 % |

| FTS.PR.K | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.50 % |

| SLF.PR.I | FixedReset | 2.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.20 Bid-YTW : 6.44 % |

| TD.PF.E | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 21.33 Evaluated at bid price : 21.61 Bid-YTW : 4.28 % |

| TD.PF.B | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.31 % |

| CU.PR.H | Perpetual-Discount | 2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 22.65 Evaluated at bid price : 23.00 Bid-YTW : 5.79 % |

| RY.PR.M | FixedReset | 2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.40 % |

| BAM.PR.T | FixedReset | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 4.91 % |

| TRP.PR.A | FixedReset | 3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.76 % |

| IFC.PR.C | FixedReset | 5.59 % | Yes, there were trades at the 19.45 level – and above! However, only 1,350 shares were traded and the VWAP was a mere 19.17. Numbers can get unreliable in a thin market! YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.45 Bid-YTW : 6.81 % |

| TRP.PR.B | FixedReset | 5.90 % | Just a recovery from yesterday‘s shenanigans. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 11.66 Evaluated at bid price : 11.66 Bid-YTW : 4.49 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PF.H | FixedReset | 1,304,995 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 23.13 Evaluated at bid price : 24.96 Bid-YTW : 4.93 % |

| BMO.PR.R | FloatingReset | 100,200 | Scotia bought 100,000 from RBC at 21.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 4.70 % |

| RY.PR.P | Perpetual-Discount | 73,494 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 24.04 Evaluated at bid price : 24.40 Bid-YTW : 5.39 % |

| TRP.PR.D | FixedReset | 47,944 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 16.04 Evaluated at bid price : 16.04 Bid-YTW : 5.19 % |

| RY.PR.Z | FixedReset | 32,530 | TD crossed 15,700 at 19.12. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 18.96 Evaluated at bid price : 18.96 Bid-YTW : 4.25 % |

| TRP.PR.E | FixedReset | 29,350 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-10-02 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.88 % |

| There were 33 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PF.D | FixedReset | Quote: 20.00 – 21.00 Spot Rate : 1.0000 Average : 0.6204 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 17.10 – 17.85 Spot Rate : 0.7500 Average : 0.5031 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 12.00 – 12.57 Spot Rate : 0.5700 Average : 0.3515 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 15.70 – 16.30 Spot Rate : 0.6000 Average : 0.3884 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 21.10 – 21.61 Spot Rate : 0.5100 Average : 0.3031 YTW SCENARIO |

| MFC.PR.K | FixedReset | Quote: 18.56 – 19.13 Spot Rate : 0.5700 Average : 0.3647 YTW SCENARIO |