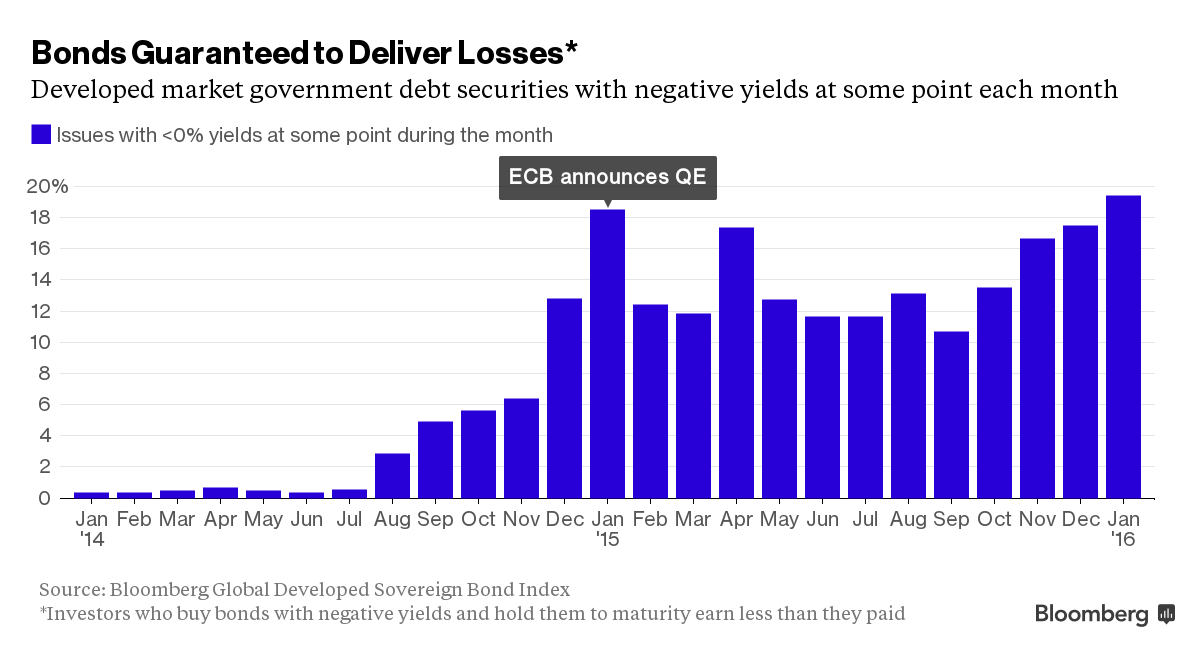

Bloomberg published a graph showing how common negative yields have become:

Click for Big

There was a good chunk of pension de-risking done by Sun Life:

Two Canadian pension plans are teaming up to buy about $530-million of annuities, in a creative deal to transfer investment, longevity and inflation risk to an insurance company.

The two defined-benefit pension plans, owned by companies that did not want to be named, have struck the joint annuity agreement with Sun Life Financial Inc. despite having no other relation to each other. The advantage of banding together and doing the transaction at the same time was more than $20-million dollars in savings combined as Sun Life balanced the inflation exposure of the two plans.

Sun Life began working with both companies separately in early 2015, and the insurer noticed that they had different inflation formulas. “One plan sponsor promised to increase benefits when inflation was low. The other promised to increase benefits when inflation was high,” said Brent Simmons, senior managing director for defined-benefits at Sun Life, adding that both promises are tricky to buy proper asset management strategies for.

…

Annuities for pension plans are part of a strategy known as “pension de-risking” in industry parlance, and they are a way of reducing long-term risks and ratcheting down income volatility for defined-benefit pension plans. These sorts of transactions became commonplace in the United States several years ago, and the U.K. has also been a leader with £19-billion ($38-billion) in de-risking deals last year. Canada’s market is still developing.Two significant de-risking annuity deals in Canada include a $150-million deal by the Canadian Wheat Board in 2013, and a $500-million deal with an unnamed Canadian company done by Industrial Alliance Insurance and Financial Services Inc. last year.

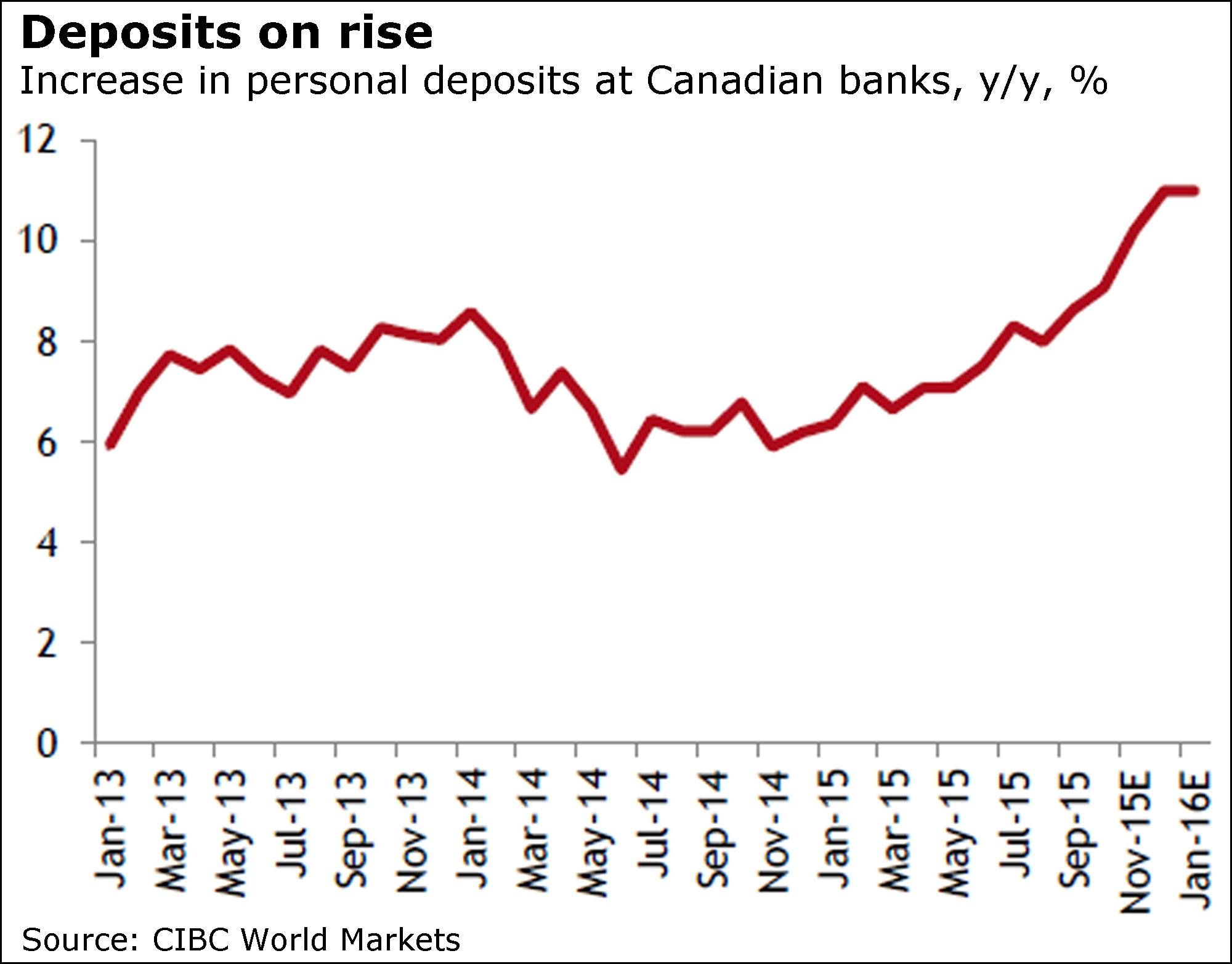

Meanwhile, Canadian retail is moving to cash:

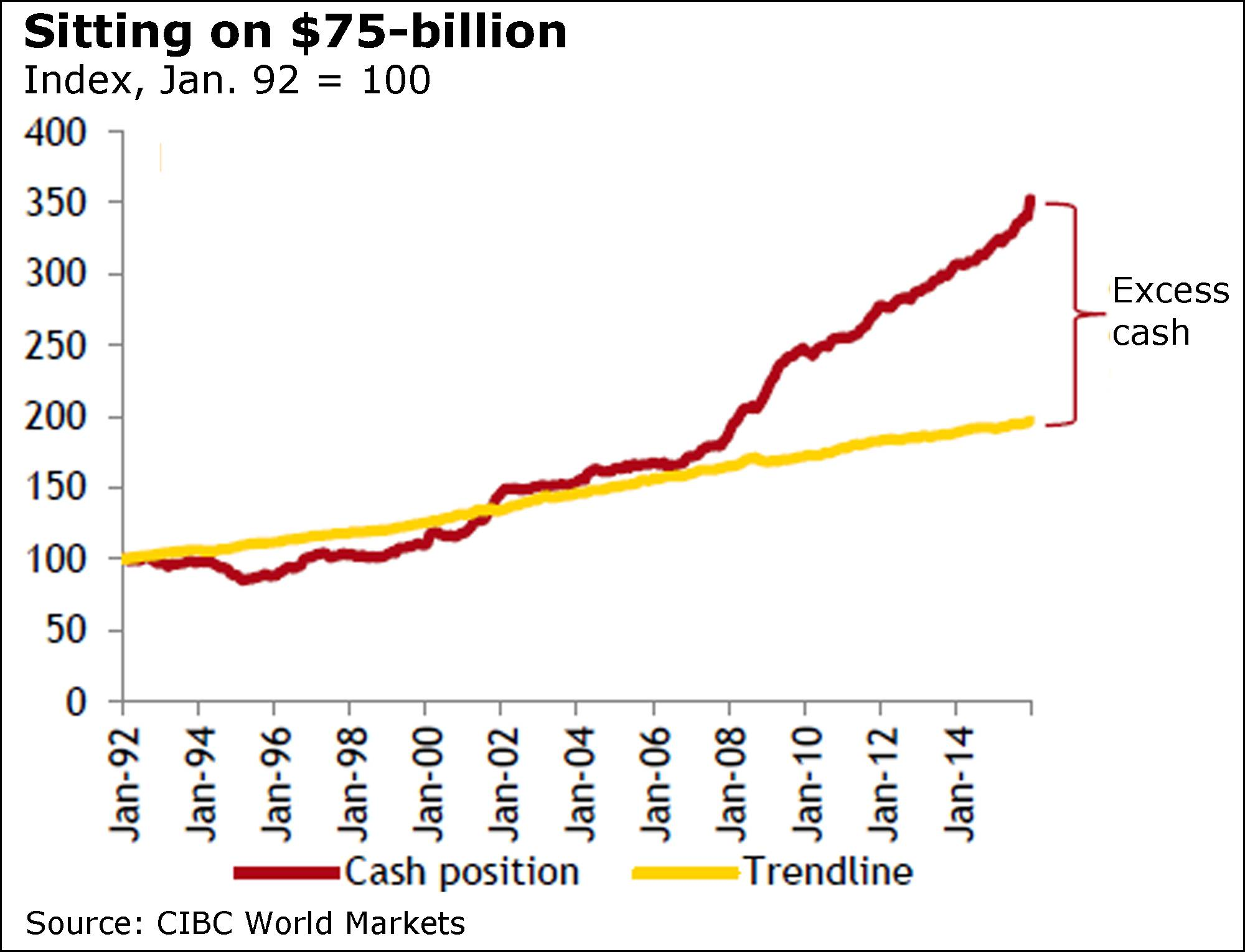

Canadians are holding a record $75-billion in cash amid an “ocean of fear” about investing in the markets, a new study finds.

That means they could miss out on billions in payback, warns the study released today by Canadian Imperial Bank of Commerce economists Benjamin Tal and Royce Mendes.

…

And here’s a stunning figure from the report: The extra money accounts for about 10 per cent of all personal liquid assets in the country.This angst isn’t new. It obviously came about during the 1987 crash, and again in 2001 and then again during the financial crisis.

Click for Big

Click for Big

Sadly, it appears there will be no more entertainment from Silver Bullion Trust:

Silver Bullion Trust (“SBT” or the “Trust”) (symbol: TSX – SBT.UN (C$) and SBT.U (US$)) today announced that SBT Unitholders voted to approve amendments to SBT’s Amended and Restated Declaration of Trust dated July 9, 2009 (the “DOT”), in order to permit its conversion from a closed-end fund to a silver-bullion exchange traded fund (the “ETF Conversion”) at a special meeting of Unitholders held earlier today in Toronto.

As soon as possible, Purpose Investments Inc. will become the new manager and trustee of the Trust once the amendments to the DOT are signed and the bullion holdings will be administered by Silver Administrators Limited, SBT’s current administrator.

It was a modestly negative day for the Canadian preferred share market, with PerpetualDiscounts down 25bp, FixedResets gaining 8bp and DeemedRetractibles off 15bp. The Performance Highlights table shows a fair bit of movement below the placid surface. Volume was on the low side of average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

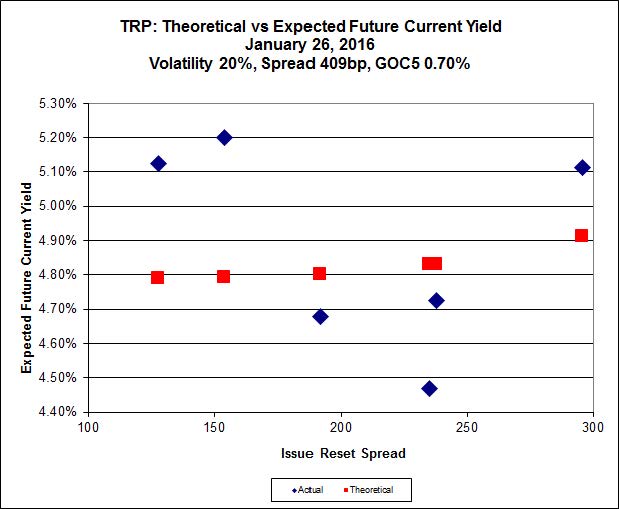

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.06 to be $1.27 rich, while TRP.PR.C, resetting 2021-1-30 at +154, is $0.92 cheap at its bid price of 10.77.

Click for Big

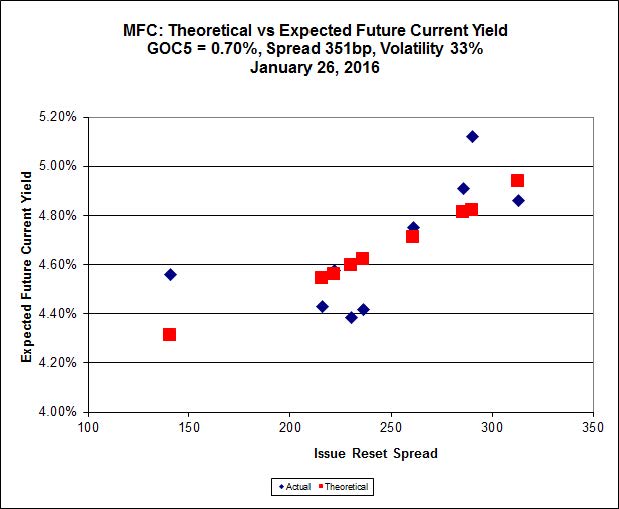

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 17.10 to be 0.78 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.57 to be 1.11 cheap.

Click for Big

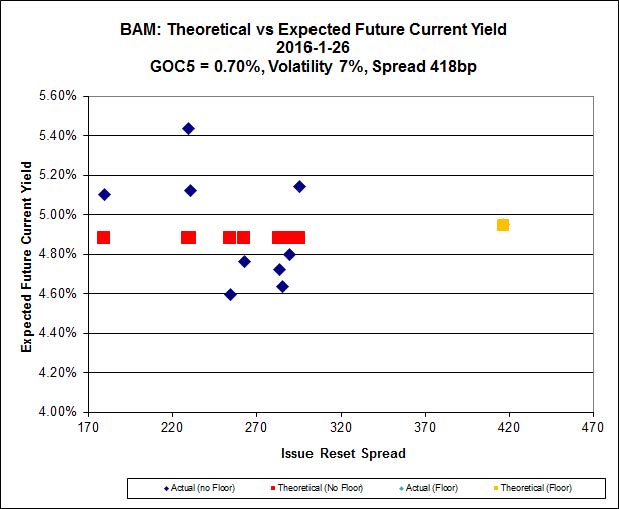

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.80 to be $1.57 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.69 and appears to be $1.04 rich.

Click for Big

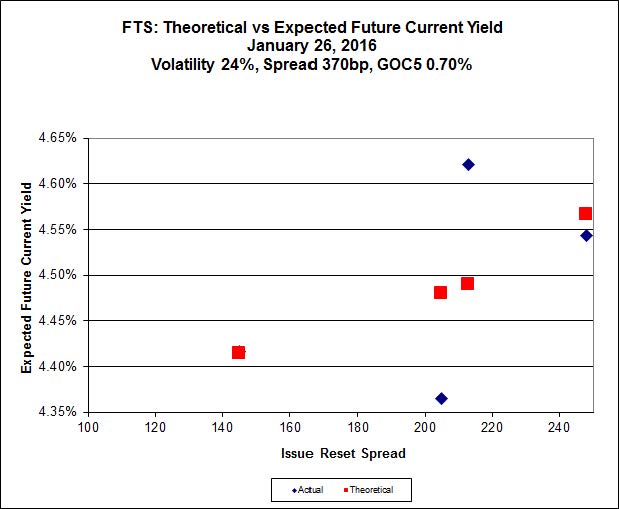

FTS.PR.K, with a spread of +205bp, and bid at 15.75, looks $0.40 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.31 and is $0.45 cheap.

Click for Big

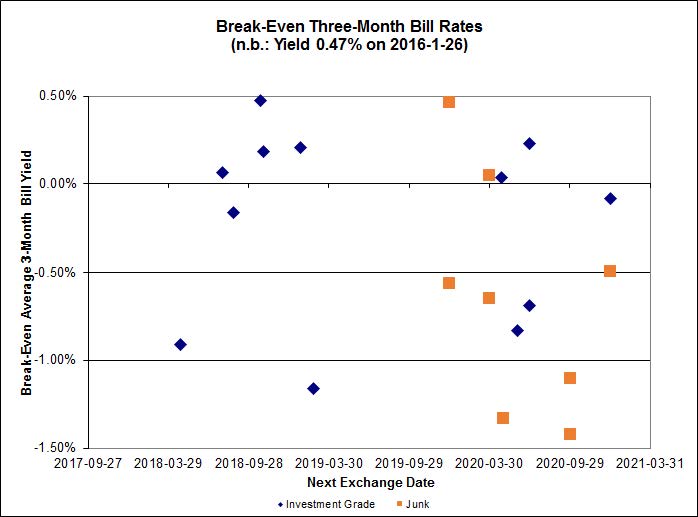

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.35%, with one outlier below -1.50%. Note the range of the y-axis has changed. There is one junk outlier below -1.50% and two above +0.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.28 % | 6.43 % | 20,369 | 16.11 | 1 | -1.1538 % | 1,473.4 |

| FixedFloater | 7.63 % | 6.66 % | 28,978 | 15.63 | 1 | 0.7282 % | 2,605.5 |

| Floater | 4.85 % | 5.05 % | 74,218 | 15.41 | 4 | -0.3831 % | 1,582.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2094 % | 2,683.2 |

| SplitShare | 4.92 % | 7.12 % | 78,662 | 2.71 | 6 | -0.2094 % | 3,139.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2094 % | 2,449.8 |

| Perpetual-Premium | 5.95 % | 5.91 % | 88,581 | 13.97 | 6 | -0.1488 % | 2,480.0 |

| Perpetual-Discount | 5.89 % | 5.91 % | 101,704 | 13.99 | 33 | -0.2510 % | 2,446.5 |

| FixedReset | 5.70 % | 5.04 % | 239,250 | 14.57 | 83 | 0.0787 % | 1,809.5 |

| Deemed-Retractible | 5.31 % | 5.86 % | 127,971 | 6.95 | 34 | -0.1462 % | 2,539.7 |

| FloatingReset | 2.98 % | 4.72 % | 61,161 | 5.57 | 13 | 0.2497 % | 2,010.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset | -4.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 10.77 Evaluated at bid price : 10.77 Bid-YTW : 5.27 % |

| BAM.PR.Z | FixedReset | -3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 5.39 % |

| NA.PR.W | FixedReset | -3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 16.01 Evaluated at bid price : 16.01 Bid-YTW : 4.96 % |

| BAM.PR.X | FixedReset | -2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 5.54 % |

| TRP.PR.B | FixedReset | -2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 9.66 Evaluated at bid price : 9.66 Bid-YTW : 5.32 % |

| VNR.PR.A | FixedReset | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 5.68 % |

| PWF.PR.T | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 19.53 Evaluated at bid price : 19.53 Bid-YTW : 4.18 % |

| POW.PR.D | Perpetual-Discount | -2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 6.02 % |

| BAM.PF.B | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.48 Evaluated at bid price : 17.48 Bid-YTW : 5.05 % |

| PWF.PR.P | FixedReset | -2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 11.10 Evaluated at bid price : 11.10 Bid-YTW : 5.25 % |

| GWO.PR.O | FloatingReset | -2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.25 Bid-YTW : 11.91 % |

| IFC.PR.C | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.65 Bid-YTW : 9.89 % |

| PVS.PR.E | SplitShare | -1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 7.12 % |

| BNS.PR.Z | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.30 Bid-YTW : 7.78 % |

| PWF.PR.A | Floater | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 10.95 Evaluated at bid price : 10.95 Bid-YTW : 4.31 % |

| POW.PR.A | Perpetual-Discount | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 23.38 Evaluated at bid price : 23.67 Bid-YTW : 5.96 % |

| GWO.PR.L | Deemed-Retractible | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.51 Bid-YTW : 6.03 % |

| TD.PR.S | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.80 Bid-YTW : 4.47 % |

| BAM.PF.E | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.69 Evaluated at bid price : 17.69 Bid-YTW : 5.04 % |

| BMO.PR.M | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.77 Bid-YTW : 4.66 % |

| SLF.PR.J | FloatingReset | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.50 Bid-YTW : 11.80 % |

| CU.PR.C | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 4.86 % |

| POW.PR.G | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 23.36 Evaluated at bid price : 23.82 Bid-YTW : 5.91 % |

| POW.PR.B | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 22.41 Evaluated at bid price : 22.67 Bid-YTW : 5.94 % |

| TRP.PR.F | FloatingReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 11.37 Evaluated at bid price : 11.37 Bid-YTW : 5.29 % |

| BAM.PR.E | Ratchet | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 25.00 Evaluated at bid price : 12.85 Bid-YTW : 6.43 % |

| IFC.PR.A | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.40 Bid-YTW : 11.37 % |

| MFC.PR.H | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.70 Bid-YTW : 7.31 % |

| TD.PF.E | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.57 % |

| RY.PR.H | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.41 Evaluated at bid price : 17.41 Bid-YTW : 4.52 % |

| BNS.PR.R | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.81 Bid-YTW : 4.96 % |

| PVS.PR.D | SplitShare | 1.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 7.28 % |

| BAM.PR.R | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 13.80 Evaluated at bid price : 13.80 Bid-YTW : 5.60 % |

| BNS.PR.A | FloatingReset | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 4.41 % |

| CCS.PR.C | Deemed-Retractible | 1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.55 Bid-YTW : 7.20 % |

| BMO.PR.Y | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 19.27 Evaluated at bid price : 19.27 Bid-YTW : 4.63 % |

| RY.PR.M | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 4.66 % |

| RY.PR.I | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.42 Bid-YTW : 4.27 % |

| FTS.PR.M | FixedReset | 1.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.92 % |

| NA.PR.Q | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 5.47 % |

| IAG.PR.G | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.90 Bid-YTW : 7.55 % |

| RY.PR.J | FixedReset | 1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 18.52 Evaluated at bid price : 18.52 Bid-YTW : 4.71 % |

| RY.PR.Z | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.44 % |

| SLF.PR.G | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.94 Bid-YTW : 10.76 % |

| TD.PF.D | FixedReset | 2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 19.01 Evaluated at bid price : 19.01 Bid-YTW : 4.66 % |

| HSE.PR.G | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 7.29 % |

| SLF.PR.H | FixedReset | 2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.10 Bid-YTW : 10.71 % |

| SLF.PR.I | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.66 Bid-YTW : 9.13 % |

| TD.PF.A | FixedReset | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.11 Evaluated at bid price : 17.11 Bid-YTW : 4.61 % |

| BNS.PR.B | FloatingReset | 3.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.68 Bid-YTW : 4.64 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.X | FixedReset | 146,614 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 23.06 Evaluated at bid price : 24.77 Bid-YTW : 5.61 % |

| TD.PF.G | FixedReset | 88,726 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.36 Bid-YTW : 5.26 % |

| RY.PR.Q | FixedReset | 76,204 | Desjardins crossed 10,700 at 25.47. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 23.29 Evaluated at bid price : 25.46 Bid-YTW : 5.17 % |

| BMO.PR.S | FixedReset | 70,795 | Nesbitt crossed 12,500 at 17.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 17.46 Evaluated at bid price : 17.46 Bid-YTW : 4.69 % |

| GWO.PR.F | Deemed-Retractible | 68,245 | Desjardins crossed 45,400 at 25.15; Nesbitt crossed 21,300 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.15 Bid-YTW : 3.71 % |

| BAM.PR.X | FixedReset | 67,200 | TD crossed 50,000 at 12.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-26 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 5.54 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.O | FloatingReset | Quote: 11.25 – 20.25 Spot Rate : 9.0000 Average : 5.9189 YTW SCENARIO |

| BNS.PR.C | FloatingReset | Quote: 21.65 – 22.73 Spot Rate : 1.0800 Average : 0.6508 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 18.90 – 19.77 Spot Rate : 0.8700 Average : 0.6118 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 17.90 – 18.65 Spot Rate : 0.7500 Average : 0.4990 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 17.80 – 18.64 Spot Rate : 0.8400 Average : 0.6271 YTW SCENARIO |

| W.PR.H | Perpetual-Discount | Quote: 22.00 – 22.47 Spot Rate : 0.4700 Average : 0.3051 YTW SCENARIO |