I forgot to mention this earlier: Tiff Macklem has gone through the revolving door:

Bank of Nova Scotia appointed Tiff Macklem, a former Bank of Canada senior deputy governor, to its board of directors.

Macklem stepped down from the Ottawa-based central bank in May 2013 and has been serving as dean of the University of Toronto’s Rotman School of Management since July of that year.

“Tiff’s professional experience and understanding of the financial-services industry makes him a strong addition,” Thomas O’Neill, chairman of the board of directors at Canada’s third-largest bank by assets, said in a statement Monday.

The Russell indices were rebalanced today:

The Russell indexes are about to go through their annual rebalancing, leading to what Convergex, the global brokerage firm that’s based in New York, says will “almost certainly be the busiest trading day of the year.”

What’s more, as much as half of today’s trading volume may come in the last five minutes of the session.

Russell’s large-cap index includes 1,000 corporate names while the small-cap index has 2,000. Together they cover more than 90 percent of “reasonably investable” U.S. stocks, according to Convergex.

It will be interesting to learn whether there is any weeping from the regulators regarding institutional desk ‘trading against their clients’ by accumulating positions in advance. Why not? That’s the sort of idiotic wail we’ve heard about FX fixing.

As it happens, Convergex’ prediction didn’t come true:

About 8.9 billion shares changed hands in the U.S. today, the third-busiest session of the year. Russell’s U.S. stock indexes, including the Russell 1000 Index and the Russell 2000, are used as benchmarks for $5.2 trillion in assets, according to the company’s website.

Bloomberg published a nice chart illustrating Greek bank deposits:

Click for Big

My old buddy Doug Grieve, who was on the preferred share institutional desk at Nesbitt for a long, long time, has recently become the Portfolio Manager for Lysander-Slater Preferred Share Dividend Fund.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 10bp, FixedResets gaining 30bp and DeemedRetractibles down 13bp. The Performance Highlights table is dominated by winning FixedResets – we haven’t seen that for a while! Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

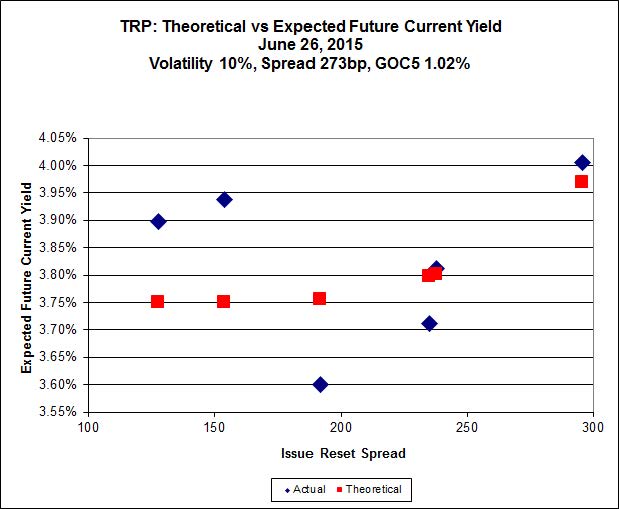

Here’s TRP:

Click for Big

TRP.PR.A, which resets 2019-12-31 at +192, is bid at 20.42 to be $0.84 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.82 cheap at its bid price of 16.25.

Click for Big

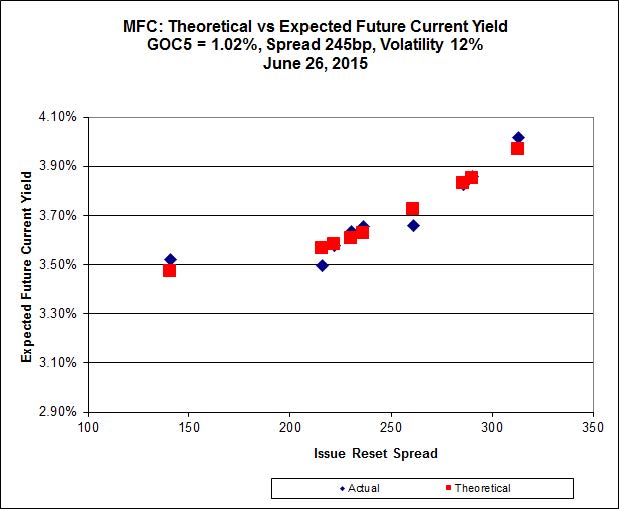

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule). The lowest spread issue, MFC.PR.F, is again noticeably off the line defined by the higher-spread issues.

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 22.75 to be $0.46 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.83 to be $0.31 cheap.

Click for Big

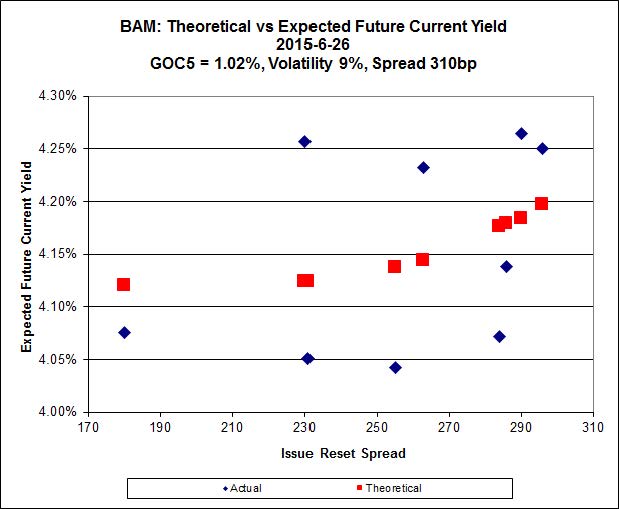

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.50 to be $0.63 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 22.08 and appears to be $0.51 rich.

Click for Big

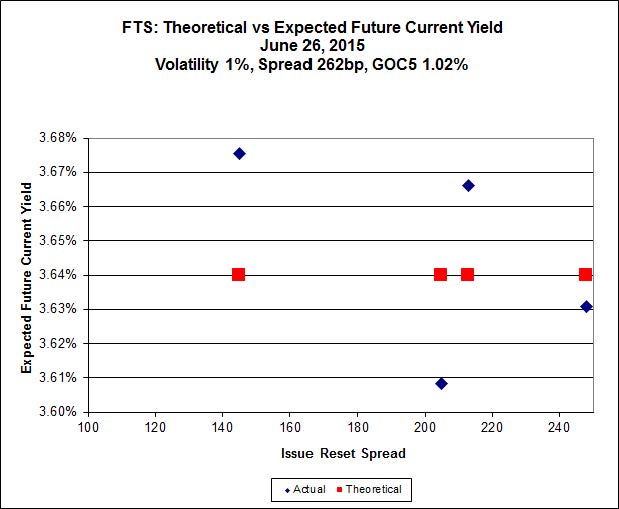

FTS.PR.H, with a spread of +145bp, and bid at 16.80, looks $0.16 cheap and resets 2020-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.27 and is $0.18 rich.

Click for Big

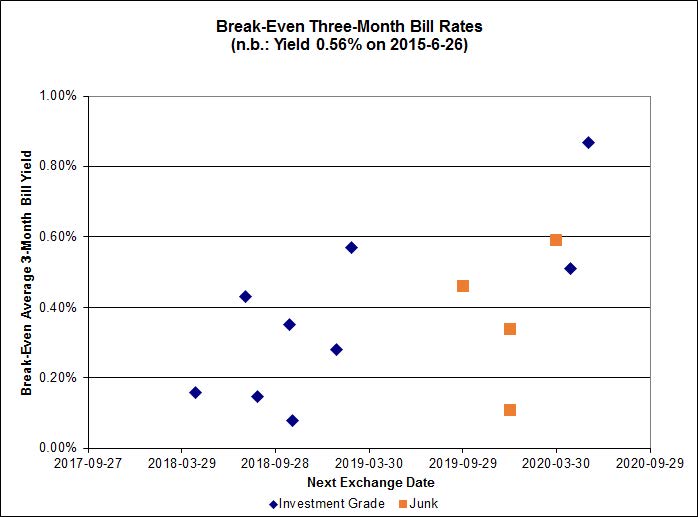

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.30%, including the outlier TRP.PR.A / TRP.PR.F at -0.50%. On the junk side there are two outliers: FFH.PR.E / FFH.PR.F at -0.54%; and BRF.PR.A / BRF.PR.B at -0.25%.

Click for Big

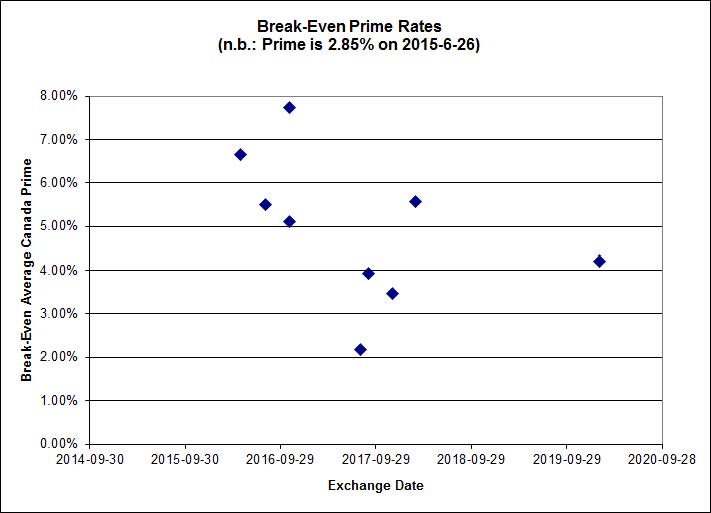

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3124 % | 2,160.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.3124 % | 3,777.5 |

| Floater | 3.58 % | 3.60 % | 61,691 | 18.28 | 3 | 0.3124 % | 2,296.7 |

| OpRet | 4.78 % | -8.20 % | 22,554 | 0.08 | 1 | 0.0000 % | 2,781.3 |

| SplitShare | 4.58 % | 4.81 % | 73,896 | 3.26 | 3 | 0.1742 % | 3,254.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,543.2 |

| Perpetual-Premium | 5.48 % | 4.24 % | 62,311 | 0.51 | 19 | 0.1339 % | 2,516.6 |

| Perpetual-Discount | 5.27 % | 5.20 % | 116,415 | 15.07 | 15 | -0.0993 % | 2,669.4 |

| FixedReset | 4.55 % | 3.80 % | 235,375 | 16.09 | 88 | 0.2959 % | 2,333.2 |

| Deemed-Retractible | 5.04 % | 3.38 % | 112,680 | 0.89 | 34 | -0.1343 % | 2,606.7 |

| FloatingReset | 2.49 % | 2.92 % | 56,168 | 6.09 | 9 | 0.0542 % | 2,334.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.E | FixedReset | -2.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 21.70 Evaluated at bid price : 22.08 Bid-YTW : 4.24 % |

| BAM.PF.B | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 21.28 Evaluated at bid price : 21.56 Bid-YTW : 4.33 % |

| MFC.PR.B | Deemed-Retractible | -1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.24 Bid-YTW : 6.24 % |

| FTS.PR.J | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 23.07 Evaluated at bid price : 23.41 Bid-YTW : 5.11 % |

| FTS.PR.K | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 21.27 Evaluated at bid price : 21.27 Bid-YTW : 3.80 % |

| BAM.PR.C | Floater | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 13.51 Evaluated at bid price : 13.51 Bid-YTW : 3.69 % |

| MFC.PR.N | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 4.72 % |

| ENB.PR.D | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 4.92 % |

| MFC.PR.K | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.65 Bid-YTW : 4.68 % |

| NA.PR.S | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 23.00 Evaluated at bid price : 24.32 Bid-YTW : 3.55 % |

| FTS.PR.H | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 3.67 % |

| BMO.PR.T | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 22.03 Evaluated at bid price : 22.51 Bid-YTW : 3.73 % |

| TRP.PR.E | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 22.14 Evaluated at bid price : 22.70 Bid-YTW : 3.83 % |

| MFC.PR.M | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.12 Bid-YTW : 4.63 % |

| MFC.PR.F | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 7.14 % |

| BMO.PR.W | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 22.04 Evaluated at bid price : 22.55 Bid-YTW : 3.68 % |

| BAM.PR.T | FixedReset | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 20.55 Evaluated at bid price : 20.55 Bid-YTW : 4.17 % |

| BAM.PR.B | Floater | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 14.40 Evaluated at bid price : 14.40 Bid-YTW : 3.46 % |

| IAG.PR.G | FixedReset | 2.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.65 Bid-YTW : 4.13 % |

| TRP.PR.C | FixedReset | 3.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 3.92 % |

| TD.PF.A | FixedReset | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 22.17 Evaluated at bid price : 22.75 Bid-YTW : 3.71 % |

| HSE.PR.A | FixedReset | 3.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 16.25 Evaluated at bid price : 16.25 Bid-YTW : 4.32 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.R | FloatingReset | 153,921 | Desjardins bought blocks of 17,100 and 85,500 from RBC, both at 24.05. TD crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.02 Bid-YTW : 2.87 % |

| ENB.PR.N | FixedReset | 88,870 | TD crossed 74,800 at 18.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 4.94 % |

| ENB.PR.F | FixedReset | 77,669 | Scotia crossed 41,900 at 18.20; RBC bought 10,000 from Nesbitt at 18.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 4.94 % |

| BNS.PR.R | FixedReset | 71,895 | Nesbitt crossed 35,000 at 25.51. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 3.18 % |

| CU.PR.F | Perpetual-Discount | 45,608 | Scotia crossed 40,000 at 21.95. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 21.56 Evaluated at bid price : 21.85 Bid-YTW : 5.19 % |

| ENB.PR.T | FixedReset | 34,865 | Scotia crossed 30,000 at 18.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-06-26 Maturity Price : 18.36 Evaluated at bid price : 18.36 Bid-YTW : 4.94 % |

| There were 25 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.C | Deemed-Retractible | Quote: 22.13 – 22.99 Spot Rate : 0.8600 Average : 0.5876 YTW SCENARIO |

| BAM.PF.B | FixedReset | Quote: 21.56 – 22.00 Spot Rate : 0.4400 Average : 0.2957 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 22.24 – 22.64 Spot Rate : 0.4000 Average : 0.2636 YTW SCENARIO |

| MFC.PR.F | FixedReset | Quote: 17.25 – 17.84 Spot Rate : 0.5900 Average : 0.4554 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 19.26 – 19.84 Spot Rate : 0.5800 Average : 0.4506 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 16.56 – 17.23 Spot Rate : 0.6700 Average : 0.5541 YTW SCENARIO |

well, whatever money might have still been in the banking system in Greece is being sucked out as fast as the Greeks can withdraw it.

At sixty euros per day each, as reported June 29; and now I see that the ATMs are pretty much empty anyway: