After years of pretending that their resource-funded low taxes meant that they were some kind of conservatives, Albertans have finally admitted they’re actually a pack of socialists:

Albertans have chosen a new political path with the stunning election of a majority New Democratic government, ending a Progressive Conservative dynasty in power for more than four decades.

The NDP, leading in the polls for much of the campaign, becomes only the third party to govern the province since 1935. Heading a new government, Leader Rachel Notley will now have a mandate to take the province in a new direction but will also inherit tough economic challenges.

Solidarity, comrades!

Australia cut policy rates and market rates rose:

Australia cut interest rates to a fresh record low and said there are signs of improving household spending, sending the currency and bond yields higher as markets bet policy makers won’t ease further.

The central bank lowered the key rate to 2 percent from 2.25 percent Tuesday, as predicted by traders and economists. Governor Glenn Stevens said in an accompanying statement “the inflation outlook provided the opportunity for monetary policy to be eased further, so as to reinforce recent encouraging trends in household demand.”

While weaker business investment and subdued spending by the government is weighing on the economy, encouraging the RBA to cut, there are signs that low borrowing costs are starting to spur stronger demand from households. Stevens cited a better jobs market and gave no indication the central bank was considering a further easing.

Treasuries fell with European bonds as oil’s rally above $60 a barrel added to signs of incipient inflation, while concern rose that Greece won’t be able to resolve its debt crisis. U.S. stocks tumbled the most in more than a month amid a retreat in global equities.

Yields on 10-year Treasury notes rose four basis points to 2.19 percent by 5 p.m. in New York, extending an eight-week high as U.S. crude jumped 2.5 percent to $60.40 a barrel. German bonds resumed losses, while Spanish debt tumbled with Greek stocks. The Standard & Poor’s 500 Index lost 1.2 percent, the steepest drop since March 25. European equities slid to the lowest level since March 10. Copper entered a bull market.

The exodus from sovereign-debt markets is accelerating as investors question the sustainability of rallies that pushed yields to record lows. Data Tuesday showed U.S. services growth accelerated more than forecast last month as the Federal Reserve considers raising interest rates. Crude traded in New York topped $60 for the first time this year on speculation the biggest supply glut in 85 years will ease.

…

Ten-year Treasury yields have increased 28 basis points, or 0.28 percentage point, since April 24 and earlier on Tuesday touched the highest level since March 6. German 10-year yields rose six basis points to 0.52 percent, for a seventh straight gain to the highest level since January. Spain’s 10-year rate jumped the most since June 2013.

There are rumblings of an increase in inflation targets:

A quarter of a century since New Zealand opened the era of inflation targeting, policy makers from the U.S., euro area, U.K. and Japan are all undershooting their consumer-price goals. Of the Group of Seven, only Canada is currently meeting its mandate.

Rather than lowering their sights to make things easier, the misses are fanning calls for targets to be increased from the 2 percent most aim for to perhaps as high as 4 percent.

While a similar idea was pitched five years ago by International Monetary Fund economists led by Olivier Blanchard, and endorsed by Nobel laureate Paul Krugman, this time around it may be the central-banking community itself proposing a rethink.

Former Federal Reserve Chair Ben S. Bernanke last month suggested he would be open to an increase in the U.S. Federal Reserve’s 2 percent goal, saying there is nothing “magical” about that number.

Fed Bank of Boston President Eric Rosengren said the same month it could be the case “inflation targets have been set too low.” His colleague from San Francisco, John Williams, told the New York Times that if the future is one of weaker growth because of demographics and productivity then it’s worth asking “is the 2 percent inflation goal sufficiently high in that kind of world?”

But if they can’t hit 2 percent, why lift the targets?

Doing so may ignite current inflation expectations, lowering so-called real interest rates and giving economic growth an extra spur, according to Jeremy Lawson, chief economist at Standard Life Investments Ltd.

And today’s drone news is about privacy:

Conflict is on the rise. A New Jersey man last year shot down a drone flying over his neighborhood. Last June, a woman in Connecticut was arrested after she was accused of assaulting a young man flying a helicopter drone over a public beach.

In the past two years, at least seven states have outlawed the use of drones to violate privacy, according to the National Conference of State Legislatures. California is considering a bill that would expand trespassing laws to include piloting a drone within 350 feet above private property without permission.

…

States already protect citizens against Peeping Toms regardless of the technology involved, said Brendan Schulman, an attorney who specializes in drones at Kramer Levin Naftalis and Frankel in New York.“Many of these state law proposals are an overreaction, because existing state privacy laws already cover the types of misconduct that people are most concerned about,” he said. “It shouldn’t matter if you use a tripod or a zoom lens or a hidden camera placed in a tree. If you’re invading someone’s privacy, it’s the misconduct that should be illegal, and not the technology.”

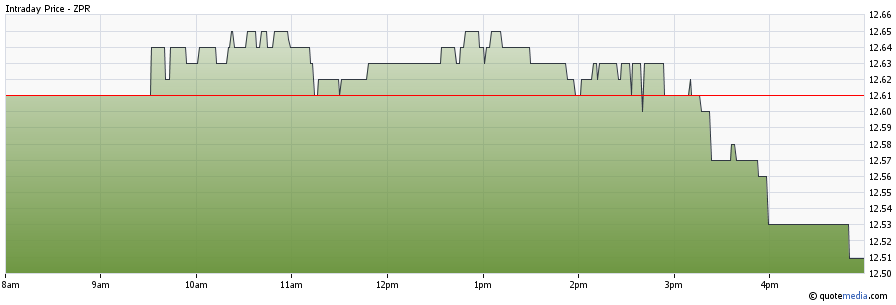

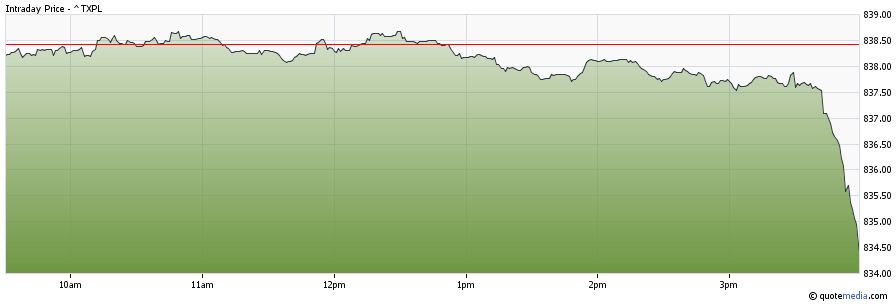

PrefBlog’s “Things That Make You Go ‘Hmmm'” department presents, for your delectation and amusement, charts of the TXPL FixedReset index and of ZPR, the ETF based on that index, for today:

Click for Big

Click for Big

So it looks like there was mild weakness in TXPL commencing at about 1pm, which had no effect on ZPR until about 3pm, when ZPR started collapsing, which in turn led to a rapid collapse just before the bell in TXPL. ZPR had volume for the day of 895,012 which, by standards of the past month, is above average but not spectacular. Total returns for the day for the two measures were roughly equal. It would be most interesting to learn just what is going on; if the liquidity pundits are correct – and I think they are – we may see more of this type of loose-linkage-fast-collapse behaviour in the future, should a general rise in bond yields become disorderly.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 29bp, FixedResets down 47bp and DeemedRetractibles gaining 6bp. ENB FixedResets dominate the bad part of the Performance Highlights table. Volume was well above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

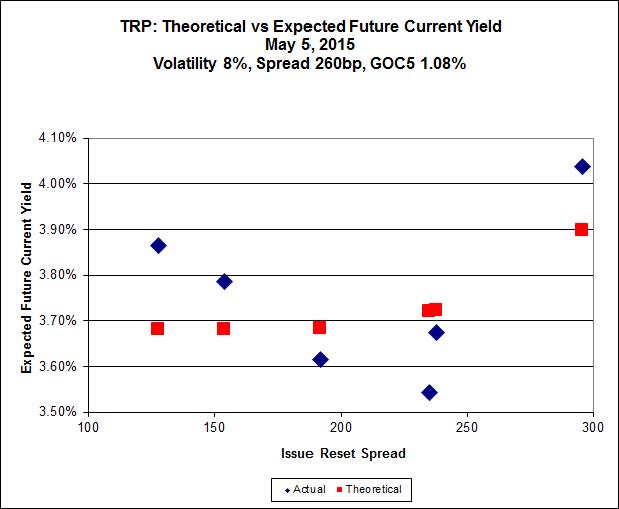

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.20 to be $1.15 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.91 cheap at its bid price of 25.01.

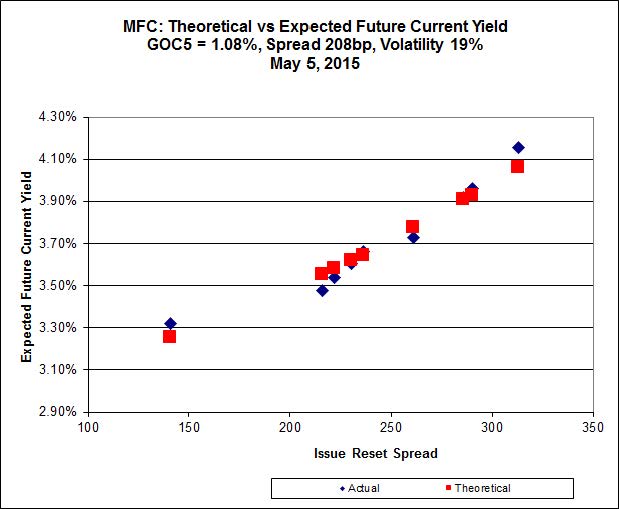

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.30 to be $0.51 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.34 to be $0.58 cheap.

Click for Big

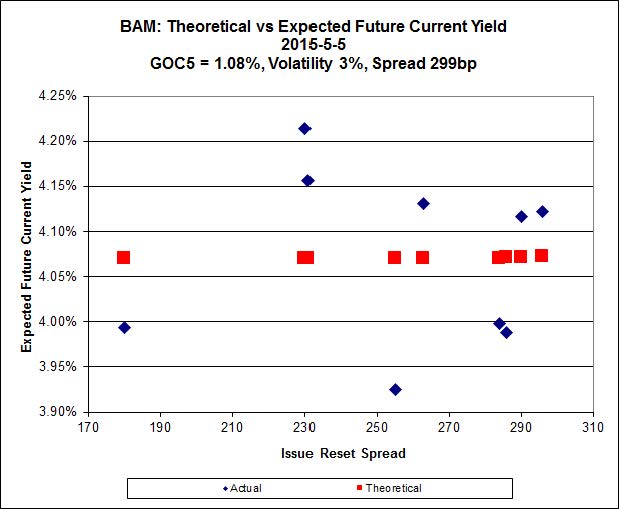

The cheapest issue relative to its peers is BAM.PF.R, resetting at +230bp on 2016-6-30, bid at 20.05 to be $0.71 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 23.12 and appears to be $0.82 rich.

Click for Big

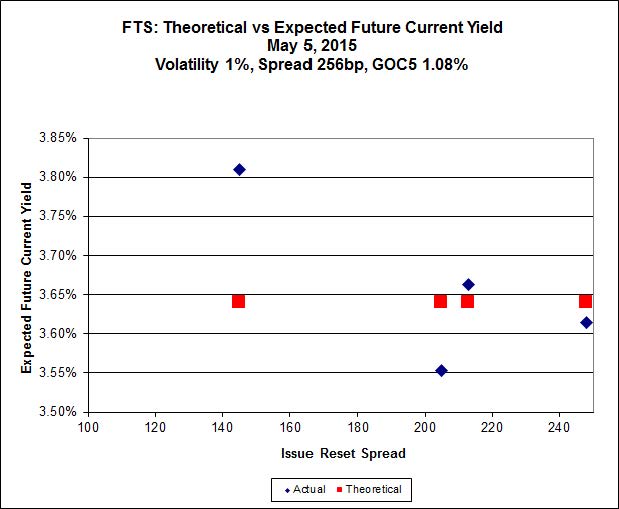

FTS.PR.H, with a spread of +145bp, and bid at 16.60, looks $0.78 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.02 and is $0.52 rich.

Click for Big

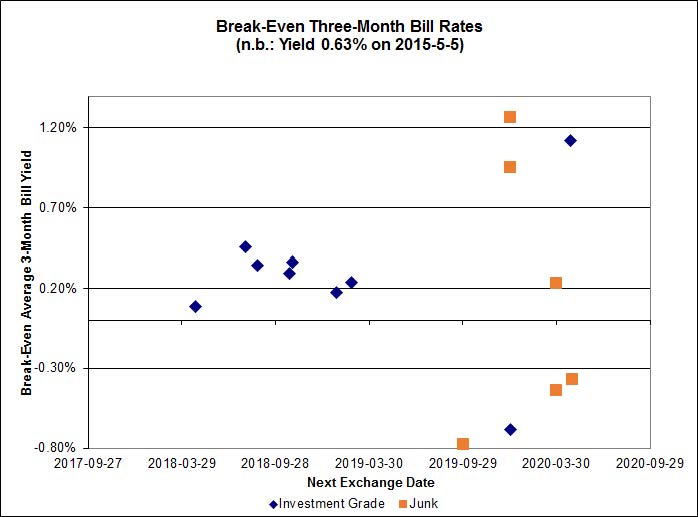

Investment-grade pairs now predict an average over the next five years of about 0.30%, but TRP.PR.A / TRP.PR.F is an outlier at -0.69%. The DC.PR.B / DC.PR.D pair retains its customary outlier status, with a breakeven rate of -0.78%, but has now managed to edge its way into the graph area while the new data point for BRF.PR.A / BRF.PR.B is at -1.22% and BRF.PR.B lost its virginity with a whopping 600 shares traded.

Click for Big

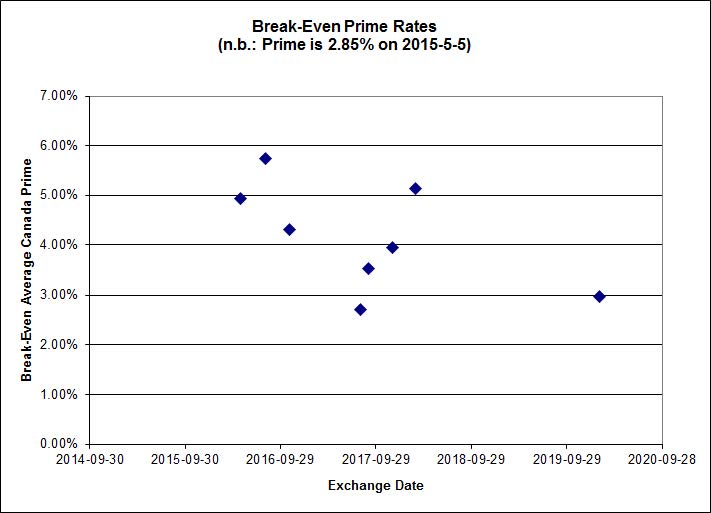

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.2035 % | 2,325.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.2035 % | 4,066.6 |

| Floater | 3.12 % | 3.21 % | 53,444 | 19.19 | 4 | 1.2035 % | 2,472.5 |

| OpRet | 4.42 % | -1.08 % | 36,619 | 0.16 | 2 | -0.0196 % | 2,767.0 |

| SplitShare | 4.56 % | 4.77 % | 67,067 | 3.36 | 3 | 0.4006 % | 3,235.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0196 % | 2,530.1 |

| Perpetual-Premium | 5.45 % | 1.35 % | 68,942 | 0.08 | 18 | -0.0523 % | 2,521.2 |

| Perpetual-Discount | 5.05 % | 5.00 % | 115,691 | 15.45 | 15 | -0.2869 % | 2,782.1 |

| FixedReset | 4.42 % | 3.90 % | 272,866 | 16.19 | 86 | -0.4716 % | 2,401.9 |

| Deemed-Retractible | 4.92 % | 3.19 % | 112,578 | 0.30 | 36 | 0.0565 % | 2,649.9 |

| FloatingReset | 2.61 % | 2.99 % | 68,831 | 6.20 | 7 | 0.0367 % | 2,321.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PR.B | FixedReset | -4.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 19.28 Evaluated at bid price : 19.28 Bid-YTW : 4.67 % |

| BAM.PR.T | FixedReset | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 20.39 Evaluated at bid price : 20.39 Bid-YTW : 4.34 % |

| FTS.PR.J | Perpetual-Discount | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 23.83 Evaluated at bid price : 24.24 Bid-YTW : 4.96 % |

| BAM.PR.X | FixedReset | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 18.03 Evaluated at bid price : 18.03 Bid-YTW : 4.31 % |

| ENB.PR.F | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.61 % |

| ENB.PR.D | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.51 % |

| ENB.PF.G | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 21.70 Evaluated at bid price : 22.11 Bid-YTW : 4.50 % |

| BAM.PR.R | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 4.41 % |

| IFC.PR.C | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.21 Bid-YTW : 4.28 % |

| ENB.PR.J | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 21.55 Evaluated at bid price : 21.81 Bid-YTW : 4.41 % |

| ENB.PF.E | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 21.63 Evaluated at bid price : 21.99 Bid-YTW : 4.50 % |

| ENB.PF.C | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 21.60 Evaluated at bid price : 21.93 Bid-YTW : 4.49 % |

| ENB.PR.T | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 20.43 Evaluated at bid price : 20.43 Bid-YTW : 4.57 % |

| BNS.PR.Y | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.82 Bid-YTW : 3.35 % |

| NA.PR.S | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 23.07 Evaluated at bid price : 24.52 Bid-YTW : 3.57 % |

| ENB.PR.N | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 4.55 % |

| ENB.PR.Y | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 19.83 Evaluated at bid price : 19.83 Bid-YTW : 4.60 % |

| TRP.PR.D | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 22.64 Evaluated at bid price : 23.54 Bid-YTW : 3.74 % |

| ENB.PR.P | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 20.66 Evaluated at bid price : 20.66 Bid-YTW : 4.51 % |

| CU.PR.E | Perpetual-Discount | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 23.98 Evaluated at bid price : 24.40 Bid-YTW : 5.00 % |

| MFC.PR.F | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 6.26 % |

| BAM.PR.K | Floater | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 15.30 Evaluated at bid price : 15.30 Bid-YTW : 3.28 % |

| CIU.PR.C | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.68 % |

| BAM.PR.C | Floater | 1.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 15.39 Evaluated at bid price : 15.39 Bid-YTW : 3.26 % |

| HSE.PR.A | FixedReset | 2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 17.17 Evaluated at bid price : 17.17 Bid-YTW : 4.24 % |

| BAM.PR.B | Floater | 2.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 15.65 Evaluated at bid price : 15.65 Bid-YTW : 3.21 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.C | FixedReset | 63,365 | TD bought 10,000 from RBC at 24.09, then crossed 20,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 22.82 Evaluated at bid price : 24.07 Bid-YTW : 3.48 % |

| ENB.PR.D | FixedReset | 63,180 | TD crossed 40,000 at 20.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 19.92 Evaluated at bid price : 19.92 Bid-YTW : 4.51 % |

| TRP.PR.G | FixedReset | 50,330 | RBC crossed 17,500 at 25.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 23.13 Evaluated at bid price : 25.01 Bid-YTW : 3.90 % |

| RY.PR.H | FixedReset | 47,655 | TD crossed 25,000 at 24.22. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 22.89 Evaluated at bid price : 24.15 Bid-YTW : 3.48 % |

| CM.PR.Q | FixedReset | 46,260 | Scotia crossed 40,000 at 24.95. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 23.02 Evaluated at bid price : 24.65 Bid-YTW : 3.78 % |

| PWF.PR.P | FixedReset | 45,955 | Scotia bought 21,300 from RBC at 18.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-05 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 3.70 % |

| There were 41 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| ENB.PR.B | FixedReset | Quote: 19.28 – 19.93 Spot Rate : 0.6500 Average : 0.3703 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 24.24 – 24.90 Spot Rate : 0.6600 Average : 0.4218 YTW SCENARIO |

| BMO.PR.T | FixedReset | Quote: 24.05 – 24.60 Spot Rate : 0.5500 Average : 0.3169 YTW SCENARIO |

| NA.PR.S | FixedReset | Quote: 24.52 – 25.00 Spot Rate : 0.4800 Average : 0.2874 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 24.21 – 24.69 Spot Rate : 0.4800 Average : 0.3131 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.40 – 24.89 Spot Rate : 0.4900 Average : 0.3266 YTW SCENARIO |