Too bad none of this activity is taking place in Canada. We spend our billions on pipelines to ship the raw material out of the country.:

While the collapse in oil and gas prices since the middle of last year caused energy companies to slash investment in oil wells, Thursday’s report on second-quarter GDP showed an interesting dynamic taking shape — investment in factories has been running full bore.

It may be surprising on the surface, given that manufacturing has simmered down this year on the heels of a weaker global economy, but spending on all types of production facilities increased at a 65 percent annualized pace in the second quarter. That was almost enough to offset a 68 percent plunge in investment in wells and mines that marked the biggest drop in 29 years.

Outlays for factory-related structures jumped even more from January through March — surging at a 95 percent pace. Over the last four quarters, investment in plants increased an average 64 percent, the strongest since records began in 1958.

…

Spending on chemical plant construction in the private sector stood at a seasonally adjusted annual rate of $48.4 billion in May, up almost 10 percent from a month earlier, according to the latest data from the Census Bureau. During the first five months of this year, an unadjusted $15.9 billion was spent on chemical plants, more than double the $7 billion for the same period in 2014.

In another bit of sensible news that is, obviously, not from Canada, electric car owners are being paid for flex-time:

One hundred owners of BMW AG’s i3 hatchback receive $1,000 upfront to participate in Pacific Gas & Electric Co.’s 18-month trial, which starts this week and is confined to the San Francisco Bay Area. Peter Berman, a 70-year-old, semi-retired Los Altos psychologist, was selected from about 400 applicants.

“My understanding is that we’ll get a text message that says ‘Hey, you’re charging your car right now, can you back off for an hour?’” said Berman, who began leasing his $40,000-plus i3 in October. “This is the wave of the future. We can’t continue to be dependent on gas and oil and coal for our energy use. I’m really curious as to how this is all going to unfold.”

The PG&E-BMW pilot is one of myriad experiments under way worldwide as utilities try to anticipate what will happen if (or when) millions of electric vehicles pour onto city streets and highways. Power companies see both challenge and promise. Yes, electric cars could put more pressure on the grid if everyone plugs them in at the same time. But utilities could also tap batteries for backup power when the grid is under strain or temporarily knocked out in an emergency, paying drivers for the electricity harvested from their parked cars.

But how about the Pan-Am Games, huh? Weren’t they something? The memories will distract us from obsessing over the fact that even the Brits are moving ahead of us in ejector bed technology.

I haven’t passed on any drone news in almost a week now, so here’s some more on air traffic control:

The Google concept, called Project Wing, would enable people to get products delivered “in short order,” even in the most populated areas, Dave Vos, the project’s leader, said here today (July 29) at a NASA-sponsored conference on drones. Project Wing was first described publicly in August 2014, when test flights of early prototypes were conducted in Australia, The Atlantic reported.

In order to take to the skies, drones need to not only communicate with people on the ground, but also with other high-fliers that are delivering small packages, taking aerial surveys or doing other work, Vos said.

Key to this vision of a drone-filled future is the use of existing cellular phone infrastructure.

“We don’t need to develop new protocols,” Vos said at the conference.

In his vision, drones would be outfitted with an automatic dependent surveillance-broadcast (ADS-B) receiver that would enable the unmanned fliers to communicate with each other, as well as with ground-based systems. Existing ADS-B systems in aircraft allow them to locate their position using satellites, and then rebroadcast that location to a ground-based station. This type of multi-way communication could enable the drones to avoid obstacles in midflight and fly safely to their destination, Vos said.

A drone equivalent of air traffic control systems will also be needed, Vos said. Google envisions cellular carriers and other private companies collaborating with the Federal Aviation Administration (FAA) to craft a drone air traffic safety system.

Nowadays, of course, there are only two things worth reading: technology news and um, something else, probably. So here’s an insurance industry projection:

A black Volkswagen Golf rolls along at 12 mph on an empty road in the heart of Virginia’s horse country. Suddenly the dashboard lights up, and there’s a warning sound. The driver ignores it. A moment later, the VW brakes hard—all on its own—and comes to a stop a foot in front of an inflated box painted to look like the rear end of a car. The Insurance Institute for Highway Safety (IIHS) has been running tests like this a few times a month at its research center in Ruckersville, Va. The objective is to vet automakers’ latest crash avoidance technologies, like the one in the Golf, to identify the most effective ones.

The auto insurance industry is having its Napster moment. Like record companies at the dawn of online music file sharing, Allstate, Geico, State Farm, and others are grappling with innovations that could put a huge dent in their revenue. As carmakers automate more aspects of driving, accidents will likely plunge and car owners will need less coverage. Premiums consumers pay could drop as much as 60 percent in 15 years as self-driving cars hit the roads, says Donald Light, head of the North America property and casualty practice for Celent, a research firm. His message for insurers: “You have to be prepared to see that part of your business shrink, probably considerably.”

…

For example, a system introduced on the 2013 Honda Accord beeps when cars get too close to traffic ahead or leave their lane without signaling. It has had a measurable effect on the frequency of some types of claims: Bodily injury liability losses dropped 40 percent and medical payments decreased 27 percent, according to a 2014 study of insurance claims data by the Highway Loss Data Institute, IIHS’s sister organization.

…

The bottom line: Insurers collected $195 billion in auto premiums from U.S. drivers last year. By 2030, consumers could pay 60 percent less.

It was a grim day for the Canadian preferred share market, with PerpetualDiscounts losing 82bp, FixedResets down 42bp and DeemedRetractibles off 36bp. Floaters were taken outside and shot. The Performance Highlights table is lengthy. Volume was above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

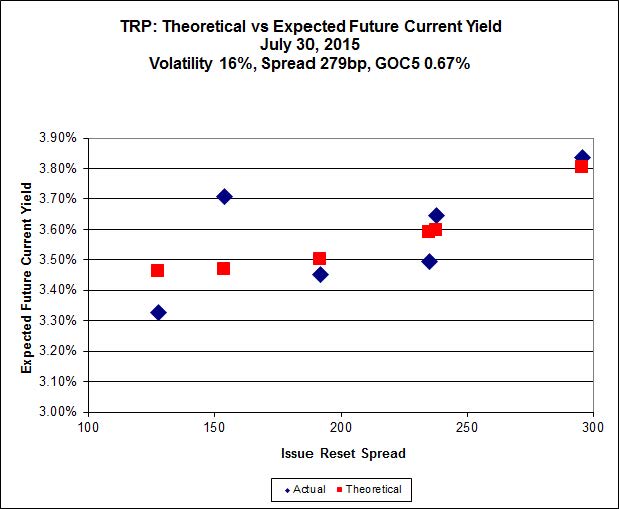

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 21.60 to be $0.58 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.04 cheap at its bid price of 14.90.

Click for Big

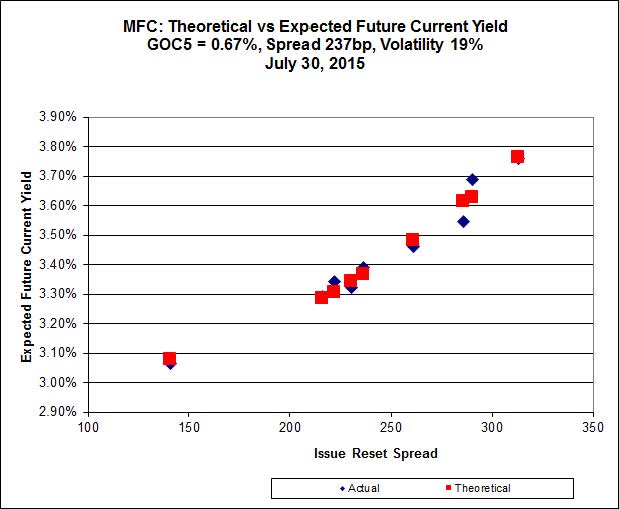

Another good fit today!

Most expensive is MFC.PR.I, resetting at +286bp on 2017-9-19, bid at 24.90 to be 0.48 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 24.21 to be $0.39 cheap.

Click for Big

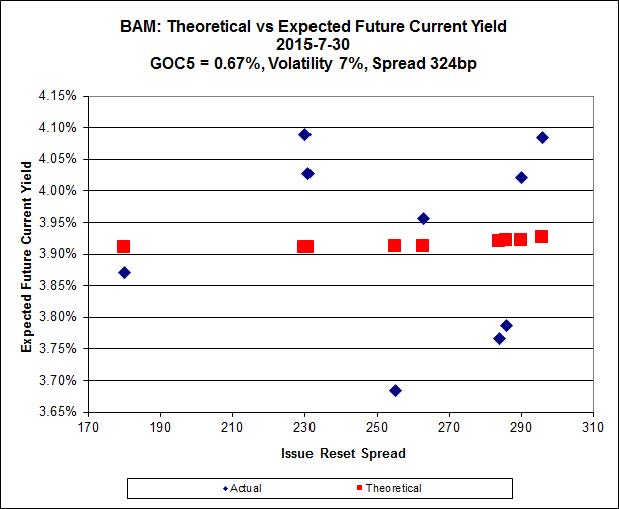

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 22.22 to be $0.89 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 21.85 and appears to be $1.27 rich.

Click for Big

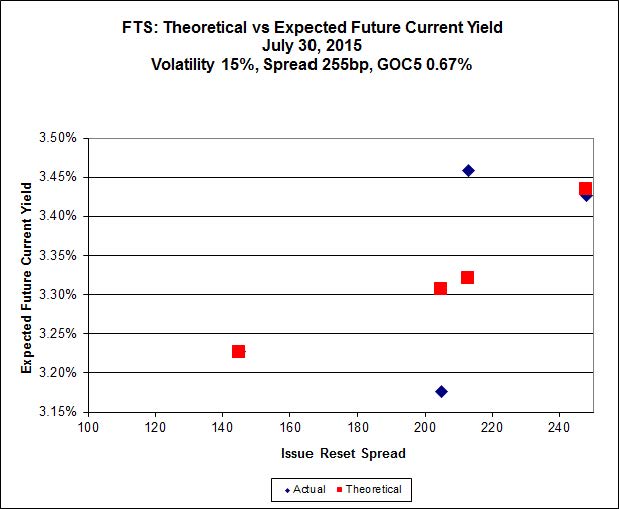

FTS.PR.K, with a spread of +205bp, and bid at 21.41, looks $0.84 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 20.24 and is $0.84 cheap.

Click for Big

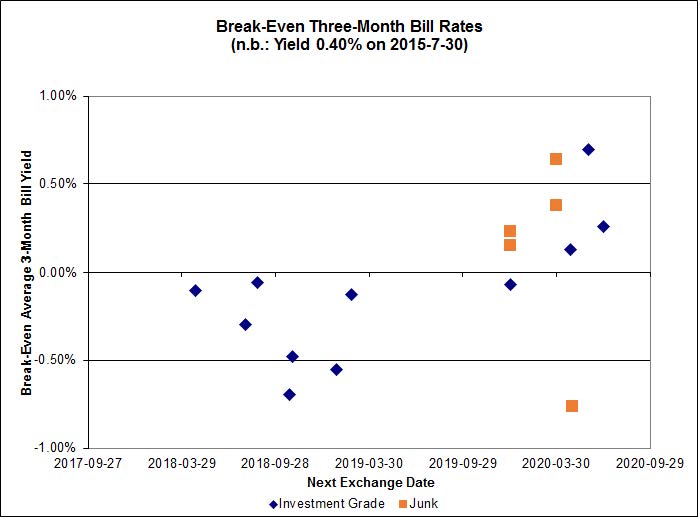

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of +0.03%, with one outlier above 1.00%. There is one junk outlier, also above +1.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -5.0559 % | 2,021.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -5.0559 % | 3,534.9 |

| Floater | 3.63 % | 3.66 % | 56,735 | 18.14 | 3 | -5.0559 % | 2,149.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1467 % | 2,781.1 |

| SplitShare | 4.57 % | 4.76 % | 61,537 | 3.17 | 3 | -0.1467 % | 3,259.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1467 % | 2,543.0 |

| Perpetual-Premium | 5.60 % | 5.48 % | 71,512 | 14.11 | 13 | -0.8312 % | 2,477.7 |

| Perpetual-Discount | 5.40 % | 5.40 % | 85,216 | 14.76 | 24 | -0.8233 % | 2,626.6 |

| FixedReset | 4.69 % | 3.82 % | 210,382 | 16.04 | 88 | -0.4211 % | 2,246.5 |

| Deemed-Retractible | 5.10 % | 5.17 % | 105,394 | 5.48 | 34 | -0.3644 % | 2,587.5 |

| FloatingReset | 2.40 % | 3.18 % | 46,922 | 6.05 | 10 | -0.3687 % | 2,268.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -7.69 % | Exaggerated, since the range for the day was 13.24-76, with a VWAP of 13.62 on volume of 3,681. It looks like a trade of 300 shares late in the day overwhelmed the market’s capacity to absorb selling pressure. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 12.72 Evaluated at bid price : 12.72 Bid-YTW : 3.74 % |

| PWF.PR.O | Perpetual-Premium | -7.34 % | Ridiculous, since the range for the day was 26.03-12 (VWAP 26.04) on volume of 3,300 shares. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.83 Evaluated at bid price : 24.12 Bid-YTW : 6.04 % |

| BAM.PR.B | Floater | -4.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 13.34 Evaluated at bid price : 13.34 Bid-YTW : 3.57 % |

| HSE.PR.E | FixedReset | -3.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.18 Evaluated at bid price : 22.80 Bid-YTW : 4.69 % |

| CU.PR.G | Perpetual-Discount | -3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 5.37 % |

| BAM.PR.C | Floater | -3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 13.00 Evaluated at bid price : 13.00 Bid-YTW : 3.66 % |

| ENB.PR.J | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.91 % |

| CU.PR.F | Perpetual-Discount | -2.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.39 % |

| BAM.PR.Z | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.97 Evaluated at bid price : 22.22 Bid-YTW : 4.24 % |

| MFC.PR.L | FixedReset | -2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 5.25 % |

| MFC.PR.C | Deemed-Retractible | -2.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 6.60 % |

| MFC.PR.B | Deemed-Retractible | -2.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.01 Bid-YTW : 6.46 % |

| TD.PF.F | Perpetual-Discount | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.35 Evaluated at bid price : 23.65 Bid-YTW : 5.20 % |

| ENB.PF.C | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 18.44 Evaluated at bid price : 18.44 Bid-YTW : 4.90 % |

| ENB.PR.B | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 16.30 Evaluated at bid price : 16.30 Bid-YTW : 4.87 % |

| TRP.PR.B | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.37 % |

| TRP.PR.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 3.71 % |

| ENB.PR.F | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 16.92 Evaluated at bid price : 16.92 Bid-YTW : 4.92 % |

| HSE.PR.G | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.90 Evaluated at bid price : 22.37 Bid-YTW : 4.80 % |

| MFC.PR.G | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.21 Bid-YTW : 4.14 % |

| RY.PR.J | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.69 Evaluated at bid price : 23.78 Bid-YTW : 3.50 % |

| POW.PR.B | Perpetual-Discount | -1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.95 Evaluated at bid price : 24.20 Bid-YTW : 5.57 % |

| ENB.PF.G | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 18.79 Evaluated at bid price : 18.79 Bid-YTW : 4.88 % |

| ENB.PF.E | FixedReset | -1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 18.49 Evaluated at bid price : 18.49 Bid-YTW : 4.92 % |

| GWO.PR.N | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.00 Bid-YTW : 7.45 % |

| FTS.PR.F | Perpetual-Discount | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.41 Evaluated at bid price : 23.68 Bid-YTW : 5.25 % |

| GWO.PR.R | Deemed-Retractible | -1.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.05 Bid-YTW : 5.98 % |

| TRP.PR.A | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 18.76 Evaluated at bid price : 18.76 Bid-YTW : 3.64 % |

| BAM.PR.X | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 15.95 Evaluated at bid price : 15.95 Bid-YTW : 4.17 % |

| RY.PR.N | Perpetual-Premium | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.67 Evaluated at bid price : 24.00 Bid-YTW : 5.17 % |

| TRP.PR.D | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 20.91 Evaluated at bid price : 20.91 Bid-YTW : 3.83 % |

| GWO.PR.I | Deemed-Retractible | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 6.28 % |

| RY.PR.Z | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.80 Evaluated at bid price : 22.15 Bid-YTW : 3.40 % |

| ENB.PR.D | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 4.84 % |

| SLF.PR.J | FloatingReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.06 Bid-YTW : 7.08 % |

| TD.PR.S | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.62 Bid-YTW : 3.04 % |

| POW.PR.D | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.69 Evaluated at bid price : 22.98 Bid-YTW : 5.47 % |

| RY.PR.M | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.58 Evaluated at bid price : 23.62 Bid-YTW : 3.44 % |

| CM.PR.O | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.19 Evaluated at bid price : 22.75 Bid-YTW : 3.41 % |

| PWF.PR.S | Perpetual-Discount | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.45 Evaluated at bid price : 22.85 Bid-YTW : 5.26 % |

| BMO.PR.Q | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.56 Bid-YTW : 3.79 % |

| TD.PF.E | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.97 Evaluated at bid price : 24.51 Bid-YTW : 3.51 % |

| ENB.PR.T | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 17.33 Evaluated at bid price : 17.33 Bid-YTW : 4.85 % |

| HSE.PR.C | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.66 Evaluated at bid price : 22.00 Bid-YTW : 4.49 % |

| NA.PR.S | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 22.30 Evaluated at bid price : 22.90 Bid-YTW : 3.47 % |

| BIP.PR.A | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.64 Evaluated at bid price : 22.00 Bid-YTW : 4.88 % |

| NA.PR.W | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 21.32 Evaluated at bid price : 21.60 Bid-YTW : 3.56 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.Z | Perpetual-Discount | 282,348 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 23.49 Evaluated at bid price : 23.81 Bid-YTW : 5.27 % |

| BMO.PR.R | FloatingReset | 107,377 | Anonymous crossed 100,400 at 23.15. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 3.18 % |

| TRP.PR.B | FixedReset | 86,020 | Scotia crossed 80,000 at 14.95. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.37 % |

| ENB.PR.Y | FixedReset | 65,913 | RBC crossed 50,000 at 17.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 17.29 Evaluated at bid price : 17.29 Bid-YTW : 4.74 % |

| ENB.PR.F | FixedReset | 60,058 | RBC crossed 47,700 at 17.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 16.92 Evaluated at bid price : 16.92 Bid-YTW : 4.92 % |

| ENB.PR.H | FixedReset | 47,166 | TD crossed 22,500 at 15.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-07-30 Maturity Price : 15.85 Evaluated at bid price : 15.85 Bid-YTW : 4.75 % |

| There were 37 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.O | Perpetual-Premium | Quote: 24.12 – 26.13 Spot Rate : 2.0100 Average : 1.1237 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 22.22 – 23.05 Spot Rate : 0.8300 Average : 0.6048 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 12.72 – 13.24 Spot Rate : 0.5200 Average : 0.3686 YTW SCENARIO |

| CM.PR.O | FixedReset | Quote: 22.75 – 23.13 Spot Rate : 0.3800 Average : 0.2441 YTW SCENARIO |

| TD.PR.S | FixedReset | Quote: 24.62 – 25.00 Spot Rate : 0.3800 Average : 0.2442 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 19.45 – 20.00 Spot Rate : 0.5500 Average : 0.4171 YTW SCENARIO |