Swap spreads are below zero:

At the height of the financial crisis, the unprecedented decline in swap rates below Treasury yields was seen as an anomaly. The phenomenon is now widespread.

Swap rates are what companies, investors and traders pay to exchange fixed interest payments for floating ones. That rate falling below Treasury yields — the spread between the two being negative — is illogical in the eyes of most market observers, because it theoretically signals that traders view the credit of banks as superior to that of the U.S. government.

Back in 2009, it was only negative in the 30-year maturity, a temporary offshoot of deleveraging and market swings following the credit crisis. These days, swap spreads are near or below zero across maturities.

…

If the flip to negative spreads persists, it would signal that its roots are in regulators’ efforts to head off another financial crisis, according to Kohli.Regulatory moves such as higher capital requirements have led banks to curtail market-making, crimping liquidity and driving repurchase agreement rates above bank funding benchmarks. Repo rates factor into Treasuries pricing because they’re considered the cost of financing positions in government debt.

There’s a very peculiar suggestion regarding ETF trading:

A group of high-frequency trading firms advised U.S. regulators on how to prevent a repeat of the wild Aug. 24 trading session that roiled hundreds of securities, leaving exchange-traded funds’ prices out of sync with the values of their assets.

In a Sept. 24 letter to the Securities and Exchange Commission, the industry group Modern Markets Initiative proposed three main solutions to prevent problems with prices of ETFs: clarifying rules for canceling trades, loosening short-selling restrictions so arbitragers can better hedge, and protecting small investors by preventing their ETF orders from executing when the price of those securities becomes detached from their underlying stocks.

…

Finally, the Modern Markets Initiative letter proposed protecting retail investors during times when ETFs diverge from their underlying stocks. If, for example, the ETF’s price is 5 percent or more away from the NAV, small investors’ orders wouldn’t be executed.

Huh? Restricting retail access to the marketplace? Well, just about anything’s possible these days…

After yesterday‘s massive losses, a lot of preferred share investors were hoping the market would come back. Be careful what you wish for …

Click for Big

The Canadian preferred share market was crushed again today, with PerpetualDiscounts down 74bp, FixedResets losing 97bp and DeemedRetractibles off 34bp; numbers that look mild only in comparison with yesterday. The Performance Highlights table is, of course, horrific and dominated by losing FixedResets, although a number of issues bounced back from yesterday’s quotes far enough to make it onto the good part of the table. Volume was very heavy and notable for blocks of NVCC non-compliant bank FloatingResets.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

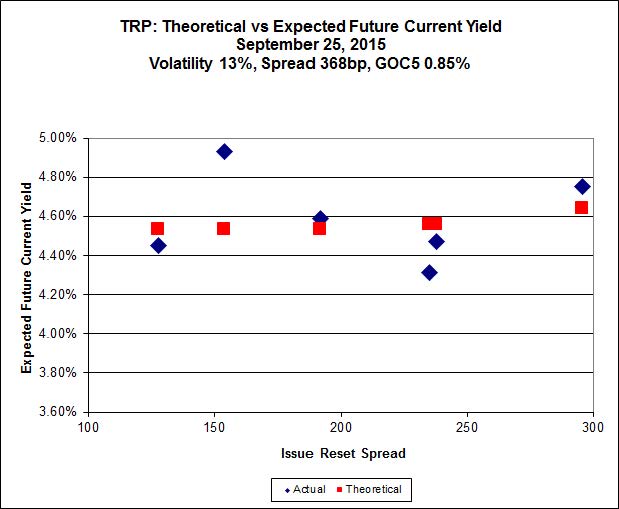

Here’s TRP:

Click for Big

Implied Volatility jumped today.

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.56 to be $1.00 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.07 cheap at its bid price of 12.12.

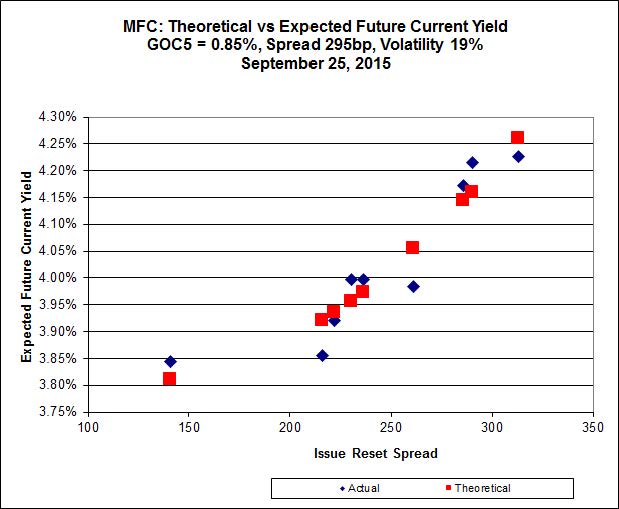

Click for Big

Another good fit today for MFC, with Implied Volatility falling back a little after yesterday’s jump.

Most expensive is MFC.PR.J, resetting at +261bp on 2018-3-19, bid at 21.71 to be 0.38 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 22.24 to be 0.30 cheap.

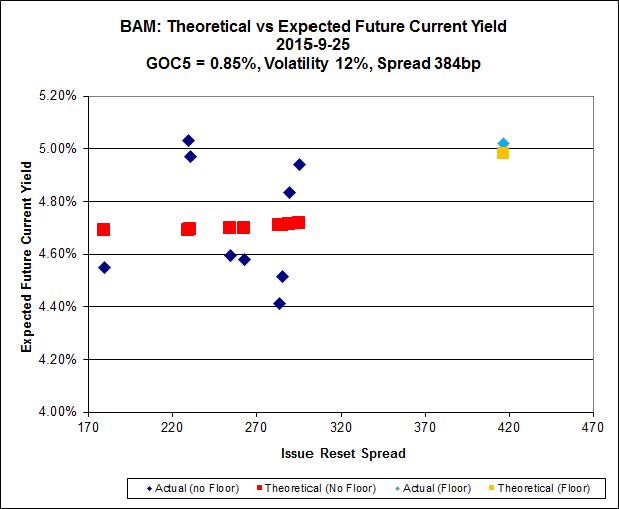

Click for Big

The fit on the BAM issues continues to be horrible. Note that the pending new issue has been added with a price of 25.00; the valuation effects of the rate floor have been ignored.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.70 to be $1.14 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.90 and appears to be $1.31 rich.

Click for Big

FTS.PR.M, with a spread of +248bp, and bid at 20.20, looks $0.70 expensive and resets 2019-12-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 16.50 and is $0.48 cheap.

Click for Big

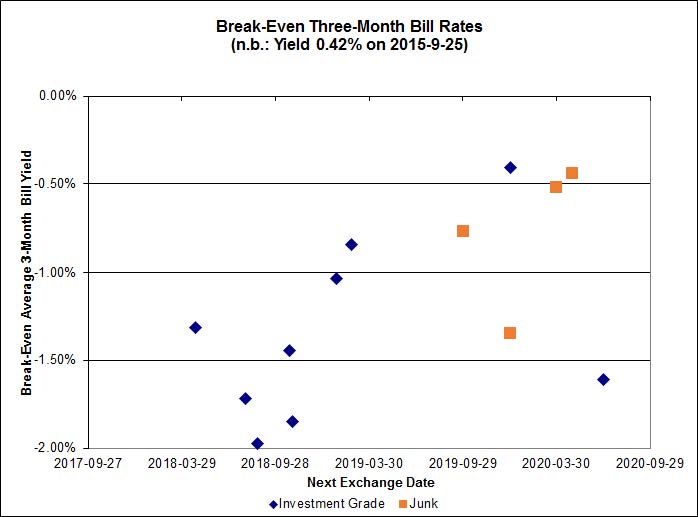

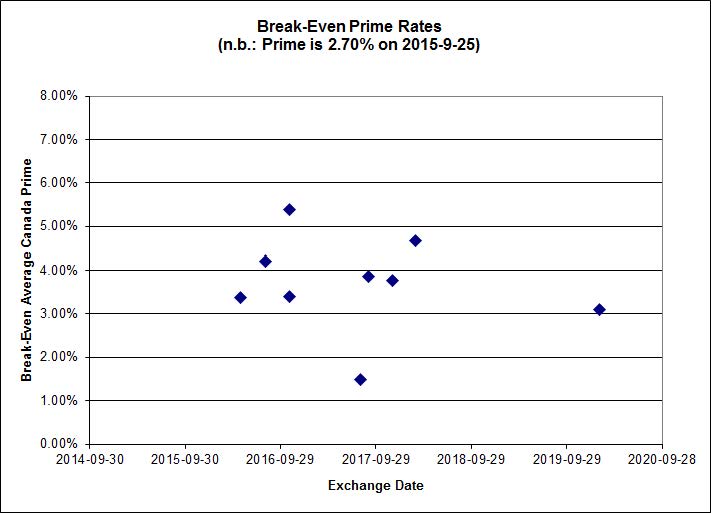

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.98%, with three outliers above 0.00%. The distribution’s bimodality has returned, with bank NVCC non-compliant pairs averaging -1.45% and other issues averaging -0.32%. There are two junk outliers above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.8629 % | 1,653.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.8629 % | 2,891.7 |

| Floater | 4.49 % | 4.48 % | 61,265 | 16.45 | 3 | 0.8629 % | 1,758.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0737 % | 2,766.9 |

| SplitShare | 4.49 % | 4.90 % | 65,029 | 3.04 | 4 | -0.0737 % | 3,242.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0737 % | 2,530.0 |

| Perpetual-Premium | 5.75 % | 4.24 % | 59,600 | 0.08 | 8 | 0.2690 % | 2,489.4 |

| Perpetual-Discount | 5.63 % | 5.71 % | 71,309 | 14.28 | 30 | -0.7389 % | 2,519.6 |

| FixedReset | 5.02 % | 4.65 % | 180,238 | 15.37 | 75 | -0.9669 % | 2,023.9 |

| Deemed-Retractible | 5.23 % | 5.09 % | 95,901 | 5.48 | 33 | -0.3399 % | 2,539.6 |

| FloatingReset | 2.56 % | 4.36 % | 60,575 | 5.87 | 9 | 0.4915 % | 2,092.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| NA.PR.S | FixedReset | -5.95 % | This is real enough! The issue traded 7,935 shares today in a range of 19.60-21.00, with a series of seventeen trades totalling 4,500 shares starting at 3:20pm at 20.10 declining slowly but surely down to 19.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.60 Evaluated at bid price : 19.60 Bid-YTW : 4.37 % |

| TRP.PR.G | FixedReset | -4.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 4.76 % |

| IAG.PR.G | FixedReset | -4.54 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.25 Bid-YTW : 5.92 % |

| PWF.PR.L | Perpetual-Discount | -4.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 21.75 Evaluated at bid price : 21.99 Bid-YTW : 5.89 % |

| BMO.PR.T | FixedReset | -4.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.26 % |

| RY.PR.J | FixedReset | -4.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 4.28 % |

| CM.PR.P | FixedReset | -4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.66 Evaluated at bid price : 18.66 Bid-YTW : 4.30 % |

| FTS.PR.K | FixedReset | -4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 4.70 % |

| TRP.PR.E | FixedReset | -3.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.56 Evaluated at bid price : 18.56 Bid-YTW : 4.66 % |

| CM.PR.O | FixedReset | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.54 Evaluated at bid price : 19.54 Bid-YTW : 4.21 % |

| RY.PR.M | FixedReset | -3.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 4.21 % |

| BMO.PR.S | FixedReset | -3.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 4.24 % |

| BNS.PR.D | FloatingReset | -3.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.25 Bid-YTW : 5.75 % |

| TRP.PR.D | FixedReset | -3.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 4.72 % |

| BMO.PR.W | FixedReset | -3.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.23 % |

| RY.PR.H | FixedReset | -2.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.43 Evaluated at bid price : 19.43 Bid-YTW : 4.21 % |

| BMO.PR.Z | Perpetual-Discount | -2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 22.94 Evaluated at bid price : 23.34 Bid-YTW : 5.43 % |

| BNS.PR.Y | FixedReset | -2.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.95 Bid-YTW : 5.72 % |

| TD.PF.C | FixedReset | -2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 4.33 % |

| VNR.PR.A | FixedReset | -2.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.87 Evaluated at bid price : 18.87 Bid-YTW : 5.01 % |

| RY.PR.Z | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 4.17 % |

| MFC.PR.F | FixedReset | -2.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.70 Bid-YTW : 9.04 % |

| CU.PR.H | Perpetual-Discount | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 22.87 Evaluated at bid price : 23.25 Bid-YTW : 5.72 % |

| SLF.PR.J | FloatingReset | -2.31 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.70 Bid-YTW : 10.01 % |

| BAM.PR.M | Perpetual-Discount | -2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 5.96 % |

| TD.PF.B | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.44 Evaluated at bid price : 19.44 Bid-YTW : 4.21 % |

| MFC.PR.M | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.08 Bid-YTW : 6.41 % |

| SLF.PR.C | Deemed-Retractible | -1.96 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.00 Bid-YTW : 7.50 % |

| CU.PR.C | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.61 Evaluated at bid price : 19.61 Bid-YTW : 4.22 % |

| FTS.PR.M | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 4.33 % |

| SLF.PR.D | Deemed-Retractible | -1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.06 Bid-YTW : 7.45 % |

| BAM.PR.X | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 14.57 Evaluated at bid price : 14.57 Bid-YTW : 4.83 % |

| FTS.PR.J | Perpetual-Discount | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.86 Evaluated at bid price : 20.86 Bid-YTW : 5.76 % |

| BAM.PF.D | Perpetual-Discount | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.01 % |

| PWF.PR.P | FixedReset | -1.87 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 14.72 Evaluated at bid price : 14.72 Bid-YTW : 4.21 % |

| BIP.PR.A | FixedReset | -1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 5.25 % |

| SLF.PR.B | Deemed-Retractible | -1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.27 Bid-YTW : 7.04 % |

| BNS.PR.Z | FixedReset | -1.84 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.23 Bid-YTW : 6.09 % |

| NA.PR.W | FixedReset | -1.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.33 % |

| BAM.PF.E | FixedReset | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.93 % |

| TD.PF.A | FixedReset | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.50 Evaluated at bid price : 19.50 Bid-YTW : 4.21 % |

| BAM.PR.Z | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.28 Evaluated at bid price : 19.28 Bid-YTW : 5.10 % |

| GWO.PR.H | Deemed-Retractible | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.90 Bid-YTW : 6.69 % |

| TRP.PR.A | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 15.09 Evaluated at bid price : 15.09 Bid-YTW : 4.76 % |

| FTS.PR.G | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 4.57 % |

| CM.PR.Q | FixedReset | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 21.55 Evaluated at bid price : 21.55 Bid-YTW : 4.17 % |

| BAM.PF.A | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 4.98 % |

| TRP.PR.F | FloatingReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 13.57 Evaluated at bid price : 13.57 Bid-YTW : 4.22 % |

| MFC.PR.I | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.23 Bid-YTW : 5.40 % |

| TD.PF.F | Perpetual-Discount | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 23.13 Evaluated at bid price : 23.55 Bid-YTW : 5.27 % |

| MFC.PR.C | Deemed-Retractible | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.45 Bid-YTW : 7.27 % |

| POW.PR.G | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 23.82 Evaluated at bid price : 24.30 Bid-YTW : 5.75 % |

| TRP.PR.C | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 12.12 Evaluated at bid price : 12.12 Bid-YTW : 5.00 % |

| PVS.PR.B | SplitShare | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.36 Bid-YTW : 5.31 % |

| BMO.PR.Q | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 5.62 % |

| TD.PR.S | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.26 Bid-YTW : 3.49 % |

| GWO.PR.R | Deemed-Retractible | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.85 Bid-YTW : 6.66 % |

| BAM.PF.G | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 4.65 % |

| BAM.PR.T | FixedReset | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 15.90 Evaluated at bid price : 15.90 Bid-YTW : 5.14 % |

| NA.PR.Q | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.79 Bid-YTW : 4.42 % |

| FTS.PR.H | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 13.61 Evaluated at bid price : 13.61 Bid-YTW : 4.30 % |

| SLF.PR.H | FixedReset | 1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.80 Bid-YTW : 7.44 % |

| TD.PR.Z | FloatingReset | 1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.22 % |

| TD.PR.T | FloatingReset | 2.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.13 % |

| POW.PR.A | Perpetual-Premium | 2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 24.30 Evaluated at bid price : 24.61 Bid-YTW : 5.69 % |

| HSE.PR.E | FixedReset | 3.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 21.44 Evaluated at bid price : 21.70 Bid-YTW : 5.09 % |

| IFC.PR.C | FixedReset | 3.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.25 Bid-YTW : 6.96 % |

| BMO.PR.R | FloatingReset | 3.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 4.38 % |

| MFC.PR.N | FixedReset | 6.49 % | Simply a reversal of the idiotic part of yesterday‘s ridiculous move, which was due to a bad quote. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.70 Bid-YTW : 6.59 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.R | FloatingReset | 142,656 | Scotia crossed 100,000 at 21.90; TD crossed 40,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.75 Bid-YTW : 4.38 % |

| CU.PR.I | FixedReset | 97,505 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-25 Maturity Price : 23.19 Evaluated at bid price : 25.12 Bid-YTW : 4.38 % |

| BNS.PR.B | FloatingReset | 75,500 | Scotia crossed blocks of 50,000 and 25,000, both at 21.85. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.80 Bid-YTW : 4.40 % |

| TD.PR.Z | FloatingReset | 52,340 | TD crossed 49,400 at 22.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.22 % |

| TD.PR.T | FloatingReset | 50,000 | TD crossed 49,300 at 22.10. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 4.13 % |

| GWO.PR.Q | Deemed-Retractible | 39,557 | Scotia crossed 25,000 at 22.90. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.52 Bid-YTW : 6.62 % |

| There were 52 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.L | Perpetual-Discount | Quote: 21.99 – 23.15 Spot Rate : 1.1600 Average : 0.6728 YTW SCENARIO |

| TRP.PR.G | FixedReset | Quote: 20.05 – 21.20 Spot Rate : 1.1500 Average : 0.7773 YTW SCENARIO |

| BSC.PR.C | SplitShare | Quote: 19.71 – 20.43 Spot Rate : 0.7200 Average : 0.3909 YTW SCENARIO |

| BAM.PF.D | Perpetual-Discount | Quote: 20.50 – 21.50 Spot Rate : 1.0000 Average : 0.6848 YTW SCENARIO |

| BNS.PR.D | FloatingReset | Quote: 19.25 – 19.85 Spot Rate : 0.6000 Average : 0.3580 YTW SCENARIO |

| BNS.PR.Y | FixedReset | Quote: 19.95 – 20.50 Spot Rate : 0.5500 Average : 0.3348 YTW SCENARIO |