I was disgusted to read an opinion piece in the Globe titled The weakest links in terror finance legislation need to be addressed:

Group of 20 leaders turned their focus to the financing question this week when they met in Antalya, Turkey. Leaders committed themselves to combatting terrorist financing by enhancing the exchange of information; criminalizing terrorist financing and implementing targeted financial-sanction regimes related to terrorism and terrorist financing; and facilitating the widespread implementation of standards developed by the Financial Action Task Force (FATF), the international institution responsible for combatting money laundering and terrorist financing.

This is just another job application from the Merchants Of Fear (Secret Police Edition).

“But conducting attacks in the heart of Europe requires a complex series of financial transactions between IS supporters and the cells committing acts of terrorism.”

It will be noted that the authors do not give any examples of these “complex series of financial transactions” that are supposedly so ubiquitous; they do not give any specifics of what new laws and regulations might be sufficient to choke off this source of funds; and they do not provide any sort of cost-benefit analysis to show that the problem justifies the solution.

That’s because they can’t. According to John Allison (who ran the BB&T bank with distinction through the Credit Crunch) the US “Patriot Act” costs US banks over $5-billion annually and “there has never been a single terrorist caught and convicted because of the Patriot Act.” Instead, the Patriot Act has enabled government snooping that, so far, has achieved success in nailing Eliot Switzer (a guy who hired prostitutes) and Dennis Hastert (a blackmail victim desperate to pay his blackmailer). Oh, very well done and well worth $5-billion per year.

The authors admit that “very few jurisdictions have obtained successful convictions”, but do not have the intestinal fortitude to admit why this should be – and the simple fact is that terrorist operations do not cost a great deal of money. Al Qaeda spent only about half a million dollars to finance the entire 9/11 plot; only about $300,000 of this was spent in the US. So, be generous, call it $20,000 per attacker during their stay of over a year in the US.

It’s no surprise that Momani and Kempthorne are so shy when it comes to talking about the specifics of their wonderful plans!

The entire article is nothing more than demagogic nonsense, seeking to expand useless banking regulations and even more useless bureaucratic oversight, through panicking the populace. But hey, I suppose the authors will get paid.

However, I was inspired to read the TERRORIST FINANCING FATF REPORT TO G20 LEADERS ACTIONS BEING TAKEN BY THE FATF, most notable for its casual request for more money:

The G20 can support this programme by: leading by example, helping low capacity jurisdictions implement essential counter terrorist financing measures, and continuing to support the FATF in its ongoing work.

…

The number of domestic designations varies widely. Thirty-seven jurisdictions have applied targeted financial sanctions on their own motion, and there is a significant variation in the number of entities, and the value of assets frozen, as shown in the table below. This may result from the nature of the terrorist and terrorist financing activity in each country, and from the different roles that targeted financial sanctions play in the context of national counter-terrorism strategies – in particular whether they are directed at restraining individuals or value, or both.

Click for Big

Pretty good, eh? Canada’s FINTRAC has a budget of about $50-million p.a. and imposes immense costs on financial intermediaries and has managed to freeze almost €100,000 in assets allegedly belonging to alleged terrorists, including “funds subsequently un-frozen or confiscated, as well as funds frozen currently”. I would dearly love to see a detailed breakdown of this number with the facts of each case attached.

And in France, the usual suspension of civil liberties (and, I’ll guess, harassment of annoying people) is occurring:

All over France, from Toulouse in the south to Paris and beyond, the police have been breaking down doors, conducting searches without warrants, aggressively questioning residents, hauling suspects to police stations and putting others under house arrest.

The extraordinary steps are now perfectly legal under the state of emergency decreed by the government after the attacks on Nov. 13 in Paris that left 130 dead — a rare kind of mobilization that will continue. The French Parliament voted last week to extend the emergency for three more months, which means more warrantless searches, more interrogations, more people placed under house arrest.

There have been 1,072 police searches already and 139 police interrogations, and 117 people have been placed in custody, the Ministry of the Interior said on Monday.

On the other hand, I was pleased to read an article regarding another favourite theme: Britain is cutting green energy subsidies:

Wind and solar farms will be forced to pay for the extra costs they impose on the UK’s electricity system as a result of their intermittent nature, Amber Rudd, the energy secretary has announced.

Renewable generators will be held “responsible for the pressures they add to the system when the wind does not blow or the sun does not shine”, she said, under new plans being drawn up by the Department of Energy and Climate Change.

In a long-awaited policy “reset” speech, Ms Rudd also unveiled plans to offer billions of pounds of new subsidies for offshore wind farms, potentially doubling the UK’s offshore wind capacity with a further 10 gigawatts in the 2020s, on top of 10GW expected by 2020.

However, she said that offshore wind remained “too expensive” and that the cash would be strictly conditional on deep cost reductions.

In the referenced policy reset speech:

Britain will no longer pursue green energy at all costs and will instead make keeping the lights on the top priority, Amber Rudd, the energy secretary, will vow this week.

Households already face paying over-the-odds for energy for years to come as a result of expensive subsidies handed out to wind and solar farms by her Labour and Lib Dem predecessors, Ms Rudd will warn.

In a major speech setting out a new strategy, the energy secretary is expected to say that from now on, policies will balance “the need to decarbonise with the need to keep bills as low as possible”.

…

Although the Government wants gas plants to replace coal, Ms Rudd is expected to admit that the UK electricity market is now so distorted by subsidies that “no form of power generation, not even gas-fired power stations, can be built without government intervention”.

…

In what will be seen as criticism of her Lib Dem predecessor, Ed Davey, Ms Rudd will say that “contracts were signed with no competition and could have offered better value for money” – an apparent reference to subsidy contracts handed out to offshore wind farms in early 2014.Only in the final months of the Coalition were subsequent offshore wind projects forced to compete for the payments – revealing they could be built with far lower levels of subsidy.

And finally, to return to the financial markets that are supposed to be the subject of this blog, CAD options markets are looking bearish for the loonie:

Traders are positioning themselves for what could be the last leg down in the Canadian dollar’s three-year collapse.

They’re paying the biggest premium since September for options contracts that protect against currency swings expiring a month from now than for similar contracts that expire three months out, as oil suddenly threatens to fall below $40 per barrel again and the U.S. Federal Reserve looks set to raise interest rates in a matter of weeks. The last time the premium for 30-day protection spiked this high the currency ended up falling to an 11-year low before month’s end.

The options market is lining up with the consensus forecast of economists, who also see weakness in the short term followed by stabilization and ultimately gains into 2016. For many, the Fed’s first interest-rate increase in almost a decade and the most recent surge in oil inventories could mark the last stage of the Canadian dollar’s 25 per cent, three-year slide.

And the market is increasingly expectant of a Fed hike:

The odds the Federal Reserve will raise interest rates at its next meeting in December climbed to 74 percent, and Pacific Investment Management Co. says a move is likely.

The probability the central bank will act at its Dec. 15-16 session increased from less than 30 percent as recently as mid-October, futures contracts show. The U.S. is scheduled to sell $35 billion of five-year notes Tuesday, after a two-year auction Monday drew the highest yield in five years, reflecting expectations among traders for rising interest rates.

Click for Big

And, to get back to non-financial news, the FAA has released proposed regulations for drones:

The recommendations, from a task force created by the agency, would be the biggest step yet by the government to deal with the proliferation of recreational drones, which are usually used for harmless purposes but have also been tools for mischief and serious wrongdoing, and pose a risk to airborne jets.

…

The task force did not go as far with its recommendations as some aviation and security experts had hoped. The proposals say owners should not have to submit any information about their aircraft, for example. It also said there should not be a requirement for drone users to be citizens or permanent residents.

…

The F.A.A. task force was composed of 25 people, including representatives of drone makers, technology companies, an airline pilots association and government officials. The agency gave them a short time — four weeks — to come up with recommendations on a registration system. The F.A.A. said it would take the recommendations into consideration and then write new rules.Members of the task force stressed on Monday that many compromises were made. The task force wrote in its report that the goal of the registration process was to “ensure accountability by creating a traceable link between aircraft and owner, and to encourage the maximum levels of regulatory compliance by making the registration process as simple as possible.”

“We tried to write it in as generic a flavor as possible,” Dave Vos, a member of the task force and the head of a drone project at Google X, a business that works on future technologies, said in a conference call.

With the “consensus we reached, everyone is quite happy here,” he said.

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts down 50bp, FixedResets losing 54bp and DeemedRetractibles off 24bp. The Performance Highlights table is enormous. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

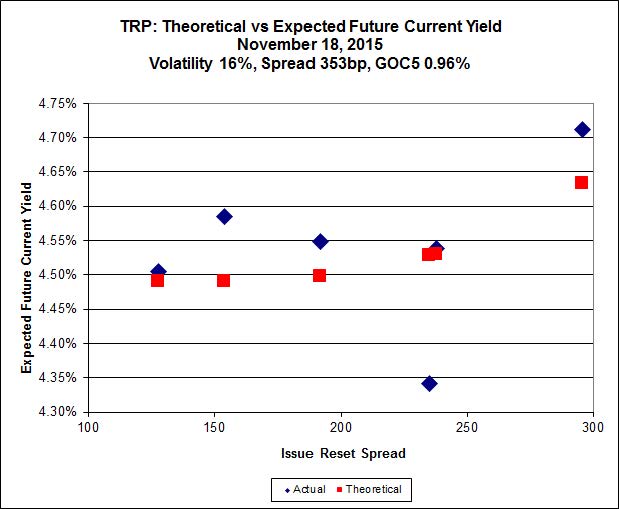

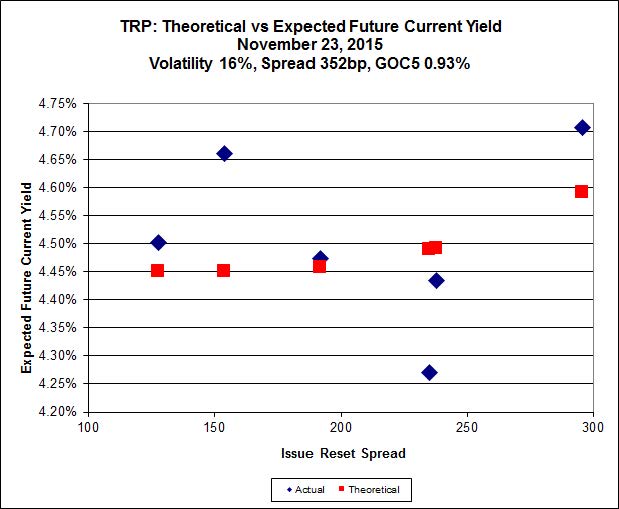

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.20 to be $0.93 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.62 cheap at its bid price of 13.25.

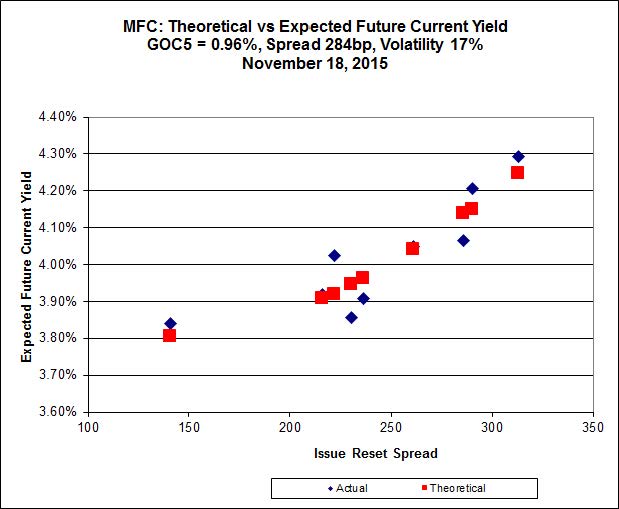

Click for Big

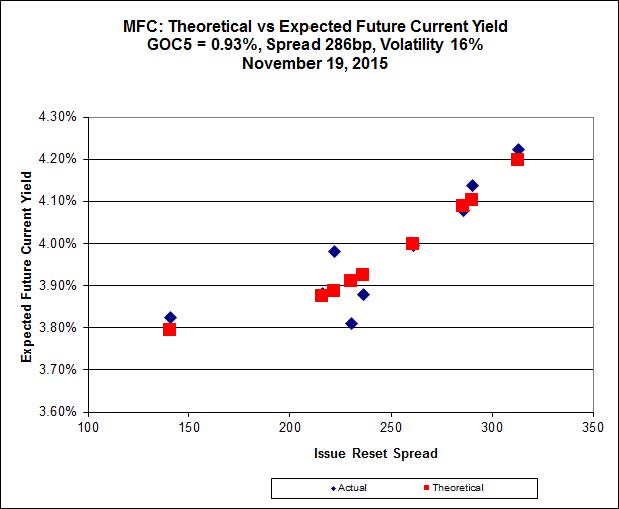

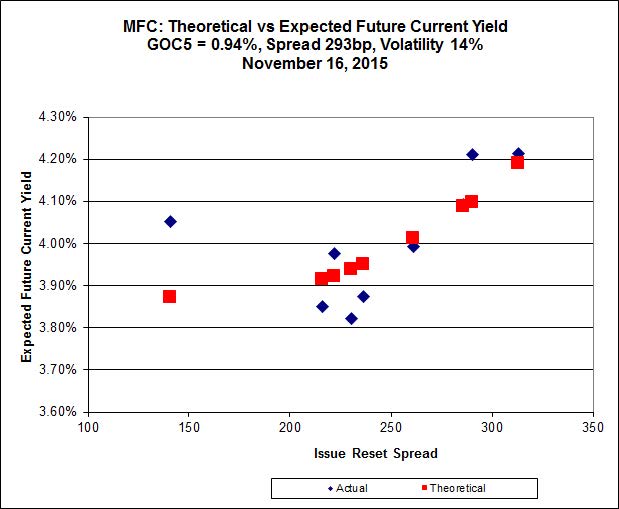

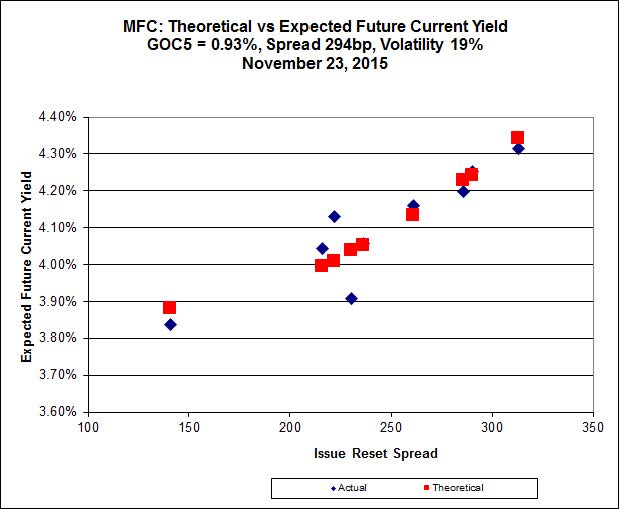

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 20.66 to be 0.66 rich, while MFC.PR.K resetting at +222bp on 2018-9-19, is bid at 19.07 to be 0.57 cheap.

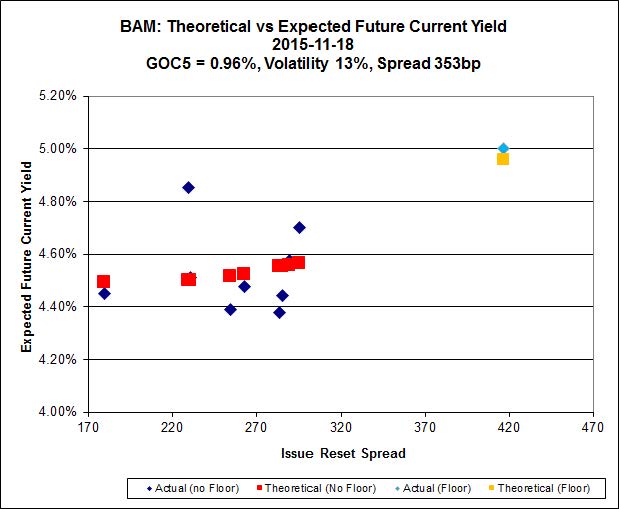

Click for Big

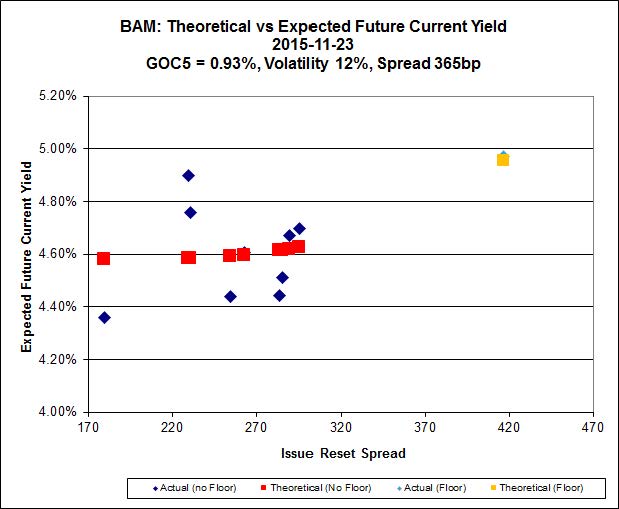

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.48 to be $1.14 cheap. BAM.PR.X, resetting at +180bp on 2017-6-30 is bid at 15.66 and appears to be $0.76 rich.

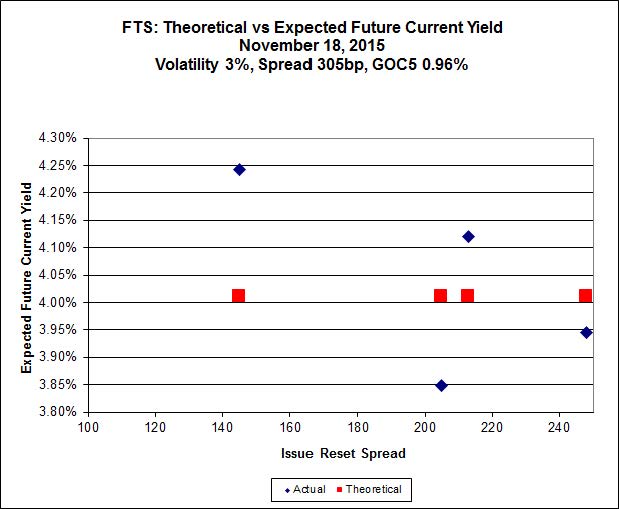

Click for Big

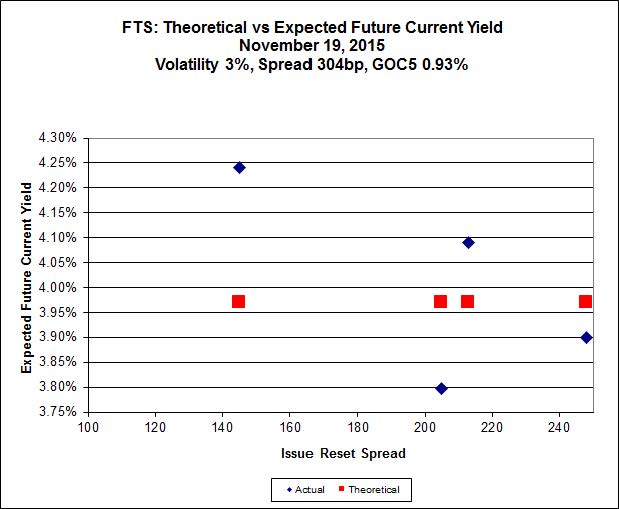

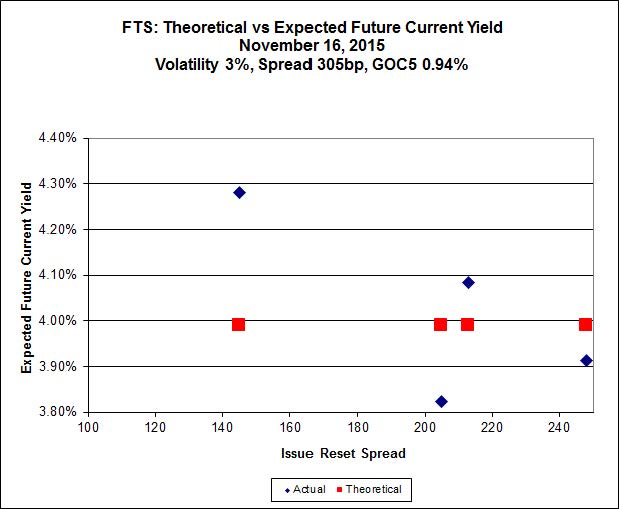

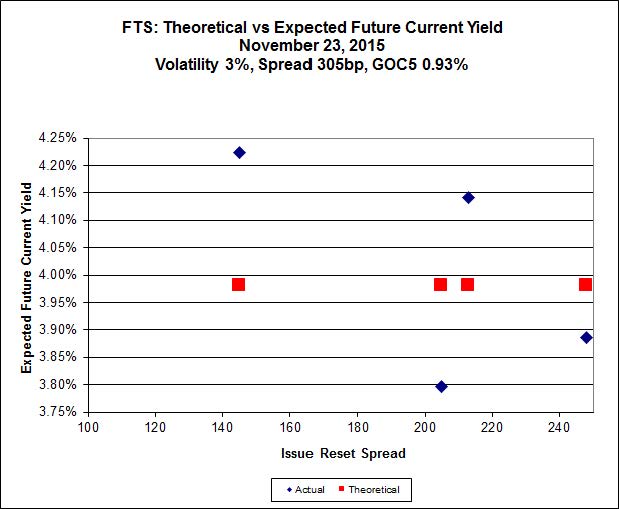

FTS.PR.K, with a spread of +205bp, and bid at 19.62, looks $0.90 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.09 and is $0.86 cheap.

Click for Big

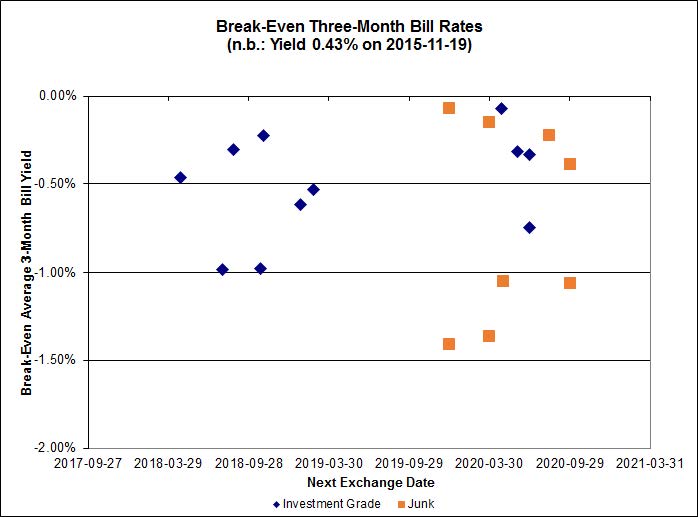

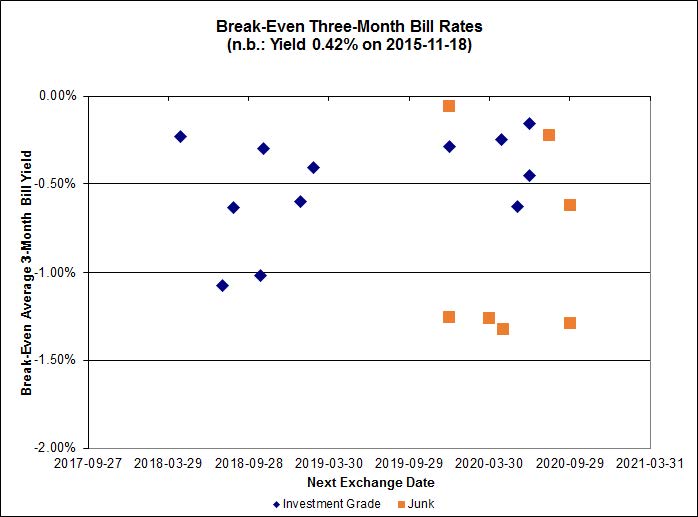

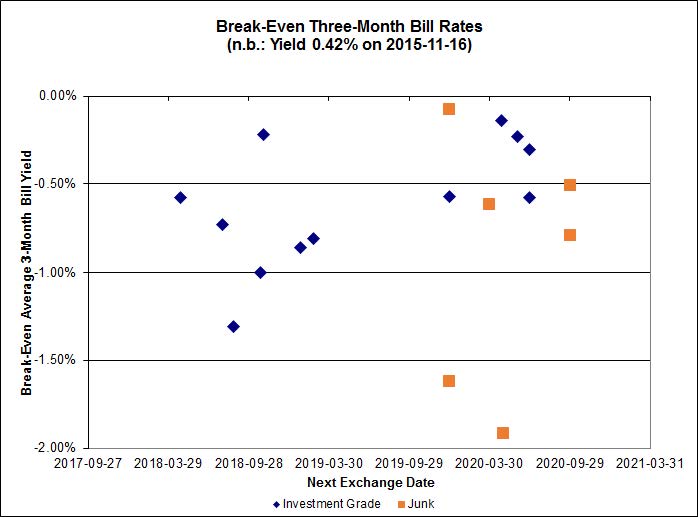

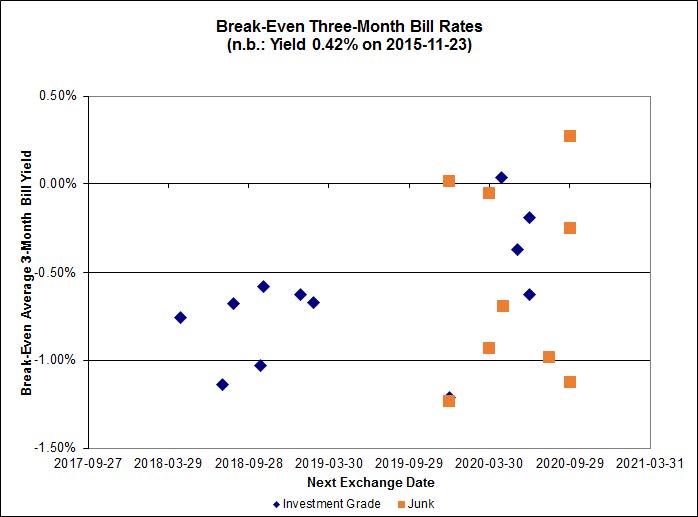

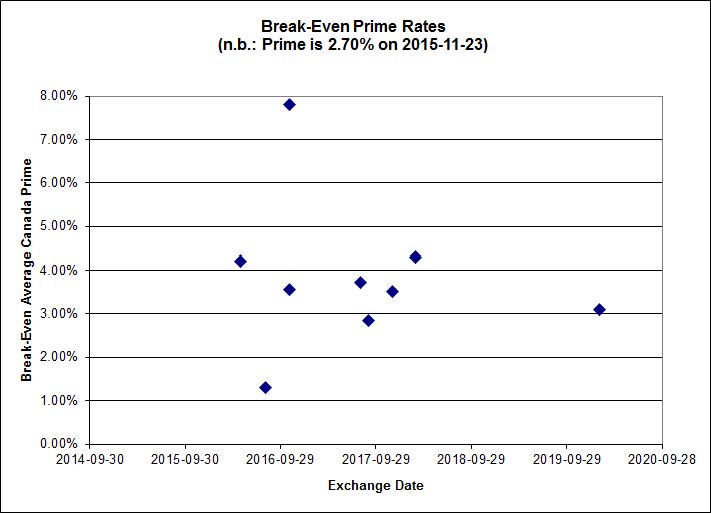

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.65%, with no outliers. There is one junk outlier below -1.50%.

Click for Big

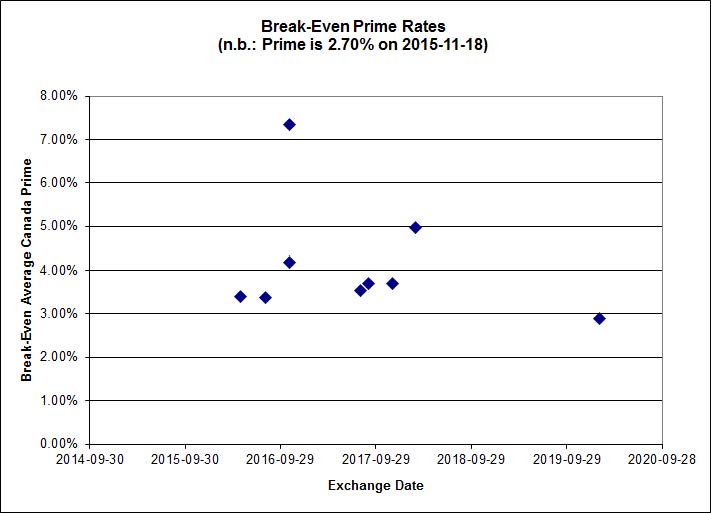

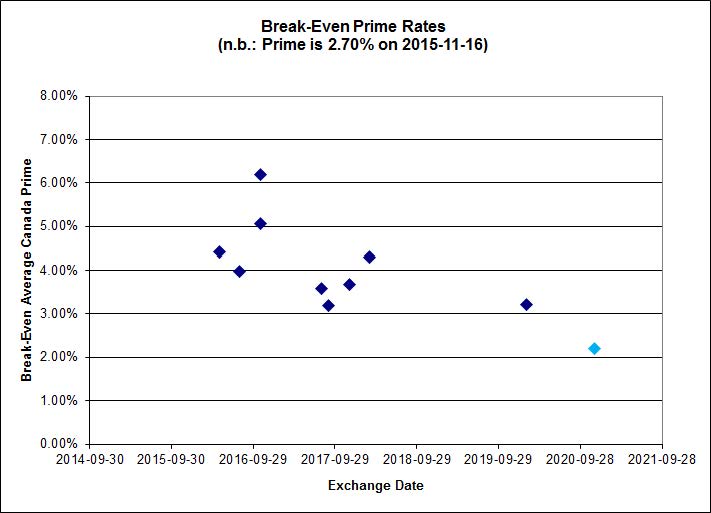

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.26 % | 5.12 % | 33,032 | 17.67 | 1 | 0.5657 % | 1,819.2 |

| FixedFloater | 6.29 % | 5.53 % | 27,768 | 16.87 | 1 | -2.8296 % | 3,103.9 |

| Floater | 4.39 % | 4.42 % | 80,827 | 16.50 | 3 | -4.6649 % | 1,798.8 |

| OpRet | 4.87 % | 3.98 % | 33,984 | 0.76 | 1 | -0.1191 % | 2,733.2 |

| SplitShare | 4.77 % | 5.74 % | 135,069 | 2.90 | 5 | -0.2870 % | 3,211.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.2870 % | 2,506.1 |

| Perpetual-Premium | 5.80 % | 2.14 % | 88,098 | 0.08 | 6 | 0.1190 % | 2,505.5 |

| Perpetual-Discount | 5.57 % | 5.65 % | 87,569 | 14.42 | 33 | -0.5001 % | 2,570.7 |

| FixedReset | 4.94 % | 4.58 % | 224,342 | 15.19 | 76 | -0.5355 % | 2,076.8 |

| Deemed-Retractible | 5.18 % | 5.27 % | 117,703 | 5.38 | 33 | -0.2428 % | 2,575.1 |

| FloatingReset | 2.61 % | 3.82 % | 60,134 | 5.75 | 10 | -0.8219 % | 2,179.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.F | FloatingReset | -8.27 % | Not even close to being real, since the issue traded 27,318 shares in a range of 14.90-48 before closing at 13.76-14.90. The VWAP was 15.03; the last trade of the regular session occurred at 3:20pm. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 13.76 Evaluated at bid price : 13.76 Bid-YTW : 4.30 % |

| BAM.PR.C | Floater | -5.18 % | Real enough, as the issue traded 5,027 shares in a range of 10.81-28 before closing at 10.81-90, 1×1. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 10.81 Evaluated at bid price : 10.81 Bid-YTW : 4.42 % |

| BAM.PR.K | Floater | -4.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 10.65 Evaluated at bid price : 10.65 Bid-YTW : 4.49 % |

| BAM.PR.B | Floater | -4.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 10.83 Evaluated at bid price : 10.83 Bid-YTW : 4.42 % |

| CM.PR.Q | FixedReset | -3.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.12 Evaluated at bid price : 21.12 Bid-YTW : 4.41 % |

| BAM.PR.G | FixedFloater | -2.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 25.00 Evaluated at bid price : 15.11 Bid-YTW : 5.53 % |

| BAM.PF.D | Perpetual-Discount | -2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 20.52 Evaluated at bid price : 20.52 Bid-YTW : 6.08 % |

| MFC.PR.L | FixedReset | -2.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.11 Bid-YTW : 6.95 % |

| BAM.PR.T | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 17.02 Evaluated at bid price : 17.02 Bid-YTW : 5.01 % |

| MFC.PR.M | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.27 Bid-YTW : 6.33 % |

| BIP.PR.A | FixedReset | -2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.44 % |

| MFC.PR.K | FixedReset | -2.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.07 Bid-YTW : 6.90 % |

| VNR.PR.A | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.85 % |

| CU.PR.F | Perpetual-Discount | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 20.42 Evaluated at bid price : 20.42 Bid-YTW : 5.54 % |

| HSE.PR.E | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.28 Evaluated at bid price : 21.56 Bid-YTW : 5.28 % |

| IFC.PR.A | FixedReset | -1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.54 Bid-YTW : 8.68 % |

| BMO.PR.W | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 4.39 % |

| GWO.PR.S | Deemed-Retractible | -1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 5.91 % |

| MFC.PR.J | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.27 Bid-YTW : 5.77 % |

| BMO.PR.T | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 4.37 % |

| TD.PF.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.11 Evaluated at bid price : 19.11 Bid-YTW : 4.36 % |

| TD.PF.B | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.33 % |

| BNS.PR.D | FloatingReset | -1.55 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.71 Bid-YTW : 5.47 % |

| BAM.PF.E | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 4.81 % |

| PWF.PR.S | Perpetual-Discount | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.48 Evaluated at bid price : 21.48 Bid-YTW : 5.65 % |

| TD.PF.A | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.35 % |

| RY.PR.M | FixedReset | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 4.33 % |

| HSE.PR.C | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.95 Evaluated at bid price : 19.95 Bid-YTW : 5.31 % |

| BAM.PF.C | Perpetual-Discount | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 6.02 % |

| RY.PR.J | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.04 Evaluated at bid price : 21.04 Bid-YTW : 4.36 % |

| MFC.PR.C | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.56 Bid-YTW : 7.16 % |

| IAG.PR.A | Deemed-Retractible | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.40 Bid-YTW : 6.88 % |

| MFC.PR.H | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.52 Bid-YTW : 4.93 % |

| GWO.PR.R | Deemed-Retractible | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.86 Bid-YTW : 6.81 % |

| MFC.PR.N | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.66 Bid-YTW : 6.00 % |

| TD.PF.E | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.81 Evaluated at bid price : 22.25 Bid-YTW : 4.25 % |

| CU.PR.E | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.74 Evaluated at bid price : 22.05 Bid-YTW : 5.57 % |

| CU.PR.G | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 5.50 % |

| RY.PR.W | Perpetual-Discount | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 22.59 Evaluated at bid price : 22.84 Bid-YTW : 5.38 % |

| RY.PR.H | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.15 Evaluated at bid price : 19.15 Bid-YTW : 4.37 % |

| HSE.PR.G | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 21.88 Evaluated at bid price : 22.32 Bid-YTW : 5.08 % |

| SLF.PR.I | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.62 Bid-YTW : 5.60 % |

| IFC.PR.C | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.16 Bid-YTW : 6.61 % |

| TRP.PR.A | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 15.93 Evaluated at bid price : 15.93 Bid-YTW : 4.69 % |

| TRP.PR.E | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.58 % |

| TRP.PR.D | FixedReset | 2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.65 % |

| HSE.PR.A | FixedReset | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-23 Maturity Price : 14.02 Evaluated at bid price : 14.02 Bid-YTW : 4.87 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.B | Deemed-Retractible | 163,645 | RBC crossed 50,000 at 24.95; Nesbitt crossed 40,000 at the same price; and Desjardins crossed blocks of 50,000 and 17,700 at the same price again. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.94 Bid-YTW : 4.77 % |

| BMO.PR.K | Deemed-Retractible | 142,912 | Scotia crossed blocks of 71,400 and 70,000, both at 25.65. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-12-25 Maturity Price : 25.25 Evaluated at bid price : 25.60 Bid-YTW : -10.56 % |

| BNS.PR.O | Deemed-Retractible | 83,300 | TD crossed blocks of 49,800 and 25,000, both at 25.63. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-12-23 Maturity Price : 25.50 Evaluated at bid price : 25.66 Bid-YTW : 2.06 % |

| CU.PR.I | FixedReset | 69,270 | Nesbitt crossed blocks of 15,300 and 15,000, both at 25.75; TD crossed 25,000 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-01 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 3.92 % |

| RY.PR.E | Deemed-Retractible | 64,200 | TD crossed 50,000 at 24.95 and 10,000 at 24.94. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.90 Bid-YTW : 4.60 % |

| RY.PR.I | FixedReset | 58,301 | Scotia crossed blocks of 26,300 and 25,000, both at 24.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.52 Bid-YTW : 3.58 % |

| There were 50 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.F | FloatingReset | Quote: 13.76 – 14.90 Spot Rate : 1.1400 Average : 0.7154 YTW SCENARIO |

| CM.PR.Q | FixedReset | Quote: 21.12 – 21.79 Spot Rate : 0.6700 Average : 0.4426 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 20.52 – 21.35 Spot Rate : 0.8300 Average : 0.6177 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 20.27 – 21.04 Spot Rate : 0.7700 Average : 0.5698 YTW SCENARIO |

| GWO.PR.I | Deemed-Retractible | Quote: 21.28 – 21.75 Spot Rate : 0.4700 Average : 0.3239 YTW SCENARIO |

| GWO.PR.S | Deemed-Retractible | Quote: 24.10 – 24.50 Spot Rate : 0.4000 Average : 0.2828 YTW SCENARIO |