I will be very disappointed if this is the end of the Silver-Sprott battle:

Today, Silver Bullion Trust (TSX:SBT.UN) (C$) (TSX:SBT.U) (US$) (“SBT”) entered into a new definitive agreement with Purpose Investments Inc. (“Purpose”), regarding the conversion of SBT into a silver bullion exchange-traded fund (“ETF”) managed by Purpose and Silver Administrators Limited. The proposed ETF conversion, which is subject to unitholder approval, has the unanimous support of your Independent Trustees and represents an exciting opportunity for SBT unitholders.

Purpose has current assets under management of over $1.4 billion across 17 funds and is one of Canada’s most experienced ETF managers, with significant experience in managing and marketing bullion funds. Purpose’s predecessor company, Claymore Investments, which was acquired by BlackRock in 2012, managed the Claymore Silver Bullion Trust, which was successfully converted into an ETF in 2012. For further information on Purpose, we encourage unitholders to visit their website at www.purposeinvest.com.

Andrew Jackson, of Carleton University and the Broadbent Institute, is making much more sense now that he no longer works for the Canadian Labour Congress! He’s written a piece for the Globe titled Global slump should be addressed by this monetary taboo, which includes a paen to micromanagement:

As Adair Turner shows in his new book, Between Debt and the Devil, private-sector debt soared as a share of GDP in most advanced economies after the 1980s, fuelling unproductive, debt-financed household consumption, housing bubbles and wasteful financial speculation.

…

Adair Turner, former chief regulator of British banks, argues that we need to reign in the growth of unproductive private debt by imposing tighter controls on banks through much higher capital requirements and by imposing limits on borrowing, such as maximum loan-to-value mortgage rules. Banks should, he argues, be pushed to support real business investment as opposed to highly leveraged financial speculation and household consumption.

Mr. Jackson’s egalitarian impulses were, no doubt, responsible for his refusal to use Lord Turner’s honorific!

The Grauniad’s review provides more detail:

When capitalism works, debt channels money into factories, machinery and know how. There will be bumps along the road, but the economy will grow. In the run up to 2007, however, the made-up money was not going into anything productive, but rather inflating the price of pre-existing homes. Indeed, Turner locates the roots of the crisis in the mismatch between a limited supply of urban land, and the limitless potential to finance rising demand for it. For individual banks, it can make sense to lend for unrealistically costly houses, since mortgaged families will sacrifice everything else to keep up payments and avoid ending up on the streets. For the economy as a whole, however, concentrating debt in property is a disaster, draining resources from worthwhile investment and wagering collective prosperity on a one-way bet. Worse, while debt-fuelled bursts of real activity will push up inflation, when all the money is in property that warning light never flashes. We’re all left exposed: unsafe as houses.

…

To kick our addiction to debt, Turner argues, we can and should restrain the banks, for example by forcing them to hold more reserves. We can and should also devise new ways to privilege productive investment over property speculation. Turner, who became chair of the Financial Services Authority days after Lehman Bros toppled, puts great emphasis on explaining how regulators could do all this practically, a dimension that gives the book extra importance, albeit at the occasional expense of readability. Every so often you yearn for him to say “posh houses”, rather than “locationally desirable real estate”.

The Independent offers some criticism:

Turner is admirably fearless. He goes where his fundamental analysis tells him to go. But is his underlying thesis right? A weakness of the book is that Turner doesn’t fully engage with the counter evidence. For instance, there are signs that small firms in the UK have been turned down for loans by their banks, or at least discouraged from seeking credit – an indication that lack of credit supply is part of the problem. Demand for mortgages in th UK seems to have bounced back, despite still elevated household debt to income ratios here in Britain.

There are also other plausible explanations, beyond excessive debt, for the weak recoveries across the world, not least the thesis of secular stagnation. Perhaps the incubus squatting on the chest of our economies is not a debt overhang, as Turner asserts, but slow growth brought on by demographic trends. Or maybe its dunderheaded fiscal austerity imposed by governments that’s primarily to blame.

Lord Turner’s previous notable production was highlighted on PrefBlog when UK FSA Publishes Turner Report on Bank Regulation with more commentary in HM Treasury Responds to Turner Report. It looks like it could be a decent book … I might buy it!

Oh, and speaking of houses:

Properties in Canadian cities don’t command New York prices but Canada is definitely rising in the ranks, Mr. Henry says.

Juwai.com crunched its latest numbers for The Globe and found that, within Canada, Chinese buyers of sumptuous properties have shifted their preference toward Toronto and away from Vancouver.

The average price for property viewed by Chinese property hunters in Toronto has increased over the past two years as the average price in Vancouver has declined, according to Juwai.com. The two cities have switched roles, with Toronto now attracting a higher-priced buyer mix than Vancouver.

In five of the past six months, Juwai.com’s users have searched for a higher average price in Toronto than in Vancouver.

In October, for example, the average search price in Toronto was $1,963,278, compared with $1,268,194 in Vancouver. In October of 2014, the average search price in Toronto was $1,582,300 and, in Vancouver, $1,840,999.

Brompton’s Life & Banc Split Corp., proud issuer of LBS.PR.A, was confirmed at Pfd-3(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the rating on the Preferred Shares issued by Life & Banc Split Corp. (the Company) at Pfd-3 (low). In October 2006, the Company raised gross proceeds of $300 million by issuing 12 million Preferred Shares (at $10 each) and an equal number of Class A Shares (at $15 each). Since then, the Company has completed several additional treasury offerings. The final redemption date for both classes of shares issued was originally November 29, 2013, but was extended to November 29, 2018.

…

The performance of the Portfolio has experienced some volatility over the past year, with the downside protection fluctuating between 41.8% and 52.0% from November 2014 to November 2015. As of November 19, 2015, the downside protection available to the Preferred Shares is approximately 45.4% and the dividend coverage ratio is about 1.1 times. The Pfd-3 (low) rating of the Preferred Shares is based primarily on the downside protection available and the additional protection provided by the asset coverage test, which does not permit any distributions to holders of the Class A Shares if the NAV of the Company falls below $15.

It was yet another mixed, mostly negative, bad-for-FixedResets day for the Canadian preferred share market, with PerpetualDiscounts off 2bp, FixedResets down 23bp and DeemedRetractibles gaining 2bp. The Performance Highlights table is lengthy. Volume was very high.

PerpetualDiscounts now yield 5.64%, equivalent to 7.33% interest at the standard conversion factor of 1.3x. Long Corporates now yield 4.33%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 300bp, a widening from the 290bp reported November 4.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

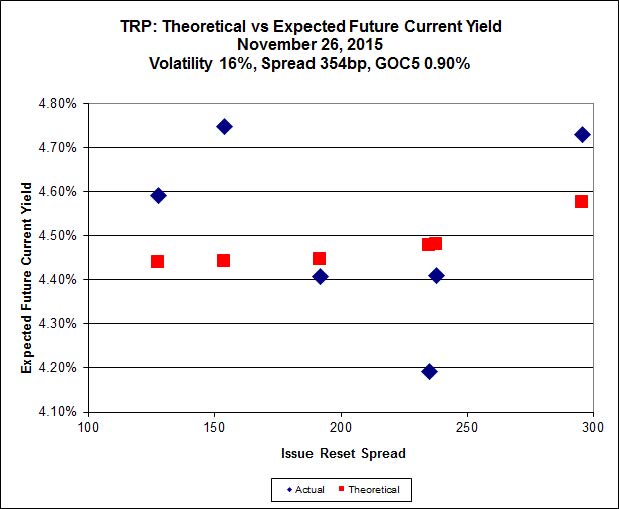

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.38 to be $1.23 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.89 cheap at its bid price of 12.85.

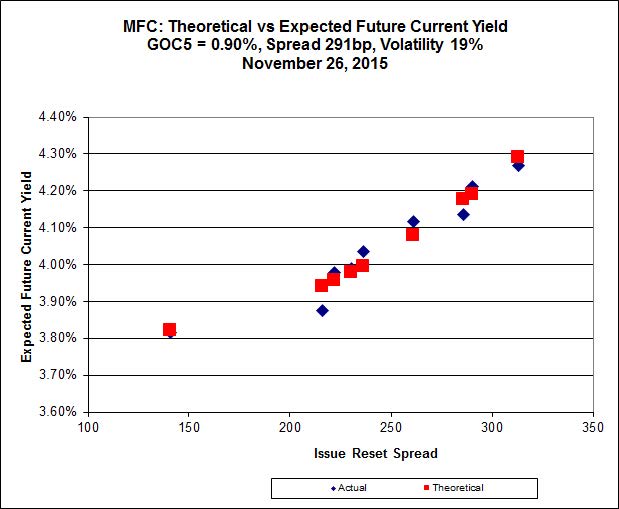

Click for Big

Most expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 19.74 to be 0.33 rich, while MFC.PR.M, resetting at +236bp on 2019-12-19, is bid at 20.20 to be 0.20 cheap.

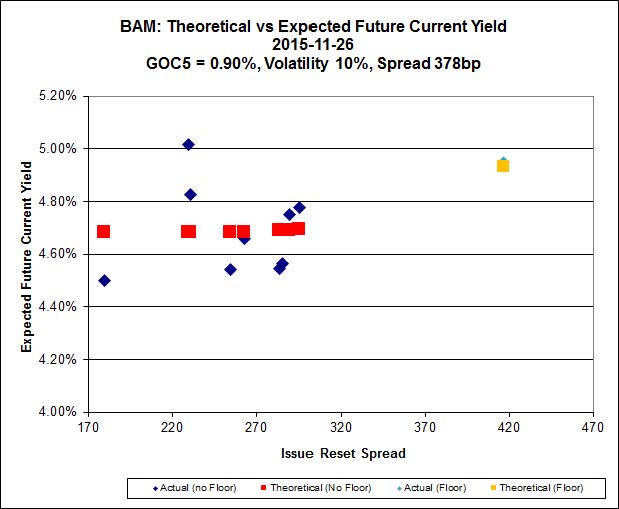

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.95 to be $1.14 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.58 and appears to be $0.63 rich.

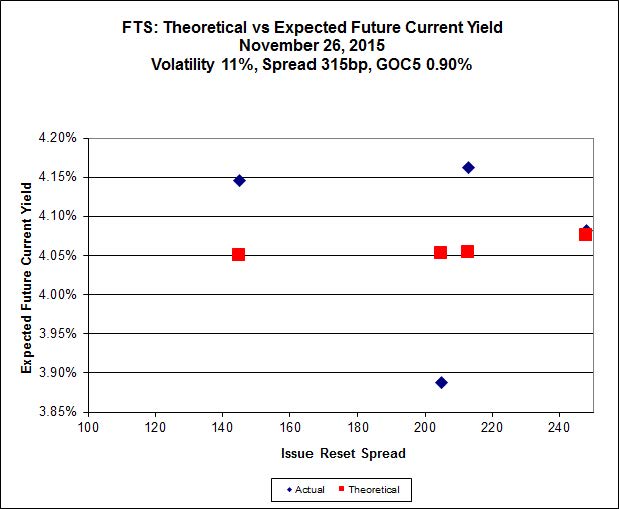

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 18.97, looks $0.77 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.20 and is $0.48 cheap.

Click for Big

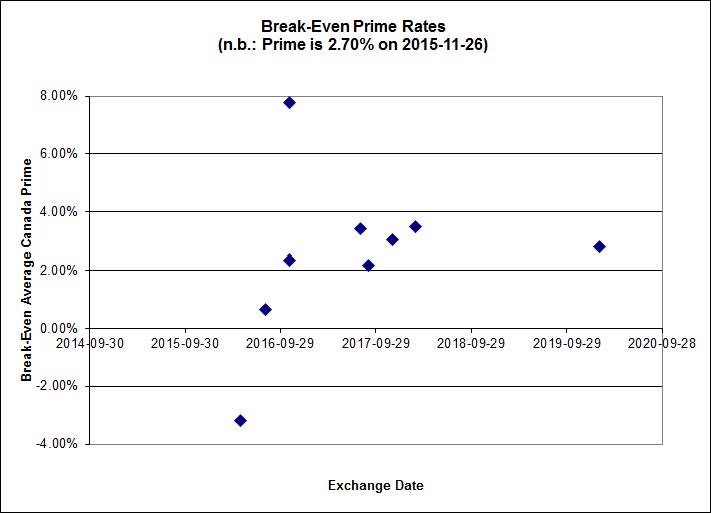

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.60%, with no outliers. There is one junk outlier below -1.50%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.26 % | 5.10 % | 34,483 | 17.75 | 1 | 1.0220 % | 1,826.3 |

| FixedFloater | 6.28 % | 5.52 % | 28,694 | 16.87 | 1 | 0.1324 % | 3,106.0 |

| Floater | 4.42 % | 4.49 % | 84,863 | 16.37 | 3 | -2.1965 % | 1,786.0 |

| OpRet | 4.86 % | 3.65 % | 30,197 | 0.75 | 1 | 0.0000 % | 2,740.8 |

| SplitShare | 4.76 % | 5.53 % | 131,161 | 4.33 | 5 | 0.0678 % | 3,221.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0678 % | 2,513.7 |

| Perpetual-Premium | 5.79 % | 0.28 % | 84,366 | 0.08 | 6 | -0.0264 % | 2,509.4 |

| Perpetual-Discount | 5.58 % | 5.64 % | 90,814 | 14.44 | 33 | -0.0213 % | 2,567.5 |

| FixedReset | 5.01 % | 4.62 % | 223,982 | 14.98 | 76 | -0.2294 % | 2,050.0 |

| Deemed-Retractible | 5.16 % | 5.28 % | 119,479 | 5.37 | 33 | 0.0150 % | 2,585.6 |

| FloatingReset | 2.61 % | 3.84 % | 60,715 | 5.74 | 10 | -0.2072 % | 2,179.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.C | Floater | -3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 10.60 Evaluated at bid price : 10.60 Bid-YTW : 4.51 % |

| BAM.PR.B | Floater | -3.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 10.66 Evaluated at bid price : 10.66 Bid-YTW : 4.49 % |

| TD.PF.D | FixedReset | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 4.46 % |

| BMO.PR.W | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 4.55 % |

| CU.PR.G | Perpetual-Discount | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.04 Evaluated at bid price : 20.04 Bid-YTW : 5.65 % |

| BAM.PF.E | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.97 % |

| CU.PR.C | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 4.42 % |

| TRP.PR.F | FloatingReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 13.75 Evaluated at bid price : 13.75 Bid-YTW : 4.24 % |

| BAM.PF.G | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.58 Evaluated at bid price : 20.58 Bid-YTW : 4.88 % |

| HSE.PR.G | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 21.04 Evaluated at bid price : 21.04 Bid-YTW : 5.33 % |

| FTS.PR.M | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 4.31 % |

| HSE.PR.E | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.69 Evaluated at bid price : 20.69 Bid-YTW : 5.44 % |

| IFC.PR.A | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.33 Bid-YTW : 8.87 % |

| RY.PR.M | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.41 % |

| TD.PF.A | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 18.55 Evaluated at bid price : 18.55 Bid-YTW : 4.52 % |

| VNR.PR.A | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 5.00 % |

| BMO.PR.M | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.36 Bid-YTW : 3.43 % |

| BAM.PR.E | Ratchet | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 25.00 Evaluated at bid price : 16.00 Bid-YTW : 5.10 % |

| W.PR.J | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 23.82 Evaluated at bid price : 24.07 Bid-YTW : 5.89 % |

| TRP.PR.D | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.67 % |

| GWO.PR.S | Deemed-Retractible | 1.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.71 Bid-YTW : 5.56 % |

| GWO.PR.Q | Deemed-Retractible | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.50 Bid-YTW : 6.17 % |

| BIP.PR.A | FixedReset | 1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 5.39 % |

| PWF.PR.T | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 21.99 Evaluated at bid price : 22.35 Bid-YTW : 3.86 % |

| BMO.PR.R | FloatingReset | 1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 3.43 % |

| MFC.PR.K | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.60 Bid-YTW : 6.54 % |

| TRP.PR.A | FixedReset | 3.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-26 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.59 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.R | FixedReset | 127,501 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.80 Bid-YTW : 3.57 % |

| GWO.PR.M | Deemed-Retractible | 115,545 | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-03-31 Maturity Price : 25.00 Evaluated at bid price : 25.46 Bid-YTW : 5.52 % |

| RY.PR.I | FixedReset | 110,855 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.35 Bid-YTW : 3.71 % |

| MFC.PR.L | FixedReset | 107,700 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.74 Bid-YTW : 6.52 % |

| IFC.PR.A | FixedReset | 101,049 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.33 Bid-YTW : 8.87 % |

| BNS.PR.Q | FixedReset | 95,910 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.38 Bid-YTW : 3.63 % |

| There were 53 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CU.PR.G | Perpetual-Discount | Quote: 20.04 – 20.62 Spot Rate : 0.5800 Average : 0.3990 YTW SCENARIO |

| MFC.PR.J | FixedReset | Quote: 21.32 – 21.74 Spot Rate : 0.4200 Average : 0.2664 YTW SCENARIO |

| W.PR.H | Perpetual-Discount | Quote: 23.80 – 24.25 Spot Rate : 0.4500 Average : 0.3164 YTW SCENARIO |

| GWO.PR.L | Deemed-Retractible | Quote: 25.08 – 25.44 Spot Rate : 0.3600 Average : 0.2358 YTW SCENARIO |

| SLF.PR.J | FloatingReset | Quote: 13.35 – 13.70 Spot Rate : 0.3500 Average : 0.2413 YTW SCENARIO |

| TRP.PR.H | FloatingReset | Quote: 11.03 – 11.35 Spot Rate : 0.3200 Average : 0.2198 YTW SCENARIO |