Holy Smokes, that was a day and a half!

Stocks tumbled around the world, with U.S. equities sinking to their lowest levels since August, and bonds and gold jumped as oil’s plunge below $30 sent markets reeling. Treasuries extended gains as economic data and earnings added to concern that global growth is faltering.

The Dow Jones Industrial Average sank 391 points, European stocks fell into a bear market and the Shanghai Composite Index wiped out gains from an unprecedented state-rescue campaign as global equities added to the worst start to a year on record. Oil touched $29.28 a barrel before closing at a 12-year low. A measure of default risk for junk-rated U.S. companies surged to the highest in three years. Yields on 10-year Treasury notes dipped under 2 percent as doubts grow that the Federal Reserve will raise interest rates. Gold surged the most in six weeks.

…

Figures on retail sales and manufacturing Friday showed the U.S. economy ended the year on a weak note, and the start of 2016 wasn’t any better. Energy firms are laying off workers and currency markets from commodity-producing countries are in turmoil. The slump is also denting the outlook for inflation, causing traders to curb bets on how far the Fed will raise rates this year.

…

The Standard & Poor’s 500 Index plunged 2.2 percent at 4 p.m. in New York. The index fell as much as 3.3 percent before paring the slide in afternoon trading. It still capped a third weekly retreat and closed at the lowest level since Aug. 25, the day that marked the bottom of the summer selloff. U.S. equities markets are closed Monday for a federal holiday.The gauge has lost 12 percent from its May record, leaving it well short of sliding into a bear market. It capped a third weekly decline, the longest slide since July. The Dow tumbled 2.463 points as none of its 30 members advanced, while small caps added to a bear market.

…

West Texas Intermediate crude fell as much as 6.2 percent, before settling 5.7 percent lower at $29.42 a barrel. Brent fell 5.9 percent to $29.05 a barrel. The discount on global benchmark Brent reached a five-year high as Iran moved closer to restoring exports.

…

The Bloomberg Commodity Index, which measures returns on 22 raw materials, dropped 1.4 percent to the lowest level in data going back to 1991.

Given all that, effects on Canada followed:

The country’s benchmark Standard & Poor’s/TSX Composite Index fell 2.1 percent to 12,073.46 at 4 p.m. in Toronto, undoing Thursday’s rally and resuming a sell-off that’s pulled Canada into a bear market. Stocks plunged 7.2 percent this year and are down about 23 percent from a September 2014 record. The Canadian dollar slumped to a new 13-year low and yields on five-year government bonds fell to a record low of 0.511 percent on Wednesday as speculation builds the Bank of Canada will cut interest rates next week.

Canada’s economy, heavily weighed toward resource industries such as oil and mining, has been rocked by concerns about the slowdown in China that has pushed the price of West Texas Intermediate crude below $30 for the first time since 2003. Prices for Canada’s heavy crude, which trades at a discount to the U.S. benchmark, have sunk to around $15 a barrel.

And TransAlta common got thumped:

TransAlta Corp. slumped after the Alberta electricity generator cut its dividend in preparation for a phase-out of coal power in the province.

The shares fell 9.8 per cent to $3.94 at 11:40 a.m. in Toronto. It initially dropped 14 per cent, the most on an intraday basis since 2008, to a record low.

The quarterly dividend was cut to 4 cents a share from 18 cents, the company said in a release Thursday. Calgary– based TransAlta doesn’t expect to raise equity this year as the reduced dividend will “strengthen its balance sheet.”

…

TransAlta, which has more than 70 power plants in Canada, the U.S. and Australia, said it will negotiate with the government of Alberta to “ensure the company has the certainty and capacity” to invest in clean power.

…

The falling Canadian dollar is making it more expensive to build new wind and gas-powered generators, [TransAlta CEO Dawn] Farrell said. The cost to build new projects with those technologies is more than double the current market price for power of about C$30 a megawatt hour, she said.

Well, hey, maybe the Alberta government will get some advice from Ontario, and buy that Green Power for $90/MWH!

So the SEC is now awarding prizes to short-sale analysts!

The Securities and Exchange Commission today announced a whistleblower award of more than $700,000 to a company outsider who conducted a detailed analysis that led to a successful SEC enforcement action.

“The voluntary submission of high-quality analysis by industry experts can be every bit as valuable as first-hand knowledge of wrongdoing by company insiders,” said Andrew Ceresney, Director of the SEC’s Enforcement Division. “We will continue to leverage all forms of information and analysis we receive from whistleblowers to help better detect and prosecute federal securities law violations.”

No mission creep there, nope, not a bit of it.

On such a day, it is pleasant to think about drones, instead:

In October, a Kentucky judge dismissed criminal charges against a man who had shot down a drone flying over his property. Now the drone’s owner has brought a federal civil suit against the shooter, William Merideth, arguing that the Federal Aviation Administration is in charge of all airspace and that it allows drones to fly over private property.

All this amounts to a legal mess. The law, both state and federal, is still pretty unclear about where you can fly a drone, and what you as a citizen may do if a drone — probably with a camera on board — is hovering above your home.

What’s needed is a comprehensive legal regime that integrates state and federal jurisdictions. I want to propose the outlines of such a legal model, distinguishing what should belong to the feds and what should be within the realm of the states.

…

These features give reason for states to outlaw the use of drones to observe and record people on private property without their consent. Federal control over airways shouldn’t be interpreted to displace state law regulating drones. The federal interest is in flying from place to place, not hovering to get a better view.Protecting privacy at the state level will allow drones to fly freely without sacrificing the individual’s legitimate interest in being left alone.

…

The slogan for drone regulation should be: Feds to let them fly, states to protect what they see. The balance should let us a benefit from a new technology without sacrificing ourselves to it.

But we can reflect that comparing costs for university education is much like comparing costs for investment advice:

So since 2011, the federal government has required all schools to provide something called a net price calculator on their websites. You put in some financial data, and the calculator estimates what your actual cost would be, after any scholarships. If you aren’t among the very affluent and are applying to a private college, that net price can be tens of thousands of dollars below the list price.

Not long after the calculator became standard, a service called College Abacus emerged, allowing families to compare multiple schools at once. That spared them the laborious task of plugging the same data into multiple calculators many times over.

And how did many colleges respond? By blocking College Abacus’s access to their calculators. Imagine if Expedia or Kayak could not search for tickets on some of the most desirable airlines, and you get the idea.

…

So what’s really going on here? One strong hint comes from a letter that [College Abacus co-founder] Ms. [Abigail] Seldin received from a dean of financial aid. He wrote to her after she sent a mass note last year urging the schools that were blocking her tool to reconsider. She declined to identify him, as she still hopes to win him and others over.“We are experiencing record student demand, engage families early in financial aid discussions and are meeting our goals,” the dean told her. “Why you think I should open myself up to a purely financial comparison when we are so much more than that, I have no idea. It is probably because you have not sat where I sit. So, kindly cease communication with me.”

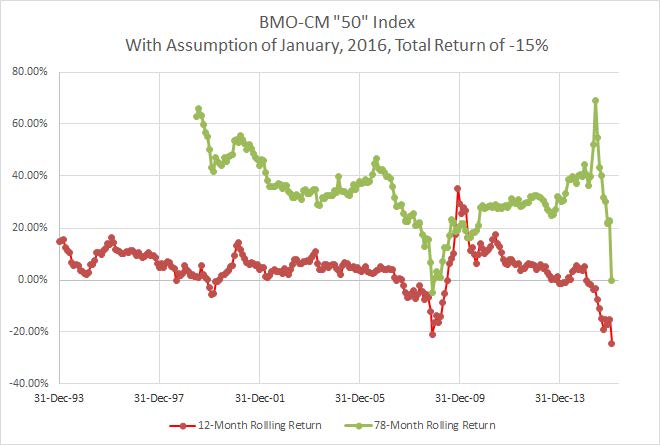

However, it seems to me that the preferred share market is signalling something …

Click for Big

It’s ridiculous. Right now the TXPR Total Return Index Value is down about 15.2% month-to-date. Assuming that this holds through to month-end and is reflected in the BMO CM-50 index, then we can conclude that this is the worst month on record: the worst is current November, 2008, at -10.7%, and October, 2008, at -8.2%. So the violence of this drop compared to the worst part of the Credit Crunch, when there were actual Bad Things happening, should give us pause.

We may also observe that such a return would imply that the Canadian preferred share market has experienced a cumulative total return of a big fat zero since July 31, 2009; a time-span of 78 months, which is 6.5 years.

And this assumption allows us to prepare the following graph:

Click for Big

So … assuming there’s no recovery in the second half of the month, we’re due to record the worst 12 months in Canadian preferred market history (well … back to 1993, anyway!) and has a six-and-a-half year cumulative total return that is only a little better than the worst on record. Nice.

Update

While pondering methods of making my Assiduous Readers feel even more terrible, it occurred to me that it’s actually worse than described above. In preparing the chart above, I simply picked the most recent time that the index moved through the estimated January value, but it also broke through this barrier in November, 2005. We may observe that the index’s total cumulative return from November 30, 2005, to [estimated] January month-end, 2016, is very slightly negative (-0.27%), so holding the index for the past 10 years and two months hasn’t made you any money. The previous low for the rolling cumulative 122-month return was reached (perhaps not surprisingly) in November, 2008, when it bottomed out at +7.78%. And this is worse.

Click for Big

It was an appalling day for the Canadian preferred share market, with PerpetualDiscounts down 211bp, FixedResets losing 277bp and DeemedRetractibles off 156bp. I will not discuss the Performance Highlights table. I will not! Volume was incredibly high.

It was yet another big day for DC.PR.C, with 122,599 shares changing hands at a VWAP of 16.92. It would seem that views are being taken! I suspect that current market conditions are making it less likely for the the abusive and debatable Plan of Arrangement to succeed … investors are attempting to cash out, not in!

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

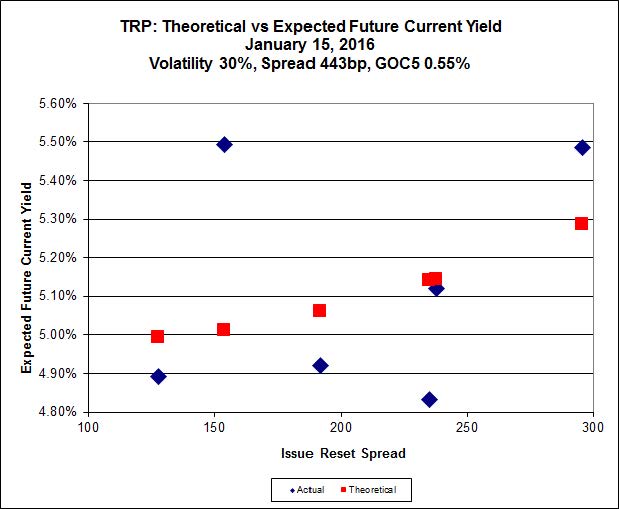

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 15.00 to be $0.90 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.92 cheap at its bid price of 9.51.

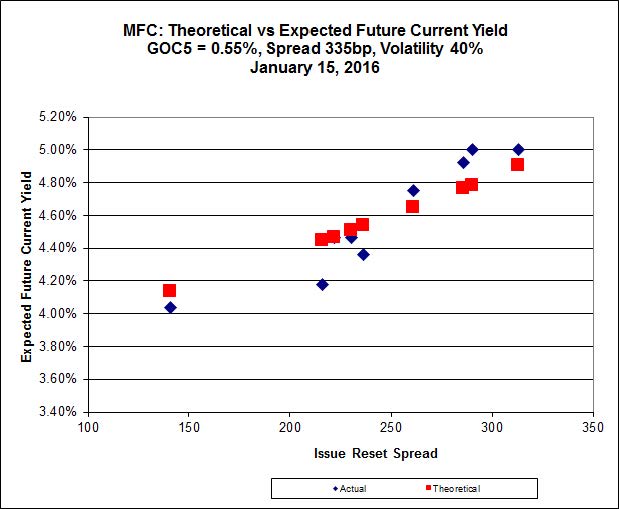

Click for Big

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 16.21 to be 0.98 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.25 to be 0.79 cheap.

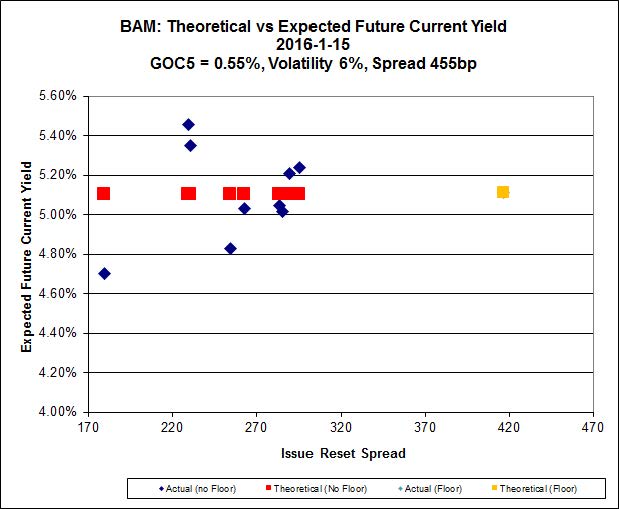

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.06 to be $0.91 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 16.05 and appears to be $0.85 rich.

Click for Big

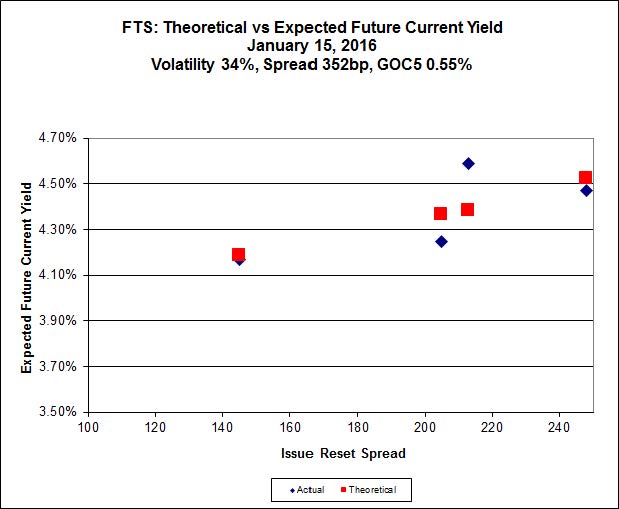

FTS.PR.K, with a spread of +205bp, and bid at 15.30, looks $0.41 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 14.60 and is $0.69 cheap.

Click for Big

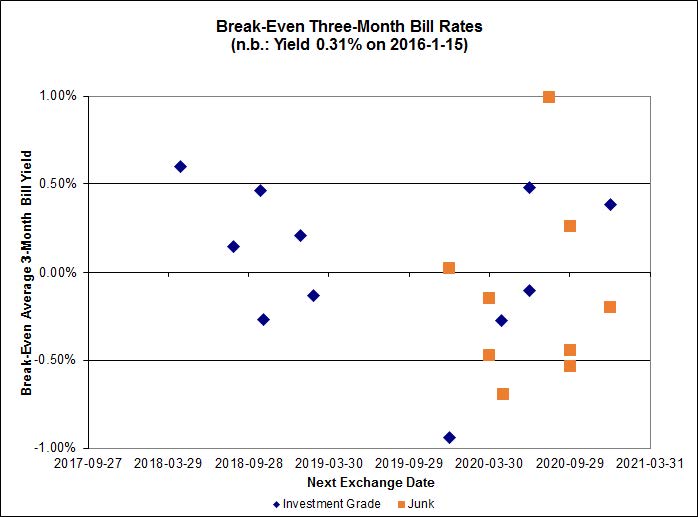

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.17%, with two outliers below -1.00%. There is one junk outlier below -1.00% and one above 1.00%. Note that today I have shifted the vertical axis of the chart.

Click for Big

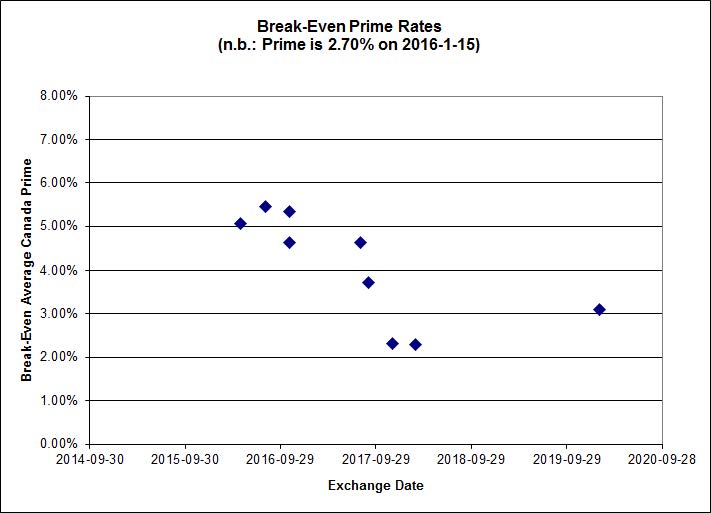

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.38 % | 6.55 % | 25,315 | 16.00 | 1 | -3.1514 % | 1,444.7 |

| FixedFloater | 7.72 % | 6.73 % | 29,483 | 15.57 | 1 | -2.0684 % | 2,576.2 |

| Floater | 4.71 % | 4.86 % | 77,910 | 15.77 | 4 | -1.9785 % | 1,622.6 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1949 % | 2,691.1 |

| SplitShare | 4.91 % | 6.50 % | 69,578 | 2.75 | 6 | -0.1949 % | 3,149.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1949 % | 2,457.1 |

| Perpetual-Premium | 6.05 % | 6.03 % | 85,337 | 13.86 | 6 | -1.4112 % | 2,440.8 |

| Perpetual-Discount | 6.03 % | 6.06 % | 99,102 | 13.81 | 34 | -2.1090 % | 2,394.3 |

| FixedReset | 5.96 % | 5.41 % | 240,878 | 14.12 | 82 | -2.7720 % | 1,728.4 |

| Deemed-Retractible | 5.48 % | 6.12 % | 131,708 | 6.94 | 34 | -1.5601 % | 2,456.7 |

| FloatingReset | 3.02 % | 5.38 % | 65,189 | 5.58 | 13 | -2.2401 % | 1,953.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| RY.PR.A | Deemed-Retractible | -10.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.05 Bid-YTW : 7.05 % |

| FTS.PR.I | FloatingReset | -10.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 10.17 Evaluated at bid price : 10.17 Bid-YTW : 4.67 % |

| SLF.PR.H | FixedReset | -6.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.66 Bid-YTW : 11.03 % |

| TRP.PR.F | FloatingReset | -6.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 10.75 Evaluated at bid price : 10.75 Bid-YTW : 5.51 % |

| MFC.PR.K | FixedReset | -6.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.50 Bid-YTW : 9.70 % |

| HSE.PR.G | FixedReset | -6.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 7.30 % |

| HSE.PR.A | FixedReset | -6.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.15 Evaluated at bid price : 9.15 Bid-YTW : 6.58 % |

| MFC.PR.N | FixedReset | -6.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.96 Bid-YTW : 9.56 % |

| BAM.PF.A | FixedReset | -5.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 5.64 % |

| MFC.PR.F | FixedReset | -5.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.14 Bid-YTW : 11.54 % |

| PWF.PR.L | Perpetual-Discount | -5.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.13 Evaluated at bid price : 20.13 Bid-YTW : 6.36 % |

| W.PR.H | Perpetual-Discount | -5.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 6.69 % |

| BAM.PF.G | FixedReset | -5.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 5.64 % |

| TRP.PR.D | FixedReset | -5.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 14.31 Evaluated at bid price : 14.31 Bid-YTW : 5.64 % |

| TRP.PR.E | FixedReset | -5.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 5.47 % |

| MFC.PR.I | FixedReset | -5.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.32 Bid-YTW : 8.80 % |

| MFC.PR.J | FixedReset | -4.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.63 Bid-YTW : 9.07 % |

| SLF.PR.I | FixedReset | -4.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.80 Bid-YTW : 9.78 % |

| RY.PR.E | Deemed-Retractible | -4.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.44 Bid-YTW : 5.90 % |

| MFC.PR.H | FixedReset | -4.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.40 Bid-YTW : 8.18 % |

| BAM.PR.T | FixedReset | -4.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 13.36 Evaluated at bid price : 13.36 Bid-YTW : 5.79 % |

| BAM.PF.F | FixedReset | -4.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.53 % |

| BNS.PR.Q | FixedReset | -4.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 5.70 % |

| RY.PR.J | FixedReset | -4.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.11 Evaluated at bid price : 17.11 Bid-YTW : 5.11 % |

| RY.PR.M | FixedReset | -4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.73 Evaluated at bid price : 16.73 Bid-YTW : 5.10 % |

| BAM.PF.C | Perpetual-Discount | -4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.48 Evaluated at bid price : 18.48 Bid-YTW : 6.64 % |

| NA.PR.W | FixedReset | -4.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.02 Evaluated at bid price : 15.02 Bid-YTW : 5.21 % |

| TD.PF.A | FixedReset | -4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.86 % |

| BAM.PF.B | FixedReset | -4.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 5.52 % |

| MFC.PR.G | FixedReset | -4.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 8.77 % |

| TRP.PR.B | FixedReset | -4.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.35 Evaluated at bid price : 9.35 Bid-YTW : 5.36 % |

| IFC.PR.C | FixedReset | -4.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.25 Bid-YTW : 10.14 % |

| BMO.PR.Y | FixedReset | -4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.76 Evaluated at bid price : 17.76 Bid-YTW : 4.96 % |

| PWF.PR.P | FixedReset | -4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 11.37 Evaluated at bid price : 11.37 Bid-YTW : 4.98 % |

| IFC.PR.A | FixedReset | -4.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.20 Bid-YTW : 11.47 % |

| TRP.PR.G | FixedReset | -3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 5.82 % |

| POW.PR.B | Perpetual-Discount | -3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 6.28 % |

| BAM.PF.D | Perpetual-Discount | -3.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 6.60 % |

| HSE.PR.E | FixedReset | -3.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 7.20 % |

| NA.PR.Q | FixedReset | -3.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.31 Bid-YTW : 6.25 % |

| BAM.PR.M | Perpetual-Discount | -3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 6.53 % |

| FTS.PR.G | FixedReset | -3.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 14.60 Evaluated at bid price : 14.60 Bid-YTW : 5.12 % |

| BIP.PR.A | FixedReset | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 6.38 % |

| TD.PF.D | FixedReset | -3.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.15 Evaluated at bid price : 17.15 Bid-YTW : 5.09 % |

| TD.PR.T | FloatingReset | -3.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.63 Bid-YTW : 5.38 % |

| SLF.PR.E | Deemed-Retractible | -3.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 8.81 % |

| TRP.PR.A | FixedReset | -3.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 12.55 Evaluated at bid price : 12.55 Bid-YTW : 5.49 % |

| BNS.PR.R | FixedReset | -3.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 5.41 % |

| BAM.PR.N | Perpetual-Discount | -3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.41 Evaluated at bid price : 18.41 Bid-YTW : 6.52 % |

| MFC.PR.M | FixedReset | -3.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.69 Bid-YTW : 9.00 % |

| BMO.PR.M | FixedReset | -3.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 5.03 % |

| W.PR.J | Perpetual-Discount | -3.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.25 Evaluated at bid price : 21.52 Bid-YTW : 6.54 % |

| FTS.PR.K | FixedReset | -3.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 4.85 % |

| TRP.PR.C | FixedReset | -3.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.51 Evaluated at bid price : 9.51 Bid-YTW : 5.80 % |

| BAM.PR.E | Ratchet | -3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 25.00 Evaluated at bid price : 12.60 Bid-YTW : 6.55 % |

| MFC.PR.L | FixedReset | -2.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.21 Bid-YTW : 9.20 % |

| ENB.PR.A | Perpetual-Discount | -2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.16 Evaluated at bid price : 21.16 Bid-YTW : 6.61 % |

| SLF.PR.A | Deemed-Retractible | -2.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.56 Bid-YTW : 8.30 % |

| BAM.PF.E | FixedReset | -2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.05 Evaluated at bid price : 16.05 Bid-YTW : 5.49 % |

| GWO.PR.H | Deemed-Retractible | -2.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.09 Bid-YTW : 8.02 % |

| RY.PR.P | Perpetual-Discount | -2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.49 Evaluated at bid price : 23.80 Bid-YTW : 5.65 % |

| BAM.PR.B | Floater | -2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.59 Evaluated at bid price : 9.59 Bid-YTW : 4.97 % |

| HSE.PR.C | FixedReset | -2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 14.27 Evaluated at bid price : 14.27 Bid-YTW : 7.04 % |

| POW.PR.C | Perpetual-Premium | -2.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.40 Evaluated at bid price : 23.69 Bid-YTW : 6.15 % |

| BAM.PR.Z | FixedReset | -2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 5.65 % |

| RY.PR.W | Perpetual-Discount | -2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.81 Evaluated at bid price : 22.05 Bid-YTW : 5.63 % |

| POW.PR.A | Perpetual-Discount | -2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 22.71 Evaluated at bid price : 23.00 Bid-YTW : 6.12 % |

| TD.PR.Y | FixedReset | -2.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.15 Bid-YTW : 5.14 % |

| VNR.PR.A | FixedReset | -2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 5.50 % |

| ELF.PR.F | Perpetual-Discount | -2.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.28 Evaluated at bid price : 21.55 Bid-YTW : 6.18 % |

| SLF.PR.G | FixedReset | -2.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.80 Bid-YTW : 10.83 % |

| BAM.PR.C | Floater | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.54 Evaluated at bid price : 9.54 Bid-YTW : 4.99 % |

| BNS.PR.B | FloatingReset | -2.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 5.47 % |

| PWF.PR.T | FixedReset | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.34 % |

| SLF.PR.J | FloatingReset | -2.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.90 Bid-YTW : 11.25 % |

| BAM.PR.R | FixedReset | -2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 13.06 Evaluated at bid price : 13.06 Bid-YTW : 5.79 % |

| BNS.PR.P | FixedReset | -2.60 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.48 Bid-YTW : 4.90 % |

| RY.PR.C | Deemed-Retractible | -2.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.15 Bid-YTW : 5.43 % |

| IAG.PR.G | FixedReset | -2.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 8.75 % |

| ELF.PR.H | Perpetual-Discount | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.97 Evaluated at bid price : 22.33 Bid-YTW : 6.18 % |

| RY.PR.L | FixedReset | -2.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.60 Bid-YTW : 5.05 % |

| GWO.PR.N | FixedReset | -2.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.00 Bid-YTW : 11.56 % |

| TD.PF.E | FixedReset | -2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 4.93 % |

| RY.PR.F | Deemed-Retractible | -2.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.05 Bid-YTW : 5.35 % |

| PWF.PR.E | Perpetual-Discount | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 22.54 Evaluated at bid price : 22.79 Bid-YTW : 6.05 % |

| RY.PR.D | Deemed-Retractible | -2.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.14 Bid-YTW : 5.33 % |

| CU.PR.F | Perpetual-Discount | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 6.10 % |

| SLF.PR.C | Deemed-Retractible | -2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.76 Bid-YTW : 8.54 % |

| BAM.PR.G | FixedFloater | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 25.00 Evaluated at bid price : 12.31 Bid-YTW : 6.73 % |

| BAM.PF.H | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 22.97 Evaluated at bid price : 24.45 Bid-YTW : 5.07 % |

| RY.PR.G | Deemed-Retractible | -1.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.15 Bid-YTW : 5.32 % |

| CU.PR.D | Perpetual-Discount | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.18 Evaluated at bid price : 20.18 Bid-YTW : 6.17 % |

| BNS.PR.M | Deemed-Retractible | -1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.80 Bid-YTW : 5.43 % |

| TD.PR.Z | FloatingReset | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.80 Bid-YTW : 5.32 % |

| NA.PR.S | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 15.78 Evaluated at bid price : 15.78 Bid-YTW : 5.14 % |

| TD.PF.B | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 4.77 % |

| PWF.PR.F | Perpetual-Discount | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 6.06 % |

| RY.PR.H | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.42 Evaluated at bid price : 16.42 Bid-YTW : 4.81 % |

| GWO.PR.S | Deemed-Retractible | -1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.66 Bid-YTW : 6.72 % |

| SLF.PR.D | Deemed-Retractible | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.71 Bid-YTW : 8.58 % |

| PWF.PR.A | Floater | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 11.20 Evaluated at bid price : 11.20 Bid-YTW : 4.27 % |

| ELF.PR.G | Perpetual-Discount | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.16 Evaluated at bid price : 20.16 Bid-YTW : 5.93 % |

| BNS.PR.D | FloatingReset | -1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.80 Bid-YTW : 7.37 % |

| BMO.PR.Q | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 7.83 % |

| RY.PR.K | FloatingReset | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.99 Bid-YTW : 5.54 % |

| BMO.PR.Z | Perpetual-Discount | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 22.15 Evaluated at bid price : 22.50 Bid-YTW : 5.63 % |

| RY.PR.B | Deemed-Retractible | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.40 Bid-YTW : 5.33 % |

| BNS.PR.Y | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.86 Bid-YTW : 6.80 % |

| BMO.PR.R | FloatingReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.31 Bid-YTW : 4.95 % |

| CM.PR.Q | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 17.52 Evaluated at bid price : 17.52 Bid-YTW : 4.99 % |

| IGM.PR.B | Perpetual-Premium | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 24.00 Evaluated at bid price : 24.46 Bid-YTW : 6.03 % |

| BNS.PR.L | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 5.35 % |

| TD.PF.F | Perpetual-Discount | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.68 Evaluated at bid price : 21.96 Bid-YTW : 5.58 % |

| CU.PR.E | Perpetual-Discount | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.31 Evaluated at bid price : 20.31 Bid-YTW : 6.13 % |

| PWF.PR.I | Perpetual-Premium | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 24.44 Evaluated at bid price : 24.68 Bid-YTW : 6.09 % |

| POW.PR.D | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 6.07 % |

| SLF.PR.B | Deemed-Retractible | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 8.03 % |

| FTS.PR.H | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 4.63 % |

| GWO.PR.Q | Deemed-Retractible | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 7.21 % |

| RY.PR.N | Perpetual-Discount | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 21.75 Evaluated at bid price : 22.05 Bid-YTW : 5.63 % |

| BAM.PR.X | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 5.29 % |

| PWF.PR.H | Perpetual-Premium | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.52 Evaluated at bid price : 23.79 Bid-YTW : 6.06 % |

| FTS.PR.J | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 20.31 Evaluated at bid price : 20.31 Bid-YTW : 5.94 % |

| BMO.PR.K | Deemed-Retractible | -1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.01 Bid-YTW : 5.42 % |

| CU.PR.G | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 18.72 Evaluated at bid price : 18.72 Bid-YTW : 6.11 % |

| RY.PR.Q | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.19 Evaluated at bid price : 25.15 Bid-YTW : 5.19 % |

| MFC.PR.B | Deemed-Retractible | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.56 Bid-YTW : 8.21 % |

| PWF.PR.G | Perpetual-Premium | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 24.25 Evaluated at bid price : 24.55 Bid-YTW : 6.02 % |

| CM.PR.P | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.84 % |

| CU.PR.C | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.95 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.G | FixedReset | 499,908 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.24 Evaluated at bid price : 25.29 Bid-YTW : 5.22 % |

| BAM.PR.K | Floater | 352,668 | TD crossed 300,000 at 10.00, then bought 11,100 from Goldman Sachs at 9.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 9.80 Evaluated at bid price : 9.80 Bid-YTW : 4.86 % |

| RY.PR.Q | FixedReset | 327,782 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 23.19 Evaluated at bid price : 25.15 Bid-YTW : 5.19 % |

| BNS.PR.R | FixedReset | 188,436 | RBC crossed blocks of 131,300 and 16,000, both at 22.97. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 5.41 % |

| RY.PR.I | FixedReset | 104,453 | Scotia crossed 96,300 at 22.10. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.18 Bid-YTW : 5.42 % |

| BMO.PR.S | FixedReset | 96,836 | Scotia crossed 81,900 at 16.61. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-15 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 4.81 % |

| There were 89 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.A | Deemed-Retractible | Quote: 22.05 – 24.60 Spot Rate : 2.5500 Average : 1.3879 YTW SCENARIO |

| PWF.PR.L | Perpetual-Discount | Quote: 20.13 – 21.57 Spot Rate : 1.4400 Average : 0.8962 YTW SCENARIO |

| W.PR.H | Perpetual-Discount | Quote: 20.73 – 22.00 Spot Rate : 1.2700 Average : 0.7651 YTW SCENARIO |

| RY.PR.E | Deemed-Retractible | Quote: 23.44 – 24.55 Spot Rate : 1.1100 Average : 0.6248 YTW SCENARIO |

| POW.PR.C | Perpetual-Premium | Quote: 23.69 – 24.81 Spot Rate : 1.1200 Average : 0.6487 YTW SCENARIO |

| BMO.PR.Q | FixedReset | Quote: 18.25 – 19.25 Spot Rate : 1.0000 Average : 0.5829 YTW SCENARIO |