Janet Yellen gave a speech today:

Federal Reserve Chair Janet Yellen said the U.S. central bank is on track to raise interest rates this year, even as she acknowledged that economic “surprises” could lead them to change that plan.

“Most FOMC participants, including myself, currently anticipate that achieving these conditions will likely entail an initial increase in the federal funds rate later this year, followed by a gradual pace of tightening thereafter,” Yellen said during a speech Thursday in Amherst, Massachusetts. “But if the economy surprises us, our judgments about appropriate monetary policy will change.”

…

While “there wasn’t anything significant enough that changed in one week for her to give us a different take,” said Tom Porcelli, chief U.S. economist at RBC Capital Markets LLC in New York, Yellen “finally acknowledges that she, specifically, does believe that a rate hike is appropriate this year.”Porcelli expects a December increase, but thinks there’s a high hurdle to moving this year.

Short-term treasuries were hammered, but the rest of the Treasury market took it in stride:

The U.S. two-year yield climbed four basis points to 0.72 percent as of 6:14 a.m. in London. The price of the 0.625 percent security due September 2017 fell 2/32, or 63 cents per $1,000 face amount, to 99 26/32.

The benchmark 10-year yield rose one basis point to 2.14 percent.

Traders aren’t convinced a rate increase is a sure thing. There’s a 49 percent probability the Fed will raise rates by its Dec. 15-16 meeting, down from 60 percent odds at the end of August, according to data compiled by Bloomberg. The calculation is based on the assumption that the effective fed funds rate will average 0.375 percent after liftoff.

Treasury 30-year bonds, which are more influenced by the outlook for inflation, eked out a gain. The difference between two- and 30-year yields shrank to as little as 2.19 percentage points, the narrowest since Sept. 8.

Preferred share investors drove to an appointment with their brokers today:

Click for Big

(hat tip: adrian2 on FWF)

“But my money!” they cried. “What has happened to my money?”

Click for Big

It was total carnage for the Canadian preferred share market today, with PerpetualDiscounts down 152bp, FixedResets losing a stunning 338bp and DeemedRetractibles off 92bp. The Performance Highlights table is ridiculous and I’m not even going to try to come to grips with the question of what’s real and what isn’t (except for MFC.PR.N … I couldn’t resist) because the entire market was surreal today. BAM issues were notable losers, but one BAM issue was the sole notable winner! Volume was extremely heavy.

So what caused the problem? Assigning specific reasons to market movements, even dramatic ones is always a bit of a mug’s game; on a day-to-day basis, the market does what it wants to do because it wants to do it. Today the influence might be this, tomorrow that; it’s only in retrospect that you can draw a correlation between the financial markets and the price of eggs in Spain and say wisely how well the market took this driving influence into account. My contempt for the market’s talking heads is mixed with pity; they have to come up with something to fill up their allotted half hour and that’s the end of it.

But it’s reasonable to suppose it was the BAM new issue that broke the camel’s back. 5.00% is a big fat dividend for an investment grade issue and 417bp is a big fat spread and the minimum rate guarantee is a big fat gift for those who seriously believe that GOC-5 can go significantly lower in the next five years (I don’t! But what do I know?). As recently as September 11, when I prepared the September PrefLetter, a spread of 417bp would have implied a yield-to-worst of only 4.49%, although correlations are poor and +417 is the highest extant investment-grade spread by far (so don’t take the decimal places too seriously, is what I’m saying) (the previous high was HSE.PR.E, with an Issue Reset Spread of a mere 357bp). A big fat yield like that could well have caused some repricing of the market as a whole; it is significant that the clobbering of BAM issues today was notable even on a day like today; and the results of that clobbering reverberated throughout the market.

Conspiracy theorists will soon be filling up my mailbox with queries about my opinion regarding the idea that Brookfield did this deliberately so they could buy up their extant issues cheaply under their NCIB, discussed August 12. But really, guys – get serious. The Illuminati would never permit me to give a favourable opinion regarding this thesis.

It is also possible that the credit rating assigned to Element Financial today had an effect; this expands the universe with four FixedResets with very nice yields; it is noteworthy that all four extant EFN issues rose today (on a close/close basis). Volumes were mostly modest, but the most recent issue, EFN.PR.G, traded a significant 35,025 shares. These issues also have high spreads:

- EFN.PR.A, FixedReset, 6.60%+471

- EFN.PR.C, FixedReset, 6.50%+481

- EFN.PR.E, FixedReset, 6.40%+472

- EFN.PR.G, FixedReset, 6.50%+534

The highest Issue Reset Spread on a junk issue previous was a mere 427bp for VSN.PR.E.

I will point out that I’m not the only guy in the universe who holds the disciplinary effects of a public credit rating in high regard – their press release disclosed that:

Concurrent with the receipt of this initial issuer rating from DBRS, the interest rate applicable to the Facility will be reduced by 35 basis points …

So I’ll suggest a strong possibility that this was an aggravating factor.

Another aggravating factor could be quarter-end. I mused that the Swoon in June, 2008, was due at least partly to end of quarter window-dressing by retail stockbrokers and I’ll muse that again. I remember being urged by a putative superior to sell a particular issue simply because it had gone down; the client was going to ask questions. It’s the stupidest rationale ever for market action, but there can be no denying that it’s real! Trades executed today settle September 29; trades executed tomorrow will still result in the position vanishing from quarter-end statements … who knows what might happen?

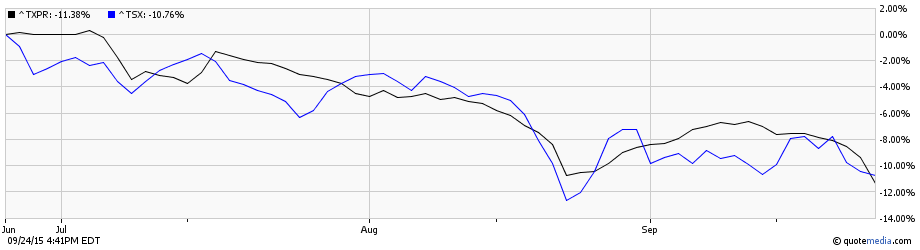

And finally, there’s the idea that in bad times all correlations go to 1: here’s the chart for TXPR vs. TSX for the past three months (hat tip: OnlyMyOpinion on FWF), which will give joy to the ‘preferreds are bonds on the way up and stocks on the way down’ crowd:

Click for Big

But in the end, the market does what it wants to do when it wants to do it. Beyond that, we’re guessing.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

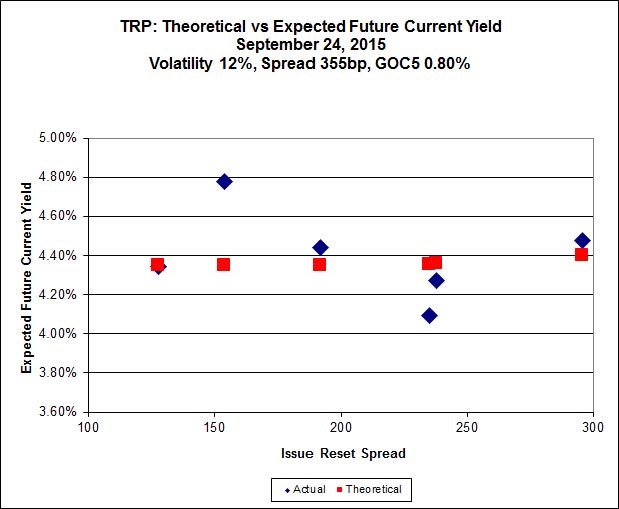

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.25 to be $1.17 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.20 cheap at its bid price of 12.25.

Click for Big

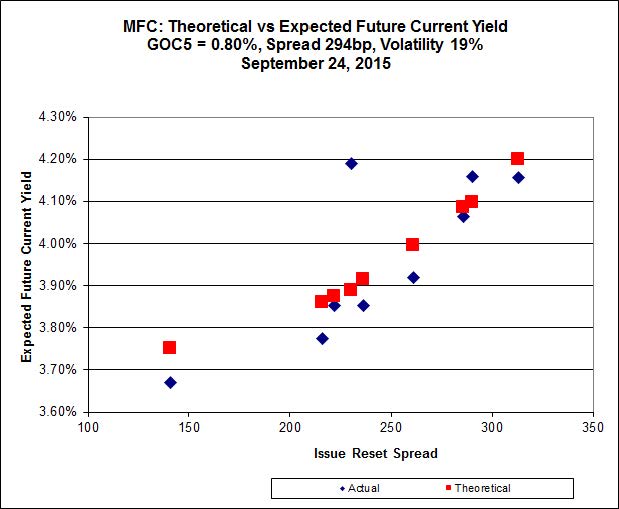

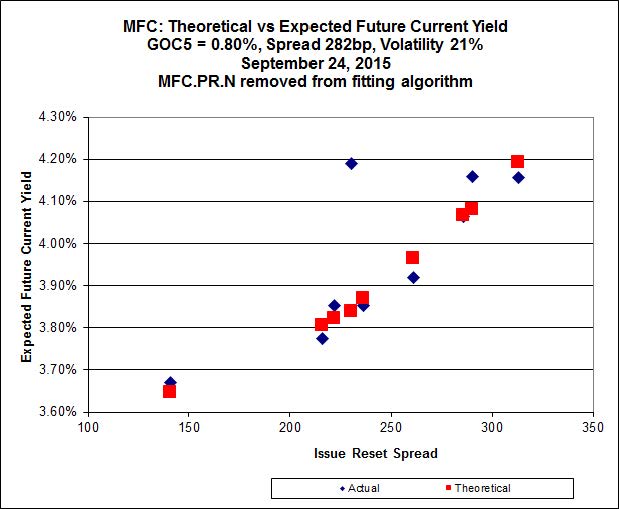

The MFC fit has been clearly distorted by the lousy and almost certainly grossly erroneous bid on MFC.PR.N (see Performance Highlights table), so we’ll remove it from the fitting and try again.

Click for Big

Another good fit today for MFC, with Implied Volatility leaping upwards today – the lower-spread issues outperformed.

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 21.75 to be 0.24 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.24 to be 0.43 cheap (MFC.PR.N has been ignored)

Click for Big

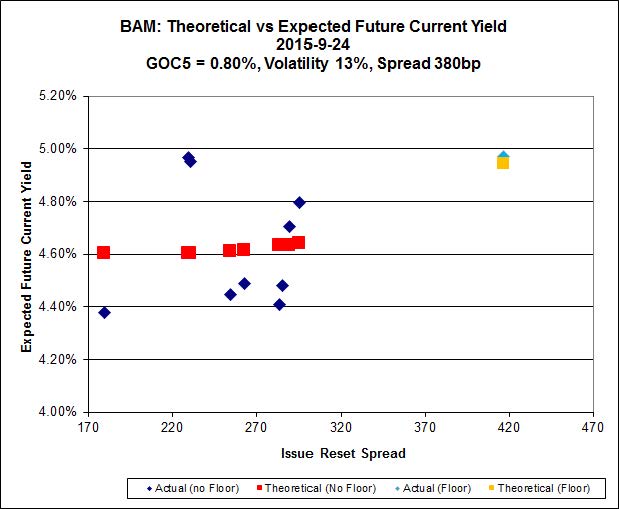

The fit on the BAM issues continues to be horrible. Note that the new issue announced today has been added with a price of 25.00; the valuation effects of the rate floor have been ignored.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.60 to be $1.24 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.65 and appears to be $1.00 rich.

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 20.60, looks $0.70 expensive and resets 2019-12-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.30 and is $0.48 cheap.

Click for Big

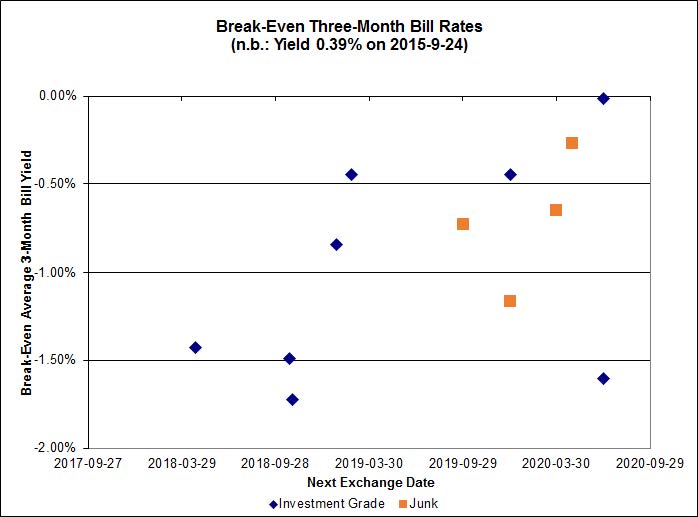

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.05%, with two outliers below -2.00% and two above 0.00%. The distribution’s bimodality has returned, with bank NVCC non-compliant pairs averaging -1.54% and other issues averaging -0.35%. There are two junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2885 % | 1,639.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2885 % | 2,866.9 |

| Floater | 4.53 % | 4.53 % | 60,746 | 16.37 | 3 | 0.2885 % | 1,743.1 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0709 % | 2,768.9 |

| SplitShare | 4.48 % | 4.96 % | 64,509 | 2.08 | 4 | -0.0709 % | 3,245.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0709 % | 2,531.9 |

| Perpetual-Premium | 5.76 % | 2.64 % | 64,771 | 0.08 | 8 | -0.4563 % | 2,482.7 |

| Perpetual-Discount | 5.59 % | 5.68 % | 68,460 | 14.38 | 30 | -1.5237 % | 2,538.3 |

| FixedReset | 4.98 % | 4.51 % | 176,429 | 15.47 | 75 | -3.3821 % | 2,043.6 |

| Deemed-Retractible | 5.22 % | 5.09 % | 93,716 | 5.48 | 33 | -0.9241 % | 2,548.3 |

| FloatingReset | 2.57 % | 4.52 % | 56,496 | 5.85 | 9 | -1.9662 % | 2,082.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.N | FixedReset | -10.41 % | Not real. The issue traded 10,244 shares today in a range of 20.00-65 before closing at 18.50-20.64 (!). I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 7.43 % |

| BAM.PF.F | FixedReset | -8.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.42 Evaluated at bid price : 20.42 Bid-YTW : 4.74 % |

| BAM.PF.A | FixedReset | -8.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.66 Evaluated at bid price : 19.66 Bid-YTW : 4.91 % |

| BAM.PF.G | FixedReset | -7.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.70 % |

| TD.PF.D | FixedReset | -7.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.52 Evaluated at bid price : 21.83 Bid-YTW : 4.16 % |

| BMO.PR.Y | FixedReset | -7.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.28 % |

| BAM.PF.E | FixedReset | -6.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 18.84 Evaluated at bid price : 18.84 Bid-YTW : 4.84 % |

| TD.PF.C | FixedReset | -6.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.33 Evaluated at bid price : 19.33 Bid-YTW : 4.22 % |

| NA.PR.W | FixedReset | -6.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.25 % |

| FTS.PR.H | FixedReset | -6.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 13.41 Evaluated at bid price : 13.41 Bid-YTW : 4.36 % |

| BAM.PF.B | FixedReset | -5.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.73 % |

| HSE.PR.E | FixedReset | -5.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.27 % |

| FTS.PR.G | FixedReset | -5.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 4.51 % |

| BMO.PR.R | FloatingReset | -5.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 4.98 % |

| BAM.PR.X | FixedReset | -5.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 14.85 Evaluated at bid price : 14.85 Bid-YTW : 4.73 % |

| GWO.PR.P | Deemed-Retractible | -5.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 6.52 % |

| FTS.PR.M | FixedReset | -5.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 4.24 % |

| CM.PR.Q | FixedReset | -4.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.54 Evaluated at bid price : 21.85 Bid-YTW : 4.09 % |

| BMO.PR.S | FixedReset | -4.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.11 % |

| BAM.PR.T | FixedReset | -4.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 15.70 Evaluated at bid price : 15.70 Bid-YTW : 5.21 % |

| TD.PF.A | FixedReset | -4.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.13 % |

| TD.PF.B | FixedReset | -4.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 4.12 % |

| IFC.PR.A | FixedReset | -4.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.25 Bid-YTW : 9.49 % |

| RY.PR.J | FixedReset | -4.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.65 Evaluated at bid price : 22.00 Bid-YTW : 4.06 % |

| RY.PR.Z | FixedReset | -4.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.87 Evaluated at bid price : 19.87 Bid-YTW : 4.07 % |

| NA.PR.Q | FixedReset | -4.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.45 Bid-YTW : 4.67 % |

| RY.PR.H | FixedReset | -4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.09 % |

| RY.PR.M | FixedReset | -4.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 4.07 % |

| BMO.PR.W | FixedReset | -4.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.69 Evaluated at bid price : 19.69 Bid-YTW : 4.10 % |

| CM.PR.O | FixedReset | -4.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.21 Evaluated at bid price : 20.21 Bid-YTW : 4.06 % |

| BMO.PR.T | FixedReset | -3.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.07 % |

| TD.PR.Z | FloatingReset | -3.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.59 Bid-YTW : 4.54 % |

| SLF.PR.I | FixedReset | -3.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 6.59 % |

| BAM.PR.R | FixedReset | -3.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 15.60 Evaluated at bid price : 15.60 Bid-YTW : 5.14 % |

| MFC.PR.J | FixedReset | -3.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 5.41 % |

| FTS.PR.K | FixedReset | -3.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 17.20 Evaluated at bid price : 17.20 Bid-YTW : 4.50 % |

| TRP.PR.G | FixedReset | -3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.01 Evaluated at bid price : 21.01 Bid-YTW : 4.54 % |

| TRP.PR.B | FixedReset | -3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 11.97 Evaluated at bid price : 11.97 Bid-YTW : 4.42 % |

| TD.PF.E | FixedReset | -3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 22.39 Evaluated at bid price : 23.21 Bid-YTW : 3.96 % |

| TD.PR.T | FloatingReset | -3.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.51 Bid-YTW : 4.52 % |

| NA.PR.S | FixedReset | -3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.84 Evaluated at bid price : 20.84 Bid-YTW : 4.10 % |

| POW.PR.A | Perpetual-Premium | -3.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.73 Evaluated at bid price : 24.04 Bid-YTW : 5.83 % |

| IFC.PR.C | FixedReset | -3.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.60 Bid-YTW : 7.42 % |

| CM.PR.P | FixedReset | -3.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.11 % |

| MFC.PR.H | FixedReset | -3.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.64 Bid-YTW : 4.81 % |

| GWO.PR.N | FixedReset | -3.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.36 % |

| GWO.PR.Q | Deemed-Retractible | -3.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.63 Bid-YTW : 6.55 % |

| TRP.PR.E | FixedReset | -3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 4.48 % |

| BAM.PF.D | Perpetual-Discount | -3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.89 Evaluated at bid price : 20.89 Bid-YTW : 5.90 % |

| PWF.PR.S | Perpetual-Discount | -2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.26 Evaluated at bid price : 21.54 Bid-YTW : 5.65 % |

| RY.PR.O | Perpetual-Discount | -2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.09 Evaluated at bid price : 23.50 Bid-YTW : 5.28 % |

| BAM.PF.C | Perpetual-Discount | -2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.48 Evaluated at bid price : 20.48 Bid-YTW : 5.96 % |

| TRP.PR.C | FixedReset | -2.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 12.25 Evaluated at bid price : 12.25 Bid-YTW : 4.95 % |

| TRP.PR.A | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 15.32 Evaluated at bid price : 15.32 Bid-YTW : 4.69 % |

| TRP.PR.D | FixedReset | -2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 18.61 Evaluated at bid price : 18.61 Bid-YTW : 4.57 % |

| PWF.PR.T | FixedReset | -2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.93 Evaluated at bid price : 22.28 Bid-YTW : 3.79 % |

| MFC.PR.G | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.24 Bid-YTW : 5.36 % |

| BAM.PR.N | Perpetual-Discount | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 5.87 % |

| POW.PR.D | Perpetual-Discount | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.72 Evaluated at bid price : 21.97 Bid-YTW : 5.69 % |

| CU.PR.C | FixedReset | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.13 % |

| VNR.PR.A | FixedReset | -2.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.35 Evaluated at bid price : 19.35 Bid-YTW : 4.88 % |

| SLF.PR.E | Deemed-Retractible | -2.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.60 Bid-YTW : 7.14 % |

| BMO.PR.Z | Perpetual-Discount | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.67 Evaluated at bid price : 24.00 Bid-YTW : 5.28 % |

| MFC.PR.I | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.52 Bid-YTW : 5.23 % |

| RY.PR.N | Perpetual-Discount | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.48 Evaluated at bid price : 23.79 Bid-YTW : 5.27 % |

| PWF.PR.F | Perpetual-Discount | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.11 Evaluated at bid price : 23.37 Bid-YTW : 5.70 % |

| GWO.PR.S | Deemed-Retractible | -2.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.18 Bid-YTW : 6.32 % |

| MFC.PR.L | FixedReset | -2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.60 Bid-YTW : 6.55 % |

| SLF.PR.B | Deemed-Retractible | -1.99 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.67 Bid-YTW : 6.77 % |

| TD.PF.F | Perpetual-Discount | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.53 Evaluated at bid price : 23.85 Bid-YTW : 5.21 % |

| MFC.PR.B | Deemed-Retractible | -1.97 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.37 Bid-YTW : 6.82 % |

| CU.PR.D | Perpetual-Discount | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.43 Evaluated at bid price : 21.75 Bid-YTW : 5.68 % |

| SLF.PR.C | Deemed-Retractible | -1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.40 Bid-YTW : 7.22 % |

| BNS.PR.B | FloatingReset | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.68 Bid-YTW : 4.49 % |

| GWO.PR.G | Deemed-Retractible | -1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.02 Bid-YTW : 6.37 % |

| SLF.PR.A | Deemed-Retractible | -1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 6.82 % |

| MFC.PR.M | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.51 Bid-YTW : 6.12 % |

| PWF.PR.K | Perpetual-Discount | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.88 Evaluated at bid price : 22.12 Bid-YTW : 5.68 % |

| W.PR.J | Perpetual-Discount | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.68 Evaluated at bid price : 23.95 Bid-YTW : 5.96 % |

| IAG.PR.G | FixedReset | -1.77 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.26 Bid-YTW : 5.31 % |

| CU.PR.G | Perpetual-Discount | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 5.63 % |

| SLF.PR.D | Deemed-Retractible | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.45 Bid-YTW : 7.18 % |

| ENB.PR.A | Perpetual-Discount | -1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.85 Evaluated at bid price : 24.10 Bid-YTW : 5.76 % |

| RY.PR.W | Perpetual-Discount | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.53 Evaluated at bid price : 23.80 Bid-YTW : 5.19 % |

| PWF.PR.P | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.13 % |

| BIP.PR.A | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.15 % |

| CU.PR.E | Perpetual-Discount | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.36 Evaluated at bid price : 21.65 Bid-YTW : 5.71 % |

| FTS.PR.J | Perpetual-Discount | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.26 Evaluated at bid price : 21.26 Bid-YTW : 5.65 % |

| BAM.PR.M | Perpetual-Discount | -1.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 5.83 % |

| GWO.PR.H | Deemed-Retractible | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 6.46 % |

| BMO.PR.Q | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.86 Bid-YTW : 5.43 % |

| BNS.PR.A | FloatingReset | -1.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.58 Bid-YTW : 4.16 % |

| MFC.PR.K | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.60 Bid-YTW : 6.46 % |

| BNS.PR.Y | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 5.25 % |

| POW.PR.B | Perpetual-Discount | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.69 % |

| ELF.PR.H | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.41 Evaluated at bid price : 23.85 Bid-YTW : 5.86 % |

| PWF.PR.L | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 22.75 Evaluated at bid price : 23.03 Bid-YTW : 5.62 % |

| GWO.PR.R | Deemed-Retractible | -1.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.61 Bid-YTW : 6.81 % |

| RY.PR.I | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 3.96 % |

| HSE.PR.G | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 21.86 Evaluated at bid price : 22.30 Bid-YTW : 4.93 % |

| GWO.PR.I | Deemed-Retractible | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.31 Bid-YTW : 6.67 % |

| BAM.PR.Z | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 5.02 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CU.PR.I | FixedReset | 973,025 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 23.18 Evaluated at bid price : 25.08 Bid-YTW : 4.39 % |

| NA.PR.M | Deemed-Retractible | 325,596 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-10-24 Maturity Price : 25.50 Evaluated at bid price : 25.80 Bid-YTW : -0.59 % |

| BAM.PF.A | FixedReset | 86,627 | CIBC crossed 31,200 at 20.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 19.66 Evaluated at bid price : 19.66 Bid-YTW : 4.91 % |

| MFC.PR.H | FixedReset | 84,372 | RBC crossed 73,800 at 24.40. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.64 Bid-YTW : 4.81 % |

| BAM.PF.G | FixedReset | 84,356 | RBC bought 16,800 from anonymous at 22.31. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-24 Maturity Price : 20.65 Evaluated at bid price : 20.65 Bid-YTW : 4.70 % |

| BNS.PR.B | FloatingReset | 50,163 | Scotia crossed 48,200 at 21.75. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.68 Bid-YTW : 4.49 % |

| There were 57 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.N | FixedReset | Quote: 18.50 – 20.64 Spot Rate : 2.1400 Average : 1.1813 YTW SCENARIO |

| BMO.PR.R | FloatingReset | Quote: 21.00 – 22.10 Spot Rate : 1.1000 Average : 0.6408 YTW SCENARIO |

| TD.PF.D | FixedReset | Quote: 21.83 – 22.83 Spot Rate : 1.0000 Average : 0.6186 YTW SCENARIO |

| BMO.PR.Y | FixedReset | Quote: 21.50 – 22.50 Spot Rate : 1.0000 Average : 0.6325 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 21.03 – 22.00 Spot Rate : 0.9700 Average : 0.6305 YTW SCENARIO |

| GWO.PR.P | Deemed-Retractible | Quote: 23.11 – 23.83 Spot Rate : 0.7200 Average : 0.4373 YTW SCENARIO |

i was wondering if we’d ever get a buying opportunity anywhere near like the one in 2008… i guess we’re getting one now..

Pretty close – but the comparison does not relive the full horror of those days. At the moment the Seniority Spread (interest-equivalent PerpetualDiscount yield less long corporate bond yield) is “only” about 320bp.

This spread was above 320bp for the period 2008-11-26 to 2008-12-24 and peaked at 445bp. It also went slightly past this level throughout May, 2010.

i don’t really want to relive the horror of 2008….