The Toronto-Dominion Bank has announced:

a domestic public offering of Non-Cumulative 5-Year Rate Reset Preferred Shares (non-viability contingent capital (NVCC)), Series 14 (the “Series 14 Shares”).

TD has entered into an agreement with a group of underwriters led by TD Securities Inc. to issue, on a bought deal basis, 12 million Series 14 Shares at a price of $25.00 per share to raise gross proceeds of $300 million. TD has also granted the underwriters an option to purchase, on the same terms, up to an additional 2 million Series 14 Shares. This option is exercisable in whole or in part by the underwriters at any time up to two business days prior to closing.

The Series 14 Shares will yield 4.85% annually, with dividends payable quarterly, as and when declared by the Board of Directors of TD, for the initial period ending October 31, 2021. Thereafter, the dividend rate will reset every five years at a level of 4.12% over the then five-year Government of Canada bond yield.

Subject to regulatory approval, on October 31, 2021 and on October 31 every 5 years thereafter, TD may redeem the Series 14 Shares, in whole or in part, at $25.00 per share. Subject to TD’s right of redemption and certain other conditions, holders of the Series 14 Shares will have the right to convert their shares into Non-Cumulative Floating Rate Preferred Shares (NVCC), Series 15 (the “Series 15 Shares”), on October 31, 2021, and on October 31 every five years thereafter. Holders of the Series 15 Shares will be entitled to receive quarterly floating rate dividends, as and when declared by the Board of Directors of TD, equal to the three-month Government of Canada Treasury bill yield plus 4.12%.

The expected closing date is September 8, 2016. TD will make an application to list the Series 14 Shares as of the closing date on the Toronto Stock Exchange. The net proceeds of the offering will be used for general corporate purposes.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of Non-Cumulative 5-Year Rate Reset Preferred Shares (non-viability contingent capital (NVCC)), Series 14 (the “Series 14 Shares”), the size of the offering has been increased to 40 million Series 14 Shares. The gross proceeds of the offering will now be $1 billion. The offering will be underwritten by a group of underwriters led by TD Securities Inc.

The expected closing date is September 8, 2016. TD will make an application to list the Series 14 Shares as of the closing date on the Toronto Stock Exchange. The net proceeds of the offering will be used for general corporate purposes.

Supersize me!

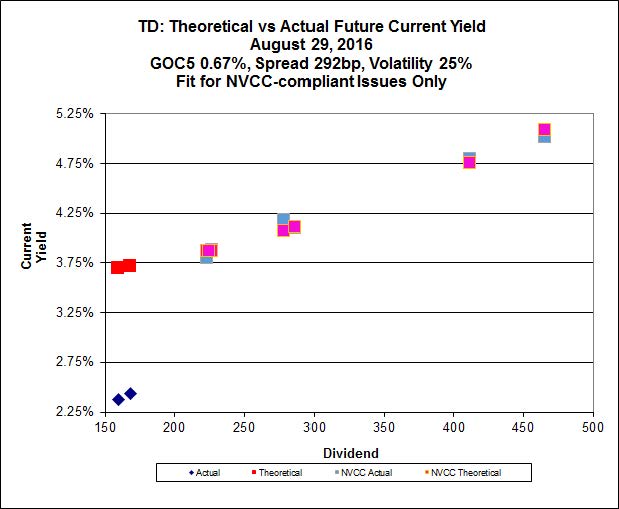

Implied Volatility analysis shows that the new issue is fairly priced relative to extant issues:

Click for Big

… provided one accepts that the calculated Implied Volatility value is OK. I claim that it isn’t – that the Implied Volatility of the spread should be in the high single digits and that therefore one can expect the curve to flatten, which implies that the high-spread issues are preferable. On the other hand, I also claim that spreads are currently far too high (a directional bias that contradicts the assumptions of Implied Volatility) and will decline substantially in the future, which implies that deeply discounted low-spread issues are preferable. So take your choice.

The issue attracted notice from David Berman in the Globe:

After five years, the yield on the new preferred shares will be 4.12 percentage points above the five-year bond yield, down more than half a percentage point.

For investors who love the idea of generating regular income in an environment where income is hard to find, the lower yields and reset rates are disappointing.

But TD is merely responding to market conditions. While preferred shares were a tough sell at the start of the year, the market appears more receptive today.

…

Yields may be down. But investor interest is heating up.

There were also some comments from Assiduous Readers.

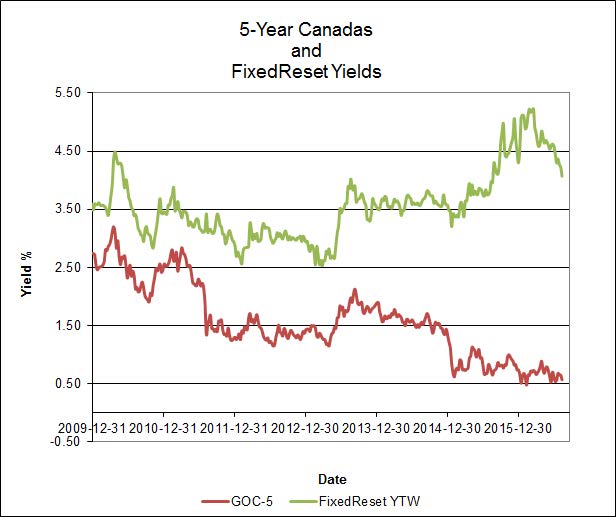

Here’s a chart comparing the yield (median YTW) of the FixedReset subindex with the five-year Canada yield, taken from PrefLetter. We are a long way from normalizing!

Click for Big

Thanks again James for all your work and drones updating. The table at the end of your post looks like what I am looking for but for the period from say 2000 to 2010 and I would have liked to limit my comparison with Canadian banks issues. I note from the one you have that the spread sharply increased by 50 bps at the end of 2014 (with GOC 5 going sharply lower) and by another 50 bps at the end of 2015 (with a sharp increase in the reset rates). NVCC compliant issued started to come in at the beginning of 2014 IIRC at +200bps which thereafter went as high as close to +500 bps. As a pure gut feeling, I would think that the “normality” for an investment grade bank NVCC compliant issue should be around +300bps. By how much the current spreads “are far too high” in your opinion? Rgds

… And for a third or fourth time, the Scotia follows up the TD within a week with a similar issue (smaller though)…