With all the idiotically mandated bonus deferrals, we’re going to see a lot more of this:

Bank of America Corp. maliciously fired a distressed-debt banker to deprive her of a bonus, a Hong Kong judge ruled, awarding Sunny Tadjudin $500,000 after a seven-year legal battle.

Tadjudin’s manager, John Liptak, was determined to fire her despite her improvement in a performance plan, and his malice can be attributed to the bank, High Court Judge Anthony To said in a 141-page ruling issued yesterday. Still, Tadjudin will receive only a fraction of the amount she requested.

Tadjudin, 51, who worked for the bank’s Asian distressed-debt trading group, had sought bonuses totaling $3.7 million after being fired in 2007 following what she said were irrational and arbitrary performance ratings. To ruled against her claims for higher 2005 and 2006 bonuses than she received.

In Canada, of course, we have the example of Scotiabank and David Berry. There is some speculation he will get his due:

How much, if any, of Bank of Nova Scotia’s $55 million legal charge is related to Dave Berry’s $100 million law suit?

Two days back the Bank of Nova Scotia surprised the markets with news that it would be taking a series of charges in the fourth quarter of its recently completed fiscal year. In all there were $451 million of pre-tax charges, which converts to $341 million on an after tax-basis.

One item has attracted particular attention: “Thirdly, the Bank expects to record a legal charge of approximately $55 million related to certain ongoing legal claims in multiple business lines.”

Could that item be related to the $100 million lawsuit filed by David Berry, the bank’s former head of preferred share trading who was terminated more than nine years ago? Berry’s lawsuit – which is slated to trial next year – alleges wrongful dismissal.

The suit also alleges that his termination – at the time he was the highest paid employee at the bank earning a percentage of the profits made by his group – “was the result of blame-shifting, corporate self interest or greed on the part of Scotia Capital and its inadequate internal compliance, training and education procedures.”

It certainly would be nice if those sleaze-bags and ignoramuses at Scotia did the right thing … even ten years later and after umpteen hearings.

The Greek Tragedy is being revived, but there is much less excitement this time:

Investor reaction to the Greek parliament’s failure to pick a president traced the familiar north-south divide. Greek stocks and bonds plunged and markets were buffeted in Italy, Portugal and Spain, while funds flowed into Germany, Europe’s biggest economy and hard-money bastion.

Yet look closer and Italy, the euro zone’s second most-indebted country after Greece, is nowhere near a fiscal calamity. Ten-year borrowing costs are hovering around 2 percent, compared to over 7 percent at the height of the crisis. Bond holders are charging Italy 144 basis points more than Germany to borrow, a far cry from 553 basis points in November 2011.

…

There were echoes of 2012 in Europe’s political reaction. Back then, German Finance Minister Wolfgang Schaeuble said “we cannot force Greece” to press on with the budget cuts needed to stay in the euro zone, while a German then on the ECB board, Joerg Asmussen, said there was “no alternative” to austerity.Schaeuble reprised that line in a statement yesterday, saying that tough reforms in Greece were bearing fruit and “they are without any alternative.” Germany will support Greece on its path of reform, he said, though “if Greece chooses a different way, it will become difficult.”

…

When Greece hurtled toward bankruptcy in early 2010, the European Union had no way of helping countries in need. When Greece toyed with quitting the euro in late 2011, and held a stalemated election in May 2012 before Samaras put together a unity government after a second election six weeks later, it had only a temporary bailout fund.Now, it has a full-time aid fund in the 500 billion-euro European Stability Mechanism and a central bank tiptoeing — amid opposition from Germany — toward large-scale bond purchases. It also boasts success stories: Ireland, Portugal and Spain have been weaned off financial aid.

The risk is less a splintering of the 18-nation euro zone – – it will become 19 on Jan. 1 when Lithuania joins — than a protracted phase of subpar economic growth that leaves a generation scarred by unemployment and tempted by political extremism, especially in the south.

The trend in robo-advising is getting a boost:

But Wealthsimple, a Toronto startup, is taking the concept [of on-line investing] in precisely the opposite direction. It’s using the Internet as a way to offer up investing that’s not only cheap to manage, but algorithmically steady, safe, and predictable.

…

The ten-person firm’s idea is to use technology both to cut out the costs of offering traditional investment advice, and to be more agile in automatically managing portfolios. New customers fill out a questionnaire, and are then paired with a certified investment advisor, who works remotely and is available by text, phone, or video chat. (The firm’s one concession to startup trendiness is its insistence on calling its advisors “wealth concierges.”)

The operation is, as far as I can tell, an ETF allocator:

We charge an annual management fee of 0.35-0.50% of assets depending on your account balance. That’s approximately ⅓ the cost of typical advisors in Canada. The only other fee you incur is the very low fee embedded in the investment products in your portfolio (averages is 0.25%) and currency conversion. We have negotiated preferred pricing on both ETF prices and currency of more than 50% and passed along all of those savings to our clients.

Wealthsimple’s management fee covers transactions, rebalancing, advice, and account administration.

Well, it’s bound to come at some point – particularly if trailer fees get banned – but it remains to be seen whether there’s a mass-market comprised of people who don’t mind actually cutting a cheque for their advice. I admit to being a little suspicious of their market timing aspirations:

While we don’t believe in picking stocks or timing the market, we do believe in a thoughtful approach to risks. In the context of the current market environment, there are two primary risks we consider:

•Interest rates

•Market volatilityFor the past 30 years, bond investors have been well rewarded as interest rates steadily declined to historic lows (when interest rates go down, bond prices go up). Looking forward, interest rates cannot get much lower. But what will they do?

Interest rate uncertainty carries lots of risk for bond investors. As a result, we use alternatives to bonds wherever possible. For example, we use real estate and dividend stocks which generate income like bonds, but are not as linked to interest rates. We also use a real estate product that is specifically designed to minimize the risk of interest rate uncertainty.

Which brings to mind the question of whether BRICS is actually an asset class or not:

While Chinese and Indian benchmark equity indexes have surged an average 40 percent this year, Russian and Brazilian gauges posted a mean drop of 4.2 percent. The annual divergence is on pace for the biggest since economist Jim O’Neill coined the term in 2001, leaving the combined market capitalization of Chinese and Indian equities $5.2 trillion larger than that of Russia and Brazil, according to data compiled by Bloomberg.

…

At the time BRIC was coined it was useful to describe the broad and increasing importance of the four largest emerging-market economies, but it was never suitable as an investing concept,” Mark Gordon-James, a senior investment manager at Aberdeen Asset Management, which managed $526 billion at the end of September, said in an interview on Dec. 18 from London.

But worry not! The marketers will soon find another bandwagon!

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 8bp, FixedResets rocketing up 55bp and DeemedRetractibles off 7bp. The Performance Highlights table is suitably lengthy, notable for a high proportion of FixedReset winners, particularly in the names that were hit hard in the early part of the month – ENB, TRP & HSE. But all this was on volume that was pathetically, horribly, awfully, grossly, incredibly low.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

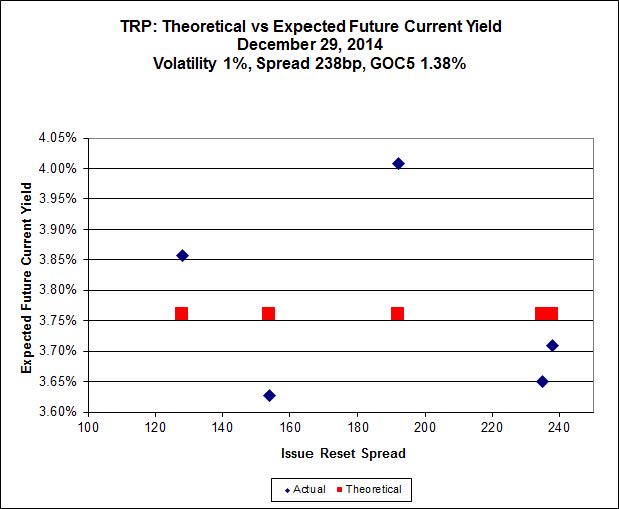

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 20.58, is $1.36 cheap, but it has already reset (at +192). TRP.PR.D, bid at 25.34 and resetting at +238bp on 2019-4-30 is $0.34 rich and TRP.PR.E, bid at 25.55 and resetting at +235bp on 2019-10-30 (two months prior to the next TRP.PR.A reset), is $0.75 rich.

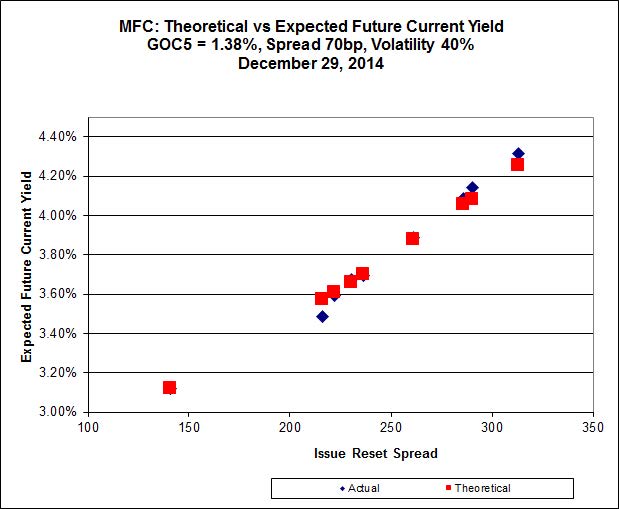

Click for Big

There is an excellent fit to theory for the MFC issues, but Implied Volatility continues to be a conundrum. It is far too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

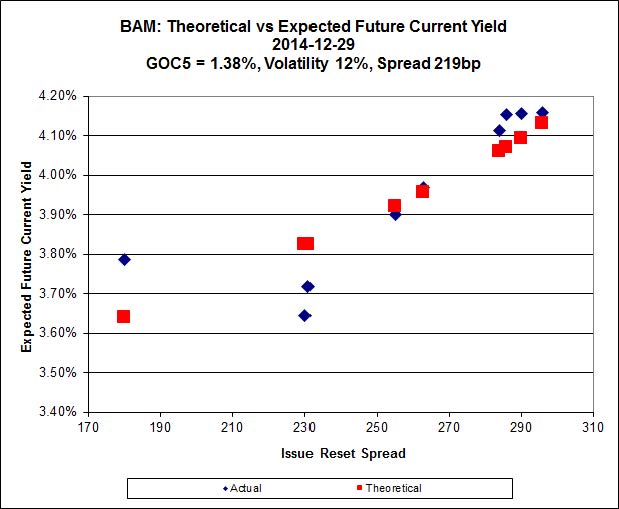

Click for Big

There continues to be cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 21.00 and appears to be $0.84 cheap, while BAM.PR.R, resetting at +230bp 2016-6-30 is bid at 25.25 and appears to be $1.19 rich.

It seems clear that the higher-spread issues define a curve with significantly more Implied Volatility than is calculated when the low-spread outlier is included.

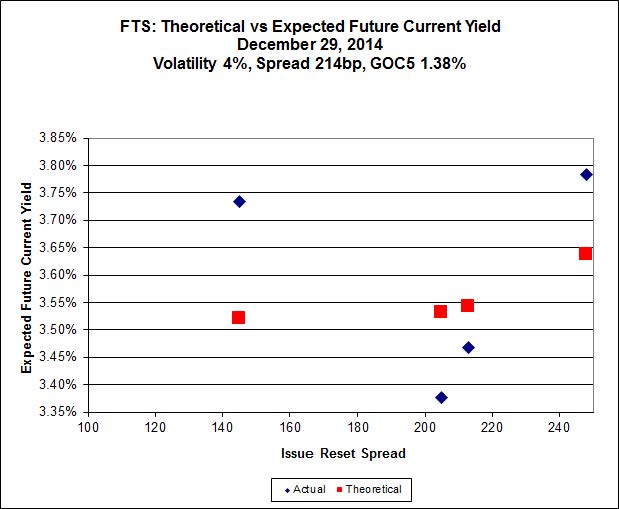

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.95, looks $1.15 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 25.40, looks $1.12 expensive and resets 2019-3-1

Click for Big

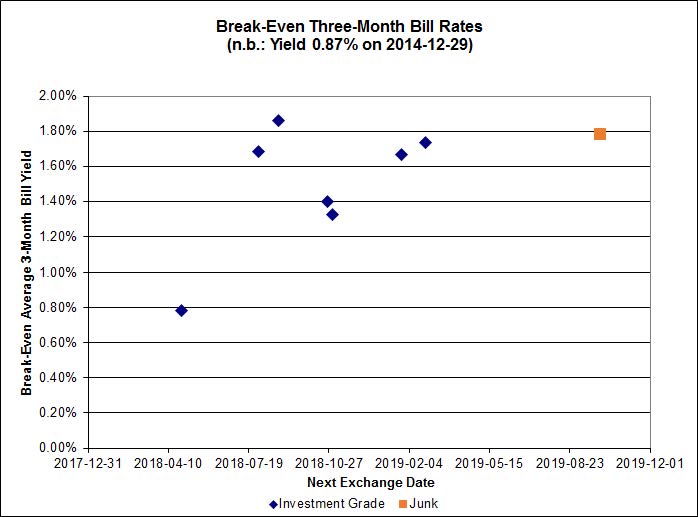

The average break-even rate has declined from 1.80%-2.00% at the time recent conversion decisions were made to a current very wide range of (mostly) 1.40%-1.80%. This decline means that the estimated profit on TRP.PR.A conversion has declined from $0.48 to a mere $0.06 (at the lower end of the range, 1.40%).

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0717 % | 2,516.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0717 % | 3,983.5 |

| Floater | 3.01 % | 3.11 % | 65,003 | 19.44 | 4 | -0.0717 % | 2,674.8 |

| OpRet | 4.41 % | -2.14 % | 23,257 | 0.08 | 2 | 0.0784 % | 2,752.0 |

| SplitShare | 4.27 % | 4.04 % | 35,851 | 3.68 | 5 | 0.0991 % | 3,202.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0784 % | 2,516.4 |

| Perpetual-Premium | 5.45 % | -3.90 % | 69,028 | 0.08 | 20 | 0.2034 % | 2,488.8 |

| Perpetual-Discount | 5.16 % | 5.04 % | 110,633 | 15.34 | 15 | 0.0760 % | 2,669.3 |

| FixedReset | 4.21 % | 3.58 % | 243,931 | 8.37 | 77 | 0.5527 % | 2,553.0 |

| Deemed-Retractible | 4.95 % | 0.70 % | 92,530 | 0.16 | 40 | -0.0660 % | 2,627.9 |

| FloatingReset | 2.56 % | 1.93 % | 63,553 | 3.41 | 5 | -0.0785 % | 2,545.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.R | Deemed-Retractible | -1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 5.19 % |

| MFC.PR.B | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.02 Bid-YTW : 5.20 % |

| MFC.PR.C | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.34 Bid-YTW : 5.41 % |

| PWF.PR.A | Floater | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 19.25 Evaluated at bid price : 19.25 Bid-YTW : 2.75 % |

| POW.PR.D | Perpetual-Discount | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 24.05 Evaluated at bid price : 24.30 Bid-YTW : 5.15 % |

| ENB.PR.D | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.38 Evaluated at bid price : 22.94 Bid-YTW : 4.15 % |

| GWO.PR.N | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.92 Bid-YTW : 4.88 % |

| ENB.PR.Y | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 21.81 Evaluated at bid price : 22.23 Bid-YTW : 4.32 % |

| ENB.PF.A | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.89 Evaluated at bid price : 24.25 Bid-YTW : 4.22 % |

| ENB.PF.G | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.91 Evaluated at bid price : 24.40 Bid-YTW : 4.21 % |

| ENB.PR.T | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.16 Evaluated at bid price : 22.75 Bid-YTW : 4.31 % |

| TRP.PR.B | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 17.24 Evaluated at bid price : 17.24 Bid-YTW : 3.94 % |

| ELF.PR.G | Perpetual-Discount | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.57 Evaluated at bid price : 22.86 Bid-YTW : 5.19 % |

| ENB.PR.N | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.58 Evaluated at bid price : 23.42 Bid-YTW : 4.30 % |

| PWF.PR.P | FixedReset | 1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.66 % |

| MFC.PR.L | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-06-19 Maturity Price : 25.00 Evaluated at bid price : 25.40 Bid-YTW : 3.56 % |

| ENB.PF.E | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.80 Evaluated at bid price : 24.10 Bid-YTW : 4.26 % |

| IFC.PR.A | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 4.70 % |

| ENB.PR.F | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.42 Evaluated at bid price : 23.05 Bid-YTW : 4.26 % |

| ENB.PR.H | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 4.32 % |

| BAM.PF.D | Perpetual-Discount | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 21.24 Evaluated at bid price : 21.52 Bid-YTW : 5.71 % |

| ENB.PR.B | FixedReset | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.33 Evaluated at bid price : 22.72 Bid-YTW : 4.22 % |

| TRP.PR.C | FixedReset | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 20.13 Evaluated at bid price : 20.13 Bid-YTW : 3.73 % |

| TRP.PR.D | FixedReset | 1.91 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.34 Bid-YTW : 3.58 % |

| MFC.PR.F | FixedReset | 2.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.35 Bid-YTW : 4.37 % |

| TRP.PR.E | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.35 Evaluated at bid price : 25.55 Bid-YTW : 3.62 % |

| ENB.PR.P | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 22.35 Evaluated at bid price : 23.03 Bid-YTW : 4.25 % |

| TRP.PR.A | FixedReset | 2.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 20.58 Evaluated at bid price : 20.58 Bid-YTW : 4.06 % |

| HSE.PR.A | FixedReset | 4.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 3.78 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.C | FixedReset | 59,200 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.14 Evaluated at bid price : 24.95 Bid-YTW : 3.57 % |

| CM.PR.P | FixedReset | 28,300 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.12 Evaluated at bid price : 24.89 Bid-YTW : 3.58 % |

| BMO.PR.T | FixedReset | 22,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.26 Evaluated at bid price : 25.23 Bid-YTW : 3.55 % |

| MFC.PR.F | FixedReset | 19,700 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.35 Bid-YTW : 4.37 % |

| TD.PF.A | FixedReset | 16,895 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.33 Evaluated at bid price : 25.51 Bid-YTW : 3.51 % |

| TD.PF.B | FixedReset | 14,440 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-29 Maturity Price : 23.32 Evaluated at bid price : 25.41 Bid-YTW : 3.53 % |

| There were 1 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PR.R | Deemed-Retractible | Quote: 26.21 – 26.84 Spot Rate : 0.6300 Average : 0.3819 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 24.02 – 24.60 Spot Rate : 0.5800 Average : 0.3506 YTW SCENARIO |

| GWO.PR.R | Deemed-Retractible | Quote: 24.30 – 24.82 Spot Rate : 0.5200 Average : 0.3365 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 23.34 – 23.79 Spot Rate : 0.4500 Average : 0.3131 YTW SCENARIO |

| RY.PR.F | Deemed-Retractible | Quote: 25.67 – 26.04 Spot Rate : 0.3700 Average : 0.2388 YTW SCENARIO |

| ENB.PR.J | FixedReset | Quote: 23.92 – 24.30 Spot Rate : 0.3800 Average : 0.2515 YTW SCENARIO |