We’ve blown a lot of money in Ontari-ari-ari-o, but at least the Chileans know how to make solar power useful:

Valhalla Energia is seeking partners to build a 600-megawatt solar project in Chile that will incorporate hydropower to deliver energy 24 hours a day.

The company is in talks with investors to raise as much as 40 percent of the estimated $1.3 billion needed for the project — $900 million for the solar component and $400 million for a 300-megawatt hydropower system — according to Juan Andres Camus, Santiago-based Valhalla’s co-founder and chief executive officer. The rest will come from bank loans.

“We are looking for sponsors that can be part of the project as equity,” Camus said in an interview in Santiago on March 18. “We are in advanced negotiations.”

The Cielos de Tarapaca solar project aims to produce electricity around the clock, using an integrated solar and hydro system that pumps sea water uphill to a reservoir during the day and letting it flow through turbines at night.

And today’s equity tip is: sell your hypodermic syringe manufacturing stock:

A stick-on patch that tracks, and even regulates, blood sugar levels could be used by people with diabetes one day, according to a new study.

Unlike finger pricking — the traditional method of monitoring levels of the blood sugar glucose — the new patch detects the levels of glucose in a person’s sweat. Research has shown that glucose levels in sweat accurately reflect glucose levels in the blood, the researchers said.

The researchers also showed that the patch can deliver the diabetes drug metformin through the skin and that it can reduce high blood glucose levels in mice with diabetes.

Meanwhile, Fed governor Charles Evans took a dovish stance on policy rates:

Federal Reserve Bank of Chicago President Charles Evans said policy makers rightly refrained from raising interest rates this month after a rocky start to the year clouded the economic outlook.

“The rationale for no rate change in March is that economic and financial risks seem somewhat higher for 2016 than we had hoped back last December when we first began raising rates,” Evans said Tuesday in a speech in Chicago. “Most of the Federal Open Market Committee’s cautionary pause in the rate normalization path is about assessing risks and just being careful.”

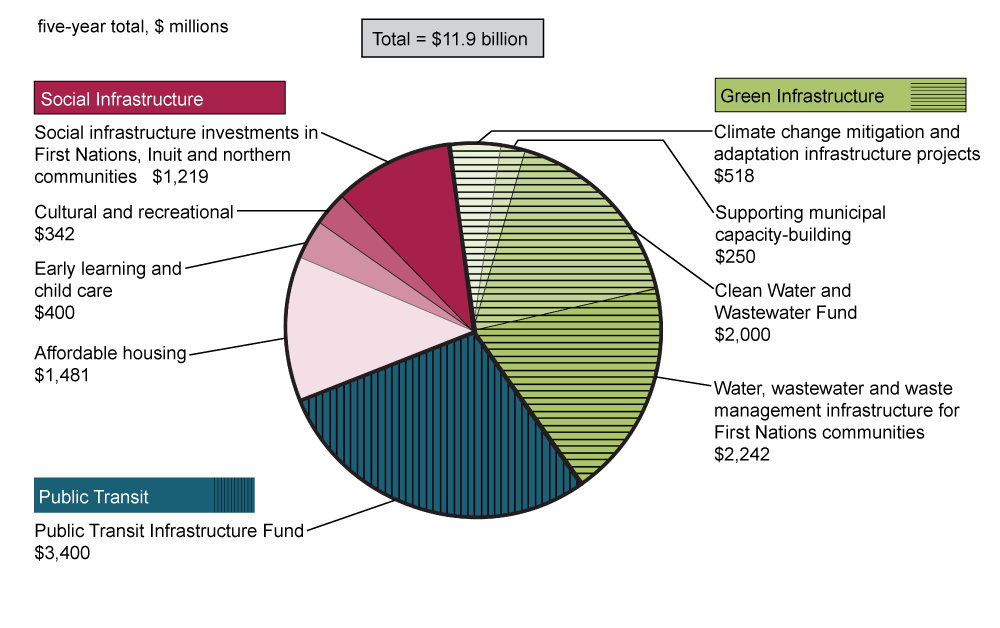

There was a federal budget today, which will be discussed by many more verbose people than me. So I’ll just say it’s pretty much as expected, with some stuff that looks halfway reasonable at first sight:

The Liberals have set aside $11.9-billion for public transit, affordable housing, wastewater systems and $3.4-billion to upgrade parks, harbours, border crossings, federal airports and to clean up contaminated sites across the country.

…. but looks like a ridiculous feel-good boondoggle at second glance:

Click for Big

… and some stuff which will be popular among morons, but is really just an exceptionally cruel way of ensuring the next generation is brought up in an isolated environment with no jobs, no hope, no future and nothing to do except drink:

Prime Minister Justin Trudeau promised “historic investments” to First Nations and the budget followed through with $8.4-billion for education, housing and clean drinking water.

… the return of the Subsidies For Sleazebags Programme:

To facilitate access to venture capital for small and medium-sized businesses and support saving by the middle class, Budget 2016 proposes to restore the Labour-Sponsored Venture Capital Corporations (LSVCC) tax credit to 15 per cent for share purchases of provincially registered LSVCCs for 2016 and subsequent tax years. The measure will provide federal tax relief of about $815 million over the 2015–16 to 2020–21 period.

The proposed bail-in regime has been endorsed, at least in principle:

To protect Canadian taxpayers in the unlikely event of a large bank failure, the Government is proposing to implement a bail-in regime that would reinforce that bank shareholders and creditors are responsible for the bank’s risks—not taxpayers. This would allow authorities to convert eligible long-term debt of a failing systemically important bank into common shares to recapitalize the bank and allow it to remain open and operating. Such a measure is in line with international efforts to address the potential risks to the financial system and broader economy of institutions perceived as “too-big-to-fail”.

The Government is proposing to introduce framework legislation for the regime along with accompanying enhancements to Canada’s bank resolution toolkit. Regulations and guidelines setting out further features of the regime will follow. This will provide stakeholders with an additional opportunity to comment on elements of the proposed regime.

So we’ll see how it goes.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.05 % | 6.15 % | 10,528 | 16.47 | 1 | 0.0000 % | 1,551.8 |

| FixedFloater | 7.07 % | 6.21 % | 24,391 | 16.05 | 1 | 0.6742 % | 2,812.6 |

| Floater | 4.67 % | 4.80 % | 64,968 | 15.87 | 4 | 1.8360 % | 1,658.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1288 % | 2,765.2 |

| SplitShare | 4.82 % | 5.69 % | 73,698 | 1.63 | 7 | -0.1288 % | 3,235.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1288 % | 2,524.7 |

| Perpetual-Premium | 5.79 % | -3.66 % | 86,040 | 0.08 | 6 | 0.1466 % | 2,553.4 |

| Perpetual-Discount | 5.65 % | 5.68 % | 96,764 | 14.38 | 33 | 0.0497 % | 2,567.7 |

| FixedReset | 5.43 % | 5.02 % | 185,513 | 13.84 | 87 | 0.9074 % | 1,879.5 |

| Deemed-Retractible | 5.25 % | 5.71 % | 131,519 | 6.91 | 34 | -0.0327 % | 2,591.4 |

| FloatingReset | 3.09 % | 4.99 % | 38,627 | 5.42 | 16 | 0.3662 % | 1,992.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BMO.PR.T | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.49 Evaluated at bid price : 17.49 Bid-YTW : 4.52 % |

| CU.PR.F | Perpetual-Discount | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 5.64 % |

| PWF.PR.P | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 12.15 Evaluated at bid price : 12.15 Bid-YTW : 4.84 % |

| HSE.PR.E | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 5.96 % |

| BMO.PR.Q | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.25 Bid-YTW : 7.93 % |

| TD.PF.B | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 4.44 % |

| TD.PF.C | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 4.43 % |

| SLF.PR.I | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.01 Bid-YTW : 8.00 % |

| FTS.PR.M | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.12 Evaluated at bid price : 17.12 Bid-YTW : 4.99 % |

| NA.PR.Q | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.56 Bid-YTW : 4.57 % |

| NA.PR.S | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.68 % |

| BAM.PF.G | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.23 Evaluated at bid price : 18.23 Bid-YTW : 5.22 % |

| SLF.PR.H | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.50 Bid-YTW : 9.36 % |

| TRP.PR.E | FixedReset | 1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.71 % |

| BAM.PF.H | FixedReset | 1.37 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.85 Bid-YTW : 4.20 % |

| CM.PR.O | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.35 Evaluated at bid price : 18.35 Bid-YTW : 4.43 % |

| BAM.PR.R | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 5.19 % |

| BAM.PF.F | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.26 Evaluated at bid price : 18.26 Bid-YTW : 5.18 % |

| NA.PR.W | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 16.78 Evaluated at bid price : 16.78 Bid-YTW : 4.78 % |

| TD.PF.A | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.43 % |

| BAM.PR.Z | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 5.29 % |

| BAM.PF.A | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 5.24 % |

| FTS.PR.K | FixedReset | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 15.65 Evaluated at bid price : 15.65 Bid-YTW : 4.79 % |

| TRP.PR.G | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 5.12 % |

| TRP.PR.D | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.01 Evaluated at bid price : 17.01 Bid-YTW : 4.86 % |

| TRP.PR.C | FixedReset | 1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.99 % |

| MFC.PR.L | FixedReset | 1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.20 Bid-YTW : 8.43 % |

| MFC.PR.H | FixedReset | 1.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.92 Bid-YTW : 7.11 % |

| CM.PR.Q | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.66 % |

| IFC.PR.A | FixedReset | 1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.91 Bid-YTW : 10.80 % |

| BAM.PF.B | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 5.23 % |

| BAM.PR.K | Floater | 2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 9.75 Evaluated at bid price : 9.75 Bid-YTW : 4.85 % |

| RY.PR.J | FixedReset | 2.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.71 Evaluated at bid price : 18.71 Bid-YTW : 4.72 % |

| BAM.PF.E | FixedReset | 2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 17.61 Evaluated at bid price : 17.61 Bid-YTW : 5.02 % |

| BAM.PR.B | Floater | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 9.85 Evaluated at bid price : 9.85 Bid-YTW : 4.80 % |

| BAM.PR.C | Floater | 2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 9.75 Evaluated at bid price : 9.75 Bid-YTW : 4.85 % |

| RY.PR.M | FixedReset | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 4.66 % |

| FTS.PR.I | FloatingReset | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 4.79 % |

| TRP.PR.B | FixedReset | 2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 10.65 Evaluated at bid price : 10.65 Bid-YTW : 4.80 % |

| TD.PF.D | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.59 % |

| TRP.PR.F | FloatingReset | 2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 12.00 Evaluated at bid price : 12.00 Bid-YTW : 4.94 % |

| IFC.PR.C | FixedReset | 2.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.00 Bid-YTW : 8.69 % |

| HSE.PR.A | FixedReset | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 5.99 % |

| BAM.PR.X | FixedReset | 3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 13.63 Evaluated at bid price : 13.63 Bid-YTW : 4.89 % |

| FTS.PR.H | FixedReset | 3.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 12.08 Evaluated at bid price : 12.08 Bid-YTW : 4.69 % |

| TRP.PR.A | FixedReset | 3.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 4.79 % |

| CU.PR.C | FixedReset | 4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 16.96 Evaluated at bid price : 16.96 Bid-YTW : 4.72 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.R | FixedReset | 182,165 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-24 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 5.07 % |

| BNS.PR.Q | FixedReset | 179,917 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.23 Bid-YTW : 4.48 % |

| GWO.PR.I | Deemed-Retractible | 103,710 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.03 Bid-YTW : 6.95 % |

| BNS.PR.R | FixedReset | 100,685 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.64 Bid-YTW : 4.42 % |

| PWF.PR.F | Perpetual-Discount | 94,846 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-22 Maturity Price : 23.09 Evaluated at bid price : 23.35 Bid-YTW : 5.70 % |

| BNS.PR.G | FixedReset | 93,805 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-07-25 Maturity Price : 25.00 Evaluated at bid price : 25.59 Bid-YTW : 5.05 % |

| There were 44 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.I | FloatingReset | Quote: 10.00 – 10.89 Spot Rate : 0.8900 Average : 0.5779 YTW SCENARIO |

| CU.PR.H | Perpetual-Discount | Quote: 23.30 – 24.00 Spot Rate : 0.7000 Average : 0.4468 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 22.15 – 22.69 Spot Rate : 0.5400 Average : 0.3560 YTW SCENARIO |

| ELF.PR.G | Perpetual-Discount | Quote: 20.07 – 20.52 Spot Rate : 0.4500 Average : 0.2843 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 21.00 – 21.45 Spot Rate : 0.4500 Average : 0.3091 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 15.58 – 16.03 Spot Rate : 0.4500 Average : 0.3173 YTW SCENARIO |