There was good news on US inflation today:

The cost of living in the U.S. excluding food and fuel increased in January by the most in more than four years, reflecting broad-based gains that signal companies may be getting some pricing power.

The so-called core consumer-price measure climbed 0.3 percent, more than forecast and the most since August 2011, after a 0.2 percent gain the month before, a Labor Department report showed Friday in Washington. Total prices were little changed, depressed by the continued plunge in energy costs.

…

In the 12 months ended January, the overall consumer price measure increased 1.4 percent after a 0.7 percent increase in the prior period.The core index advanced 2.2 percent from a year earlier, the most since June 2012.

But, of course, there’s always worry:

The U.S. economy may be saddled with a “deflationary bias” after the last recession that makes it harder for the Federal Reserve to achieve its 2 percent inflation goal, according to research published this month by the central bank.

Economists Timothy Hills, Taisuke Nakata and Sebastian Schmidt argue that the bias stems from a recognition by companies that the Fed has limited ability to spur the economy when interest rates are low.

That in turn prompts firms to reduce expectations of future costs, affecting what they decide to charge for their products and services.

“Our result provides a cautionary tale for policy makers aiming to raise inflation from currently low levels,” the economists wrote in a paper and an accompanying note. “Achieving the inflation target may be more difficult now than before the Great Recession.”

…

To try to offset the deflationary bias, the authors suggest the Fed should place more emphasis on lifting inflation than on stabilizing output. That would imply allowing unemployment to fall below its long-run natural rate.The central bank could also raise its inflation target from 2 percent to help increase expectations of future price increases, the researchers said.

At the core of the paper is an assumption that the zero lower bound on interest rates constrains the Fed’s ability to promote faster economic growth and higher inflation. It is that constraint — and the likelihood that the central bank will encounter it more frequently in the future — that prompts companies to lower their inflation expectations.

However, even if the Fed pushed rates below zero to a negative half percentage point, the model finds that inflation would still fall short of the central bank’s goal, albeit not by as much as otherwise.

Negative rates are a “dangerous experiment,” according to Huw van Steenis, an analyst at Morgan Stanley who warns in a recent report that they will erode banks’ profitability. The push below zero signals “policy exhaustion,” says Chris Xiao at Merrill Lynch. The moves in Switzerland and the euro zone have so far failed to boost growth, notes Christopher Swann, a strategist at UBS Wealth Management.

Some observers worry about possible dangers to international trade. “Negative interest rates represent another escalation of the so-called currency wars,” warns Mr. Mather of Pimco, who is concerned that some central banks are using subzero rates as a way to devalue their currencies and boost exports.

For his part, Mr. de Verteuil of CIBC cautions that subzero rates could lead to a stampede out of money market funds. “We aren’t sure whether individual investors will be prepared to pay to own a money market fund – but we highly doubt it,” he writes. Since those funds play an important role in buying companies’ short-term debt, the result could be a severe crimping of lending to the corporate sector.

Meanwhile, Canada’s economy is still in the doldrums:

The OECD now projects economic growth of just 1.4 per cent in Canada this year as the oil shock wreaks havoc on parts of the country, with a ripple effect outward. That’s well shy of its earlier call in November for 2 per cent.

…

While that downgrade is the steepest among the G7, it would still put Canada ahead of Germany, France, Italy and Japan.However, Canada would still trail the forecast showings of Britain and the United States, at 2.1 per cent and 2 per cent, respectively.

While growth of 1.4 per cent is lame, it’s not as bad as some other economists project. Those other forecasts tend to be in the area of 1 per cent or even worse.

And there’s a contra-indicator to the idea that the bright lights of the new generation will bail us out:

Perhaps millennials should just stick to investing in index funds—or at least the exchange-traded funds that their robo-advisers put them in.

According to research from online brokerage TD Ameritrade Holding Corporation, one particularly risky ETF is attracting the millennial demographic far more than other age groups. In fact, it was one of the top 10 stocks traded by millennials in 2015.

The VelocityShares Daily 3x Long Crude ETN (UWTI) isn’t just a risky product; it is arguably the most dangerous ETF on planet Earth. First off, it is triple leveraged, which makes it extremely volatile—nearly 10 times more jumpy than the S&P 500 Index and more than double any of the other stocks on the list. The leverage amount in UWTI also gets reset each day, which can make for some epic days when oil does go up but over time causes returns to corrode.

As aficionados of Sequence of Returns risk will remember, these leveraged funds have an implicit policy to sell low and buy high … how could they not lose money?

Amidst all this gloom, let’s focus on a bright spot: supply management is losing its allure:

In a policy about-face, senior Quebec bureaucrat Florent Gagné is urging the province to end strict maple-syrup quotas and let producers sell what they want, to who they want.

“It’s hard to understand why in an international race that we impose constraints [on our producers] that the other players don’t,” Mr. Gagné lamented as he released a controversial report on the challenges facing the maple-syrup industry.

…

Quebec has been called the Saudi Arabia of maple syrup, producing more than 60 per cent of the global output of the sweet and sticky stuff – roughly 100 million pounds a year. A provincially sanctioned cartel was created in the early 2000s, run by the Federation of Quebec Maple Syrup Producers and blessed by government. The federation imposes production quotas, stockpiles surplus syrup and sets the price paid to producers.But the province is bleeding market share to New England states, Ontario and New Brunswick, where producers are free to make and sell whatever they want. U.S. producers, in particular, have been ramping up output at the expense of Quebec.

Dream Office REIT, managed by Dream Unlimited, proud issuer of DRM.PR.A, is biting the bullet:

Battered by tumbling investor confidence in Alberta companies, and hamstrung by heavy cash outlays for the foreseeable future, Dream Office REIT has unveiled a stunning strategic shift.

Late Thursday, the real estate investment trust, which is one of Canada’s largest office tower owners, announced sweeping plans to slash its distribution by one-third, top up its credit facility to $800-million and unload at least $1.2-billion worth of properties over the next three years.

The ambitious strategy is something investors and analysts have been looking for. Partly because 20 per cent of Dream’s portfolio is in Alberta, spooked investors had sent its units tumbling 60 per cent from their peak in 2012. The REIT must also spend hundreds of millions to upgrade and maintain its buildings and pay its distribution. Cash was getting so tight that it looked likely Dream would need to borrow in order to fund its monthly payout next year. Slashing the distribution saves roughly $80-million annually.

It was a good solid day for the Canadian preferred share market, with PerpetualDiscounts up 43bp, FixedResets winning 44bp and DeemedRetractibles gaining 27bp. Floating Rate issues did very well. The Performance Highlights table continues to show lots of churn. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

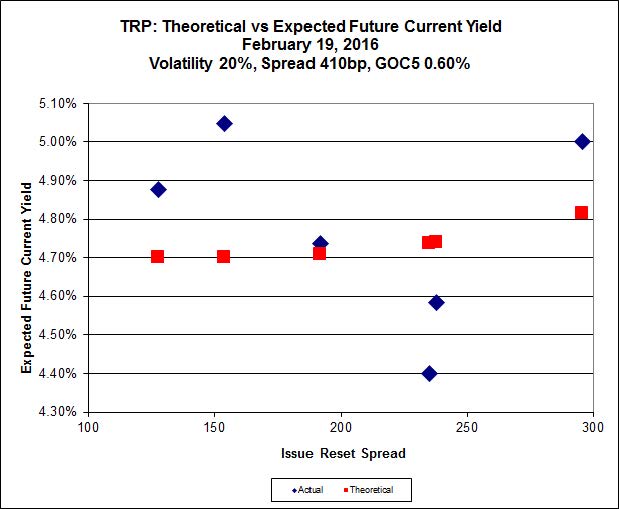

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 16.76 to be $1.19 rich, while TRP.PR.C, resetting 2021-1-30 at +154, is $0.78 cheap at its bid price of 10.60.

Click for Big

This analysis includes the new issue with a deemed price of 25.00.

Most expensive is the new issue, resetting at +497bp on 2021-6-19, deemed at 25.00 to be 1.23 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.00 to be 1.39 cheap.

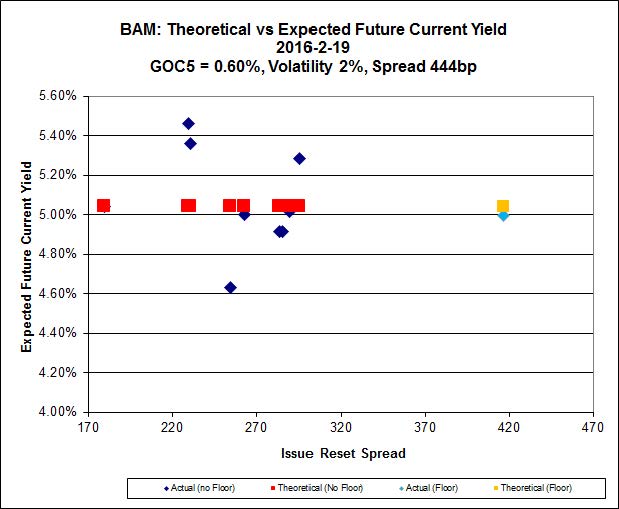

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.28 to be $1.10 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.00 and appears to be $1.38 rich.

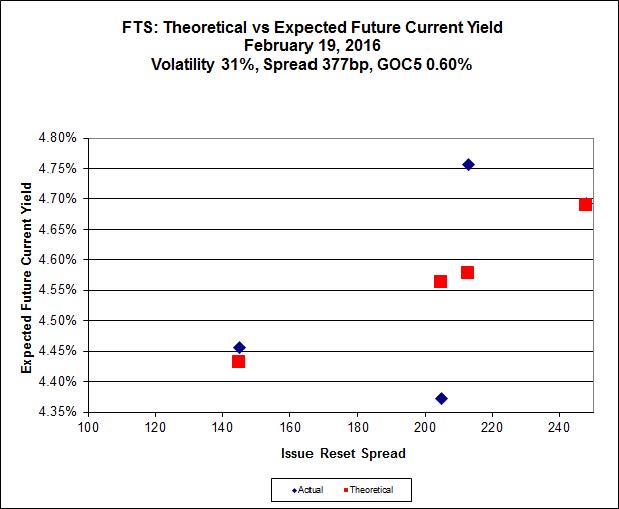

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 15.15, looks $0.63 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 14.35 and is $0.56 cheap.

Click for Big

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.65%, with two outliers above 0.00%. Note that the range of the y-axis has changed. There are two junk outliers above 0.00% and one below -2.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.33 % | 6.49 % | 15,250 | 16.05 | 1 | 6.2762 % | 1,463.2 |

| FixedFloater | 7.82 % | 6.84 % | 23,928 | 15.36 | 1 | 0.8299 % | 2,542.7 |

| Floater | 4.96 % | 5.12 % | 79,668 | 15.23 | 4 | 4.4694 % | 1,545.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1035 % | 2,750.0 |

| SplitShare | 4.85 % | 5.67 % | 74,429 | 2.70 | 6 | 0.1035 % | 3,218.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1035 % | 2,510.8 |

| Perpetual-Premium | 5.83 % | 5.79 % | 83,155 | 13.88 | 6 | 0.2396 % | 2,529.8 |

| Perpetual-Discount | 5.77 % | 5.80 % | 98,660 | 14.16 | 33 | 0.4296 % | 2,507.3 |

| FixedReset | 5.70 % | 5.10 % | 206,438 | 14.47 | 84 | 0.4363 % | 1,781.5 |

| Deemed-Retractible | 5.32 % | 5.77 % | 122,564 | 6.88 | 34 | 0.2709 % | 2,539.7 |

| FloatingReset | 3.11 % | 5.20 % | 50,076 | 5.50 | 16 | -0.0653 % | 1,965.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| RY.PR.K | FloatingReset | -2.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.81 Bid-YTW : 4.80 % |

| BNS.PR.C | FloatingReset | -2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.02 Bid-YTW : 5.44 % |

| HSE.PR.E | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 7.11 % |

| TD.PF.E | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 17.86 Evaluated at bid price : 17.86 Bid-YTW : 4.98 % |

| HSE.PR.G | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 15.29 Evaluated at bid price : 15.29 Bid-YTW : 7.09 % |

| VNR.PR.A | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 5.36 % |

| NA.PR.Q | FixedReset | -1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.40 Bid-YTW : 5.36 % |

| TRP.PR.C | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 10.60 Evaluated at bid price : 10.60 Bid-YTW : 5.16 % |

| TD.PF.C | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.72 Evaluated at bid price : 16.72 Bid-YTW : 4.57 % |

| CM.PR.P | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.37 Evaluated at bid price : 16.37 Bid-YTW : 4.68 % |

| GWO.PR.Q | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.79 Bid-YTW : 6.62 % |

| PWF.PR.F | Perpetual-Discount | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 22.43 Evaluated at bid price : 22.69 Bid-YTW : 5.83 % |

| GWO.PR.H | Deemed-Retractible | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.63 Bid-YTW : 7.05 % |

| FTS.PR.J | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 5.70 % |

| NA.PR.S | FixedReset | 1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.52 Evaluated at bid price : 16.52 Bid-YTW : 4.85 % |

| BAM.PR.T | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 13.58 Evaluated at bid price : 13.58 Bid-YTW : 5.63 % |

| BAM.PR.R | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 13.28 Evaluated at bid price : 13.28 Bid-YTW : 5.62 % |

| MFC.PR.H | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.00 Bid-YTW : 7.77 % |

| TRP.PR.H | FloatingReset | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 8.91 Evaluated at bid price : 8.91 Bid-YTW : 4.89 % |

| IAG.PR.G | FixedReset | 1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.10 Bid-YTW : 8.93 % |

| MFC.PR.F | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.69 Bid-YTW : 10.98 % |

| BNS.PR.Y | FixedReset | 1.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.15 Bid-YTW : 6.62 % |

| TD.PF.D | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 18.04 Evaluated at bid price : 18.04 Bid-YTW : 4.80 % |

| RY.PR.M | FixedReset | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.67 % |

| MFC.PR.J | FixedReset | 1.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.58 Bid-YTW : 9.18 % |

| MFC.PR.G | FixedReset | 1.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.00 Bid-YTW : 9.03 % |

| PWF.PR.P | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 4.75 % |

| BMO.PR.W | FixedReset | 1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.64 Evaluated at bid price : 16.64 Bid-YTW : 4.54 % |

| RY.PR.F | Deemed-Retractible | 1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.68 Bid-YTW : 5.52 % |

| FTS.PR.G | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 14.35 Evaluated at bid price : 14.35 Bid-YTW : 5.04 % |

| FTS.PR.H | FixedReset | 2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.68 % |

| BMO.PR.T | FixedReset | 2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.48 % |

| BNS.PR.Z | FixedReset | 2.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.82 Bid-YTW : 7.28 % |

| FTS.PR.K | FixedReset | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 15.15 Evaluated at bid price : 15.15 Bid-YTW : 4.74 % |

| RY.PR.J | FixedReset | 2.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 4.71 % |

| FTS.PR.M | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.41 Evaluated at bid price : 16.41 Bid-YTW : 5.03 % |

| CIU.PR.C | FixedReset | 2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 10.01 Evaluated at bid price : 10.01 Bid-YTW : 4.91 % |

| SLF.PR.H | FixedReset | 2.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.11 Bid-YTW : 9.66 % |

| BAM.PR.C | Floater | 4.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 9.20 Evaluated at bid price : 9.20 Bid-YTW : 5.21 % |

| BAM.PR.B | Floater | 4.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 9.33 Evaluated at bid price : 9.33 Bid-YTW : 5.13 % |

| TRP.PR.I | FloatingReset | 4.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 4.44 % |

| BAM.PR.E | Ratchet | 6.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 25.00 Evaluated at bid price : 12.70 Bid-YTW : 6.49 % |

| BAM.PR.K | Floater | 9.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 9.35 Evaluated at bid price : 9.35 Bid-YTW : 5.12 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.P | FixedReset | 117,700 | Scotia crossed blocks of 62,000 and 50,000, both at 16.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.37 Evaluated at bid price : 16.37 Bid-YTW : 4.68 % |

| CU.PR.I | FixedReset | 103,258 | Scotia crossed 100,000 at 25.08. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 23.20 Evaluated at bid price : 25.08 Bid-YTW : 4.38 % |

| BMO.PR.W | FixedReset | 70,540 | Scotia crossed 40,000 and 25,000, both at 16.51. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 16.64 Evaluated at bid price : 16.64 Bid-YTW : 4.54 % |

| SLF.PR.I | FixedReset | 68,192 | TD crossed 60,000 at 16.90. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.76 Bid-YTW : 8.99 % |

| TD.PF.G | FixedReset | 43,914 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 23.28 Evaluated at bid price : 25.41 Bid-YTW : 5.18 % |

| BAM.PF.H | FixedReset | 39,611 | Scotia crossed 30,000 at 25.02. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-02-19 Maturity Price : 23.18 Evaluated at bid price : 25.02 Bid-YTW : 4.96 % |

| There were 25 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CM.PR.Q | FixedReset | Quote: 18.40 – 19.79 Spot Rate : 1.3900 Average : 0.8143 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 13.00 – 13.80 Spot Rate : 0.8000 Average : 0.5271 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 16.76 – 17.65 Spot Rate : 0.8900 Average : 0.6229 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 11.90 – 12.65 Spot Rate : 0.7500 Average : 0.5154 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 17.86 – 18.80 Spot Rate : 0.9400 Average : 0.7083 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 12.15 – 12.89 Spot Rate : 0.7400 Average : 0.5120 YTW SCENARIO |