Today’s big news was the Bank of Japan moving the deposit rate to negative:

Bank of Japan Governor Haruhiko Kuroda is matching European Central Bank President Mario Draghi in pursuing negative interest rates, and even pulling ahead when it comes to driving longer-term bond yields lower.

The yen plunged more than 1 percent against the euro after Kuroda unexpectedly cut the rate on excess reserves held by financial institutions at the BOJ to minus 0.1 percent. Two-year Japanese government bond yields sank to minus 0.085 percent, closing the gap on German negative yields, while 10-year JGB yields of 0.09 percent are lower than similar-dated bunds. Kuroda said the central bank will cut the rate further if needed and that he expects to drive yields lower across the bond curve.

…

Kuroda said Friday that negative rates don’t replace quantitative easing, they simply add to the BOJ’s options. The central bank pushed back its time frame for reaching stable 2 percent inflation to around the six months starting in April 2017, the third postponement in less than a year. The bank now sees inflation rising 0.8 percent in the 12 months starting this April, down from a previous forecast of 1.4 percent.European and Japanese policy makers have faced extra pressure to boost stimulus after the yen and euro outperformed major peers for most of this month amid demand for havens as tumbling crude oil prices and concerns China’s economy is slowing spurred a more than $6 trillion rout in global stock markets.

This had an immediate effect on US equities:

U.S. stocks joined an advance in global equities, while bonds rallied as the Bank of Japan’s unexpected monetary stimulus boosted confidence that central banks remain vigilant of slowing economic growth. The yen tumbled, while oil gained.

The Standard & Poor’s 500 Index extended gains throughout the day to post the biggest advance since Sept. 8, while the Dow Jones Industrial Average rose almost 400 points as Microsoft Corp. rallied on earnings. Yields on 10-year Treasury notes retreated, while Japanese yields fell to records after the BOJ adopted a negative interest rate. The yen weakened versus the U.S. dollar by the most in more than a year. Oil climbed for a fourth day.

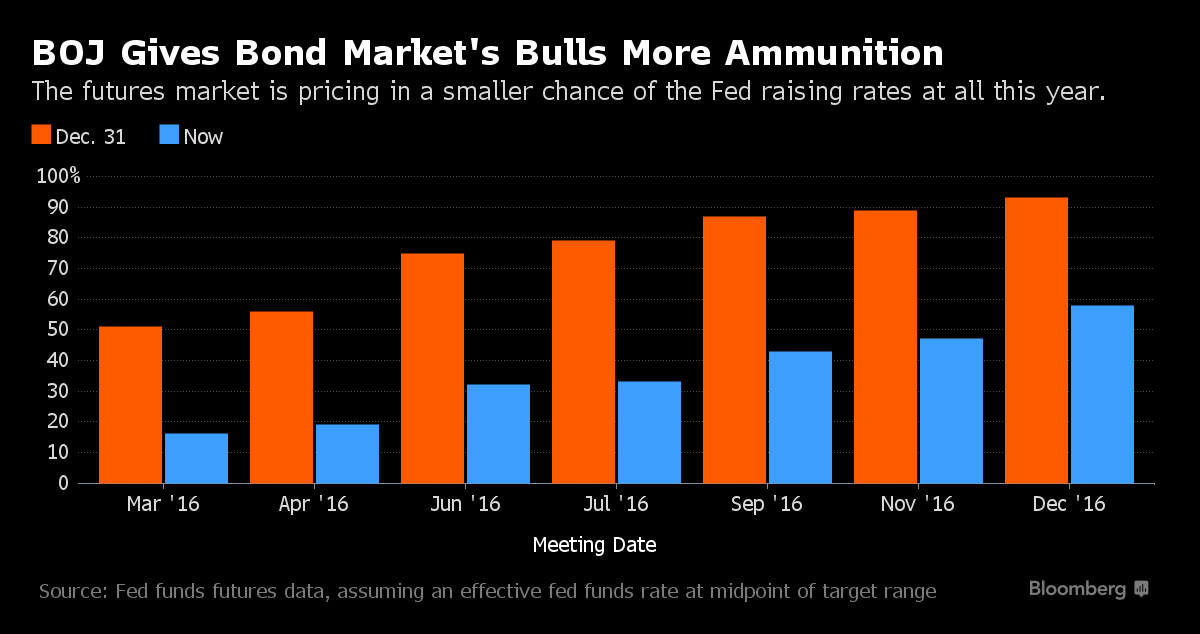

… and further doubt was cast on the prospects for Fed hikes:

In the bond market’s view, the chance of a Federal Reserve interest-rate increase this year is practically a toss-up after the Bank of Japan’s surprise policy move.

Yields on sovereign debt fell worldwide after BOJ Governor Haruhiko Kuroda introduced negative interest rates for some bank reserves to support the world’s third-biggest economy. Derivatives traders see less than a 60 percent shot that the Fed will raise its benchmark even once this year, let alone the four quarter-point increases that policy makers projected in December.

The move from Japan is another sign of slowing global economic growth, which triggered volatility across global markets to start the year. The European Central Bank has also signaled it may add stimulus. The divergence between U.S. monetary policy and the stances in Japan and the euro region risk strengthening the greenback by driving global investors to higher-yielding American assets. That could further damp inflation in the U.S., which hasn’t reached the Fed’s 2 percent target since 2012.

Click for Big

And the rise in oil helped out Canada’s market as well:

Canadian stocks climbed a fourth day, trimming a monthly drop that sent shares into a bear market earlier this year, as crude prices rose and data showed the resource-rich nation’s economy expanded for the first time in three months.

The Standard & Poor’s/TSX Composite Index rose 1.8 percent to 12,822.13 at 4 p.m. in Toronto. The index has rallied 8.3 percent since hitting a 2 1/2-year low on Jan. 20. While the benchmark equity gauge posted its first negative January since 2010, the late rally among energy producers has boosted the S&P/TSX’s performance to the best among developed markets this year.

Which is a good thing, because real estate is the only Canadian bright spot:

Softness in the economy has been concentrated in goods-producing sectors, which shrunk by 2.6 percent year-to-date through November. Given the carnage in commodities, the slump in construction tied to non-residential investment and mining and oil and gas extraction comes as no surprise.

Meanwhile, the services sector continues to chug along with real output up 1 percent. This suggests that the commodity collapse has yet to infect the broader economy. The bad news? The majority of that growth–53 percent–can be attributed to a single sub-sector, and one that many economists fear was cyclically overextended even before this stretch of out-performance.

Click for Big

I seem to remember a similar figure being cited for the proportion of US growth attributable to housing in the 2000-2007 period, but can’t find a citation.

But we’ll close for today with a lecture on history modification:

Oxford University’s Oriel College has decided not to tear down its statue of the British colonialist Cecil Rhodes, because of the “overwhelming message” it received that the statue should stay. The true motive appears to have been money.

The college reportedly cut short its promised six-month “listening exercise,” after it became clear that even to continue a debate on the subject could cost as much as £100 million in donations from alumni. That would catch the attention of any educational institution.

…

Chris Patten, the last British governor of Hong Kong and the University’s Chancellor, had it right when he said earlier this month that students were free to speak out against whatever they wish — Rhodes, racism or the British Empire — but not to erase history. If that’s what they need, “they should think about being educated elsewhere”:We have to listen to those who presume that they can re-write history within the confines of their own notion of what is politically, culturally and morally correct. We do have to listen, yes – but speaking for myself, I believe it would be intellectually pusillanimous to listen for too long without saying what we think, reaffirming the values that are at the heart of Karl Popper’s ‘Open Society’ and the generosity of spirit that animated the life of Nelson Mandela. One thing we should never tolerate is intolerance. We do not want to turn our university into a drab, bland, suburb of the soul where the diet is intellectual porridge.

It was a superb day for the Canadian preferred share market, with PerpetualDiscounts winning 108bp, FixedResets up 99bp and DeemedRetractibles gaining 75bp. The lengthy Performance Highlights table shows two HSE issues at the top – even as HSE was put on Trend-Negative by DBRS. Volume was average.

But however pleasant the day might have been, it’s a big relief to have finished the month! The TXPR Total Return index is down about 10.40% on the month while TXPL is down about 14.73%. This is stunning. As discussed on January 15, the worst month recorded by the BMO-CM “50” since 1993 was November, 2008, at -10.7%, while October, 2008, will probably slip to third place with a mere 8.2% loss. It’s incredible.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

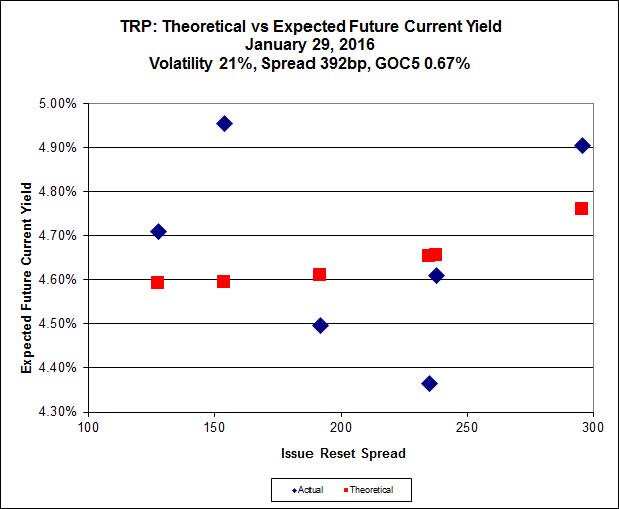

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.30 to be $1.07 rich, while TRP.PR.C, resetting 2021-1-30 at +154, is $0.88 cheap at its bid price of 11.15.

Click for Big

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 17.65 to be 1.04 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.89 to be 0.92 cheap.

Click for Big

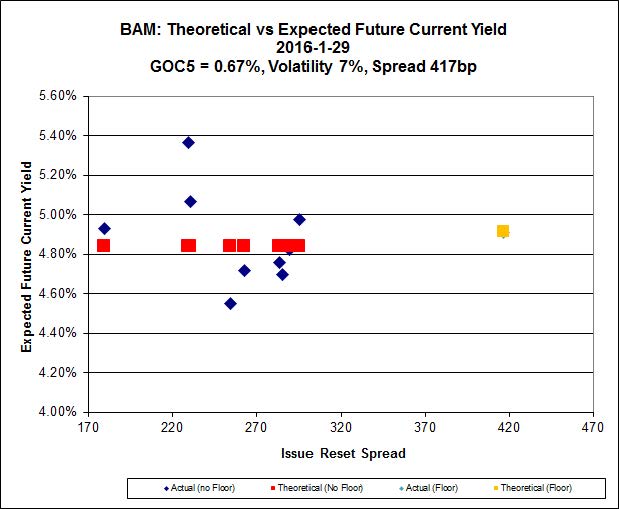

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.84 to be $1.50 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.70 and appears to be $1.07 rich.

Click for Big

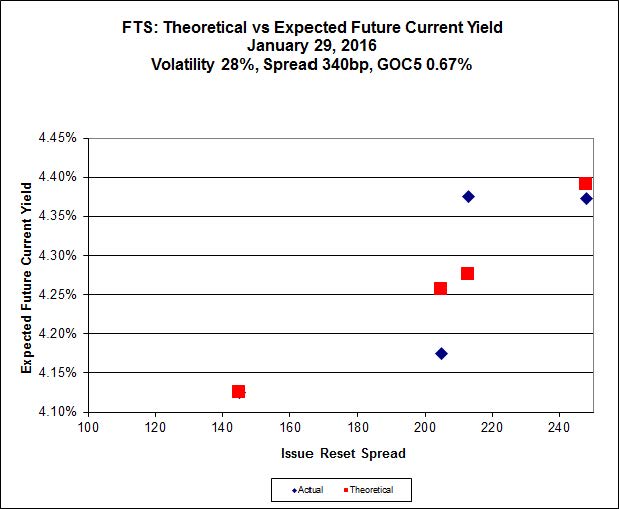

FTS.PR.K, with a spread of +205bp, and bid at 16.29, looks $0.32 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.00 and is $0.37 cheap.

Click for Big

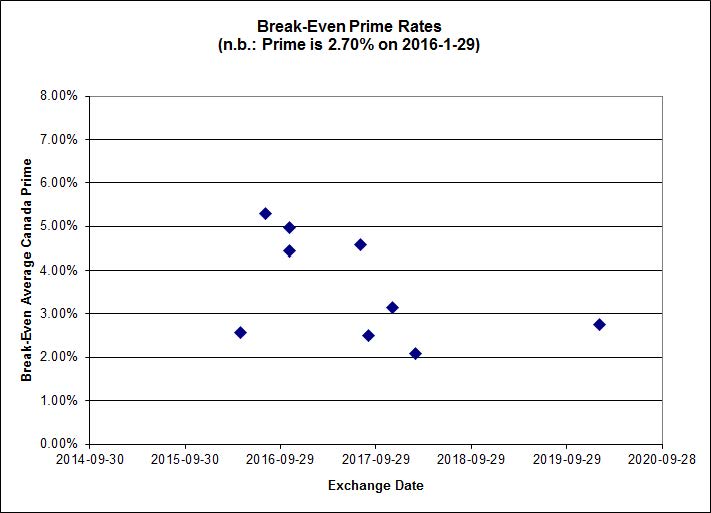

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.04%, with one outlier below -2.00% and one above 0.00%. There are two junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.29 % | 6.43 % | 19,060 | 16.17 | 1 | 0.0782 % | 1,474.7 |

| FixedFloater | 7.55 % | 6.59 % | 27,928 | 15.71 | 1 | 1.5323 % | 2,634.8 |

| Floater | 4.65 % | 4.77 % | 71,286 | 15.90 | 4 | 0.0984 % | 1,649.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4614 % | 2,697.2 |

| SplitShare | 4.90 % | 6.71 % | 81,879 | 2.72 | 6 | 0.4614 % | 3,156.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4614 % | 2,462.7 |

| Perpetual-Premium | 5.87 % | 5.85 % | 84,063 | 13.94 | 6 | 0.7474 % | 2,513.2 |

| Perpetual-Discount | 5.80 % | 5.86 % | 101,817 | 14.09 | 33 | 1.0802 % | 2,486.0 |

| FixedReset | 5.61 % | 4.96 % | 236,096 | 14.62 | 83 | 0.9863 % | 1,841.6 |

| Deemed-Retractible | 5.25 % | 5.68 % | 133,217 | 6.96 | 34 | 0.7483 % | 2,571.1 |

| FloatingReset | 2.98 % | 4.61 % | 57,808 | 5.57 | 13 | -0.0089 % | 2,016.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IAG.PR.G | FixedReset | -2.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 7.67 % |

| RY.PR.K | FloatingReset | -1.97 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 5.12 % |

| PWF.PR.S | Perpetual-Discount | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 20.44 Evaluated at bid price : 20.44 Bid-YTW : 5.91 % |

| GWO.PR.N | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.02 Bid-YTW : 11.63 % |

| GWO.PR.I | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.92 Bid-YTW : 7.07 % |

| RY.PR.P | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 23.99 Evaluated at bid price : 24.35 Bid-YTW : 5.38 % |

| BAM.PR.M | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 6.25 % |

| BMO.PR.Z | Perpetual-Discount | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.39 Evaluated at bid price : 22.70 Bid-YTW : 5.50 % |

| ELF.PR.F | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.01 Evaluated at bid price : 22.25 Bid-YTW : 6.00 % |

| GWO.PR.P | Deemed-Retractible | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.89 Bid-YTW : 6.15 % |

| BMO.PR.T | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.58 % |

| GWO.PR.G | Deemed-Retractible | 1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.08 Bid-YTW : 6.44 % |

| BNS.PR.M | Deemed-Retractible | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.32 Bid-YTW : 5.05 % |

| TRP.PR.F | FloatingReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 11.71 Evaluated at bid price : 11.71 Bid-YTW : 5.13 % |

| BAM.PF.D | Perpetual-Discount | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 6.29 % |

| PWF.PR.K | Perpetual-Discount | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.38 Evaluated at bid price : 21.38 Bid-YTW : 5.83 % |

| MFC.PR.B | Deemed-Retractible | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.27 Bid-YTW : 7.03 % |

| RY.PR.N | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.12 Evaluated at bid price : 22.46 Bid-YTW : 5.45 % |

| TD.PR.S | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 3.60 % |

| NA.PR.Q | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 4.76 % |

| MFC.PR.G | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.89 Bid-YTW : 8.37 % |

| CU.PR.E | Perpetual-Discount | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 5.85 % |

| CM.PR.O | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 4.58 % |

| BAM.PR.Z | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 5.26 % |

| TD.PF.F | Perpetual-Discount | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.16 Evaluated at bid price : 22.51 Bid-YTW : 5.46 % |

| PVS.PR.B | SplitShare | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 23.83 Bid-YTW : 6.39 % |

| POW.PR.G | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 23.71 Evaluated at bid price : 24.16 Bid-YTW : 5.83 % |

| CU.PR.D | Perpetual-Discount | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.27 Evaluated at bid price : 21.27 Bid-YTW : 5.87 % |

| RY.PR.A | Deemed-Retractible | 1.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.09 Bid-YTW : 5.13 % |

| RY.PR.O | Perpetual-Discount | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.08 Evaluated at bid price : 22.40 Bid-YTW : 5.46 % |

| RY.PR.G | Deemed-Retractible | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.17 Bid-YTW : 5.12 % |

| TRP.PR.A | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 14.40 Evaluated at bid price : 14.40 Bid-YTW : 4.86 % |

| IFC.PR.A | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.21 Bid-YTW : 10.53 % |

| GWO.PR.H | Deemed-Retractible | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.89 Bid-YTW : 6.82 % |

| BAM.PR.G | FixedFloater | 1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 25.00 Evaluated at bid price : 12.59 Bid-YTW : 6.59 % |

| ELF.PR.H | Perpetual-Discount | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.65 Evaluated at bid price : 23.00 Bid-YTW : 6.02 % |

| CU.PR.C | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.67 % |

| MFC.PR.H | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.54 Bid-YTW : 7.43 % |

| TRP.PR.G | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 5.09 % |

| CIU.PR.C | FixedReset | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 10.57 Evaluated at bid price : 10.57 Bid-YTW : 5.05 % |

| POW.PR.B | Perpetual-Discount | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.69 Evaluated at bid price : 22.98 Bid-YTW : 5.86 % |

| RY.PR.W | Perpetual-Discount | 1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.66 Evaluated at bid price : 22.90 Bid-YTW : 5.35 % |

| BAM.PR.X | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 12.53 Evaluated at bid price : 12.53 Bid-YTW : 5.41 % |

| CU.PR.F | Perpetual-Discount | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 5.79 % |

| POW.PR.A | Perpetual-Discount | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 23.83 Evaluated at bid price : 24.08 Bid-YTW : 5.86 % |

| FTS.PR.F | Perpetual-Discount | 2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.69 Evaluated at bid price : 21.94 Bid-YTW : 5.67 % |

| TD.PR.Y | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.83 Bid-YTW : 3.84 % |

| CU.PR.G | Perpetual-Discount | 2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 5.85 % |

| MFC.PR.I | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 8.15 % |

| BAM.PR.R | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 13.84 Evaluated at bid price : 13.84 Bid-YTW : 5.58 % |

| RY.PR.M | FixedReset | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.62 % |

| MFC.PR.N | FixedReset | 2.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.65 Bid-YTW : 8.21 % |

| PWF.PR.H | Perpetual-Premium | 2.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 24.29 Evaluated at bid price : 24.60 Bid-YTW : 5.87 % |

| BIP.PR.B | FixedReset | 2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 22.31 Evaluated at bid price : 23.05 Bid-YTW : 6.03 % |

| FTS.PR.K | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 16.29 Evaluated at bid price : 16.29 Bid-YTW : 4.64 % |

| HSE.PR.G | FixedReset | 2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 15.40 Evaluated at bid price : 15.40 Bid-YTW : 7.15 % |

| HSE.PR.C | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 14.10 Evaluated at bid price : 14.10 Bid-YTW : 7.23 % |

| BNS.PR.L | Deemed-Retractible | 2.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.20 Bid-YTW : 5.15 % |

| MFC.PR.F | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.05 Bid-YTW : 11.79 % |

| MFC.PR.M | FixedReset | 2.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.80 Bid-YTW : 8.17 % |

| FTS.PR.H | FixedReset | 2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 4.42 % |

| FTS.PR.J | Perpetual-Discount | 2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.70 % |

| BIP.PR.A | FixedReset | 2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 17.81 Evaluated at bid price : 17.81 Bid-YTW : 6.16 % |

| CCS.PR.C | Deemed-Retractible | 3.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.71 Bid-YTW : 7.11 % |

| FTS.PR.G | FixedReset | 3.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.76 % |

| FTS.PR.M | FixedReset | 3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 4.78 % |

| FTS.PR.I | FloatingReset | 3.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 10.70 Evaluated at bid price : 10.70 Bid-YTW : 4.52 % |

| PWF.PR.P | FixedReset | 3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 4.86 % |

| TRP.PR.B | FixedReset | 3.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 10.35 Evaluated at bid price : 10.35 Bid-YTW : 4.96 % |

| SLF.PR.H | FixedReset | 3.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.60 Bid-YTW : 10.22 % |

| PWF.PR.T | FixedReset | 4.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 3.82 % |

| HSE.PR.A | FixedReset | 4.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 8.90 Evaluated at bid price : 8.90 Bid-YTW : 6.96 % |

| HSE.PR.E | FixedReset | 5.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 7.20 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.G | FixedReset | 177,471 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.61 Bid-YTW : 5.05 % |

| NA.PR.X | FixedReset | 103,750 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 23.12 Evaluated at bid price : 24.94 Bid-YTW : 5.57 % |

| RY.PR.M | FixedReset | 56,839 | TD crossed 40,600 at 18.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 4.62 % |

| MFC.PR.G | FixedReset | 51,500 | Scotia crossed 40,000 at 17.66. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.89 Bid-YTW : 8.37 % |

| RY.PR.Q | FixedReset | 50,272 | Desjardins crossed 15,000 at 25.65. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-29 Maturity Price : 23.33 Evaluated at bid price : 25.61 Bid-YTW : 5.14 % |

| SLF.PR.H | FixedReset | 46,100 | Scotia crossed 40,000 at 14.30. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.60 Bid-YTW : 10.22 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BMO.PR.R | FloatingReset | Quote: 21.79 – 22.50 Spot Rate : 0.7100 Average : 0.5274 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 14.60 – 15.10 Spot Rate : 0.5000 Average : 0.3290 YTW SCENARIO |

| BMO.PR.S | FixedReset | Quote: 17.40 – 17.87 Spot Rate : 0.4700 Average : 0.3032 YTW SCENARIO |

| BNS.PR.P | FixedReset | Quote: 23.58 – 24.29 Spot Rate : 0.7100 Average : 0.5701 YTW SCENARIO |

| BAM.PF.F | FixedReset | Quote: 18.80 – 19.60 Spot Rate : 0.8000 Average : 0.6625 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 21.16 – 21.80 Spot Rate : 0.6400 Average : 0.5269 YTW SCENARIO |