Who wants to buy some European bank shares? There might be some on sale soon!

European banks have a capital shortfall of as much as 767 billion euros ($1 trillion) before the European Central Bank’s probe into the financial health of the region’s lenders, according to a study.

French banks show the biggest gap of 285 billion euros, followed by German lenders with as much as 199 billion euros, Sascha Steffen of the European School of Management and Technology in Berlin and Viral Acharya at New York University said in their study dated Jan. 15. The figures assume a benchmark capital ratio for other book measures of leverage of 7 percent, they wrote.

…

The authors see particularly high risks among German state-owned banks, or Landesbanken. “Germany has many government-owned institutions that may require capital issuances and/or bail-ins,” they wrote.Spanish banks have a shortfall of 92 billion euros, while Italian banks lack 45 billion euros, the study showed.

Watch out for those rising interest rates:

Royal Bank of Canada, the country’s largest mortgage lender, has quietly cut some of its mortgage rates this weekend. The move appears to be part of a broader dip in rates, although economists generally still expect an increase in 2014.

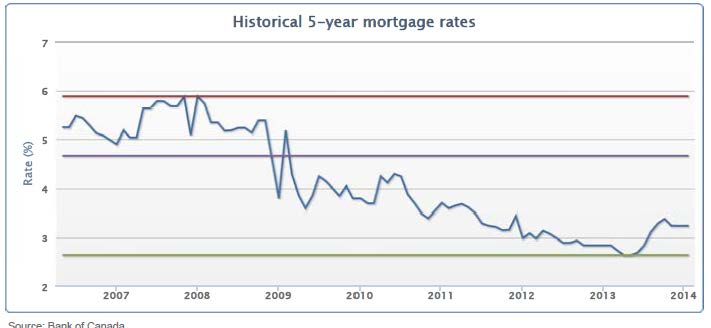

Five-year fixed mortgage rates rose industry-wide for much of 2013, from their low of 2.64 per cent in April to their high of 3.39 per cent in September, according to Alyssa Richard, the chief executive officer of RateHub.ca. They edged down a bit later in the fall but had generally been steady at around 3.25 per cent since then.

RBC is now cutting its two-, three-, four– and five-year fixed mortgage rates each by 10 basis points. In an emailed statement, the bank said that some mortgage lenders have recently been pricing at lower rates, prompting it to move.

Royal Bank is often a price leader when it comes to mortgages, and other big banks frequently follow suit after it changes its prices. Its five-year fixed mortgage rate is now 3.69 per cent.

The numbers in that story don’t exactly add up all that well, and the Bank of Canada insists that a five year mortgage now runs at 5.14%. Whatever. The reason for the discrepancy, according to ratehub.ca, is:

While the Bank of Canada has the most comprehensive data set, with the high prevelance of mortgage rate discounting, it is not the most accurate. The Canadian Association of Accredited Mortgage Professionals estimates that the average discount applied to a 5 year mortgage rate in 2010 was 1.42%. To source the discounted rates, we have combined our proprietary data supplemented with discount brokerage data from 2006-2010.

They have a picture:

Click for Big

Banks do this ridiculous posted-rate / discounted-rate thing because when you close out a mortgage early, you have to buy it back according to its posted rate, which is much more expensive than buying it back at the discounted rate. The US system, where the standard is a thirty year term with the mortgagee able to pay off at any time at par, is much better for home-owners – but of course, in the US there’s competition.

It was a mildly positive day for the Canadian preferred share market, with PerpetualDiscounts up 9bp, FixedResets winning 11bp and DeemedRetractibles gaining 6bp. Floaters fared poorly. The Performance Highlights table is notable for it’s heavy concentration of BAM issues … will you, won’t you, will you, won’t you, will you join the dance? Volume was above average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.2011 % | 2,459.4 |

| FixedFloater | 4.45 % | 3.69 % | 32,782 | 18.04 | 1 | -0.2801 % | 3,815.7 |

| Floater | 3.04 % | 3.06 % | 71,848 | 19.58 | 3 | -1.2011 % | 2,655.5 |

| OpRet | 4.62 % | 0.86 % | 75,237 | 0.19 | 3 | -0.0256 % | 2,674.9 |

| SplitShare | 4.84 % | 4.75 % | 61,645 | 4.41 | 5 | 0.0000 % | 3,028.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0256 % | 2,445.9 |

| Perpetual-Premium | 5.63 % | 3.93 % | 124,929 | 0.12 | 13 | 0.1611 % | 2,323.9 |

| Perpetual-Discount | 5.65 % | 5.69 % | 162,483 | 14.38 | 25 | 0.0916 % | 2,349.6 |

| FixedReset | 4.93 % | 3.61 % | 226,299 | 3.96 | 83 | 0.1105 % | 2,493.4 |

| Deemed-Retractible | 5.16 % | 4.52 % | 169,636 | 2.15 | 42 | 0.0600 % | 2,396.4 |

| FloatingReset | 2.60 % | 2.32 % | 258,965 | 4.31 | 5 | -0.0079 % | 2,475.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.C | Floater | -1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 3.06 % |

| BAM.PR.K | Floater | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 17.22 Evaluated at bid price : 17.22 Bid-YTW : 3.07 % |

| BAM.PF.B | FixedReset | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 23.16 Evaluated at bid price : 25.03 Bid-YTW : 4.18 % |

| BAM.PF.C | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 6.12 % |

| BAM.PR.X | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 21.70 Evaluated at bid price : 21.97 Bid-YTW : 4.19 % |

| PWF.PR.P | FixedReset | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 22.96 Evaluated at bid price : 23.29 Bid-YTW : 3.61 % |

| IAG.PR.G | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-06-30 Maturity Price : 25.00 Evaluated at bid price : 26.04 Bid-YTW : 3.11 % |

| TRP.PR.C | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 22.08 Evaluated at bid price : 22.30 Bid-YTW : 3.72 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.E | FixedReset | 490,441 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-01-20 Maturity Price : 23.07 Evaluated at bid price : 24.86 Bid-YTW : 4.00 % |

| BNS.PR.Q | FixedReset | 93,400 | RBC crossed blocks of 25,000 and 28,000, both at 25.10. Scotia crossed 37,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 3.46 % |

| BNS.PR.B | FloatingReset | 88,299 | RBC Crossed 35,100 at 25.10; TD crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Call Maturity Date : 2018-10-25 Maturity Price : 25.00 Evaluated at bid price : 25.09 Bid-YTW : 2.38 % |

| TD.PR.C | FixedReset | 56,917 | Called for redemption. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.98 Bid-YTW : 4.46 % |

| BNS.PR.O | Deemed-Retractible | 52,400 | RBC crossed 50,000 at 26.09. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-04-28 Maturity Price : 25.75 Evaluated at bid price : 26.05 Bid-YTW : 0.42 % |

| IGM.PR.B | Perpetual-Premium | 35,269 | Scotia crossed 30,000 at 25.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2018-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.38 Bid-YTW : 5.55 % |

| There were 41 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.L | Deemed-Retractible | Quote: 24.94 – 25.39 Spot Rate : 0.4500 Average : 0.3090 YTW SCENARIO |

| BNA.PR.D | SplitShare | Quote: 25.36 – 25.64 Spot Rate : 0.2800 Average : 0.1753 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 20.87 – 21.37 Spot Rate : 0.5000 Average : 0.4088 YTW SCENARIO |

| CU.PR.F | Perpetual-Discount | Quote: 21.27 – 21.53 Spot Rate : 0.2600 Average : 0.1793 YTW SCENARIO |

| CGI.PR.D | SplitShare | Quote: 24.81 – 25.05 Spot Rate : 0.2400 Average : 0.1677 YTW SCENARIO |

| TD.PR.P | Deemed-Retractible | Quote: 25.70 – 25.98 Spot Rate : 0.2800 Average : 0.2113 YTW SCENARIO |

I see RBC is issuing a new Basel III-compliant 5-Year Rate Reset Preferred Shares Series AZ. The spread is 221bp.

“Royal Bank of Canada (RY on TSX and NYSE) today announced an inaugural Basel III-compliant domestic public offering of $200 million of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series AZ. ”

http://www.newswire.ca/en/story/1292375/royal-bank-of-canada-announces-preferred-share-issue

ltr