DBRS has announced (on March 20) that it:

notes the impact of the announcement by the Federal Energy Regulatory Commission (FERC) that it will no longer allow master limited partnership (MLP) interstate natural gas and oil pipelines to recover an income tax allowance in cost of service (COS) rates on the following ratings of Enbridge Energy Partners, L.P. (EEP):

— Issuer Rating of BBB, Stable trend

— Senior Unsecured Notes rating of BBB, Stable trend

— Junior Subordinated Notes rating of BB (high), Stable trend

— Commercial Paper rating of R-2 (middle), Stable trendDBRS estimates that the potential financial impact of the FERC decision and U.S. Tax Reform noted below would likely reduce EEP’s financial risk profile (on a DBRS modified-consolidated basis) to the low end of the BBB range in the absence of corrective measures. However, DBRS’s current business risk assessment of EEP as well as Enbridge Inc.’s (ENB; rated BBB (high) with a Stable trend by DBRS) history of supporting EEP through various measures are both supportive of the current ratings.

As an MLP, EEP’s credit metrics would be negatively affected by the implementation of the FERC decision, as some of the rates applicable to its expansion projects are tolled annually on a COS basis via the Lakehead Facility Surcharge Mechanism (FSM). EEP has indicated that, should FERC’s new policy be announced with an assumed implementation date of March 31, 2018, the 2018 financial impact to EEP is expected to be an approximate $100 million reduction in revenues and a $60 million reduction to distributable cash flow (DCF), net of non-controlling interests. Consequently, EEP has adjusted its 2018 DCF guidance range to $650 million — $700 million and 2018 total distribution coverage to approximately 1.0 times (x) from approximately 1.15x.

DBRS notes that the current 2018 Guidance adjustments follow previous 2018 Guidance adjustments announced on February 15, 2018 (concurrently with the Q4 2017 results announcement). In that case, as a result of U.S. Tax Reform, EEP adjusted its 2018 DCF guidance range to $720 million – $770 million from $775 million – $825 million and 2018 total distribution coverage to approximately 1.15x from approximately 1.2x.

On a combined basis, the impact of these 2018 Guidance adjustments would be to reduce mid-point 2018 DCF guidance by approximately 15.6%, eliminate the approximate 20% cushion on 2018 total distribution coverage (or, stated differently, to increase EEP’s payout ratio to 100% from 80%) and, in the absence of corrective measures, significantly weaken EEP’s key credit metrics. This would eliminate a significant portion of the remaining cushion currently embedded in EEP’s ratings. Please see DBRS’s rating report on EEP dated September 29, 2017, for further information.

This commentary has been picked up by the Financial Post:

Credit ratings agency DBRS Ltd. is warning that one of Enbridge Inc. subsidiary’s revenues could tumble by $100 million this year and its credit ratings hurt by new policies in the U.S., which have led to a sector-wide stock selloff.

DBRS said in a note Tuesday that said a recent decision by the U.S. Federal Regulatory Commission could “significantly weaken” the key credit metrics of Enbridge Energy Partners L.P. (EEP), a subsidiary of Calgary-based Enbridge.

Last week, the FERC announced that master limited partnerships (MLPs) — a tax-friendly corporate structure popular with pipeline firms — would no longer be able to recover an income tax allowance in certain pipeline service contracts.

… which printed a Canadian Press story on last week’s damage to the common after the ruling was announced:

Shares in Canadian pipeline companies Enbridge Inc. and TransCanada Corp. failed to recover fully Friday [March 16] from a steep sell-off on Thursday [March 15] after the U.S. said it would eliminate a tax break for owners of certain interstate pipelines.

Both Calgary-based companies hold such pipelines in the United States through master limited partnerships or MLPs.

The decision by the U.S. Federal Energy Regulatory Commission to no longer allow MLPs to recover an income tax allowance from cost of service tariffs came in response to a 2016 court ruling that found its long-standing tax policy could result in double recovery of costs.

Enbridge shares fell by 4.2 per cent to $41.06 on Thursday but recovered to close at $41.28 on Friday, up 22 cents, after it issued a statement that says it is not expecting a “material change” to its financial guidance over the next three years because of the FERC ruling.

The Globe also printed the CP story, and published three different perspectives on ENB common following the drop:

Enbridge Inc. shares skidded 4.2 per cent Thursday, adding to the frustration of shareholders who have seen more than a quarter of the company’s market capitalization wiped out in just the past year.

Investors have been worried about Enbridge’s high debt load – which sits at around $60-billion after the $37-billion acquisition of Spectra Energy Corp. that closed last year. The stock has also been pressured by a move out of dividend-paying stocks in a rising interest rate environment.

…

The Globe and Mail earlier this month talked to three portfolio managers with different views of Enbridge, as well as with the company about investors’ concerns.

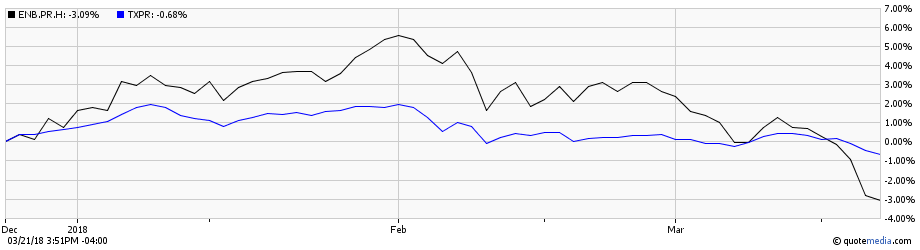

ENB.PR.H (to pick one of their issues at random) has significantly underperformed the TXPR index in the past while:

Click for Big

The fall in ENB preferreds generally has attracted comment on PrefBlog.

This is significant, because Enbridge’s issuance frenzy of about five years ago made them a very significant part of the market … they have about $7.25-billion (face value) of preferreds outstanding (including USD issues), call it about $5.8-billion market value, compared to a total estimated market capitalization of $76.1-billion. Their issues have a weight of just under 10% of the BMO-CM “50” Preferred Share Index (as of February, 2018) and just under 9% of TXPR (as of 2017-7-31).

Affected issues are (deep breath): ENB.PF.A, ENB.PF.C, ENB.PF.E, ENB.PF.G, ENB.PF.I, ENB.PF.K, ENB.PR.A, ENB.PR.B, ENB.PR.C, ENB.PR.D, ENB.PR.F, ENB.PR.H, ENB.PR.J, ENB.PR.N, ENB.PR.P, ENB.PR.T, ENB.PR.Y and the USD-denominated issues, ENB.PR.U, ENB.PR.V, ENB.PF.U and ENB.PF.V.