Bank of Montreal has announced:

it has closed its inaugural Basel III-compliant public offering of Non-Cumulative 5-year Rate Reset Class B Preferred Shares Series 27 (the “Preferred Shares Series 27”). The offering was underwritten on a bought deal basis by a syndicate led by BMO Capital Markets. Bank of Montreal issued 20 million Preferred Shares Series 27 at a price of $25 per share to raise gross proceeds of $500 million.

The Preferred Shares Series 27 were issued under a prospectus supplement dated April 16, 2014, to the Bank’s short form base shelf prospectus dated March 13, 2014. Such shares will commence trading on the Toronto Stock Exchange today under the ticker symbol BMO.PR.S.

BMO.PR.S is a FixedReset, 4.00%+233, NVCC-compliant issue announced April 14. It will be tracked by HIMIPref™ and is assigned to the FixedReset Sub-Index. DBRS has confirmed their Pfd-2(stable) preliminary rating on the issue. Note that this is one notch below the other BMO issues due to NVCC uncertainty.

The issue traded 1,557,213 shares today in a range of 25.31-43 before closing at 25.42-44, 89×30. Vital statistics are:

| BMO.PR.S | FixedReset | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-05-25 Maturity Price : 25.00 Evaluated at bid price : 25.42 Bid-YTW : 3.65 % |

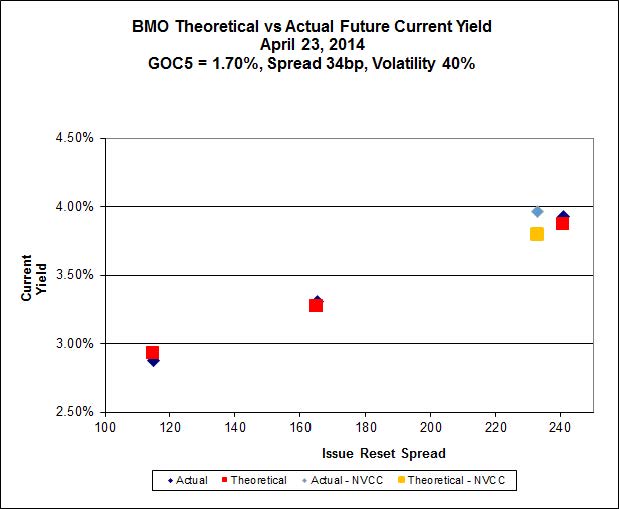

If we compare BMO.PR.S to its sort-of peers with volatility theory, we find:

Click for Big

So, we see that BMO.PR.S is still cheap to the theoretical curve, and that the theoretical curve is absurdly steep, which favours higher-spread issue such as BMO.PR.S. On the other hand, BMO.PR.S has over five years to go until its call date, well in excess of the 3-year figure I use for convenience, and that it’s NVCC compliant unlike the other plotted members, and that an assumption of directionality in price (and therefore a steep curve) is entirely rational for the non-NVCC issues. So take your choice.

[…] is a FixedReset, 4.00%+233, NVCC-compliant issue that commenced trading 2014-4-23 after being announced 2014-4-14. It is tracked by HIMIPref™ and is assigned to the […]

[…] is a FixedReset, 4.00%+233, NVCC-compliant issue that commenced trading 2014-4-23 after being announced 2014-4-14. The issue will reset At 3.852% effective May 25, 2019. I […]

[…] is a FixedReset, 4.00%+233, NVCC-compliant issue that commenced trading 2014-4-23 after being announced 2014-4-14. It is tracked by HIMIPref™ and is assigned to the […]