As I reported previously, there was a 15% conversion to GWO.PR.O, the FloatingReset, from GWO.PR.N, the FixedReset, following the latter issue’s reset to 2.176% for the next five years, a reduction of just over 40% in the dividend rate.

GWO.PR.O will pay 3-month bills +130bp, reset quarterly. It will be tracked by HIMIPref™ and has been assigned to the FloatingReset subindex.

Note that since the issue is issued by an insurance holding company and is not convertible into common at the option of the issuer, I consider it to have a “Deemed Maturity” 2025-1-31 (this date may change in the future). This is due to my belief that OSFI will eventually extend the Non-Viability Contingent Capital (NVCC) rules to insurers and insurance holding companies. There is a brief explanation of this on the PrefLetter website (under the heading “DeemedRetractibles”) and with more detailed argument and progress reports on international negotiations in every edition of PrefLetter.

I will note that the market does not share my views regarding future application of the NVCC rules insurers and insurance issues trade very similarly to perpetuals.

GWO.PR.O was listed today although, as is normally the case, there was no trading because brokerage customers haven’t actually seen the shares in their accounts yet – and, presumably, having recently made the decision to convert, are less likely than most to want to sell.

The issue closed with the extraordinary quote of 13.10-21.00, 10×2. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

Vital Statistics are:

| GWO.PR.O | FloatingReset | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.10 Bid-YTW : 9.80 % |

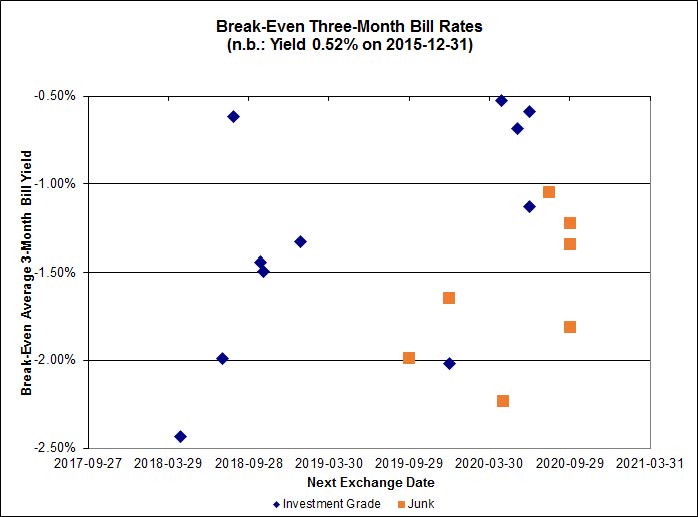

Strong Pair theory, for which a calculator is available, allows us to examine the consistency of the bid price of GWO.PR.N with GWO.PR.O; they are interconvertible in the future. The bids of 13.99 and 13.00, respectively, allow us to gauge that total returns over the next five years will be equal if the three-month Bill Yield exceeds -0.07%. While this is a laughably low figure, it is not as low as that of other investment-grade FixedReset/FloatingReset pairs.

Click for Big

Whatever one might think of the probability of the bill yield averaging over -0.07% over the next five years, it is clearly rational to believe that the break-even yield will decline in the future, to become more comparable to the break-even yield of the issues’ peers. This implies an expectation that the bid price of the FloatingReset, GWO.PR.O, will decline in the next little while relative to that of GWO.PR.N [note the word “relative”! They could both increase or both decrease!]. In fact, keeping the bid price of GWO.PR.N constant at 13.99, a decline of the bid for GWO.PR.O to 11.50 will bring the break-even yield of the pair to -1.50%, the centerpoint of the chart.

In other words, I suggest that although GWO.PR.O is currently cheap relative to GWO.PR.N, there is good reason to believe it will get cheaper!

If floaters are so low right now, as indicated by such a low break even rate, wouldn’t it makes sense to convert all strong pairs holdings into floaters and readjust holdings again when the prices come more into alignment , or at next conversion date?

Yes

wouldn’t it makes sense to convert all strong pairs holdings into floaters

Yes, given a few conditions.

First, remember that the rich/cheap analysis of Strong Pairs only applies within that pair; e.g., if X and Y form a strong pair, one will generally be better than the other, but there is no information about how good this one is versus every other letter of the alphabet.

Also, you must have a long time horizion, because sometimes these things don’t converge until the next Exchange Date – and sometimes not even then!

And, in the interim, you must be prepared for volatility of income from the FixedReset.

But … if you like X on its own merits, and you consider [given your view on average 3-month bill rates vs. the break-even rate] that Y is cheaper … then yes, it makes sense to swap the issues on the market.

I kept all that in mind, but it is a very easy thing to forget, so thanks for the reminder.

Also, seeing as how many floaters are now yielding 3-5%, and the US is increasing rates which will presumably pressure Canada to follow suit soon, why isn’t everyone jumping on them?

Shhh… finish your buying, then tell everyone! 😉

fed says: “Also, seeing as how many floaters are now yielding 3-5%, and the US is increasing rates which will presumably pressure Canada to follow suit soon, why isn’t everyone jumping on them?”

Perhaps, everyone remembers what a slam-dunk fixed rate resets were a year ago, and look what happened there.

everyone remembers what a slam-dunk fixed rate resets were a year ago, and look what happened there.

Yes. *sigh*

I was telling a client today that I can do a reasonable amount of hand-waving to explain the market up to mid-year; but after mid-year, I’m lost. It seems like pure emotion.

Remember too that Floating Rate preferred shares are not Money Market vehicles; they demonstrated this during the Credit Crunch.

Thanks for the articles. I had already seen them and found them helpful.

I am wondering what is the rate declared on GWO.PR.O. I can’t seem to find it.

GWO.PR.O resets every 3 months at a rate of 1.30% over 3 month T-bills. It think it’s going to pay 10.9 cents dividend (= 1.74%) at the end of March and then reset again.

Thanks, but I am wondering where I can find the initial exDiv date and dividend on these new (and there will soon be many more) 3m floaters. Any ideas?

Back in December, James posted…

The floating dividend rate for the period commencing on December 31, 2015 and ending on March 30, 2016 applicable to any Series O Shares issued on December 31, 2015 will be 1.742% per annum (or $0.108578 per Series O Share). The 1.742% annual rate is equal to the sum of the T-Bill Rate (as defined in the Series O Share Conditions) on December 1, 2015 plus 1.30%.

… which is presumably an announcement on the Great West web site. I’m not sure when they will post the new dividend for Apr/May/Jun but I think the current 3 month T-bill is at about 0.47% so, if it stayed the same, the new June dividend will be about ((1.30+0.47) * 25 /4 =) 11.06 cents

I usually get my dividend amounts and ex-div dates from the tmxmoney web site (http://web.tmxmoney.com/quote.php?qm_symbol=gwo.pr.o) – not sure how reliable they are. You can always get dividend info from the individual company’s web site but it’s easier to just look for a single source of info. Anybody have any suggestions for a better source?

–