The regulatory push to move trading jobs offshore is showing signs of success:

The $13.2 trillion Treasuries market is getting pushed around more by global developments, the [JPMorgan] analysts wrote in a note titled “24 hour party people redux: Global liquidity in U.S. Treasury futures.”

…

Sleep-deprived Wall Street traders aren’t the only ones who should care. It underscores the changing structure of a market where plenty of strange distortions are happening, the analysts said.Bond dealers’ trading books are smaller than before the financial crisis, and new regulations are making it more expensive to facilitate trades and provide some types of overnight financing. On top of that, reserve managers at global central banks sold more U.S. debt to raise cash last year, which put more pressure on the balance sheets of the dealers handling that business, the analysts said.

As a result, more trading is happening in futures relative to cash Treasuries, according to the note, since futures transactions don’t require banks to use their balance sheets. For one 10-year Treasury futures contract, about 5 percent of its volume comes around the open of trading in Tokyo and more than 25 percent is traded around the open in London, the analysts said.

To my dismay, the NYT has endorsed a Tobin Tax:

A well-designed financial transaction tax — one that applies a tiny tax rate to an array of transactions and is split between buyers and sellers — would be a progressive way to raise substantial revenue without damaging the markets. A new study by researchers at the nonpartisan Tax Policy Center has found that a 0.1 percent tax rate could bring in $66 billion a year, with 40 percent coming from the top 1 percent of income earners and 75 percent from the top 20 percent. As the rate rises, however, traders would most likely curtail their activity. The tax could bring in $76 billion a year if it was set at 0.3 percent, but above that rate, trading would probably decrease and the total revenue raised would start to fall.

The burden of this tax would be concentrated at the top, because that’s where the ownership of financial assets is concentrated.

…

Critics also contend that a financial transaction tax would have damaging effects on trade volume, volatility and the ability of markets to determine asset prices. That is debatable, and setting the tax rate low at first, and raising it gradually, would help avoid potential damage. But the possibility of unintended consequences is not the real obstacle to a broad and prudent financial transaction tax. It is that a majority of lawmakers are not willing to challenge Wall Street’s power. Imposing the tax will take leadership from the next president.

My opposition to a Tobin tax was last discussed on December 29, 2015.

A link in Ken Kivenko’s Fund Observer led me to an exhortation from the Consumers Council of Canada, which led me to an OSC-commissioned report titled Current Practices for Risk Profiling in Canada And Review of Global Best Practices, which led me to a Morningstar paper titled Variable Risk Preference Bias:

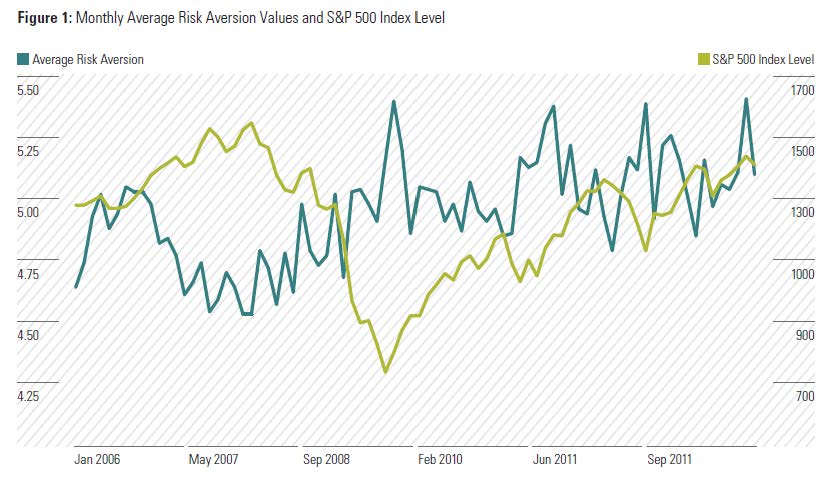

The average monthly risk aversion scores from our dataset are shown in Figure 1 along with the S&P 500 Index to illustrate the relation between stock returns and risk aversion over time.

Click for Big

The OSC report claims that:

Guillemette and Finke (2014) find that the correlation between a popular risk tolerance assessment score and the S&P 500 was 0.90 (or nearly perfect) during the January 2007 through March 2009 bear market, but then only 0.01 between the remainder of 2009 and April 2012. A review of scores from a 3-question risk tolerance instrument given to employees participating in Morningstar’s Managed Account program shows a similar correlation between S&P values and measured risk tolerance.

So that was kind of interesting. But what made me laugh was the paragraph in the Morningstar report that read:

Differences in the method of compensation provided through share class structure may influence whether the advisor gains from de-biasing a client who is tempted to shift his or her portfolio to safety during an equity market decline. Class A shares compensate the advisor through the payment of an upfront load. Advisors may have an incentive to encourage a client to buy a safer fund (and pay a front-end load) when they feel more risk averse and then sell them another risky fund when their risk aversion declines after prices rise. This provides a disincentive to de-bias a client. Advisors who receive compensation through higher trail commissions (C shares) have no incentive to encourage a client to shift out of risky funds during a temporary increase in risk aversion. Higher trail compensation may provide a valuable de-biasing incentive since the advisor does not need to sell a new fund to receive compensation. We hypothesize that lower 12b-1 fees lead to an incentive for advisors not to de-bias clients since their compensation is increased by catering to investor variable risk preferences by selling them new funds. For example, if the stock market falls and the client becomes more risk averse, an advisor compensated through front-end commissions has a greater incentive to move that client into bonds than an advisor who receives more commissions on a trail basis.

Granted, this is in the context of a comparison between transaction-based and asset-based fees, but it still made me laugh. I don’t think that part will be cited in an OSC report any time soon! However, the Morningstar paper also led me to a paper published by the Chicago Fed titled From the Horse’s Mouth: How do Investor Expectations of Risk and Return Vary with Economic Conditions?:

Data obtained from monthly Gallup/UBS surveys from 1998-2007 and from a special supplement to the Michigan Surveys of Consumer Attitudes, run in 22 monthly surveys between 2000-2005, are used to analyze stock market beliefs and portfolio choices of household investors. We show that the key variables found to be positive predictors of actual stock returns in the asset-pricing literature are also highly correlated with investor’s reported expected returns, but with the opposite sign. Moreover, analysis of the micro data indicates that expectations of both risk and returns on stocks are strongly influenced by perceptions of economic conditions. In particular, when investors believe macroeconomic conditions are more expansionary, they tend to expect both higher returns and lower volatility. This is difficult to reconcile with the canonical view that expected returns on stocks rise during recessions to compensate household investors for increased exposure or sensitivity to macroeconomic risks. Finally, the relevance of these investors’ reported expectations is supported by the finding of a significant link between their expectations and portfolio choices. In particular, we show that portfolio equity positions tend to be higher for those respondents that anticipate higher expected returns or lower uncertainty.

So it’s all interesting and goes a long way towards providing comfort that the ‘people are selling because the market is down’ hypothesis has at least some basis in fact.

Here’s a good illustration about how empty-headed regulatory do-goodism can reduce civil liberties while inflating university costs:

The online admissions application for Auburn University appears simple, until you get to this question on Page 7:

“Have you ever been charged with or convicted of or pled guilty or nolo contendere to a crime other than a minor traffic offense, or are there any criminal charges now pending against you?”

Those who check “yes,” even though they have never been convicted of any crime, face extra scrutiny — a follow-up call from the admissions office asking for additional information, the university says.

…

“Lots of colleges and universities don’t like the fact that they feel like they have to ask these questions,” said Michael Reilly, the executive director of the American Association of Collegiate Registrars and Admissions Officers. “But they feel like they do, just because of how prominent some of these cases are of things like sexual assault on college campuses. And they feel like they need to do what they can to screen students.”

It was a very good day for the Canadian preferred share market, with PerpetualDiscounts winning 80bp, FixedResets up 64bp and DeemedRetractibles gaining 36bp. There are lots of winners in the Performance Highlights table! Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

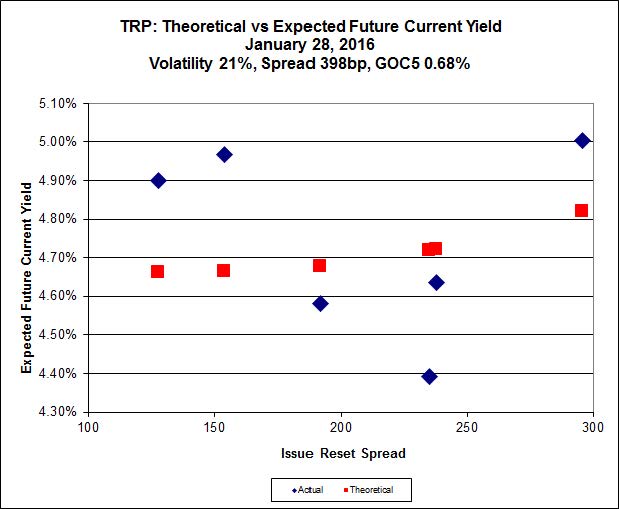

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.25 to be $1.20 rich, while TRP.PR.C, resetting 2021-1-30 at +154, is $0.73 cheap at its bid price of 11.17.

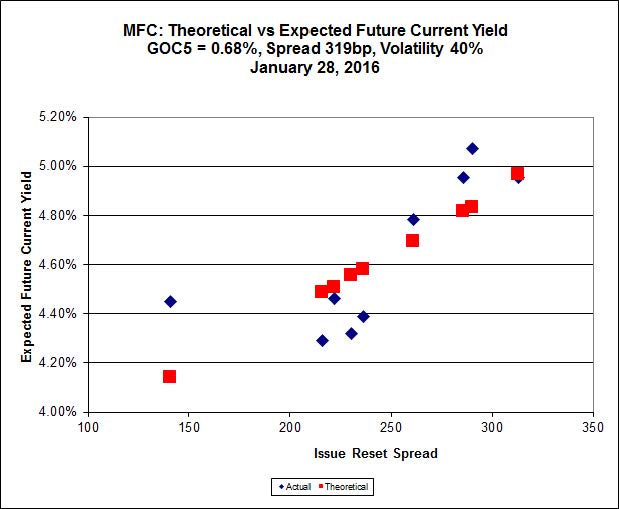

Click for Big

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 17.25 to be 0.89 rich, while MFC.PR.F, resetting at +141bp on 2016-6-19, is bid at 11.74 to be 0.88 cheap.

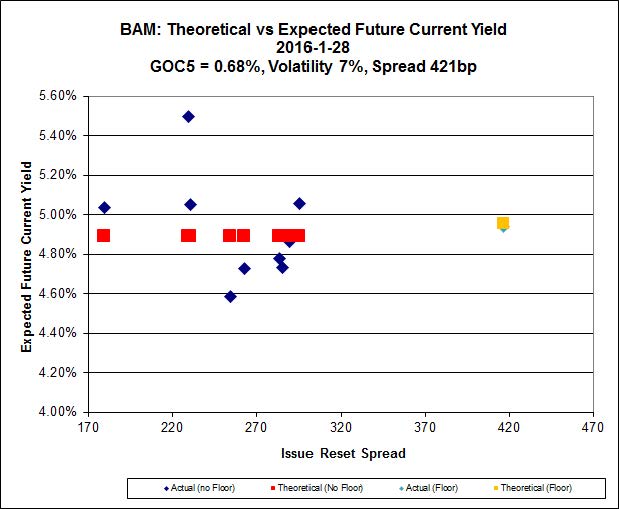

Click for Big

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.55 to be $1.69 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.61 and appears to be $1.10 rich.

Click for Big

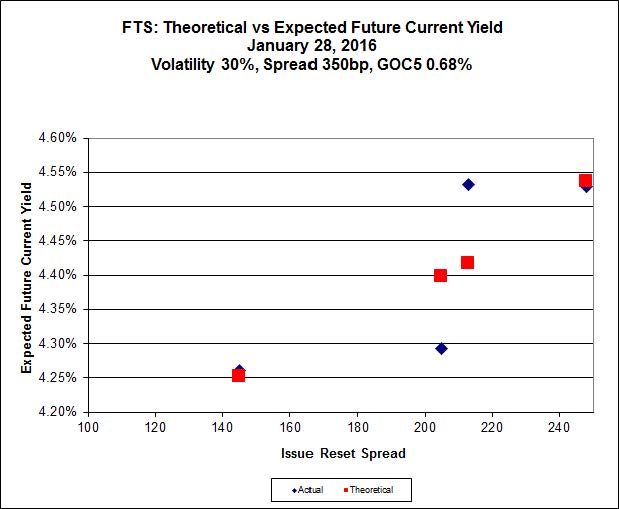

FTS.PR.K, with a spread of +205bp, and bid at 15.90, looks $0.38 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.50 and is $0.41 cheap.

Click for Big

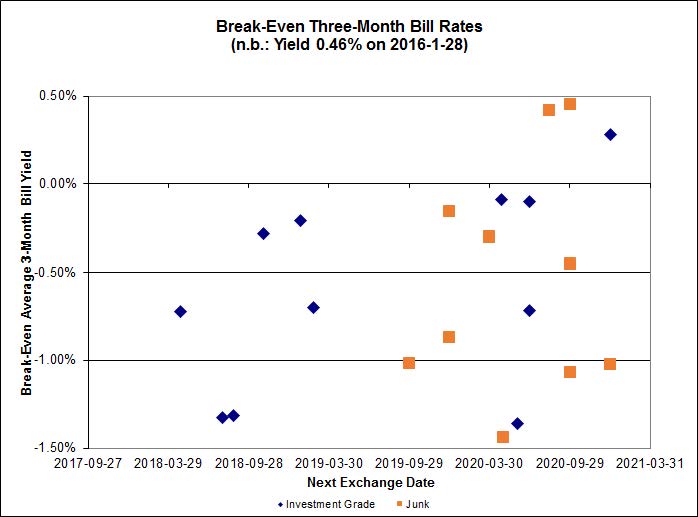

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.81%, with two outliers below -1.50%. There are no junk outliers.

Click for Big

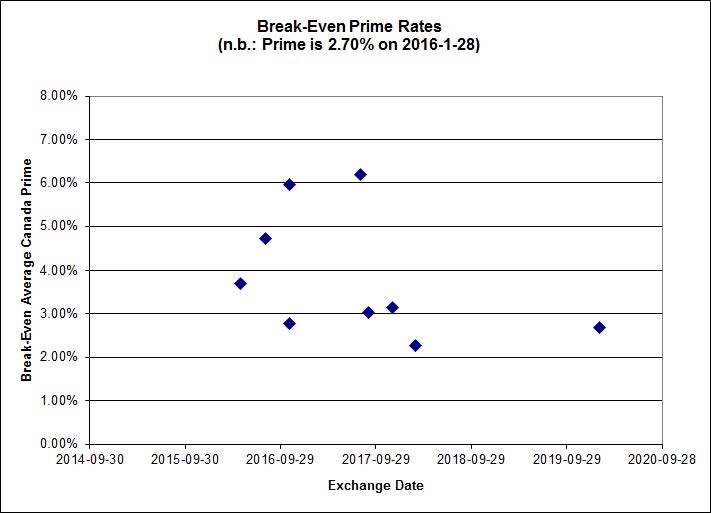

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.30 % | 6.43 % | 19,181 | 16.17 | 1 | -1.6154 % | 1,473.5 |

| FixedFloater | 7.66 % | 6.69 % | 28,181 | 15.59 | 1 | 0.6494 % | 2,595.0 |

| Floater | 4.65 % | 4.79 % | 72,305 | 15.86 | 4 | 2.5492 % | 1,648.3 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3275 % | 2,684.9 |

| SplitShare | 4.92 % | 6.90 % | 81,025 | 2.71 | 6 | -0.3275 % | 3,141.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3275 % | 2,451.4 |

| Perpetual-Premium | 5.92 % | 5.89 % | 84,349 | 13.87 | 6 | 0.1146 % | 2,494.6 |

| Perpetual-Discount | 5.86 % | 5.91 % | 101,914 | 14.00 | 33 | 0.7968 % | 2,459.4 |

| FixedReset | 5.66 % | 5.05 % | 237,273 | 14.62 | 83 | 0.6386 % | 1,823.6 |

| Deemed-Retractible | 5.29 % | 5.78 % | 134,694 | 6.95 | 34 | 0.3613 % | 2,552.0 |

| FloatingReset | 2.98 % | 4.67 % | 58,561 | 5.57 | 13 | 0.1107 % | 2,016.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.H | FloatingReset | -2.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 9.13 Evaluated at bid price : 9.13 Bid-YTW : 4.81 % |

| PWF.PR.A | Floater | -2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 10.90 Evaluated at bid price : 10.90 Bid-YTW : 4.33 % |

| CCS.PR.C | Deemed-Retractible | -2.09 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.07 Bid-YTW : 7.54 % |

| GWO.PR.N | FixedReset | -2.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.90 Bid-YTW : 11.77 % |

| CIU.PR.C | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 10.39 Evaluated at bid price : 10.39 Bid-YTW : 5.14 % |

| BNS.PR.L | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.61 Bid-YTW : 5.63 % |

| BAM.PR.E | Ratchet | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 25.00 Evaluated at bid price : 12.79 Bid-YTW : 6.43 % |

| FTS.PR.M | FixedReset | -1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.44 Evaluated at bid price : 17.44 Bid-YTW : 4.94 % |

| PWF.PR.H | Perpetual-Premium | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 23.71 Evaluated at bid price : 24.02 Bid-YTW : 6.01 % |

| MFC.PR.H | FixedReset | -1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.22 Bid-YTW : 7.66 % |

| PVS.PR.C | SplitShare | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2017-12-10 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 6.89 % |

| CM.PR.Q | FixedReset | -1.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 4.70 % |

| TD.PR.T | FloatingReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.82 Bid-YTW : 4.43 % |

| BNS.PR.B | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 5.22 % |

| BNS.PR.D | FloatingReset | -1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.42 Bid-YTW : 6.83 % |

| SLF.PR.H | FixedReset | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.10 Bid-YTW : 10.72 % |

| RY.PR.E | Deemed-Retractible | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 5.25 % |

| GWO.PR.I | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.71 Bid-YTW : 7.21 % |

| MFC.PR.F | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.74 Bid-YTW : 12.15 % |

| RY.PR.I | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.41 Bid-YTW : 4.29 % |

| PWF.PR.E | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 23.09 Evaluated at bid price : 23.35 Bid-YTW : 5.91 % |

| NA.PR.W | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 16.51 Evaluated at bid price : 16.51 Bid-YTW : 4.81 % |

| RY.PR.N | Perpetual-Discount | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 21.84 Evaluated at bid price : 22.18 Bid-YTW : 5.51 % |

| BAM.PF.H | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 4.84 % |

| SLF.PR.C | Deemed-Retractible | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.74 Bid-YTW : 7.14 % |

| GWO.PR.G | Deemed-Retractible | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.82 Bid-YTW : 6.60 % |

| TRP.PR.E | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.82 % |

| TRP.PR.F | FloatingReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 11.57 Evaluated at bid price : 11.57 Bid-YTW : 5.20 % |

| BMO.PR.M | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.48 Bid-YTW : 3.93 % |

| TRP.PR.B | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 10.00 Evaluated at bid price : 10.00 Bid-YTW : 5.13 % |

| TRP.PR.A | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 14.19 Evaluated at bid price : 14.19 Bid-YTW : 4.93 % |

| CU.PR.G | Perpetual-Discount | 1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 5.97 % |

| HSE.PR.E | FixedReset | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 14.52 Evaluated at bid price : 14.52 Bid-YTW : 7.60 % |

| BIP.PR.A | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 6.35 % |

| MFC.PR.N | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.25 Bid-YTW : 8.54 % |

| NA.PR.S | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.06 Evaluated at bid price : 17.06 Bid-YTW : 4.83 % |

| HSE.PR.C | FixedReset | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 13.76 Evaluated at bid price : 13.76 Bid-YTW : 7.41 % |

| MFC.PR.C | Deemed-Retractible | 1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.78 Bid-YTW : 7.19 % |

| CU.PR.F | Perpetual-Discount | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.45 Evaluated at bid price : 19.45 Bid-YTW : 5.89 % |

| RY.PR.F | Deemed-Retractible | 1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.97 Bid-YTW : 5.22 % |

| CU.PR.H | Perpetual-Discount | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 22.26 Evaluated at bid price : 22.55 Bid-YTW : 5.91 % |

| BMO.PR.Q | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.56 Bid-YTW : 7.39 % |

| CU.PR.E | Perpetual-Discount | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.93 % |

| BAM.PR.N | Perpetual-Discount | 1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.03 Evaluated at bid price : 19.03 Bid-YTW : 6.32 % |

| BNS.PR.C | FloatingReset | 1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.07 Bid-YTW : 4.51 % |

| FTS.PR.H | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 4.55 % |

| GWO.PR.Q | Deemed-Retractible | 1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.98 Bid-YTW : 6.44 % |

| TD.PF.C | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.35 Evaluated at bid price : 17.35 Bid-YTW : 4.53 % |

| ELF.PR.G | Perpetual-Discount | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 5.89 % |

| IFC.PR.C | FixedReset | 1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.19 Bid-YTW : 9.41 % |

| BAM.PF.D | Perpetual-Discount | 1.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 6.36 % |

| MFC.PR.K | FixedReset | 1.88 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.25 Bid-YTW : 9.13 % |

| RY.PR.K | FloatingReset | 2.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.83 Bid-YTW : 4.76 % |

| CU.PR.D | Perpetual-Discount | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 20.97 Evaluated at bid price : 20.97 Bid-YTW : 5.95 % |

| MFC.PR.L | FixedReset | 2.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.55 Bid-YTW : 8.99 % |

| BAM.PR.M | Perpetual-Discount | 2.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 6.32 % |

| BAM.PF.F | FixedReset | 2.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.09 % |

| MFC.PR.J | FixedReset | 2.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.19 Bid-YTW : 8.70 % |

| BNS.PR.Q | FixedReset | 2.76 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.44 Bid-YTW : 4.19 % |

| NA.PR.Q | FixedReset | 2.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.85 Bid-YTW : 5.01 % |

| HSE.PR.A | FixedReset | 3.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 8.50 Evaluated at bid price : 8.50 Bid-YTW : 7.29 % |

| CIU.PR.A | Perpetual-Discount | 3.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 5.94 % |

| IFC.PR.A | FixedReset | 3.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 10.74 % |

| BAM.PR.B | Floater | 4.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 9.93 Evaluated at bid price : 9.93 Bid-YTW : 4.80 % |

| BAM.PR.C | Floater | 4.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 9.85 Evaluated at bid price : 9.85 Bid-YTW : 4.84 % |

| BNS.PR.R | FixedReset | 4.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.51 Bid-YTW : 4.40 % |

| BAM.PR.K | Floater | 4.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 9.95 Evaluated at bid price : 9.95 Bid-YTW : 4.79 % |

| PWF.PR.P | FixedReset | 6.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 11.60 Evaluated at bid price : 11.60 Bid-YTW : 5.02 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.E | FixedReset | 112,233 | Nesbitt crossed 75,000 at 25.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 23.28 Evaluated at bid price : 25.43 Bid-YTW : 5.16 % |

| TD.PF.G | FixedReset | 86,650 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-04-30 Maturity Price : 25.00 Evaluated at bid price : 25.45 Bid-YTW : 5.18 % |

| NA.PR.X | FixedReset | 81,645 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 23.09 Evaluated at bid price : 24.86 Bid-YTW : 5.59 % |

| RY.PR.M | FixedReset | 78,680 | Nesbitt crossed 74,500 at 18.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 18.03 Evaluated at bid price : 18.03 Bid-YTW : 4.72 % |

| BAM.PF.C | Perpetual-Discount | 73,400 | Scotia crossed 70,000 at 19.32. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 19.32 Evaluated at bid price : 19.32 Bid-YTW : 6.36 % |

| BMO.PR.S | FixedReset | 69,756 | Nesbitt crossed 56,700 at 17.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-01-28 Maturity Price : 17.23 Evaluated at bid price : 17.23 Bid-YTW : 4.66 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.E | FixedReset | Quote: 17.61 – 18.75 Spot Rate : 1.1400 Average : 0.7170 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 17.32 – 18.37 Spot Rate : 1.0500 Average : 0.6620 YTW SCENARIO |

| TRP.PR.C | FixedReset | Quote: 11.17 – 12.10 Spot Rate : 0.9300 Average : 0.5588 YTW SCENARIO |

| TRP.PR.B | FixedReset | Quote: 10.00 – 10.70 Spot Rate : 0.7000 Average : 0.4075 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 14.19 – 14.90 Spot Rate : 0.7100 Average : 0.4527 YTW SCENARIO |

| MFC.PR.N | FixedReset | Quote: 17.25 – 17.96 Spot Rate : 0.7100 Average : 0.4724 YTW SCENARIO |

Re: Tobin tax

How is that fundamentally different than the existing U.S. Securities and Exchange Commission (SEC) fee of USD$0.01 per USD$446.43 (or any fraction) of the proceeds of sale?

The SEC fee is paid by the seller and is, by my calculations, 44.6 times smaller than the proposal 0.1%, but the principle is the same. In other countries it is labelled a stamp tax.

How is that fundamentally different than the existing U.S. Securities and Exchange Commission (SEC) fee of USD$0.01 per USD$446.43 (or any fraction) of the proceeds of sale?

You are quite right that to draw the comparison between the SEC fee and the Tobin Tax on a qualitative basis; the differences are quantitative and philosophical.

The SEC fee is a cost-recovery mechanism.

The rate recently changed:

This can be compared with the proposed rate of Tobin Tax of 10bp, or $1,000.00 per million.

So that’s quite the difference, and the effects on market liquidity will probably accelerate as the frictional charge grows.

I don’t have a problem with cost recovery. Much as I like to mock the regulators, I will be the first to defend their existence. There are Bad People in the business, some regulation and enforcement is needed, and therefore there will be costs incurred to implement a structure.

On the other hand, when the Tobin Tax isn’t being lauded as a cash-grab – and a progressive one at that, as the quoted NYT piece gleefully states – it is hailed for precisely the reason that it will decrease trading and impair liquidity. I say that if we, as a democratic society, decide that it is meet and right to increase tax revenue, taking the proceeds “with 40 percent coming from the top 1 percent of income earners and 75 percent from the top 20 percent”, then we should explicitly create such a tax, rather than designing a tax that punishes those engaged in a particular business endeavor.

This tax grab discourages trading of equities, but it does not discourage trading of houses. It does not discourage holding equities and collecting the dividend. It does not discourage rent collection, professional athletics or mass entertainment. It does not even discourage the trading of bonds. If you’re going to justify a tax based on the income of the payers, wouldn’t it be better to tax the income of the payers in the first place?