Royal Bank of Canada has announced:

a domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BM.

Royal Bank of Canada will issue 12 million Preferred Shares Series BM priced at $25 per share to raise gross proceeds of $300 million. The bank has granted the Underwriters an option, exercisable in whole or in part, to purchase up to an additional 2 million Preferred Shares Series BM at the same offering price.

The Preferred Shares Series BM will yield 5.50 per cent annually, payable quarterly, as and when declared by the Board of Directors of Royal Bank of Canada, for the initial period ending August 24, 2021. Thereafter, the dividend rate will reset every five years at a rate equal to 4.80 per cent over the 5-year Government of Canada bond yield.

Subject to regulatory approval, on or after August 24, 2021, the bank may redeem the Preferred Shares Series BM in whole or in part at par. Holders of Preferred Shares Series BM will, subject to certain conditions, have the right to convert all or any part of their shares to Non-Cumulative Floating Rate Preferred Shares Series BN on August 24, 2021 and on August 24 every five years thereafter.

Holders of the Preferred Shares Series BN will be entitled to receive a non-cumulative quarterly floating dividend, as and when declared by the Board of Directors of Royal Bank of Canada, at a rate equal to the 3-month Government of Canada Treasury Bill yield plus 4.80 per cent. Holders of Preferred Shares Series BN will, subject to certain conditions, have the right to convert all or any part of their shares to Preferred Shares Series BM on August 24, 2026 and on August 24 every five years thereafter.

The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is March 7, 2016.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BM, the size of the offering has been increased to 30 million shares. The gross proceeds of the offering will now be $750 million. The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is March 7, 2016.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

$750-million! Wow! That’s bigger than TD.PF.G, a shrimpy little issue of only $700-million.

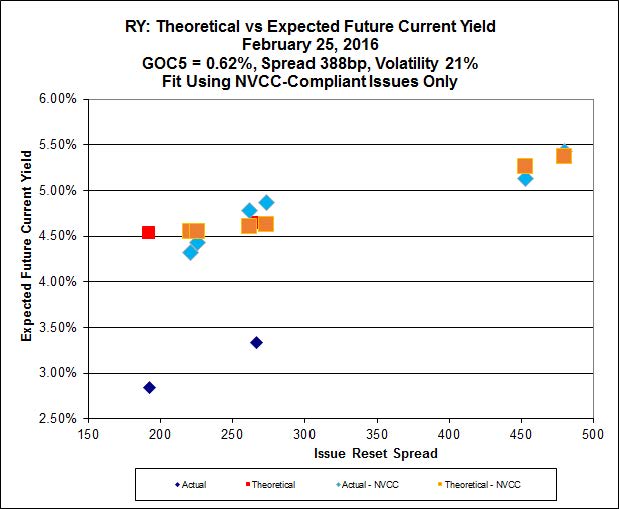

Implied Volatility analysis yields the following chart:

Click for Big

Interpretation of this chart using the standard assumptions that everything will remain the same forever leads us to believe that the new issue is reasonably priced – fair value is $25.22 when compared to the indicated theoretical values.

However, the standard assumptions are even more shaky than they usually are. Some will say that the derived value of Implied Volatility, at 21%, is far too high and may be expected to decline in the future. This will cause the theoretical curve to flatten, which implies that the higher-spread issues will outperform the lower spread issues. Some will say, however, that the fundamental assumption of non-directionality in the Black-Scholes theory is wrong; that spreads in general are far too high, will narrow, and therefore the lower-spread issues will outperform the higher-spread issues. Some, like myself, will say that both criticisms are correct but that on balance the lower-spread issues are preferable. If, for instance, you plug in a 250bp spread and 10% Implied Volatility – numbers I would consider more reflective of a normal market – you find that the four lower spread issues increase in price by over 40%, compared to the higher-spread issues, which may well go substantially above the $25 call price, but not 40% worth. Mind you, the critical part of the above analysis is “normal” … i.e., with five year Canadas yielding more than inflation and that’s just for starters! There will be some who believe that current conditions represent the new normal; these players will probably prefer the higher-spread issues.

The Break Even Rate Shock for this issue is a mere 1bp. What a difference a few years make!

The Preferred Shares Series BM will yield 5.50 per cent annually, payable quarterly, as and when declared by the Board of Directors of Royal Bank of Canada

To this newbie – that sounds very rich. Yes? The convertible prefs look cheap and go against the grain.

To this newbie – that sounds very rich.

Well … sort of. See the penultimate paragraph.