Employers in December added 292,000 workers, exceeding the highest estimate in a Bloomberg survey, and payrolls for the previous two months were revised higher, a Labor Department report showed on Friday. The jobless rate held at 5 percent as people entering the labor force found work. At the same time, worker pay disappointed, rising less than forecast from a year earlier.

…

Labor Department revisions to prior reports added a total of 50,000 jobs to payrolls in November and October. For all of 2015, employment climbed by 2.65 million after a 3.1 million gain in 2014, for the best back-to-back years since 1998-99.

…

While employers continue to aggressively add to headcounts, worker pay has yet to show a sustainable pickup. Average hourly earnings in December were unchanged from the prior month and increased 2.5 percent from a year earlier. The median forecast called for a 2.7 percent year-over-year gain.

…

Among measures of labor-market slack, the number of Americans who are working part time though would rather have a full time position, or the measure known as part-time for economic reasons, eased to 6.02 million from 6.09 million.The underemployment rate — which includes part-time workers who’d prefer a full-time position and people who want to work but have given up looking — held at 9.9 percent.

…

Hiring gains last month were broad-based, with construction adding 45,000 jobs, health-care providers taking on 52,600 and temporary help services boosting headcounts by 34,400. Factories even added the most jobs — 8,000 — in five months.

There will even be job openings for Secret Policemen and government propagandists!

The Obama administration on Friday asked some of the nation’s biggest technology companies for help in the fight against terrorism as it announced steps to thwart the recruitment and radicalization of extremists.

Top administration officials met in San Jose, California with representatives of Twitter Inc., Apple Inc., Facebook Inc. and other Silicon Valley companies. In a seven-page memo sent in advance, the companies were asked for ideas on how extremist content online can be identified and removed, as well as help creating alternative messages, according to excerpts of the document obtained and described to Bloomberg News.

“We are interested in exploring all options with you for how to deal with the growing threat of terrorists and other malicious actors using technology,” the memo said. “Are there high-level principles we could agree on for working through these problems together? And are there technologies that could make it harder for terrorists to use the Internet to mobilize, facilitate, and operationalize?”

Meanwhile, Canadians got government work:

Canada added 23,000 jobs in December, surpassing expectations due to gains in self-employment, health care and education.

December’s gains helped reverse huge election-related job declines in November and capped a tumultuous year for job creation. The country added a total of 158,000 jobs in 2015, an increase of 0.9 per cent over the previous year, despite mass layoffs in the energy sector.

…

Hiring in the private sector was flat compared with the previous year while the public sector added 41,000 new jobs, an increase of 1.1 per cent, and self-employment grew by 92,000 jobs, or 3.4 per cent.

But soon we’ll be able to beg tourists for American dollars!

Toronto has made it onto the New York Times’s list of 52 top global tourist destinations for 2016, at No. 7.

I want to see the sights of 10-15 years ago again … walk around downtown, see a tour bus on every corner, theatre industry booming … who knows, maybe they’ll even start up a Toronto-Rochester catamaran!

But anyway, despite the encouraging job news, equities fell:

U.S. stocks tumbled in a late-afternoon selloff that sent major equity indexes to their worst weekly declines in more than four years, as investors found little relief in moves by China to restore calm to its sinking markets and data that showed resilience in the U.S labor market.

…

The S&P 500 dropped 1.1 percent to 1,922.03 at 4 p.m. in New York, and fell 6 percent for the week. The Dow Jones Industrial Average sank 167.65 points, or 1 percent, to 16,346.45. The index lost more than 1,000 points this week in its worst opening five-days to a year ever. The Nasdaq Composite Index declined 1 percent, stretching its losing streak to seven days, the longest since 2011.

…

The S&P 500 has fallen 7.3 percent since the Federal Reserve raised interest rates last month for the first time in nearly a decade. The central bank balked at boosting borrowing costs in September in part due to turbulence sparked by China’s August currency devaluation. The poor start to 2016 has left the benchmark index 9.8 percent below its all-time high set in May after coming within 1 percent of the record as recently as November. It’s 2.9 percent above the August bottom.

And now there are calls for fiscal stimulus:

[Central Banks] have only themselves to blame for becoming agents of volatility, according to Christopher Walen, senior managing director at Kroll Bond Rating Agency Inc.

He told Bloomberg Television this week that officials’ willingness to keep interest rates near zero and repeatedly buy bonds and other assets meant they became “way too involved in the global economy” and should have left more of the lifting work to governments.

The handover to looser fiscal policy now needs to happen if economic growth and inflation are to get the spur they need, said Martin Malone, global macro policy strategist at London-based brokerage Mint Partners.

“Major economies have exhausted monetary and foreign-exchange policies,” he said. “Government action must take over from central-bank policies, triggering more confident private-sector investment and spending.”

The influence of central bankers was underscored by a report this week from currency strategists at HSBC Holdings Plc, which calculated foreign-exchange markets are more sensitive to interest-rate decision-making than at any time in the last 15 years.

But it will take a long time for the Fed to shrink its balance sheet:

It will take the U.S. central bank at least six years to reduce its bloated balance sheet back to more a normal size, San Francisco Federal Reserve Bank President John Williamssaid, as officials take a gradual approach to withdrawing crisis-level stimulus.

“Our plan is to shrink the balance sheet ‘organically,’ if you will, through the maturation of the assets,” Williams said in the text of remarks Friday in Santa Barbara, California. “It’s likely going to take at least six years to get the balance sheet back to normal, which is in keeping with the overall approach to removing accommodation gradually.”

The Federal Reserve is slowly weaning the economy off of ultra-easy monetary policy that saw it hold interest rates near zero for seven years and balloon the balance sheet to around $4.5 trillion through three rounds of buying mainly Treasuries and mortgage-backed securities. Officials took a major step in December, raising interest rates for the first time since 2006, and said they’ll wait until the process of policy normalization is well under way before beginning to allow excess balance-sheet holdings to roll off.

“The Fed has started the process of raising interest rates, but the path to normal will be gradual,” Williams said Friday.

Dividend Split Corp. II, proud issuer of DF.PR.A has been confirmed at Pfd-3(Low) by DBRS:

DBRS Limited (DBRS) has today confirmed the rating of the Preferred Shares issued by Dividend 15 Split Corp. II (the Company) at Pfd-3 (low). In November and December of 2006, the Company issued 5.6 million Preferred Shares (at $10.00 each) and an equal number of Class A Shares (at $15.00 each). The final redemption date for both classes of shares issued is December 1, 2019 (extended from December 1, 2014, at a special meeting of shareholders on June 3, 2013).

…

Holders of the Class A Shares receive regular monthly cash dividends targeted to be $0.10 per Class A Share to yield 8% per annum on the issue price of $15.00. No monthly distributions to the Class A Shares are made if the dividends of the Preferred Shares are in arrears or the NAV of the Company falls below 1.5 times the principal amount of the outstanding Preferred Shares. Furthermore, no special distributions are made if the NAV of the Company is below $25.00. The NAV as of December 15, 2015, was $14.52, resulting in no distributions paid to the Class A Shares for December 31, 2015. On maturity, the holders of the Preferred Shares will be entitled to the value of the Company, up to the face value of the Preferred Shares, in priority to the holders of the Class A Shares. Holders of the Class A Shares will receive all remaining value of the Company.The confirmation of the Pfd-3 (low) rating of the Preferred Shares is based primarily on the downside protection available and the additional protection provided by the asset coverage test, which does not permit any distributions to holders of the Class A Shares if the NAV of the Company falls below $15.00.

The year-end NAVPU for DF.PR.A was 14.51; the sort-of comparable, XDV is down about 4% since then.

But for now, Canadian preferred share investors can look forward to two days with no losses!

Click for Big

It was another horrid day for Canadian preferred share investors, with PerpetualDiscounts down 32bp, FixedResets losing 84bp and DeemedRetractibles off 27bp. The Performance Highlights table is lengthy. Volume was very low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

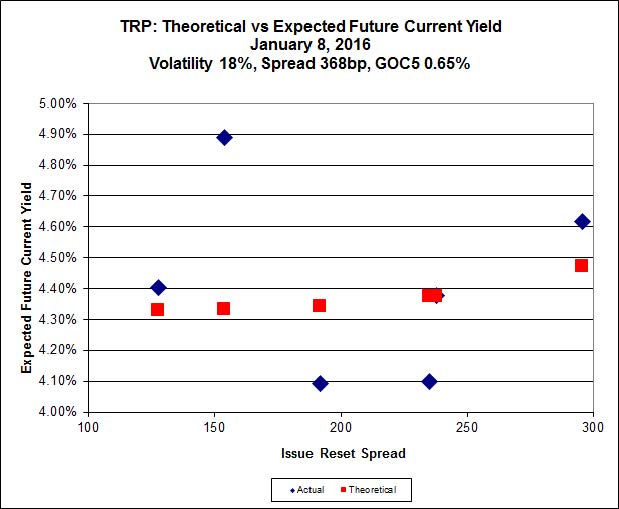

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.30 to be $1.15 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.44 cheap at its bid price of 11.20.

Click for Big

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 18.98 to be 0.56 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 19.34 to be 1.03 cheap.

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.18 to be $1.10 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 18.34 and appears to be $0.69 rich.

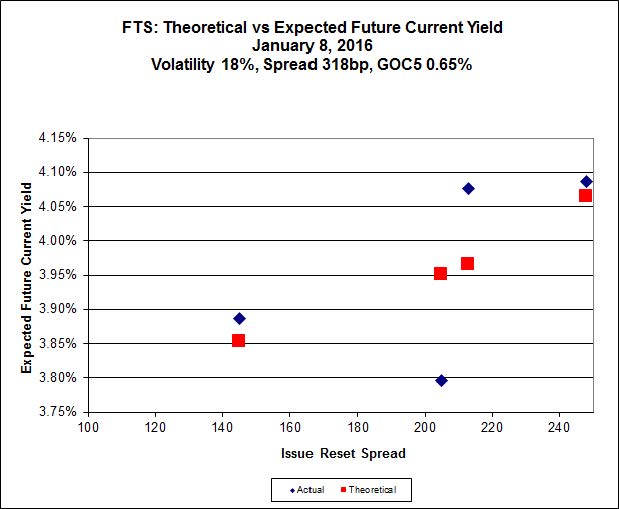

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 17.78, looks $0.69 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.05 and is $0.48 cheap.

Click for Big

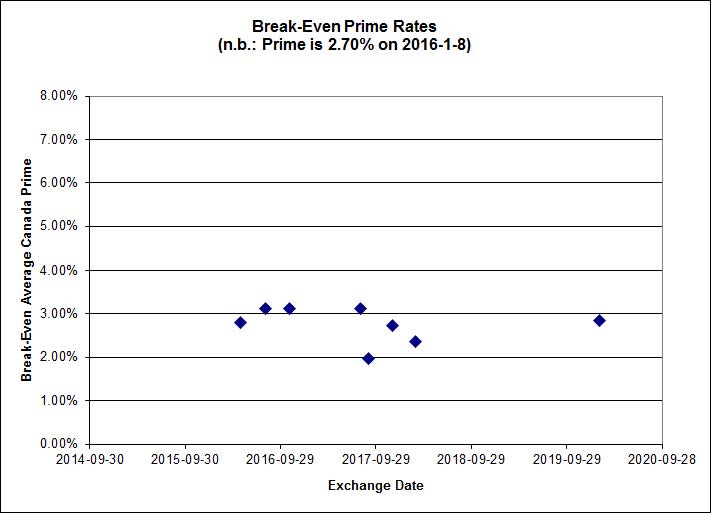

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.27%, with three outliers below -2.00%. There is one junk outlier below -2.00% and three above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

But now … on to PrefLetter.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.76 % | 5.77 % | 26,798 | 16.93 | 1 | 1.7857 % | 1,633.9 |

| FixedFloater | 7.32 % | 6.50 % | 32,713 | 15.58 | 1 | -6.7529 % | 2,666.4 |

| Floater | 4.29 % | 4.49 % | 80,694 | 16.47 | 4 | 0.0454 % | 1,781.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0069 % | 2,735.7 |

| SplitShare | 4.83 % | 5.77 % | 71,882 | 1.81 | 6 | 0.0069 % | 3,201.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0069 % | 2,497.8 |

| Perpetual-Premium | 5.87 % | 5.66 % | 86,132 | 2.73 | 6 | -0.0067 % | 2,515.4 |

| Perpetual-Discount | 5.72 % | 5.79 % | 94,230 | 14.23 | 34 | -0.3168 % | 2,520.5 |

| FixedReset | 5.33 % | 4.63 % | 239,519 | 14.87 | 81 | -0.8361 % | 1,935.3 |

| Deemed-Retractible | 5.27 % | 5.15 % | 121,027 | 5.28 | 34 | -0.2747 % | 2,552.5 |

| FloatingReset | 2.87 % | 4.64 % | 63,131 | 5.62 | 13 | -1.3458 % | 2,057.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.G | FixedFloater | -6.75 % | Just more nonsense from Nonsense Central. The issue traded 2,000 shares in a range of 13.75-35 before closing at 12.98-14.35, 3×4; this is particularly ridiculous in light of the fact that according to TMX figures, BAM.PR.E, this issue’s Strong Pair, had a very good day. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO |

| BAM.PF.G | FixedReset | -4.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 4.82 % |

| RY.PR.K | FloatingReset | -4.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 5.21 % |

| MFC.PR.G | FixedReset | -3.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.34 Bid-YTW : 7.15 % |

| TRP.PR.F | FloatingReset | -3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 4.64 % |

| CIU.PR.C | FixedReset | -3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 11.91 Evaluated at bid price : 11.91 Bid-YTW : 4.33 % |

| CU.PR.C | FixedReset | -3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.58 % |

| BAM.PF.B | FixedReset | -3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.79 % |

| BMO.PR.T | FixedReset | -2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.71 Evaluated at bid price : 17.71 Bid-YTW : 4.41 % |

| SLF.PR.I | FixedReset | -2.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.52 Bid-YTW : 7.52 % |

| BAM.PF.A | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.76 % |

| MFC.PR.N | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.61 Bid-YTW : 7.38 % |

| MFC.PR.M | FixedReset | -2.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.98 Bid-YTW : 7.17 % |

| BAM.PR.Z | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.16 Evaluated at bid price : 19.16 Bid-YTW : 4.91 % |

| FTS.PR.H | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 13.51 Evaluated at bid price : 13.51 Bid-YTW : 4.10 % |

| MFC.PR.I | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.07 Bid-YTW : 6.70 % |

| PWF.PR.L | Perpetual-Discount | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 21.48 Evaluated at bid price : 21.74 Bid-YTW : 5.87 % |

| BAM.PF.E | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 18.34 Evaluated at bid price : 18.34 Bid-YTW : 4.77 % |

| BIP.PR.A | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 18.88 Evaluated at bid price : 18.88 Bid-YTW : 5.72 % |

| SLF.PR.J | FloatingReset | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.90 Bid-YTW : 10.15 % |

| CIU.PR.A | Perpetual-Discount | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 5.75 % |

| BAM.PF.F | FixedReset | -1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.88 Evaluated at bid price : 19.88 Bid-YTW : 4.70 % |

| PWF.PR.A | Floater | -1.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 12.38 Evaluated at bid price : 12.38 Bid-YTW : 3.86 % |

| BAM.PR.T | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 15.92 Evaluated at bid price : 15.92 Bid-YTW : 4.83 % |

| TD.PF.C | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.62 Evaluated at bid price : 17.62 Bid-YTW : 4.37 % |

| HSE.PR.A | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 11.12 Evaluated at bid price : 11.12 Bid-YTW : 5.40 % |

| TD.PF.E | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 20.12 Evaluated at bid price : 20.12 Bid-YTW : 4.44 % |

| IAG.PR.G | FixedReset | -1.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.74 Bid-YTW : 6.84 % |

| BNS.PR.Q | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.58 Bid-YTW : 4.00 % |

| TRP.PR.C | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 11.20 Evaluated at bid price : 11.20 Bid-YTW : 4.91 % |

| SLF.PR.H | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.16 Bid-YTW : 8.66 % |

| TRP.PR.B | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 10.96 Evaluated at bid price : 10.96 Bid-YTW : 4.55 % |

| TRP.PR.D | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.31 Evaluated at bid price : 17.31 Bid-YTW : 4.63 % |

| GWO.PR.Q | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 6.70 % |

| GWO.PR.R | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.11 Bid-YTW : 7.23 % |

| BNS.PR.R | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.07 Bid-YTW : 3.88 % |

| SLF.PR.D | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.80 Bid-YTW : 7.74 % |

| IAG.PR.A | Deemed-Retractible | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 7.21 % |

| TD.PF.A | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.99 Evaluated at bid price : 17.99 Bid-YTW : 4.30 % |

| BNS.PR.A | FloatingReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.10 Bid-YTW : 4.59 % |

| POW.PR.B | Perpetual-Discount | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.86 % |

| TRP.PR.A | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 4.35 % |

| CU.PR.E | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 21.53 Evaluated at bid price : 21.53 Bid-YTW : 5.77 % |

| GWO.PR.I | Deemed-Retractible | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 7.51 % |

| RY.PR.M | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.47 % |

| BNS.PR.C | FloatingReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 4.70 % |

| CM.PR.P | FixedReset | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.67 Evaluated at bid price : 17.67 Bid-YTW : 4.37 % |

| TD.PR.T | FloatingReset | -1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 4.45 % |

| TRP.PR.E | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 4.44 % |

| TD.PF.D | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.29 Evaluated at bid price : 19.29 Bid-YTW : 4.52 % |

| BAM.PR.R | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 15.18 Evaluated at bid price : 15.18 Bid-YTW : 4.96 % |

| TD.PR.Z | FloatingReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.60 Bid-YTW : 4.62 % |

| SLF.PR.C | Deemed-Retractible | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.04 Bid-YTW : 7.57 % |

| GWO.PR.P | Deemed-Retractible | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.70 Bid-YTW : 6.22 % |

| SLF.PR.B | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.17 Bid-YTW : 7.19 % |

| SLF.PR.A | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.18 Bid-YTW : 7.12 % |

| PWF.PR.E | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 23.17 Evaluated at bid price : 23.47 Bid-YTW : 5.86 % |

| TRP.PR.G | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.74 % |

| CU.PR.D | Perpetual-Discount | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 5.77 % |

| HSE.PR.C | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 5.62 % |

| PWF.PR.T | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 3.76 % |

| IFC.PR.C | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.30 Bid-YTW : 7.56 % |

| BNS.PR.N | Deemed-Retractible | 1.52 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-02-26 Maturity Price : 25.25 Evaluated at bid price : 25.45 Bid-YTW : -3.21 % |

| BAM.PR.E | Ratchet | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 25.00 Evaluated at bid price : 14.25 Bid-YTW : 5.77 % |

| VNR.PR.A | FixedReset | 3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 4.91 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.M | Deemed-Retractible | 115,800 | RBC crossed 98,000 at 24.60. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 4.86 % |

| RY.PR.Q | FixedReset | 84,345 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 5.04 % |

| BNS.PR.L | Deemed-Retractible | 74,544 | RBC bought 20,000 from Nesbitt at 24.50, then another 27,500 at 24.52. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.50 Bid-YTW : 4.86 % |

| NA.PR.Q | FixedReset | 65,285 | RBC crossed 40,000 at 24.23. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.03 Bid-YTW : 3.98 % |

| FTS.PR.J | Perpetual-Discount | 44,500 | Desjardins crossed 40,000 at 21.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 21.47 Evaluated at bid price : 21.80 Bid-YTW : 5.50 % |

| TD.PF.B | FixedReset | 38,613 | Scotia crossed 25,000 at 18.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-08 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 4.30 % |

| There were 14 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.G | FixedFloater | Quote: 12.98 – 14.35 Spot Rate : 1.3700 Average : 0.8740 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 12.75 – 13.59 Spot Rate : 0.8400 Average : 0.5329 YTW SCENARIO |

| FTS.PR.M | FixedReset | Quote: 19.15 – 19.97 Spot Rate : 0.8200 Average : 0.5229 YTW SCENARIO |

| RY.PR.K | FloatingReset | Quote: 21.35 – 22.13 Spot Rate : 0.7800 Average : 0.5004 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 19.34 – 19.90 Spot Rate : 0.5600 Average : 0.3467 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 11.91 – 12.82 Spot Rate : 0.9100 Average : 0.7146 YTW SCENARIO |