The proposed Plan of Arrangement involving DC.PR.C has been covered on PrefBlog in the posts DC.PR.C: Coercive Exchange Offer, DC.PR.C: Coercive Offer Attracts Wider Notice and DC.PR.C: Consider Exercising Dissent Rights To Defeat Management’s Coercive Plan.

This morning, Dundee blinked:

Dundee Corporation (TSX:DC.A)(TSX:DC.PR.C) is today announcing that it continues to seek a collaborative dialogue with its Series 4 Preferred Shareholders in respect of its proposed plan of arrangement. Since the mailing of its Circular, the Corporation has heard from a broader group of beneficial shareholders, including large institutional holders, who have expressed concerns.

The Corporation continues to engage in dialogue with known beneficial shareholders, in order to achieve a favourable result. However there can be no assurance that this dialogue will result in the support necessary for the proposed transaction to become effective. Accordingly, it is possible that, among other things, the proposed transaction terms may be amended or withdrawn.

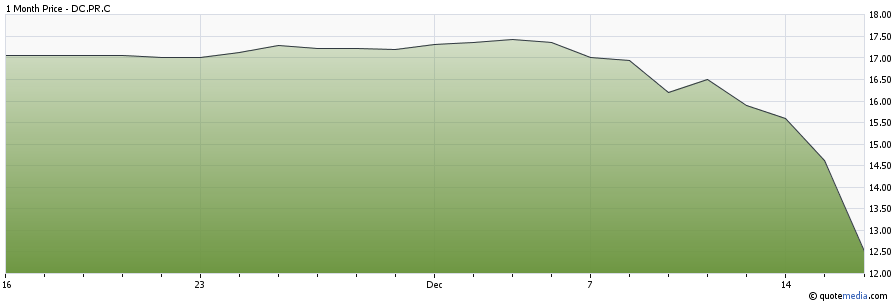

But the shares plunged anyway, down a stunning 14.50% (close / close) on heavy volume of 68,201 shares:

Click for Big

They’ve been going in one direction ever since the announcement:

Click for Big

I have no idea how sincere they are or with whom they are negotiating, but the “known beneficial shareholders” will, I’m sure, appreciate a bit of support to strengthen their hand. Don’t delay – vote “No” now and seriously consider exercising your right of dissent. The objective is to obtain a “Special Retraction Right”, as is standard when the maturities of Split Shares are extended, that will allow shareholders to opt to receive the original deal. That’s the main thing. But those who are interested in extending term should demand that the company renew and maintain a public credit rating from two major credit rating agencies – it was almost three years ago that the company cancelled this service which, while being of controversial intrinsic value, serves admirably to focus management’s and directors’ attention during bad times – which is particularly important in the fragmented, retail preferred share market.

I’d be curious about James’ and other reader’s interpretations, but when I’m looking at the price action it makes me think 2 things:

1 – Perhaps this is just the market demanding the same rate on the extended term that they currently demand on the two other, longer lived, issues (current yield in the 11-12% range – which we hit if you bought the close and decide to tender).

2 – Perhaps there is a real credit risk worry creeping up – can they afford to retire this issue should they fail to extend it? I haven’t done the fundamental work to assess this (love to hear from anyone that has).

Like I said – curious to see other opinions

There is a good discussion here: http://divestor.com/?p=6706&cpage=1#comment-103563

Based on the last quarter they have plenty of liquidity to handle the retraction of these preferred but who knows if the credit line has been cut since then.

Perhaps this is just the market demanding the same rate on the extended term that they currently demand on the two other, longer lived, issues

At a bit price of 13.60, the yield to a call at 17.64 in June 2016 is ridiculously high, of course. But yield to call in 2019, with a 6% coupon, is now 14.83%, which is actually a bit higher that what is available to perpetuity with DC.PR.B [11.85%] and DC.PR.D [13.33%].

So yes, it certainly looks as if the market is assuming that the company’s plan will pass as it is, and doesn’t like the implications of that assumption.

Perhaps there is a real credit risk worry creeping up – can they afford to retire this issue should they fail to extend it?

If they don’t have the cash, they can issue DC.A as full payment.

See SEDAR, “Dundee Corporation Jun 21 2006 14:01:56 ET Final short form prospectus – English -PDF 336 K”.

This would be a massive dilution, though. At its current price of 4.50, DC.A has a market cap of $250-million. DC.PR.C has a par value of $106-million and this gets boosted ~5% by the terms of conversion [provided the price of DC.A remains above $2].

It is my presumption that the company is desperately attempting to avoid conversion.

There is a good discussion here: http://divestor.com/?p=6706&cpage=1#comment-103563.

I like this link, this is a good link. Thank you.