Lucky Assiduous Readers! It’s time for me to get on my favourite hobby-horse again … one I’ve been riding for over twenty five years now … and will probably keep flogging even if it dies:

GICs also have a psychological benefit because, unlike bonds, GIC prices don’t change when interest rates rise or fall.

” GIC prices don’t change when interest rates rise or fall.”

This is not correct. Reported GIC prices generally don’t change, but the actual price you can get for it (if transferable) does – and so does the actual value of the cash flows.

The brokerage industry’s obfuscation of value with respect to GICs is going to be yet another competitive advantage for the banks when CRM2 and mandatory performance reporting come into force.

For a longer rant, see my essay Preferred Shares and GICs; those who are more interested in cheap entertainment can just look at the comments to the Globe story.

But the big news of the day was FOMC press release:

Consistent with its previous statement, the Committee judges that an increase in the target range for the federal funds rate remains unlikely at the April FOMC meeting. The Committee anticipates that it will be appropriate to raise the target range for the federal funds rate when it has seen further improvement in the labor market and is reasonably confident that inflation will move back to its 2 percent objective over the medium term. This change in the forward guidance does not indicate that the Committee has decided on the timing of the initial increase in the target range.

…

When the Committee decides to begin to remove policy accommodation, it will take a balanced approach consistent with its longer-run goals of maximum employment and inflation of 2 percent. The Committee currently anticipates that, even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target federal funds rate below levels the Committee views as normal in the longer run.

There was no dissent.

And the markets went wild!

The Federal Reserve dropped an assurance it will be “patient” in raising interest rates, ending an era in its communications policy and opening the door for higher borrowing costs as early as June.

“An increase in the target range for the federal funds rate remains unlikely at the April” meeting, the Federal Open Market Committee said in a statement Wednesday in Washington. Fed officials also lowered their median estimate for the federal funds rate at the end of 2015 to 0.625 percent, compared with 1.125 percent in December forecasts.

…

Stocks rose, erasing earlier losses, after the FOMC announcement. The Standard & Poor’s 500 Index was up 0.6 percent at 2,087.04 as of 2:11 p.m. in New York. Ten-year Treasury notes yielded 1.99 percent, down 6 basis points.

…

In December, the FOMC dropped a clause from its statement that it would hold rates low for a “considerable time” and instead said it would be “patient” in weighing an increase.

In fact, the market took the release as a whole to be a dovish indicator:

Money-market futures traders cut the odds of a Federal Reserve interest-rate increase below 50 percent until December after Chair Janet Yellen lowered her outlook for growth and the pace of policy tightening.

The likelihood that policy makers will lift their benchmark rate from near zero in September fell to 39 percent from 55 percent on Tuesday, according to calculations by Bloomberg using federal fund futures contracts. Futures traders have wiped out the chance of an increase in June, assigning it an 11 percent probability.

While the policy-setting Federal Open Market Committee dropped a commitment to be “patient” when raising rates, a key shift was policy makers’ lowering of their median estimate for benchmark borrowing costs during the next two years, according to Brian Smedley, an interest-rate strategist at Bank of America Corp. in New York. The fresh set of estimates reduced the median for the federal funds rate at the end of 2015 to 0.625 percent, compared with a December forecast of 1.125 percent.

The OECD is not impressed by Canada’s prospects:

Smacked by the oil crash, Canada has taken a big hit in a new OECD economic forecast.

In its updated projections released Wednesday, the Organization for Economic Co-operation and Development cut its outlook for growth in Canada this year to 2.2 per cent, down from 2.6 per cent in its November forecast.

For 2016, the group now sees growth of 2.1 per cent, down from 2.4 per cent.

“Oil and commodity exporters are facing weaker growth prospects as the result of lower prices,” the OECD said.

…

Like Canada, the forecast for Brazil has been cut.“The main class of countries for which near-term growth prospects have worsened since the November 2014 economic outlook is the commodity exporters,” the OECD said.

“The interim projections are significantly lower for oil-exporters Canada and Brazil, with short-term growth prospects in Brazil also being restrained by monetary and fiscal tightening and increasing political uncertainty,” it added.

“Growth has already slowed in many other oil-exporting countries, and with the fall in commodity prices going well beyond oil, exporters of metals, coal and some agricultural commodities also face less favourable growth prospects this year.”

It was a mildly positive day for the Canadian preferred share market, with PerpetualDiscounts gaining 3bp, FixedResets flat, and DeemedRetractibles up 6bp. The overall calmness masked a lot of volatility, with a fairly lengthy Performance Highlights table dominated by losing FixedResets. Volume was very high.

PerpetualDiscounts now yield 4.99%, equivalent to 6.49% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.7%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now 280bp, a widening from the 270bp reported March 11.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

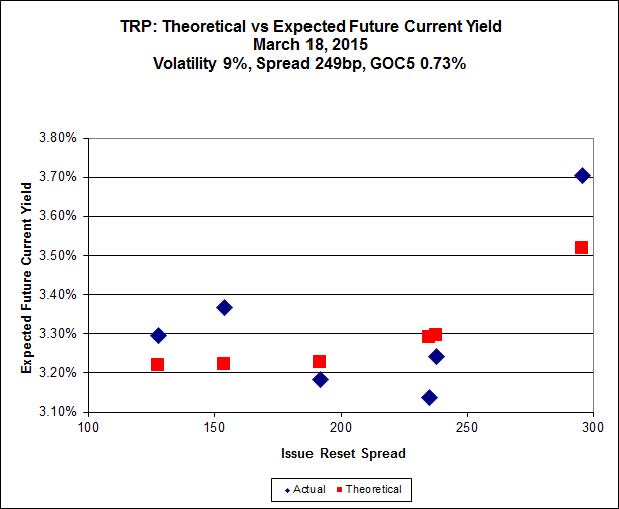

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.55 to be $1.15 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.32 cheap at its bid price of 24.90.

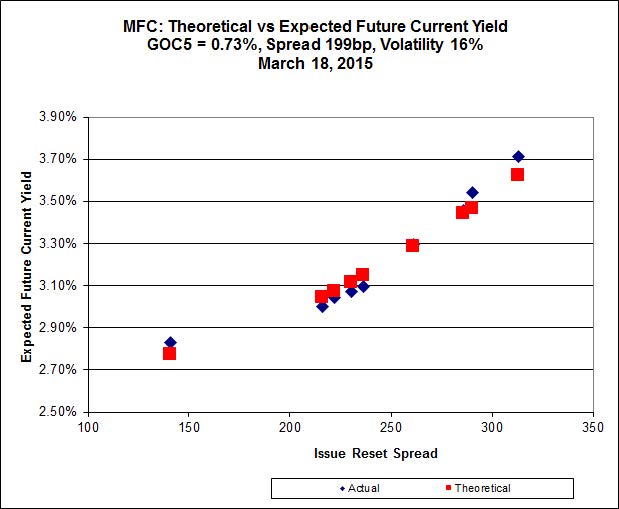

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236 on 2019-12-19, bid at 24.95 to be $0.40 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.99 to be $0.67 cheap.

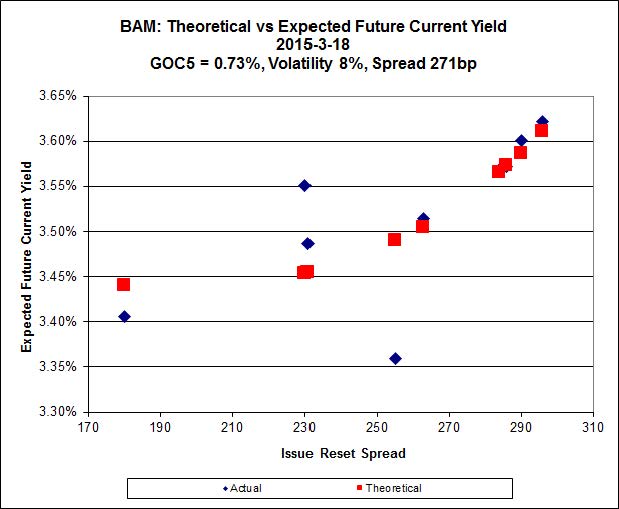

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.33 to be $0.61 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.41 and appears to be $0.91 rich.

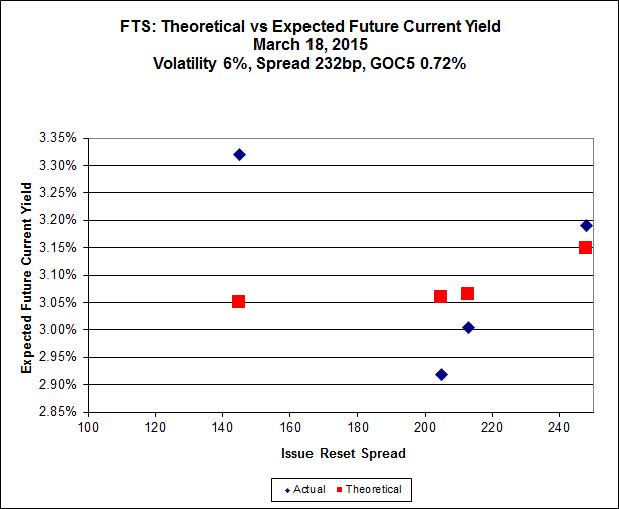

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.42, looks $1.45 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.82 and is $1.09 rich.

Click for Big

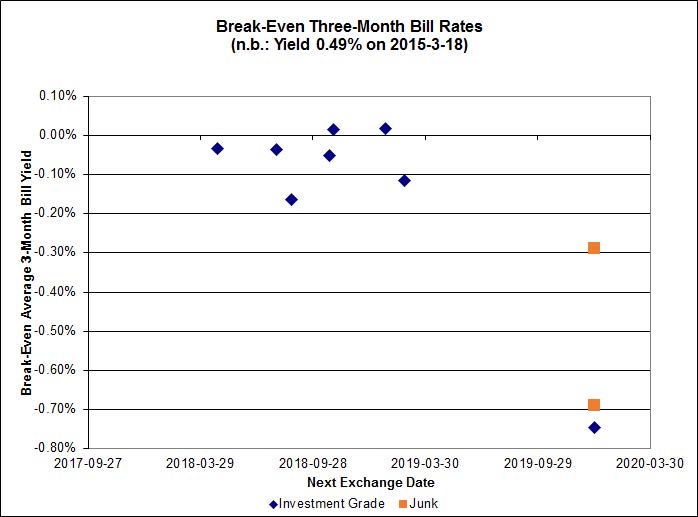

Investment-grade pairs predict an average over the next five years of about 0.00% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.75%. The DC.PR.B / DC.PR.D pair has gone from the extreme to the ludicrous and now predicts an average bill rate over the next 4 3/4 years of -2.06%

Click for Big

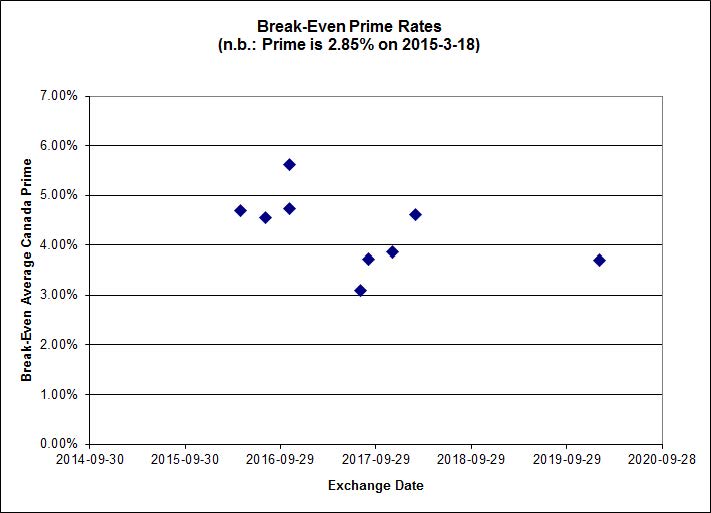

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.2762 % | 2,313.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.2762 % | 4,044.7 |

| Floater | 3.28 % | 3.28 % | 64,441 | 19.05 | 3 | -1.2762 % | 2,459.2 |

| OpRet | 4.07 % | 1.38 % | 108,246 | 0.25 | 1 | -0.0397 % | 2,762.6 |

| SplitShare | 4.46 % | 4.42 % | 57,844 | 4.43 | 5 | -0.0040 % | 3,220.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0397 % | 2,526.1 |

| Perpetual-Premium | 5.30 % | 1.28 % | 56,233 | 0.08 | 25 | -0.1768 % | 2,517.1 |

| Perpetual-Discount | 5.00 % | 4.99 % | 164,286 | 15.43 | 9 | 0.0281 % | 2,798.8 |

| FixedReset | 4.39 % | 3.51 % | 244,388 | 16.67 | 85 | -0.0036 % | 2,427.6 |

| Deemed-Retractible | 4.90 % | -1.61 % | 106,628 | 0.12 | 37 | 0.0587 % | 2,659.6 |

| FloatingReset | 2.50 % | 2.93 % | 90,485 | 6.31 | 8 | -0.0214 % | 2,328.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ELF.PR.H | Perpetual-Premium | -2.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 24.58 Evaluated at bid price : 25.06 Bid-YTW : 5.56 % |

| MFC.PR.F | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.90 Bid-YTW : 5.82 % |

| SLF.PR.G | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.66 Bid-YTW : 6.31 % |

| TRP.PR.C | FixedReset | -2.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 16.86 Evaluated at bid price : 16.86 Bid-YTW : 3.70 % |

| HSE.PR.A | FixedReset | -2.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 16.98 Evaluated at bid price : 16.98 Bid-YTW : 3.92 % |

| BAM.PR.C | Floater | -1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 15.17 Evaluated at bid price : 15.17 Bid-YTW : 3.28 % |

| BMO.PR.Q | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 3.61 % |

| MFC.PR.L | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.06 Bid-YTW : 3.89 % |

| BAM.PR.K | Floater | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 15.12 Evaluated at bid price : 15.12 Bid-YTW : 3.29 % |

| BAM.PR.B | Floater | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 3.24 % |

| ENB.PR.T | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 20.39 Evaluated at bid price : 20.39 Bid-YTW : 4.31 % |

| GWO.PR.N | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.35 Bid-YTW : 5.83 % |

| PWF.PR.P | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 18.71 Evaluated at bid price : 18.71 Bid-YTW : 3.41 % |

| FTS.PR.M | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 23.23 Evaluated at bid price : 25.15 Bid-YTW : 3.34 % |

| MFC.PR.N | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.66 Bid-YTW : 3.67 % |

| CIU.PR.C | FixedReset | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 16.65 Evaluated at bid price : 16.65 Bid-YTW : 3.45 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.G | Perpetual-Premium | 322,060 | Called for redemption April 30. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-17 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : -0.26 % |

| RY.PR.M | FixedReset | 315,655 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 22.91 Evaluated at bid price : 24.40 Bid-YTW : 3.48 % |

| FTS.PR.H | FixedReset | 230,857 | TD crossed blocks of 41,900 and 70,000 at 16.94, then crossed 110,900 at 16.75. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 16.42 Evaluated at bid price : 16.42 Bid-YTW : 3.51 % |

| W.PR.H | Perpetual-Premium | 194,892 | Desjardins crossed blocks of 96,300 and 96,800 at 25.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 24.87 Evaluated at bid price : 25.18 Bid-YTW : 5.55 % |

| CU.PR.C | FixedReset | 165,965 | Desjardins crossed 159,200 at 24.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 23.16 Evaluated at bid price : 24.11 Bid-YTW : 3.39 % |

| BNS.PR.R | FixedReset | 145,300 | Nesbitt crossed 62,700 and 75,000 at 25.67. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.64 Bid-YTW : 3.05 % |

| BMO.PR.T | FixedReset | 144,975 | Nesbitt crossed 46,900 and 75,000 at 24.79. TD sold 19,900 to anonymous at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-18 Maturity Price : 23.10 Evaluated at bid price : 24.70 Bid-YTW : 3.18 % |

| RY.PR.B | Deemed-Retractible | 114,122 | Nesbitt crossed 111,200 at 25.65. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-04-17 Maturity Price : 25.25 Evaluated at bid price : 25.62 Bid-YTW : -9.44 % |

| There were 56 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ELF.PR.H | Perpetual-Premium | Quote: 25.06 – 26.00 Spot Rate : 0.9400 Average : 0.5411 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 15.12 – 15.89 Spot Rate : 0.7700 Average : 0.5081 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 24.06 – 24.54 Spot Rate : 0.4800 Average : 0.3081 YTW SCENARIO |

| FTS.PR.J | Perpetual-Premium | Quote: 24.60 – 25.25 Spot Rate : 0.6500 Average : 0.4875 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 23.75 – 24.23 Spot Rate : 0.4800 Average : 0.3527 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 16.42 – 16.83 Spot Rate : 0.4100 Average : 0.2940 YTW SCENARIO |