On December 19 my attention was drawn to a parallel between the Suez Crisis in 1956 and the current Ukraine Crisis. The Chinese provide a counter-parallel, assuming that’s a word:

China is stepping up its role as the lender of last resort to some of the world’s most financially strapped countries.

Chinese officials signaled on the weekend they are willing to expand a $24 billion currency swap program to help Russia weather the worst economic crisis since the 1998 default. China has provided $2.3 billion in funds to Argentina since October as part of a currency swap, and last month it lent $4 billion to Venezuela, whose reserves cover just two years of debt payments.

By lending to nations shut out of overseas capital markets, Chinese President Xi Jinping is bolstering the country’s influence in the global economy and cutting into the International Monetary Fund’s status as the go-to financier for governments in financial distress. While the IMF tends to demand reforms aimed at stabilizing a country’s economy in exchange for loans, analysts speculate that China’s terms are more focused on securing its interests in the resource-rich countries.

Today’s PrefBlog Movie Of The Week is:

Ukraine opened a criminal probe after several gold bars at the central bank’s storage in the southern city of Odessa turned to be painted lead.

“The management of the central bank’s branch in Odessa asked us to investigate fraud by their employee,” Volodymyr Shablienko, head of the Odessa police’s press office, said by phone today. “We are conducting a forensic audit now.”

A central bank employee passed lead bars covered with golden paint to the storage unit, registering them as gold, the Vesti newspaper reported today, citing an unidentified person with knowledge of the matter in Odessa’s police department.

Speaking of Russian, how about them banks, eh?:

After arresting a decline in the ruble, Russia is now trying to avert a banking crisis.

Lawmakers rushed legislation through the lower house of parliament today allowing the Deposit Insurance Agency to buy stakes in banks before they face bankruptcy proceedings to keep the system stable. While the ruble strengthened for a third day as the government told state-run exporters to sell foreign currency, it’s still down 30 percent in three months. Standard & Poor’s said today it may cut Russia’s credit rating to junk in part because of concern about the banking system.

…

The central bank put National Bank Trust, the country’s 15th-biggest based on retail deposits, under the control of the Deposit Insurance Agency yesterday. An investor will soon be selected to carry out the 30 billion-ruble ($550 million) rescue, the Bank of Russia said.Trust, once part of exiled former oil tycoon Mikhail Khodorkovsky’s business empire, had a capital hole of tens of billions of rubles and lost more than 3 billion rubles in retail deposits last week, central bank Deputy Governor Mikhail Sukhov said yesterday. Bank of Russia’s press service confirmed his comments, earlier reported by the Interfax newswire.

And the Dow Jones Industrial Average is also pretty interesting:

The Dow Jones Industrial Average rose 5.6 percent over the past five days for the biggest rally since 2011, climbing to 18,024.17 yesterday, as the central bank pledged patience in raising interest rates while data showed the economy roared the most in the third quarter since 2003. A measure of expected volatility in the Dow has fallen the most in three years during the recent rally.

…

The Dow closed at a six-month low on Oct. 16 before rallying more than 1,882 points, or 12 percent, to top 18,000. The Chicago Board Options Exchange Dow Jones Industrial Average (INDU) Volatility Index, a measure of demand for options on the blue-chip stocks gauge, has bounced back after two jumps of more than 70 percent since September.The industrial average has risen about 175 percent during the bull market that began in March 2009, propelled by better-than-estimated corporate results and three rounds of Fed bond purchases. The Standard & Poor’s 500 Index has more than tripled in that time. It rose 0.2 percent yesterday to finish at an all-time high.

The press might get interested in credit ratings again; e.g., Bloomberg:

One large company and four smaller firms didn’t follow their own methodologies in determining ratings, the SEC said in its report on Nationally Recognized Statistical Rating Organizations, or NRSROs.

After reviewing e-mails of one of the larger raters, the regulator determined that business and market-share conditions influenced the substance of its criteria. Employees on the business side of this rater worked in a concerted effort to change the criteria to appease an industry trade group, the SEC said.

OK, so let’s look at the relevant section in the actual staff report, titled 2014 SUMMARY REPORT OF COMMISSION STAFF’S EXAMINATIONS OF EACH NATIONALLY RECOGNIZED STATISTICAL RATING ORGANIZATION:

The Staff’s review of one larger NRSRO’s revisions to one of its rating criteria, including extensive review of its emails, suggests that this NRSRO’s business and market-share concerns influenced the substance of the criteria. Some of this NRSRO’s business personnel engaged in a concerted effort to address concerns raised by a trade association about this NRSRO’s contemplated revisions to the criteria report, and this criteria report was changed in a manner that addressed the business personnel’s concerns and was advantageous to the trade group. Also, documentation to support this change was lacking. The Staff recommended that this NRSRO enforce its policies and procedures and internal controls to separate the analytical process from commercial influence and ensure that the analytic justification of its criteria is adequately recorded and maintained. The Staff also recommended that this NRSRO’s Board retain an independent auditor, to be approved by OCR, to conduct a review of the development of the criteria and provide a written report summarizing the review to this NRSRO’s Board and compliance group as well as OCR.

It’s very difficult to see anything to be upset about here. First, the external body being dealt with was a trade group, not an individual company, which alleviates at least some of the automatic concerns right away (to a degree that can only be determined once we know how the trade group functions, for starters). Second, SEC Staff are shocked and horrified that the changes sought by the trade group are advantageous to the trade group. Well, yeah. Does anybody really expect anything else? Third, the criteria were changed in a manner that addressed the business personnel’s concerns … OK. Were the business personnel’s concerns grounded or ungrounded? Fourth, the documentation to support this change was lacking. Well, I can let you guys in on a little secret about regulatory paperwork: it’s always lacking. God and all his angels could not maintain records that would survive a determined fault-finding mission by regulators; not while doing any work of substance, anyway.

So the summary sounds bad, and the raw material hints that maybe something could be bad, but there’s nothing of real substance in this finding. However, look for it to be quoted as unequivocal damnation in debates to come.

Fortis Inc., proud issuer of FTS.PR.E, FTS.PR.F, FTS.PR.G, FTS.PR.H, FTS.PR.J, FTS.PR.K and FTS.PR.M, was confirmed at Pfd-2(low) by DBRS and removed from ‘Review-Developing’:

DBRS Limited (DBRS) has today removed the A (low) Issuer Rating, A (low) Unsecured Debentures and Pfd-2 (low) Preferred Shares ratings of Fortis Inc. (Fortis, the Parent or the Company) from Under Review with Developing Implications and has confirmed the ratings as listed above with Stable trends. This action follows the completion of the Company’s acquisition of UNS Energy Corporation (UNS) (the Acquisition) and the conversion of $1.8 billion of convertible debentures into common equity in late October 2014.

…

In DBRS’s view, the overall business risk profile of Fortis’ investment portfolio should remain in the A (low) range following the completion of the Acquisition.Fortis’ financing of the USD 2.5 billion Acquisition was consistent with DBRS’s expectation. Fortis issued $1.8 billion in convertible debentures, approximately $600 million in preferred shares and the remaining portion in debt. Most of the convertible debentures were converted into common equity in late October 2014. As a result, the financial risk profile on a non-consolidated basis remains consistent with DBRS’s expectation, with all pro forma non-consolidated credit ratios improving from 2013. Fortis’ non-consolidated debt in the capital structure would remain within DBRS’s 20% guideline for holding company notching while all other key credit metrics would solidly remain within the current rating range.

FTS has been on Review-Developing for over a year.

The Canadian preferred share market was on wheels today, with PerpetualDiscounts up 33bp, FixedResets winning 47bp and DeemedRetractibles gaining 18bp. The Performance Highlights table is suitably enormous, with only one loser; led on the upside by the low-reset insurance issues that had the stuffing kicked out of them in the first week of the month. Volume was above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

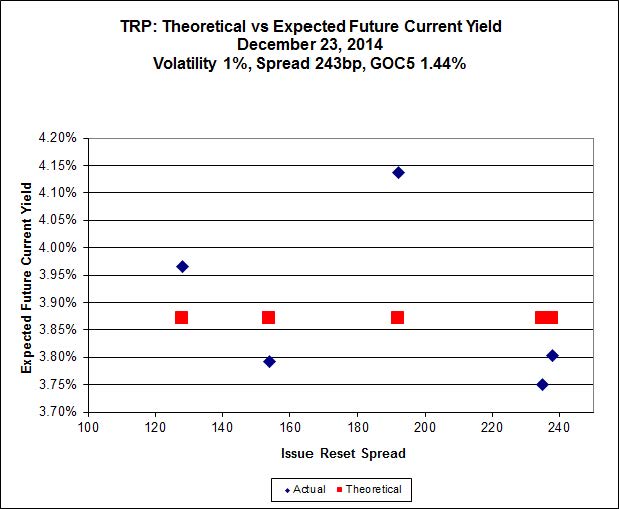

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 20.30, is $1.41 cheap, but it has already reset (at +192). TRP.PR.D, bid at 25.11 and resetting at +238bp on 2019-4-30 is $0.43 rich and TRP.PR.E, bid at 25.27 and resetting at +235bp on 2019-10-30, is $0.79 rich.

This particular calculation is fascinating because it is apparent that – disregarding the TRP.PR.A outlier – the slope of the line used to calculate implied volatility is negative. I can’t remember seeing one of those since the Credit Crunch!

Click for Big

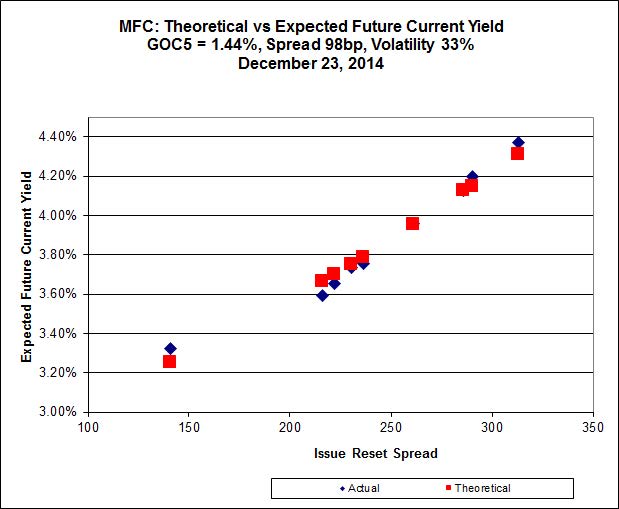

The impressive performance of MFC.PR.F brought it back to consistency with the curve defined by the higher reset issues today, but the Implied Volatility continues to be a conundrum. It is far too high if we consider that NVCC rules will never apply to these issues; it is far too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Click for Big

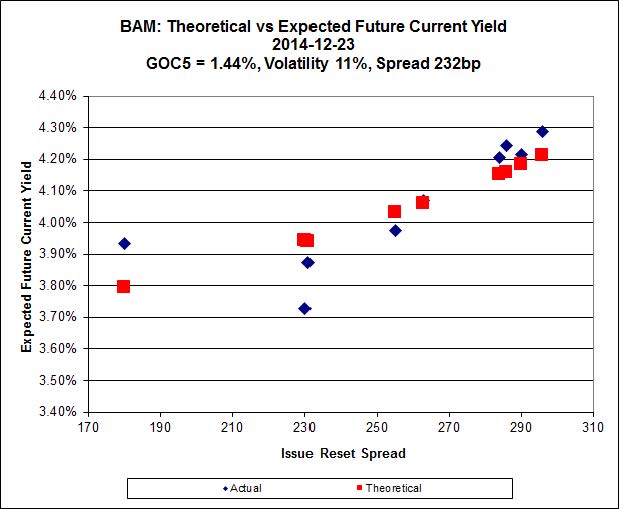

There continues to be cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 20.60 after superb performance today and appears to be $0.76 cheap, while BAM.PR.R, resetting at +230bp 2016-6-30 is bid at 25.08 and appears to be $1.36 rich.

Click for Big

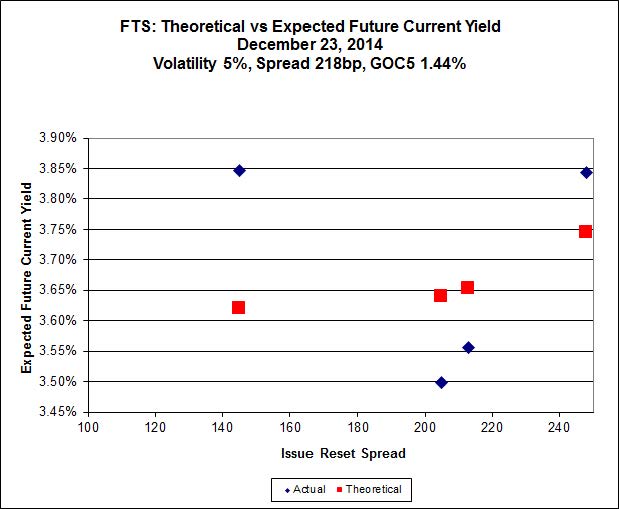

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.78, looks $1.18 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 24.94, looks $0.96 expensive and resets 2019-3-1

Click for Big

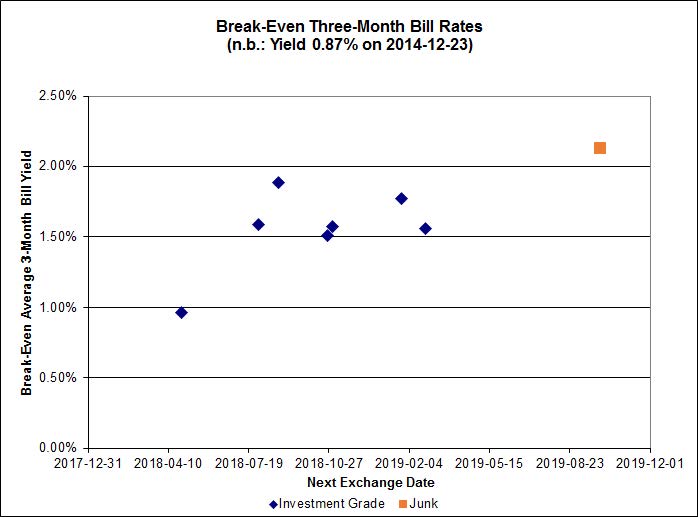

The average break-even rate has declined from 1.80%-2.00% at the time recent conversion decisions were made to a current cluster of (mostly) 1.55%-1.60%. This decline means that the estimated profit on TRP.PR.A conversion has declined from $0.48 to a mere $0.21 (at the lower end of the range, 1.55%).

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.5690 % | 2,521.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.5690 % | 3,992.6 |

| Floater | 3.01 % | 3.11 % | 66,751 | 19.44 | 4 | 2.5690 % | 2,680.9 |

| OpRet | 4.41 % | -3.08 % | 25,222 | 0.08 | 2 | 0.0588 % | 2,750.4 |

| SplitShare | 4.28 % | 4.08 % | 37,327 | 3.69 | 5 | 0.1490 % | 3,196.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0588 % | 2,515.0 |

| Perpetual-Premium | 5.45 % | -0.21 % | 71,880 | 0.08 | 20 | 0.1291 % | 2,479.8 |

| Perpetual-Discount | 5.20 % | 5.08 % | 110,410 | 15.31 | 15 | 0.3281 % | 2,648.8 |

| FixedReset | 4.24 % | 3.63 % | 247,985 | 16.45 | 77 | 0.4734 % | 2,529.7 |

| Deemed-Retractible | 4.97 % | 1.04 % | 96,558 | 0.27 | 40 | 0.1766 % | 2,616.6 |

| FloatingReset | 2.57 % | 2.11 % | 63,812 | 3.50 | 5 | 0.0079 % | 2,536.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| FTS.PR.J | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.76 Evaluated at bid price : 24.15 Bid-YTW : 4.94 % |

| BAM.PR.T | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.19 Evaluated at bid price : 24.20 Bid-YTW : 3.84 % |

| MFC.PR.B | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.04 Bid-YTW : 5.18 % |

| BAM.PF.B | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.22 Evaluated at bid price : 25.00 Bid-YTW : 3.93 % |

| BNS.PR.P | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-04-25 Maturity Price : 25.00 Evaluated at bid price : 25.91 Bid-YTW : 2.37 % |

| CU.PR.C | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-01 Maturity Price : 25.00 Evaluated at bid price : 25.80 Bid-YTW : 2.75 % |

| MFC.PR.C | Deemed-Retractible | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.45 Bid-YTW : 5.34 % |

| TRP.PR.A | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.07 % |

| FTS.PR.F | Perpetual-Discount | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 24.53 Evaluated at bid price : 24.80 Bid-YTW : 4.97 % |

| PWF.PR.P | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 21.27 Evaluated at bid price : 21.27 Bid-YTW : 3.63 % |

| BAM.PR.Z | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.65 Bid-YTW : 3.86 % |

| IAG.PR.A | Deemed-Retractible | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.95 Bid-YTW : 5.15 % |

| CU.PR.E | Perpetual-Discount | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.87 Evaluated at bid price : 24.27 Bid-YTW : 5.08 % |

| BAM.PR.C | Floater | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 16.74 Evaluated at bid price : 16.74 Bid-YTW : 3.13 % |

| GWO.PR.H | Deemed-Retractible | 1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.68 Bid-YTW : 5.03 % |

| BAM.PR.K | Floater | 2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 16.83 Evaluated at bid price : 16.83 Bid-YTW : 3.11 % |

| TRP.PR.C | FixedReset | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 3.86 % |

| BAM.PR.X | FixedReset | 2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.08 % |

| PWF.PR.A | Floater | 2.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 2.71 % |

| BAM.PR.B | Floater | 3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 3.12 % |

| SLF.PR.G | FixedReset | 3.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 4.43 % |

| MFC.PR.F | FixedReset | 4.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.45 Bid-YTW : 4.82 % |

| GWO.PR.N | FixedReset | 5.47 % | A real move. All trades after 3:18pm were higher than the “last” 20.83 bid; and these amounted to 3300 shares. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.83 Bid-YTW : 4.89 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.E | Perpetual-Premium | 192,259 | Called for redemption effective January 31 YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-22 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : -0.03 % |

| TD.PF.C | FixedReset | 110,049 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.10 Evaluated at bid price : 24.85 Bid-YTW : 3.56 % |

| CM.PR.P | FixedReset | 92,894 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.11 Evaluated at bid price : 24.86 Bid-YTW : 3.55 % |

| BMO.PR.W | FixedReset | 83,585 | RBC crossed 64,800 at 25.07. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.22 Evaluated at bid price : 25.15 Bid-YTW : 3.50 % |

| RY.PR.H | FixedReset | 72,465 | RBC crossed 62,000 at 25.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.32 Evaluated at bid price : 25.41 Bid-YTW : 3.50 % |

| RY.PR.Z | FixedReset | 54,366 | RBC crossed 50,000 at 25.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-23 Maturity Price : 23.38 Evaluated at bid price : 25.55 Bid-YTW : 3.46 % |

| There were 37 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ENB.PR.Y | FixedReset | Quote: 21.96 – 22.49 Spot Rate : 0.5300 Average : 0.3295 YTW SCENARIO |

| ELF.PR.H | Perpetual-Premium | Quote: 25.44 – 26.00 Spot Rate : 0.5600 Average : 0.3923 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 24.28 – 24.75 Spot Rate : 0.4700 Average : 0.3026 YTW SCENARIO |

| GWO.PR.L | Deemed-Retractible | Quote: 25.80 – 26.20 Spot Rate : 0.4000 Average : 0.2399 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 24.15 – 24.75 Spot Rate : 0.6000 Average : 0.4517 YTW SCENARIO |

| NEW.PR.D | SplitShare | Quote: 32.41 – 33.41 Spot Rate : 1.0000 Average : 0.8572 YTW SCENARIO |

Are YTW calculations assuming a certain commission?

YTW SCENARIO for CM.PR.E

Maturity Type : Call

Maturity Date : 2015-01-22

Maturity Price : 25.00

Evaluated at bid price : 24.97

Bid-YTW : -0.03 %

3 cents is a small but still positive profit, how come YTW is negative?

This is a bit peculiar; you must appreciate that the system does not “know” that it actually has been called at this point but is merely applying it usual algorithms.

The Pseudo-Portfolio Report shows the following possibilities for a call:

Evaluated at bid price : 24.9700

Call 2015-01-22 YTM: -0.03 % [Restricted: -0.00 %] (Prob: 17.04 %)

Call 2015-02-21 YTM: 2.80 % [Restricted: 0.46 %] (Prob: 5.64 %)

Call 2015-04-22 YTM: 4.21 % [Restricted: 1.38 %] (Prob: 5.04 %)

Call 2015-10-19 YTM: 5.09 % [Restricted: 4.18 %] (Prob: 5.41 %)

Call 2017-12-07 YTM: 5.47 % [Restricted: 5.47 %] (Prob: 5.05 %)

Limit Maturity 2044-12-23 YTM: 5.59 % [Restricted: 5.59 %] (Prob:61.82%)

Yield to Worst : -0.0316 %

And the cash flow report for the YTW scenario provides the following schedule of cash flows for the instrument:

******************

A4203425 0139

2015-01-22 FINAL DIVIDEND -0.03 1.000026 -0.03

2015-01-22 MATURITY 25.00 1.000026 25.00

Total Cash Flows 24.9693

Total Present Value 24.9700

Discounting Rate -0.0316 % (Annual rate compounded semi-annually)

**************

Yes, that’s right the system is working this out with a NEGATIVE final dividend: -$0.0307 to be precise.

This is due to the dividend schedule:

*****************

2014-03-26 2014-03-28 2014-04-30 0.350000

2014-06-25 2014-06-27 2014-07-30 0.350000

2014-09-25 2014-09-29 2014-10-30 0.350000

2014-12-23 2014-12-29 2015-01-30 0.350000

************

So what is happening is:

– the first calculation performed is 30 days hence.

– the instrument is callable at $25.00, so that’s added to the cash flow schedule

– when calculating the dividend that will be due on a call Jan 22, the system calculates that 84 days will have elapsed since the pay date of the previous dividend and that 92 days are required to earn the full $0.35 dividend

– therefore, it calculates an accrued and unpaid dividend of $0.35 * (84/92) = $0.3196

– BUT! The final dividend has already been declared, the ex-date has passed and holders will actually be receiving $0.35.

– That’s $0.0304 too much! So when the holders have their shares redeemed on the 22nd, they will have to pay it back.

– I know I’m saying $0.0304 here and $0.0307 above. There will be something weird with the day-count that was programmed in years ago, which I’ve forgotten and cannot be bothered to look up. Geez! Sue me.

Thank you for the detailed explanation.