Employers added more workers in February than projected but wages unexpectedly declined, dashing hopes that reduced slack in the labor market was starting to benefit all Americans.

The 242,000 gain followed a 172,000 rise in January that was larger than previously estimated, a Labor Department report showed Friday. The jobless rate held at 4.9 percent as people entered the labor force and found work. Average hourly earnings dropped, the first monthly decline in more than a year, and workers put in fewer hours.

…

Average hourly earnings dropped by 0.1 percent from the prior month, the first decline since December 2014, the Labor Department’s figures showed. Worker pay increased 2.2 percent over the 12 months ended in February, less than the 2.5 percent forecast in the Bloomberg survey. Wage growth has been hovering just above 2 percent year-over-year on average since the current expansion began in mid-2009.

…

Payrolls at retailers climbed about 55,000 in February after a 62,000 advance a month earlier, while health care employment increased 57,400.Payrolls at factories declined by 16,000 after a 23,000 gain and construction companies added 19,000 workers.

The participation rate, which shows the share of working-age people in the labor force, jumped to 62.9 percent, the highest since January 2015.

An otherwise interesting article quantifying projected investor losses from negative yields was spoilt by a misconception about the bond market:

As central bankers in Europe and Japan experiment with negative-rate policies to ignite their economies, investors are essentially being charged a fee to own about $7.7 trillion of sovereign debt.

How big of a tax is this on bond buyers? Well, here’s one way to get a sense of it: Investors would lose about 71 billion euros ($78 billion) if they were to buy all of Germany’s negative-yielding bonds coming due in more than two years and held them to maturity, according to calculations by Bloomberg Intelligence analyst David Powell.

…

Of course, this is an entirely hypothetical exercise. Many investors aren’t planning to hold this debt until maturity. Some are counting on yields to go even more negative, meaning that prices would increase, allowing them to get out without losses or even a profit if and when they want to.

It’s the last paragraph, of course, that is complete bullshit. This stuff is Fixed Income. It has a fixed coupon (mostly!) and a fixed maturity date and a fixed redemption price.

Therefore, the loss from today’s price to maturity is fixed. OK, so some investors are hoping prices will increase between now and maturity, if only a little bit and if only for a short while. So what? If current investors in German bonds should be so lucky as to unload their stakes with a 71-billion euro profit (from today’s prices) instead of an equally sized loss, all that means is that the buyers will, between transaction date and maturity, realize a 142-billion euro loss.

Because, you see, this stuff is fixed income.

Quibbling that the central banks / government treasuries could be the buyer is meaningless. In that case the central banks and government treasuries are taking the loss, even if they wish to cast it as a redemption.

There has been some philosophizing over productivity:

It’s a paradox that’s been puzzling economists for a while. How can U.S. productivity growth be slowing down at the same time that innovation in everything from smartphones to 3D printing seems to be speeding up?

A trio of economists from the Federal Reserve and the International Monetary Fund think they have the answer and it’s not particularly pretty. They argue in a new paper that the down-shift in productivity is for real. It’s not a mirage of mis-measurement by government statisticians unable to keep up with rapidly changing technology.

…

The authors — David Byrne from the Fed in Washington, John Fernald from the San Francisco Fed and Marshall Reinsdorf from the International Monetary Fund — also don’t deny that IT has made Americans’ lives easier and more enjoyable in many ways, from calling up directions on Google Maps to trading cat videos on Facebook.But that doesn’t translate into more economic output. The researchers compare such online services to an old economy innovation: television. It too enhanced Americans’ leisure time but didn’t make them more productive.

There are lots of available critiques of GDP; perhaps the productivity problem is just another one of them.

Matt Levine writes an entertaining piece on the valuation of private equities:

Today’s Wall Street Journal has a terrific story about how mutual funds that bought stakes in large closely held technology companies are now writing down some of those stakes:

BlackRock Inc., Fidelity Investments, T. Rowe Price Group Inc. and Wellington Management run or advise mutual funds that own shares in at least 40 closely held startups valued at $1 billion or more apiece, according to securities filings analyzed by The Wall Street Journal.

For 13 of the startups, at least one mutual-fund firm values its investment at less than what it paid, the Journal’s analysis shows. Those firms are valuing the 13 companies at an average of 28% below their original purchase price.

…

You know what I think! Private markets are the new public markets, and if you want to run a giant company with hundreds of employees, a multibillion-dollar valuation, and millions of dollars raised from public mutual funds, while still calling it a “startup,” you can do that now. (You can even call it a “unicorn,” if “startup” seems a little low-rent.) But what this means is that private companies are the new public companies, and sometimes public companies’ stocks go down. In a world where venture-funded startups exist in a sort of trial-and-error, proof-of-concept phase, and go public when it turns out the concept works, private valuations shouldn’t fluctuate unpredictably: You raise money, your thing works, you raise more money at a higher valuation, your thing scales a bit, and you go public at a yet higher valuation. (Or: You raise money, your thing fails, you send your venture capitalists a note with your condolences, and that is that.) The problems of running an operating business for the long term, with revenue fluctuations and competitive pressures and changing market conditions, get worked out in your stock price as a public company. Sometimes it goes down!In a world where venture-funded startups are also mutual-fund-funded multibillion-dollar companies with massive established businesses used by millions of people, that’s not the model any more.

…

They [privately held companies] can even avoid the discipline of fluctuating stock prices. Just don’t sell to mutual funds! It is an obvious answer, and private companies have noticed:Some venture capitalists anticipate further markdowns by mutual funds. That could make some startups more reluctant to seek mutual-fund money, since public disclosure of their valuations is watched so closely.

Assiduous Readers will remember that I expect that sooner or later we’re going to see a gigantic juicy private equity valuation scandal … and then we’ll learn which pension funds and which public investment companies (such as insurers) have been naughty.

It was another superb day for the Canadian preferred share market, with PerpetualDiscounts up 51bp, FixedResets winning 75bp and DeemedRetractibles up 36bp. The Performance Highlights table has only three losers. Volume was well below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

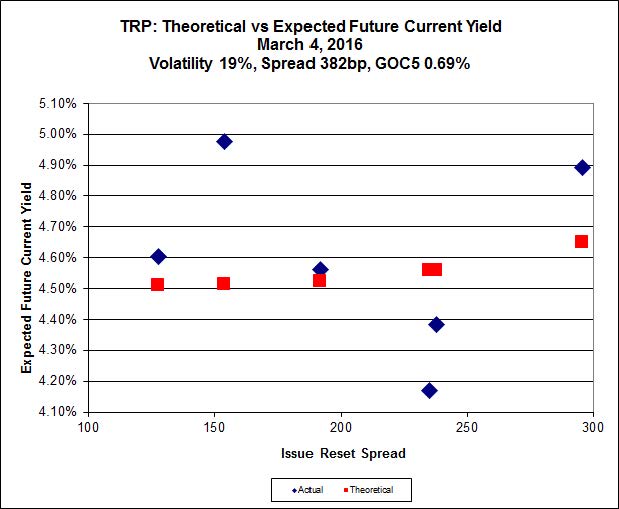

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.22 to be $1.54 rich, while TRP.PR.C, resetting 2021-1-30 at +296, is $1.16 cheap at its bid price of 11.20.

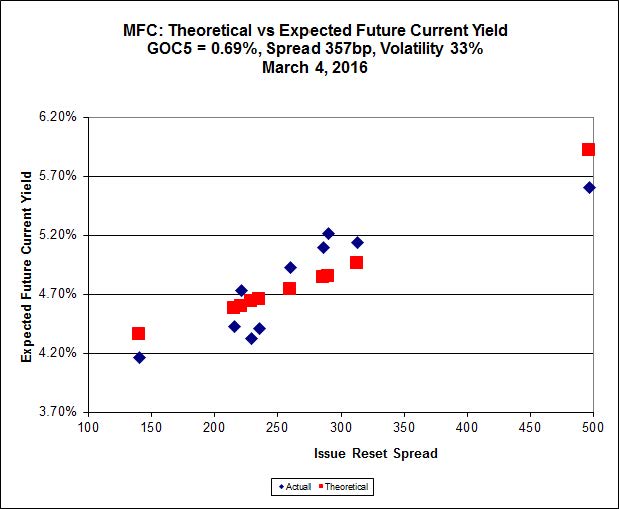

Click for Big

Most expensive is MFC.PR.O, resetting at +497bp on 2021-6-19, bid at 25.25 to be 1.32 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.21 to be 1.30 cheap.

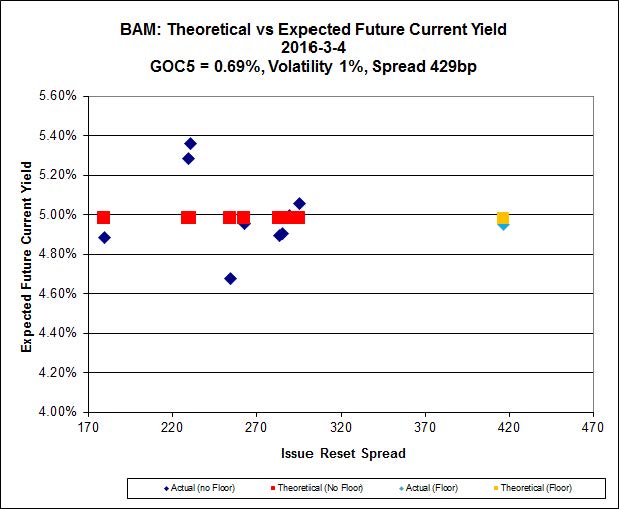

Click for Big

The cheapest issue relative to its peers is BAM.PR.T, resetting at +231bp on 2017-3-31, bid at 14.00 to be $1.06 cheap. BAM.PF.E, resetting at +255 on 2020-3-31 is bid at 17.33 and appears to be $1.06 rich.

Click for Big

FTS.PR.K, with a spread of +205bp, and bid at 15.02 looks $0.44 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 11.12 and is $0.31 cheap.

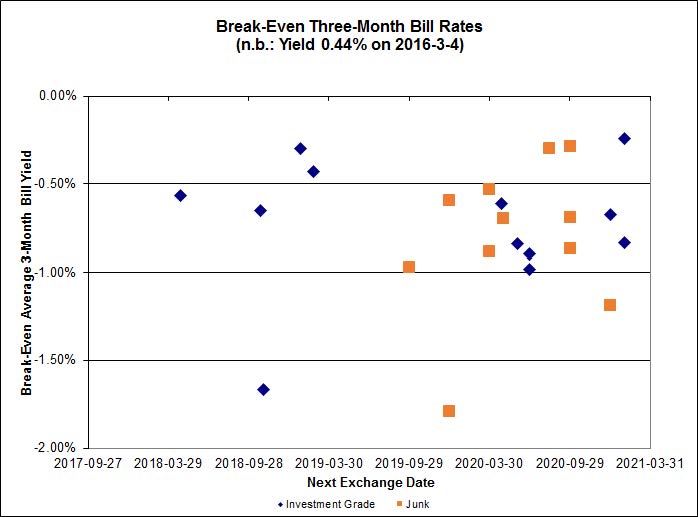

Click for Big

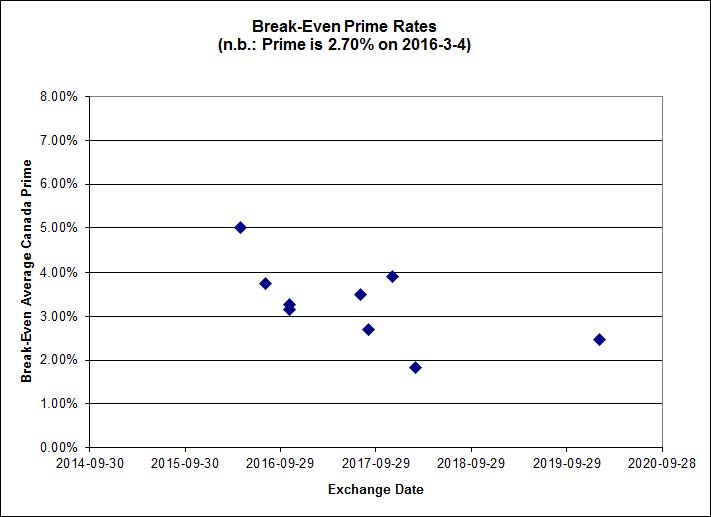

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.96%, with three outliers below -2.00% and one above 0.00%. There are no junk outliers.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.34 % | 6.49 % | 12,958 | 16.09 | 1 | -0.3150 % | 1,466.1 |

| FixedFloater | 7.45 % | 6.53 % | 23,749 | 15.70 | 1 | -0.0783 % | 2,670.3 |

| Floater | 4.58 % | 4.74 % | 77,562 | 15.88 | 4 | 0.5600 % | 1,675.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0338 % | 2,745.4 |

| SplitShare | 4.84 % | 5.87 % | 77,232 | 2.65 | 7 | -0.0338 % | 3,212.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0338 % | 2,506.6 |

| Perpetual-Premium | 5.81 % | 0.98 % | 76,539 | 0.08 | 6 | 0.0662 % | 2,540.9 |

| Perpetual-Discount | 5.72 % | 5.77 % | 101,095 | 14.15 | 33 | 0.5145 % | 2,529.0 |

| FixedReset | 5.59 % | 5.13 % | 196,630 | 14.49 | 85 | 0.7490 % | 1,818.3 |

| Deemed-Retractible | 5.29 % | 5.71 % | 113,059 | 5.14 | 34 | 0.3586 % | 2,572.6 |

| FloatingReset | 3.10 % | 5.26 % | 41,029 | 5.46 | 16 | 0.5543 % | 1,964.5 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.T | FixedReset | -3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 5.60 % |

| HSE.PR.G | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 16.60 Evaluated at bid price : 16.60 Bid-YTW : 6.61 % |

| BMO.PR.Q | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.39 Bid-YTW : 7.64 % |

| RY.PR.I | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.15 Bid-YTW : 4.55 % |

| FTS.PR.I | FloatingReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 9.50 Evaluated at bid price : 9.50 Bid-YTW : 4.98 % |

| IFC.PR.C | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.94 Bid-YTW : 9.70 % |

| BMO.PR.W | FixedReset | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 16.77 Evaluated at bid price : 16.77 Bid-YTW : 4.60 % |

| ELF.PR.G | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 20.08 Evaluated at bid price : 20.08 Bid-YTW : 6.01 % |

| RY.PR.H | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 17.10 Evaluated at bid price : 17.10 Bid-YTW : 4.57 % |

| VNR.PR.A | FixedReset | 1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 5.37 % |

| SLF.PR.J | FloatingReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 11.69 Bid-YTW : 11.56 % |

| CU.PR.C | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 15.85 Evaluated at bid price : 15.85 Bid-YTW : 4.95 % |

| MFC.PR.G | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.21 Bid-YTW : 8.76 % |

| TD.PR.Z | FloatingReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 5.26 % |

| CU.PR.H | Perpetual-Discount | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 22.94 Evaluated at bid price : 23.35 Bid-YTW : 5.64 % |

| BAM.PF.C | Perpetual-Discount | 1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 19.99 Evaluated at bid price : 19.99 Bid-YTW : 6.19 % |

| TD.PR.S | FixedReset | 1.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.53 Bid-YTW : 3.93 % |

| MFC.PR.J | FixedReset | 1.45 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.75 Bid-YTW : 8.93 % |

| IAG.PR.G | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.40 Bid-YTW : 8.58 % |

| BIP.PR.A | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.01 Evaluated at bid price : 18.01 Bid-YTW : 5.97 % |

| MFC.PR.M | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.29 Bid-YTW : 8.46 % |

| RY.PR.Z | FixedReset | 1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 17.25 Evaluated at bid price : 17.25 Bid-YTW : 4.47 % |

| TRP.PR.E | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.22 Evaluated at bid price : 18.22 Bid-YTW : 4.52 % |

| BAM.PR.M | Perpetual-Discount | 1.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 19.78 Evaluated at bid price : 19.78 Bid-YTW : 6.13 % |

| BMO.PR.Y | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 4.78 % |

| BAM.PF.A | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 17.96 Evaluated at bid price : 17.96 Bid-YTW : 5.25 % |

| CM.PR.Q | FixedReset | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.15 Evaluated at bid price : 18.15 Bid-YTW : 4.86 % |

| FTS.PR.F | Perpetual-Discount | 1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 21.94 Evaluated at bid price : 22.18 Bid-YTW : 5.55 % |

| FTS.PR.J | Perpetual-Discount | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 21.42 Evaluated at bid price : 21.42 Bid-YTW : 5.58 % |

| BAM.PF.D | Perpetual-Discount | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 6.20 % |

| BAM.PR.N | Perpetual-Discount | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 19.83 Evaluated at bid price : 19.83 Bid-YTW : 6.11 % |

| MFC.PR.I | FixedReset | 1.81 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.41 Bid-YTW : 8.67 % |

| HSE.PR.A | FixedReset | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 8.76 Evaluated at bid price : 8.76 Bid-YTW : 6.99 % |

| BMO.PR.M | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.20 Bid-YTW : 4.20 % |

| IFC.PR.A | FixedReset | 2.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.62 Bid-YTW : 11.24 % |

| MFC.PR.L | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.10 Bid-YTW : 9.26 % |

| TD.PF.D | FixedReset | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.37 Evaluated at bid price : 18.37 Bid-YTW : 4.80 % |

| PWF.PR.T | FixedReset | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 19.70 Evaluated at bid price : 19.70 Bid-YTW : 4.11 % |

| BNS.PR.C | FloatingReset | 2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.22 Bid-YTW : 5.29 % |

| BAM.PR.Z | FixedReset | 2.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.05 Evaluated at bid price : 18.05 Bid-YTW : 5.29 % |

| MFC.PR.N | FixedReset | 2.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.30 Bid-YTW : 8.39 % |

| BAM.PF.F | FixedReset | 2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 5.24 % |

| TD.PF.E | FixedReset | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 4.76 % |

| NA.PR.S | FixedReset | 2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 16.76 Evaluated at bid price : 16.76 Bid-YTW : 4.88 % |

| NA.PR.W | FixedReset | 2.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 5.00 % |

| PWF.PR.A | Floater | 2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 11.30 Evaluated at bid price : 11.30 Bid-YTW : 4.21 % |

| TRP.PR.D | FixedReset | 3.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 17.51 Evaluated at bid price : 17.51 Bid-YTW : 4.63 % |

| SLF.PR.H | FixedReset | 3.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.89 Bid-YTW : 9.78 % |

| FTS.PR.G | FixedReset | 3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 4.93 % |

| TRP.PR.F | FloatingReset | 3.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 11.60 Evaluated at bid price : 11.60 Bid-YTW : 5.06 % |

| CIU.PR.C | FixedReset | 3.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 10.60 Evaluated at bid price : 10.60 Bid-YTW : 4.80 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.H | FixedReset | 161,200 | Scotia crossed 160,000 at 14.52. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.89 Bid-YTW : 9.78 % |

| RY.PR.Q | FixedReset | 38,817 | RBC crossed 15,000 at 25.52. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 23.29 Evaluated at bid price : 25.45 Bid-YTW : 5.17 % |

| TD.PF.G | FixedReset | 35,839 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 23.31 Evaluated at bid price : 25.50 Bid-YTW : 5.23 % |

| MFC.PR.O | FixedReset | 35,385 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2021-06-19 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 5.45 % |

| HSE.PR.A | FixedReset | 34,260 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-03-04 Maturity Price : 8.76 Evaluated at bid price : 8.76 Bid-YTW : 6.99 % |

| SLF.PR.G | FixedReset | 32,056 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.30 Bid-YTW : 10.35 % |

| There were 21 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| HSE.PR.C | FixedReset | Quote: 15.17 – 18.00 Spot Rate : 2.8300 Average : 1.5785 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 21.01 – 22.75 Spot Rate : 1.7400 Average : 1.3684 YTW SCENARIO |

| TRP.PR.I | FloatingReset | Quote: 10.25 – 11.99 Spot Rate : 1.7400 Average : 1.4284 YTW SCENARIO |

| BMO.PR.M | FixedReset | Quote: 23.20 – 23.90 Spot Rate : 0.7000 Average : 0.4183 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 15.00 – 15.78 Spot Rate : 0.7800 Average : 0.5113 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 11.12 – 11.78 Spot Rate : 0.6600 Average : 0.4031 YTW SCENARIO |