Bank of Montreal has announced (although not yet on their website):

it has closed its domestic public offering of Non-Cumulative 5-Year Rate Reset Class B Preferred Shares Series 38 (the “Preferred Shares Series 38”). The offering was underwritten on a bought deal basis by a syndicate of underwriters led by BMO Capital Markets. Bank of Montreal issued 24 million Preferred Shares Series 38 at a price of $25 per share to raise gross proceeds of $600 million.

The Preferred Shares Series 38 were issued under a prospectus supplement dated October 14, 2016, to the Bank’s short form base shelf prospectus dated April 13, 2016. Such shares will commence trading on the Toronto Stock Exchange today under the ticker symbol BMO.PR.B.

BMO.PR.B is a FixedReset, 4.85%+406, NVCC-compliant issue announced October 14. It will be tracked by HIMIPref™ and assigned to the FixedResets subindex.

The issue traded a staggering 4,330,078 shares in a range of 25.69-82 before closing at 25.69-70, 27×87. The volume ranks it sixth in my database (over 1-million records dating back to 1993-12-31), just behind NVA.PR.A (Nova Energy), which traded 4.4-million shares on 1997-3-24 (shortly after issue) and the highest single-issue daily volume since GWO.PR.E, which traded 5.3-million shares on 1999-3-18 (also shortly after issue). So, this is the highest single-issue daily volume so far this century.

Vital statistics are:

| BMO.PR.B | FixedReset | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 4.29 % |

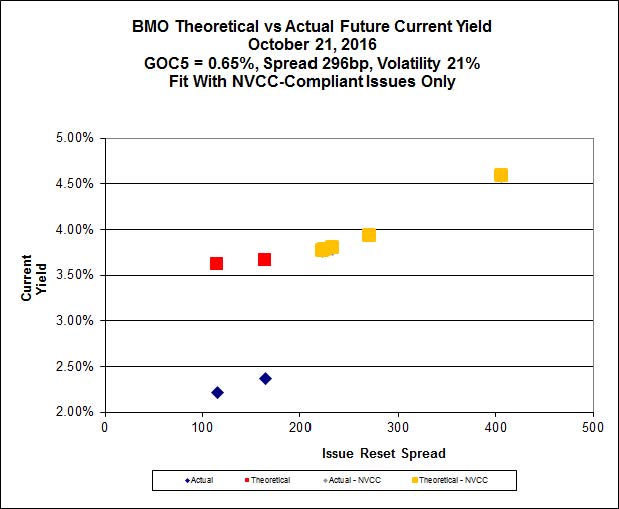

As has often been the case lately, Implied Volatility analysis results in a chart that can be interpreted in two ways:

Click for Big

The curve fits very well, with a very high Implied Volatility. If one takes the view that GOC-5 rates will increase dramatically over the next few years, the low-spread, low-price issues will be preferred (as this will lead to capital gains on these issues, but not the new one since the call provision caps the expected price); if one takes the view that the current GOC yield curve represents the new normal, then the new issue will be preferred (as one will then expect Implied Volatility to decrease, flattening the fitted curve, resulting in capital losses for the low-spread issues).

How many of these new bank issues will it take for the banks to understand they are getting ripped off by the underwirters. Again as with the previous bank issues of the last 6 months, none were available from discount trading platform (TD Waterhouse, BMOligne d’action or RYdirect) within minutes the new issue was announced. I could only get 1,000 begging my personal broker at Scotia. Her answer was that they did not have much since they were not a lead underwriter on that issue.

… Then again with this new issue, 4 Million shares+ (and still on a much smaller issue than the formers from RY, TD & BNS) get traded on their retail opening day. Dear issuers, open your eyes! In addition to the $+0.75 per share you pay to your friends underwriters (IIRC, the issuer only gets $24 per share with the remaining $1 being paid to the underwriters of the issue as fee and in costs for the issuance), the very same underwriters or their friends make an extra quick capital gain of about $0.70 per share in one day on the very day they are issued by keeping them for or between themselves and making that quick profit on the retail market on the very first day of their issuance. This also allows to justify the existence and jobs of the traditional brokers whose only tangible advantage nowadays is to be able to tell their clients: “Well I was able to get you some of these new shares while you could not do it yourself through retail online brokers… Nah! Nah! Nah!

Wake up big bank issuer! You are getting framed by your brothers of the underwriting divisions who convince you to issue at low pricing what Mr. Market is prepared to buy for far more than what is proposed to you!!!

Retail is again the loser here. By having new issues issued at a lower price than their market value it pressures down the market value of the existing older issues.

Anyhow, let’s cash the quick profit on the 1000 I could get now and stop whinning…