Click for Big

Well, let’s just be grateful that February is a short month:

Stocks tumbled for a seventh consecutive day on Friday, with the S&P 500 index falling about 0.8 percent, bringing its loss for the week to more than 11 percent. It was the worst weekly decline for stocks since the 2008 financial crisis. In early October that year, the S&P 500 fell about 18 percent.

The Dow Jones industrial average fell more than 1 percent on Friday.

…

Here’s how the major indexes around the world fared this week:S&P 500 in United States: ⬇️ 11%

Dow Jones in United States: ⬇️ 12%

FTSE 100 in Britain: ⬇️ 11%

DAX in Germany: ⬇️ 12%

KOSPI in South Korea: ⬇️ 8%

Hang Seng Index in Hong Kong: ⬇️ 4%

Nikkei 225 in Japan: ⬇️10%

I see the TSX Composite was down 2.72% today, and down 8.68% on the week.

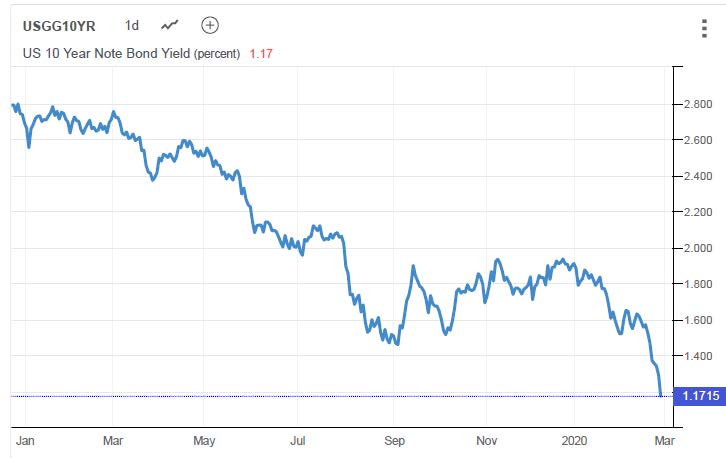

The yield on the benchmark 10-year United States Treasury bonds fell to a record low of 1.16 percent in trading Friday morning, down from 1.9 percent at the start of the year and 2.7 percent one year ago. From Japan to Germany to Australia, every other major economy is experiencing a similar shift.

Click for Big

TXPR closed at 590.00, down 1.74% on the day and the Total Return version down 4.30% on the week and 3.38% on the month. Volume today was 2.61-million, second-highest of the past thirty days, behind only January 30.

CPD closed at 11.77, down 1.51% on the day. Volume of 127,586 was the fourth-highest of the past 30 days … each of the three bigger days happened this week.

ZPR closed at 9.48, down 0.42% on the day. Volume of 734,205 was second-highest of the past 30 days, behind only February 24.

Five-year Canada yields were down 6bp to 1.07% today.

There is renewed speculation about a Fed rate cut:

Federal Reserve officials signaled a willingness to cut interest rates if the coronavirus outbreak worsens, laying out a scenario in which the central bank might respond as infections and quarantines spread globally.

“We could cut rates if we got a global pandemic that actually develops with health effects that seem to be approaching the same level as seasonal influenza, but that doesn’t look like the baseline as of today,” James Bullard, president of the Federal Reserve Bank of St. Louis, said during a speech in Florida on Friday. Mr. Bullard does not vote on rate moves this year, but he is one of 17 regional and Washington-based officials who participate in policy discussions.

… and Powell released a statement:

The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook. We will use our tools and act as appropriate to support the economy.

The decline in oil prices has taken its toll on oil stocks which has taken a toll on OSP.PR.A, which I have recommended that shareholders retract. The NAVPU was a mere 8.73 as of February 27 … and maybe even less today, eh? So, unless there’s a March Miracle, this thing’s going to default … not technically, because technically preferred shares don’t default, but, well, for all intents and purposes …

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.7037 % | 1,886.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -3.7037 % | 3,461.8 |

| Floater | 6.48 % | 6.74 % | 48,488 | 12.78 | 4 | -3.7037 % | 1,995.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8668 % | 3,432.9 |

| SplitShare | 4.85 % | 4.31 % | 45,205 | 3.67 | 6 | -0.8668 % | 4,099.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8668 % | 3,198.7 |

| Perpetual-Premium | 5.61 % | 4.93 % | 69,792 | 4.37 | 12 | -0.7941 % | 3,035.2 |

| Perpetual-Discount | 5.33 % | 5.42 % | 70,562 | 14.79 | 24 | -1.4526 % | 3,280.7 |

| FixedReset Disc | 5.89 % | 5.48 % | 179,782 | 14.64 | 64 | -2.4129 % | 2,037.5 |

| Deemed-Retractible | 5.23 % | 5.38 % | 67,731 | 14.58 | 27 | -1.0240 % | 3,213.3 |

| FloatingReset | 6.28 % | 6.23 % | 66,123 | 13.55 | 3 | -2.6502 % | 2,330.6 |

| FixedReset Prem | 5.14 % | 4.32 % | 131,257 | 1.55 | 22 | -0.7786 % | 2,631.6 |

| FixedReset Bank Non | 1.93 % | 3.39 % | 90,321 | 1.88 | 3 | -0.0543 % | 2,750.9 |

| FixedReset Ins Non | 5.71 % | 5.36 % | 95,875 | 14.69 | 22 | -2.3877 % | 2,075.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.A | Floater | -6.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 11.51 Evaluated at bid price : 11.51 Bid-YTW : 6.06 % |

| BAM.PR.B | Floater | -5.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 10.32 Evaluated at bid price : 10.32 Bid-YTW : 6.83 % |

| MFC.PR.F | FixedReset Ins Non | -4.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 11.28 Evaluated at bid price : 11.28 Bid-YTW : 5.47 % |

| PVS.PR.G | SplitShare | -4.67 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 24.08 Bid-YTW : 5.64 % |

| TD.PF.D | FixedReset Disc | -4.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 5.39 % |

| IAF.PR.B | Deemed-Retractible | -4.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.40 % |

| W.PR.K | FixedReset Prem | -4.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.14 Evaluated at bid price : 24.62 Bid-YTW : 5.46 % |

| BAM.PF.B | FixedReset Disc | -4.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.93 Evaluated at bid price : 16.93 Bid-YTW : 5.84 % |

| HSE.PR.A | FixedReset Disc | -4.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 10.10 Evaluated at bid price : 10.10 Bid-YTW : 7.00 % |

| EMA.PR.F | FixedReset Disc | -4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.51 Evaluated at bid price : 16.51 Bid-YTW : 5.88 % |

| RY.PR.J | FixedReset Disc | -4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.42 Evaluated at bid price : 17.42 Bid-YTW : 5.51 % |

| TRP.PR.C | FixedReset Disc | -4.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 10.80 Evaluated at bid price : 10.80 Bid-YTW : 6.08 % |

| BMO.PR.C | FixedReset Disc | -3.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 5.37 % |

| TRP.PR.B | FixedReset Disc | -3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 10.10 Evaluated at bid price : 10.10 Bid-YTW : 5.82 % |

| TD.PF.E | FixedReset Disc | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 5.44 % |

| HSE.PR.G | FixedReset Disc | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 6.89 % |

| NA.PR.W | FixedReset Disc | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 5.57 % |

| SLF.PR.H | FixedReset Ins Non | -3.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 14.85 Evaluated at bid price : 14.85 Bid-YTW : 5.40 % |

| TD.PF.J | FixedReset Disc | -3.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 5.39 % |

| NA.PR.S | FixedReset Disc | -3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.51 % |

| BAM.PR.X | FixedReset Disc | -3.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 12.01 Evaluated at bid price : 12.01 Bid-YTW : 6.04 % |

| BAM.PR.C | Floater | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 10.46 Evaluated at bid price : 10.46 Bid-YTW : 6.74 % |

| CU.PR.F | Perpetual-Discount | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.21 Evaluated at bid price : 21.21 Bid-YTW : 5.34 % |

| RY.PR.H | FixedReset Disc | -3.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.39 Evaluated at bid price : 16.39 Bid-YTW : 5.24 % |

| MFC.PR.Q | FixedReset Ins Non | -3.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 5.30 % |

| MFC.PR.R | FixedReset Ins Non | -3.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.79 Evaluated at bid price : 23.12 Bid-YTW : 5.29 % |

| TRP.PR.G | FixedReset Disc | -3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.41 Evaluated at bid price : 17.41 Bid-YTW : 5.81 % |

| MFC.PR.K | FixedReset Ins Non | -3.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 5.33 % |

| BNS.PR.I | FixedReset Disc | -3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 5.13 % |

| NA.PR.C | FixedReset Disc | -3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 5.50 % |

| POW.PR.D | Perpetual-Discount | -3.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.60 Evaluated at bid price : 22.85 Bid-YTW : 5.54 % |

| BMO.PR.D | FixedReset Disc | -3.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 5.41 % |

| BAM.PF.A | FixedReset Disc | -3.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 5.70 % |

| SLF.PR.G | FixedReset Ins Non | -3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 11.83 Evaluated at bid price : 11.83 Bid-YTW : 5.24 % |

| BMO.PR.E | FixedReset Disc | -3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 5.25 % |

| BAM.PR.T | FixedReset Disc | -3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 14.37 Evaluated at bid price : 14.37 Bid-YTW : 6.01 % |

| GWO.PR.Q | Deemed-Retractible | -3.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.23 Evaluated at bid price : 23.71 Bid-YTW : 5.50 % |

| TRP.PR.F | FloatingReset | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 12.90 Evaluated at bid price : 12.90 Bid-YTW : 6.57 % |

| CM.PR.O | FixedReset Disc | -2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.73 Evaluated at bid price : 15.73 Bid-YTW : 5.60 % |

| TRP.PR.A | FixedReset Disc | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 5.79 % |

| CM.PR.S | FixedReset Disc | -2.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.28 Evaluated at bid price : 17.28 Bid-YTW : 5.42 % |

| CM.PR.Q | FixedReset Disc | -2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 5.60 % |

| MFC.PR.L | FixedReset Ins Non | -2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.22 Evaluated at bid price : 15.22 Bid-YTW : 5.55 % |

| NA.PR.G | FixedReset Disc | -2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.77 Evaluated at bid price : 18.77 Bid-YTW : 5.48 % |

| TRP.PR.D | FixedReset Disc | -2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 5.88 % |

| MFC.PR.M | FixedReset Ins Non | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 5.34 % |

| CM.PR.R | FixedReset Disc | -2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.52 Evaluated at bid price : 20.52 Bid-YTW : 5.48 % |

| BMO.PR.S | FixedReset Disc | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 5.34 % |

| MFC.PR.J | FixedReset Ins Non | -2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 5.36 % |

| IAF.PR.I | FixedReset Ins Non | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 5.32 % |

| TD.PF.I | FixedReset Disc | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.09 Evaluated at bid price : 20.09 Bid-YTW : 5.22 % |

| IAF.PR.G | FixedReset Ins Non | -2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 5.45 % |

| PWF.PR.Q | FloatingReset | -2.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 12.48 Evaluated at bid price : 12.48 Bid-YTW : 6.23 % |

| RY.PR.Z | FixedReset Disc | -2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 5.23 % |

| BMO.PR.Y | FixedReset Disc | -2.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 5.41 % |

| BAM.PR.R | FixedReset Disc | -2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 14.22 Evaluated at bid price : 14.22 Bid-YTW : 5.98 % |

| MFC.PR.I | FixedReset Ins Non | -2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.08 Evaluated at bid price : 18.08 Bid-YTW : 5.54 % |

| EMA.PR.E | Perpetual-Discount | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 5.28 % |

| TD.PF.B | FixedReset Disc | -2.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 5.32 % |

| PWF.PR.P | FixedReset Disc | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 12.38 Evaluated at bid price : 12.38 Bid-YTW : 5.42 % |

| SLF.PR.J | FloatingReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 11.82 Evaluated at bid price : 11.82 Bid-YTW : 6.09 % |

| HSE.PR.C | FixedReset Disc | -2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.92 Evaluated at bid price : 15.92 Bid-YTW : 6.99 % |

| TD.PF.K | FixedReset Disc | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.26 % |

| CM.PR.P | FixedReset Disc | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 5.61 % |

| BMO.PR.T | FixedReset Disc | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.99 Evaluated at bid price : 15.99 Bid-YTW : 5.34 % |

| TRP.PR.E | FixedReset Disc | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 5.82 % |

| BAM.PR.N | Perpetual-Discount | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.35 Evaluated at bid price : 21.62 Bid-YTW : 5.58 % |

| BAM.PR.M | Perpetual-Discount | -2.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.36 Evaluated at bid price : 21.63 Bid-YTW : 5.57 % |

| MFC.PR.G | FixedReset Ins Non | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.91 Evaluated at bid price : 17.91 Bid-YTW : 5.55 % |

| RY.PR.M | FixedReset Disc | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 5.31 % |

| SLF.PR.I | FixedReset Ins Non | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.54 Evaluated at bid price : 17.54 Bid-YTW : 5.42 % |

| TD.PF.M | FixedReset Disc | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.56 Evaluated at bid price : 23.45 Bid-YTW : 5.06 % |

| BAM.PF.C | Perpetual-Discount | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.81 Evaluated at bid price : 21.81 Bid-YTW : 5.66 % |

| CU.PR.H | Perpetual-Discount | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.75 Evaluated at bid price : 24.24 Bid-YTW : 5.42 % |

| BAM.PF.G | FixedReset Disc | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 6.00 % |

| HSE.PR.E | FixedReset Disc | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 7.10 % |

| MFC.PR.N | FixedReset Ins Non | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.97 Evaluated at bid price : 15.97 Bid-YTW : 5.29 % |

| RY.PR.S | FixedReset Disc | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.96 Evaluated at bid price : 18.96 Bid-YTW : 4.97 % |

| IFC.PR.E | Deemed-Retractible | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.61 Evaluated at bid price : 24.01 Bid-YTW : 5.49 % |

| TRP.PR.K | FixedReset Prem | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.49 Evaluated at bid price : 24.90 Bid-YTW : 4.88 % |

| TD.PF.L | FixedReset Disc | -1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.44 Evaluated at bid price : 23.20 Bid-YTW : 4.89 % |

| EMA.PR.C | FixedReset Disc | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 5.76 % |

| GWO.PR.N | FixedReset Ins Non | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 12.51 Evaluated at bid price : 12.51 Bid-YTW : 4.79 % |

| BIP.PR.F | FixedReset Disc | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.68 Evaluated at bid price : 21.98 Bid-YTW : 5.79 % |

| SLF.PR.A | Deemed-Retractible | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.66 Evaluated at bid price : 21.91 Bid-YTW : 5.41 % |

| GWO.PR.S | Deemed-Retractible | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.22 Evaluated at bid price : 24.51 Bid-YTW : 5.43 % |

| SLF.PR.B | Deemed-Retractible | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.91 Evaluated at bid price : 22.15 Bid-YTW : 5.41 % |

| GWO.PR.G | Deemed-Retractible | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.63 Evaluated at bid price : 23.90 Bid-YTW : 5.52 % |

| PWF.PR.L | Perpetual-Discount | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.10 Evaluated at bid price : 23.36 Bid-YTW : 5.51 % |

| CU.PR.G | Perpetual-Discount | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.26 Evaluated at bid price : 21.26 Bid-YTW : 5.32 % |

| IFC.PR.C | FixedReset Ins Non | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 5.66 % |

| POW.PR.C | Perpetual-Premium | -1.75 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-29 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 2.12 % |

| BIP.PR.D | FixedReset Disc | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.35 Evaluated at bid price : 22.65 Bid-YTW : 5.51 % |

| POW.PR.B | Perpetual-Discount | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.15 Evaluated at bid price : 24.40 Bid-YTW : 5.55 % |

| GWO.PR.H | Deemed-Retractible | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.44 Evaluated at bid price : 22.70 Bid-YTW : 5.42 % |

| PWF.PR.K | Perpetual-Discount | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.60 Evaluated at bid price : 22.85 Bid-YTW : 5.47 % |

| CU.PR.E | Perpetual-Discount | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.73 Evaluated at bid price : 23.00 Bid-YTW : 5.34 % |

| CU.PR.D | Perpetual-Discount | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.59 Evaluated at bid price : 22.86 Bid-YTW : 5.38 % |

| GWO.PR.T | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.79 Evaluated at bid price : 24.20 Bid-YTW : 5.39 % |

| TD.PF.A | FixedReset Disc | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.34 Evaluated at bid price : 16.34 Bid-YTW : 5.27 % |

| MFC.PR.H | FixedReset Ins Non | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 19.62 Evaluated at bid price : 19.62 Bid-YTW : 5.38 % |

| BAM.PF.E | FixedReset Disc | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 15.55 Evaluated at bid price : 15.55 Bid-YTW : 5.93 % |

| CM.PR.Y | FixedReset Disc | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 22.69 Evaluated at bid price : 23.72 Bid-YTW : 5.07 % |

| BAM.PR.Z | FixedReset Disc | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.37 Evaluated at bid price : 18.37 Bid-YTW : 5.75 % |

| MFC.PR.O | FixedReset Ins Non | -1.55 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 25.34 Bid-YTW : 4.31 % |

| TD.PF.C | FixedReset Disc | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.59 Evaluated at bid price : 16.59 Bid-YTW : 5.31 % |

| CIU.PR.A | Perpetual-Discount | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.23 Evaluated at bid price : 21.23 Bid-YTW : 5.45 % |

| EMA.PR.H | FixedReset Prem | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.20 Evaluated at bid price : 24.70 Bid-YTW : 4.91 % |

| PWF.PR.F | Perpetual-Discount | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.92 Evaluated at bid price : 24.16 Bid-YTW : 5.48 % |

| IFC.PR.G | FixedReset Ins Non | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 5.48 % |

| POW.PR.G | Perpetual-Premium | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.67 Evaluated at bid price : 25.00 Bid-YTW : 5.67 % |

| PWF.PR.E | Perpetual-Premium | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.46 Evaluated at bid price : 24.70 Bid-YTW : 5.62 % |

| POW.PR.A | Perpetual-Premium | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.64 Evaluated at bid price : 24.90 Bid-YTW : 5.70 % |

| RY.PR.W | Perpetual-Discount | -1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.22 Evaluated at bid price : 24.51 Bid-YTW : 5.02 % |

| SLF.PR.C | Deemed-Retractible | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.78 Evaluated at bid price : 20.78 Bid-YTW : 5.36 % |

| GWO.PR.P | Deemed-Retractible | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.60 Evaluated at bid price : 24.85 Bid-YTW : 5.52 % |

| BMO.PR.Z | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.13 Evaluated at bid price : 24.63 Bid-YTW : 5.08 % |

| MFC.PR.C | Deemed-Retractible | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.99 Evaluated at bid price : 20.99 Bid-YTW : 5.38 % |

| SLF.PR.D | Deemed-Retractible | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 20.92 Evaluated at bid price : 20.92 Bid-YTW : 5.32 % |

| EML.PR.A | FixedReset Ins Non | -1.08 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-17 Maturity Price : 25.00 Evaluated at bid price : 25.61 Bid-YTW : 4.15 % |

| BAM.PF.I | FixedReset Prem | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.54 Evaluated at bid price : 24.93 Bid-YTW : 4.92 % |

| PWF.PR.T | FixedReset Disc | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 5.30 % |

| GWO.PR.I | Deemed-Retractible | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.20 Evaluated at bid price : 21.20 Bid-YTW : 5.40 % |

| BAM.PF.F | FixedReset Disc | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.70 Evaluated at bid price : 16.70 Bid-YTW : 6.04 % |

| CCS.PR.C | Deemed-Retractible | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.30 % |

| BAM.PF.D | Perpetual-Discount | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 21.99 Evaluated at bid price : 21.99 Bid-YTW : 5.67 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.R | FixedReset Disc | 44,757 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 14.22 Evaluated at bid price : 14.22 Bid-YTW : 5.98 % |

| TD.PF.H | FixedReset Prem | 42,428 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 25.49 Bid-YTW : 3.88 % |

| IFC.PR.I | Perpetual-Premium | 38,800 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 24.55 Evaluated at bid price : 24.94 Bid-YTW : 5.44 % |

| TD.PF.J | FixedReset Disc | 33,710 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 18.51 Evaluated at bid price : 18.51 Bid-YTW : 5.39 % |

| RY.PR.Z | FixedReset Disc | 33,010 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 5.23 % |

| TD.PF.A | FixedReset Disc | 30,896 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-02-28 Maturity Price : 16.34 Evaluated at bid price : 16.34 Bid-YTW : 5.27 % |

| There were 72 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| W.PR.K | FixedReset Prem | Quote: 24.62 – 26.19 Spot Rate : 1.5700 Average : 0.8641 YTW SCENARIO |

| PVS.PR.G | SplitShare | Quote: 24.08 – 25.45 Spot Rate : 1.3700 Average : 0.7731 YTW SCENARIO |

| HSE.PR.E | FixedReset Disc | Quote: 16.70 – 18.36 Spot Rate : 1.6600 Average : 1.1052 YTW SCENARIO |

| SLF.PR.I | FixedReset Ins Non | Quote: 17.54 – 18.35 Spot Rate : 0.8100 Average : 0.5194 YTW SCENARIO |

| RY.PR.J | FixedReset Disc | Quote: 17.42 – 18.24 Spot Rate : 0.8200 Average : 0.5307 YTW SCENARIO |

| EMA.PR.H | FixedReset Prem | Quote: 24.70 – 25.47 Spot Rate : 0.7700 Average : 0.4832 YTW SCENARIO |

Here are some proposals to make the investment climate even more ‘wonderful’ in Canada. NDP plus liberals eyeing to bump the capital gains tax to 75% inclusion.

https://nationalpost.com/opinion/john-ivison-expanding-capital-gains-tax-would-be-very-short-sighted-approach-to-fighting-federal-deficit

Let’s hope they have better sense of timing. But they see $8 billion in new revenue and a bridge to win over NDP.

I think they should just bump the GST to 10% and be done with it. We are so European in everything, why should the GST lag? Most of Europe has VAT between 20 to 30%, so we are not taxed enough.

How do you spell “SIB”?

I’m looking at you specifically Prem Watsa. Time to put that big pile of cash on your balance sheet to work buying back common and preferred shares.

Companies flush with cash or able to borrow long really ought to act to reduce their WACC right about now.

For that 20% VAT Europeans get free university, free extended health and a much better pension system. I don’t mind paying more but I want value in return.

For the moment when the equity markets have sorted out their mess, at least temporarily, the preferred market is now worrying about falling rates.

This market worries about falling equities, falling yields, rising yields, corona virus, recession, change in dividend tax credits, credit ratings of issuers, oil prices….

And then there are Tesla investors happily flipping away stuff on their RobindHood screens.

boy are the preferred investors carrying all the worries of the world on their shoulders 🙂

I would love to see a TOP 20 preferred stocks list. I purchased your newsletter a couple of times and still find it difficult to decipher. (Lack of knowledge on my part). I bought some perferred over the years and have paid dearly for it. The preferred market has been massacred.

Anyways, just a thought. I would subscribe to it, for sure. Of course they would change monthly as prices move.

And on the more serious side, just look at what Brookfiled is paying for its debentures versus what’s the yield on their perpetuals. And looking at just how efficient they are with financing, they didn’t even want to overpay for an extra year at a higher rate and recalled their debentures paying 5.3%.

30 year notes yielding 3.5%.

https://bam.brookfield.com/press-releases/2020/02-18-2020-220808435

Brookfield Asset Management Inc. (“Brookfield”) (TSX: BAM.A, NYSE: BAM) today announced the pricing of its previously announced public offering of notes due 2050 (the “notes”). The size of the offering will be US$600 million.

The notes will have a coupon of 3.450% and will be issued at a price equal to 99.058% of their face value for an effective yield of 3.501%. The notes will be issued by Brookfield Finance LLC, an indirect 100% owned subsidiary of Brookfield, and will be fully and unconditionally guaranteed by Brookfield. The net proceeds from the sale of the notes will be used to redeem all of the outstanding Cdn$350 million aggregate principal amount of 5.30% notes due March 1, 2021 issued by Brookfield and the remainder for general corporate purposes. The offering is expected to close on or about February 21, 2020.