How ’bout that ruble, eh?

After the single worst day in Russia’s nine-month-old financial crisis, the fallout is spreading across global markets.

Pacific Investment Management Co. (PEBIX) is facing mounting losses on its Russian bond holdings; almost every bullish ruble option contract registered in the U.S. has been made worthless; and foreign-exchange brokers in New York and London told clients they’re no longer taking ruble trades. Sergey Shvetsov, a first deputy central bank governor, expressed astonishment at the scope of the collapse during a business conference in Moscow.

“We couldn’t imagine what’s happening in our worst nightmare even a year ago,” Shvetsov, who oversees financial markets at the central bank, said yesterday. He said the bank’s surprise interest-rate increase in the middle of the night, a 6.5 percentage-point move that failed to stem the run on the ruble yesterday, was a choice between a “very bad” option and and a “very, very bad” option.

The ruble sank beyond 80 per dollar, a record low, as panic swept across Moscow’s financial markets before it rebounded after Economy Minister Alexei Ulyukayev denied speculation the government would impose restrictions to stop Russians from converting cash into dollars. The currency ended the day at 67.9 per dollar, down 5.4 percent on the day, while bonds and stocks also tumbled, sending the RTS equity gauge down the most since 2008.

Russians have long experience of state-run media:

Russians like Vladimir Rudenkov from Voronezh, a city about 500 kilometers (311 miles) from Moscow, were ignoring the government-media assurances and taking action. Rudenkov transfered a portion of his savings into dollars this morning and said he regretted that he didn’t transfer it all.

“The situation is catastrophic,” said Rudenkov, a 35-year-old manager. “I don’t believe that the ruble collapse is happening only due to the falling oil prices. The government is the one to blame as it didn’t defend the national currency.”

The BoC has published a paper by George J. Jiang, Ingrid Lo and Giorgio Valente titled High-Frequency Trading around Macroeconomic News Announcements: Evidence from the U.S. Treasury Market:

This paper investigates high-frequency (HF) market and limit orders in the U.S. Treasury market around major macroeconomic news announcements. BrokerTec introduced i-Cross at the end of 2007 and we use this exogenous event as an instrument to analyze the impact of HF activities on liquidity and price efficiency. Our results show that HF activities have a negative effect on liquidity around economic announcements: they widen spreads during the pre-announcement period and lower depth on the order book during the post-announcement period. The negative impact on liquidity mainly derives from HF trades. Nonetheless, HF trades improve price efficiency during both the preannouncement and post-announcement periods.

Intact Financial Corporation, proud issuer of IFC.PR.A and IFC.PR.C, has been confirmed at Pfd-2(low) by DBRS:

DBRS Limited (DBRS) has today confirmed Intact Financial Corporation’s (Intact or the Company) Issuer Rating at A (low), Senior Unsecured Debt at A (low) and Non-Cumulative Preferred Shares at Pfd-2 (low). The trends are Stable.

The Company’s operating subsidiaries are among the strongest performers in the Canadian property and casualty insurance industry, achieving underwriting profits and obtaining above-industry return on capital results. The Company’s overall underwriting performance hinges on tightening benefits, reducing exposures, scale and analysis, which allows it to identify and price risks by mining its extensive database. Scale also enhances the ability of the Company to keep claims costs lower than those of its peer group and to more efficiently service its multi-channel distribution networks. Recent efforts to increase pricing in firmer commercial markets, to tighten benefits and to reduce earthquake exposures should improve the Company’s performance after three years of elevated catastrophic claims. An efficient capital structure keeps the Company’s overall financial leverage within bounds, and it has seen improving financial leverage ratios since 2011. There is a possibility of acquisition activity increasing the financial leverage if financed with debt.

DBRS calculates Intact’s annualized return on equity for the first nine months of 2014 to be 16.2%, a positive result benefiting from lower catastrophic claims so far this year compared with 2013 and generally improved underwriting results with higher premiums and reduced benefit obligations. The important Ontario auto insurance market, which comprises the largest segment of Intact’s business, is challenging with the provincial government’s desire to lower auto insurance premiums. To achieve the desired premium reductions, the industry is asking for a reduction in benefit costs and greater ability to discourage fraud.

It was (yet another) poor day for the Canadian preferred share market, with PerpetualDiscounts down 9bp, FixedResets losing 22bp and DeemedRetractibles off 8bp. There is (yet another) lengthy list of Performance Highlights, dominated (yet again) by losing FixedResets with (yet more) heavy representation from the credit-dubious Enbridge. Volume was above average, enlivened by the two new issues, CM.PR.P and TD.PF.C.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 19.45, is $1.84 cheap, but it has already reset (at +192). TRP.PR.D, bid at 25.00 and resetting at +238bp on 2019-4-30 is $0.66 rich and TRP.PR.E, bid at 25.04 and resetting at +235bp on 2019-10-30, is $0.90 rich. The TRP issues seem to be rationalizing, but there continues to be pressure on TRP.PR.A.

Now, this is really interesting. TRP.PR.A will pay 3.266%, which is to say $0.8165, until its next reset date 2019-12-31. TRP.PR.E will continue to pay its initial dividend of $1.0625 until it resets 2019-10-30 at +235. See that? Two month’s difference in reset. I think we can disregard forecasts of changes in GOC-5 yield that get that precise. That is to say, over the next five years, TRP.PR.E will pay a total of about $1.25 more than TRP.PR.A. Then it will reset at 46bp more, which is to say $0.115 p.a., forever.

And yet the difference in price is $5.59! That seems to me to be a lot to pay for a short term payment of $1.25, leaving $4.34, to earn $0.115, or 2.65%. But some people, it would seem, find this quite reasonable. It will be noted as well that TRP.PR.A is exposed to possible capital gains if the Market Reset Spread narrows; so it could gain up to $5.55 in price while TRP.PR.E got nothing.

Click for Big

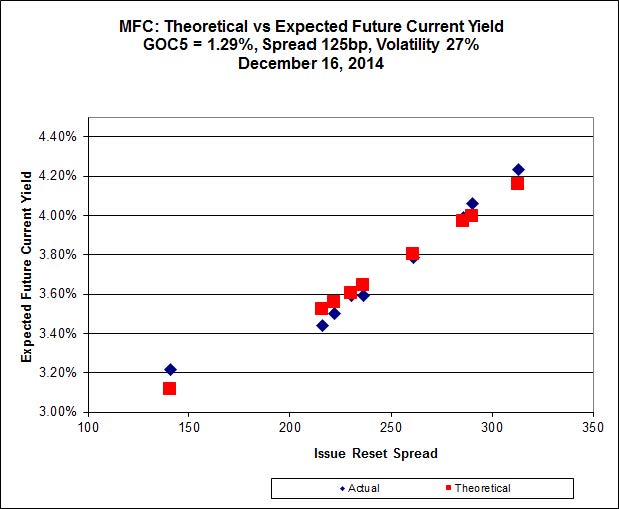

It looks like MFC.PR.F, resetting at 141bp on 2016-06-19 is in another world and distorting results again.

Click for Big

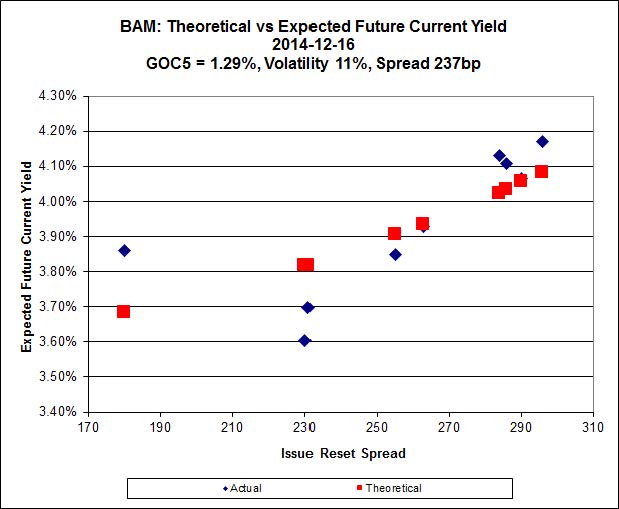

There continues to be extraordinary cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, is bid at 20.01 and appears to be $0.96 cheap, while BAM.PR.R, resetting at +230bp 2016-6-30 is bid at 24.90 and appears to be $1.39 rich.

Click for Big

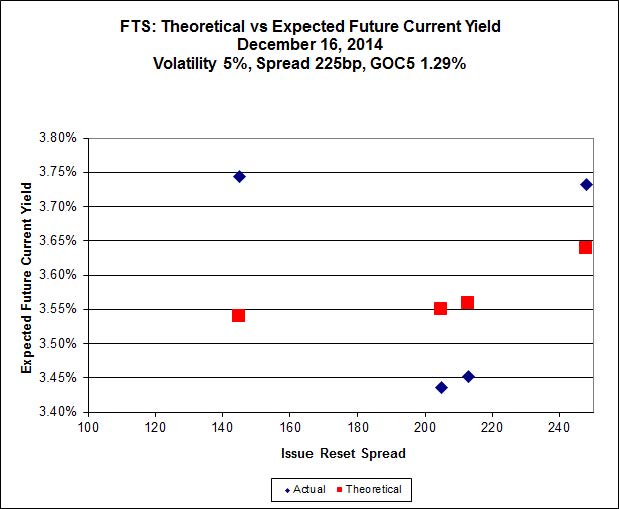

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.30, looks $1.05 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 24.30, looks $0.77 expensive and resets 2019-3-1

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1438 % | 2,505.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1438 % | 3,966.9 |

| Floater | 3.03 % | 3.12 % | 60,256 | 19.44 | 4 | -0.1438 % | 2,663.7 |

| OpRet | 4.41 % | -3.71 % | 27,354 | 0.08 | 2 | -0.0196 % | 2,748.8 |

| SplitShare | 4.31 % | 4.02 % | 43,390 | 3.71 | 5 | -0.0294 % | 3,172.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0196 % | 2,513.5 |

| Perpetual-Premium | 5.44 % | 1.18 % | 74,181 | 0.09 | 20 | -0.0020 % | 2,473.8 |

| Perpetual-Discount | 5.22 % | 5.14 % | 111,245 | 15.18 | 15 | -0.0864 % | 2,634.1 |

| FixedReset | 4.28 % | 3.60 % | 233,669 | 16.45 | 77 | -0.2249 % | 2,511.5 |

| Deemed-Retractible | 5.00 % | 1.37 % | 98,170 | 0.29 | 40 | -0.0837 % | 2,598.5 |

| FloatingReset | 2.56 % | 2.10 % | 64,191 | 3.51 | 5 | -0.0868 % | 2,531.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.T | FixedReset | -4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.11 Evaluated at bid price : 24.64 Bid-YTW : 3.77 % |

| IFC.PR.A | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.61 Bid-YTW : 4.61 % |

| ENB.PR.B | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 22.21 Evaluated at bid price : 22.56 Bid-YTW : 4.16 % |

| BNS.PR.P | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.62 Bid-YTW : 2.71 % |

| MFC.PR.F | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 5.01 % |

| GWO.PR.N | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 5.29 % |

| ENB.PR.N | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 22.23 Evaluated at bid price : 22.80 Bid-YTW : 4.34 % |

| BAM.PF.F | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.26 Evaluated at bid price : 25.25 Bid-YTW : 4.08 % |

| ENB.PR.F | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 22.20 Evaluated at bid price : 22.70 Bid-YTW : 4.24 % |

| TRP.PR.A | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 4.17 % |

| BAM.PF.A | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.76 Bid-YTW : 3.60 % |

| HSE.PR.A | FixedReset | 2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.01 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.C | FixedReset | 749,016 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.11 Evaluated at bid price : 24.87 Bid-YTW : 3.51 % |

| CM.PR.P | FixedReset | 692,550 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.07 Evaluated at bid price : 24.75 Bid-YTW : 3.53 % |

| FTS.PR.M | FixedReset | 269,800 | Desjardins crossed blocks of 197,100 and 60,000 at 25.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.25 Evaluated at bid price : 25.25 Bid-YTW : 3.71 % |

| TRP.PR.E | FixedReset | 116,806 | RBC crossed 114,600 at 25.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 23.18 Evaluated at bid price : 25.04 Bid-YTW : 3.70 % |

| CM.PR.E | Perpetual-Premium | 66,242 | Called for redemption January 31. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-15 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : -0.24 % |

| ENB.PR.A | Perpetual-Premium | 56,250 | RBC crossed 42,700 at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-16 Maturity Price : 24.68 Evaluated at bid price : 24.99 Bid-YTW : 5.54 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.T | FixedReset | Quote: 24.64 – 25.44 Spot Rate : 0.8000 Average : 0.5662 YTW SCENARIO |

| ENB.PR.A | Perpetual-Premium | Quote: 24.99 – 25.63 Spot Rate : 0.6400 Average : 0.4751 YTW SCENARIO |

| NEW.PR.D | SplitShare | Quote: 32.12 – 33.12 Spot Rate : 1.0000 Average : 0.8457 YTW SCENARIO |

| SLF.PR.A | Deemed-Retractible | Quote: 23.91 – 24.35 Spot Rate : 0.4400 Average : 0.2925 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 19.25 – 20.00 Spot Rate : 0.7500 Average : 0.6105 YTW SCENARIO |

| FTS.PR.K | FixedReset | Quote: 24.30 – 24.95 Spot Rate : 0.6500 Average : 0.5176 YTW SCENARIO |