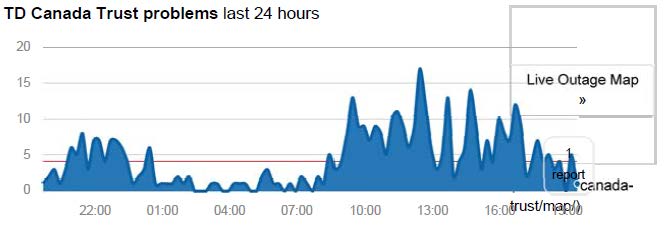

TD continues to provide cruddy service:

Been trying 5 days straight to get through to an advisor without any success. Totally, gun shy to make any risky trades after last week system issues. Why does anyone still trade with TD?.

Will TD update its customers on the outages last week? About future up trades to prevent any further issues? Compensation to investors for loses? When customers will have phone access to advisors again?

Probably no to all my questions. They don’t seem to care. I did notice their stock is the only Canadian bank stock that is trading down today.

Click for Big

The pathetic excuses for poor performance provided by Canada’s pathetic excuses for brokerage houses has really started to bother me, so I looked up the Toronto Stock Exchange Daily Trading Reports. The 2018-01-02 Report states that the TSX experienced 829,930 trades on the day (number of trades will be a better indication of retail volume than trading value), while the 2017-11-15 Report (date chosen to be reasonable recent and reasonably typical) reports 889,332 trades.

Obviously this is the smallest of all possible samples using an imperfect proxy, but this doesn’t look like an unprecedented explosion of retail activity to me! I might put a chart together at some point, or perhaps some Industrious and Assiduous Reader could do it for me. But it does seem that perhaps a few more details are required before we can understand the horrible service Canadian retail investors are getting from their beloved banks. Until we get both a convincing explanation of the problem and a reasonably well-detailed exposition of what is being done to address the problem, I suggest that retail investors not count on being able to trade during an actual market break.

However, the market was up again today, presumably due to the five-year Canada yield continuing to rise … now at 2.00%! So I’m all right, Jack.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.0924 % | 2,811.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.0924 % | 5,159.1 |

| Floater | 3.27 % | 3.41 % | 33,987 | 18.76 | 4 | 1.0924 % | 2,973.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5069 % | 3,159.7 |

| SplitShare | 4.65 % | 4.11 % | 61,066 | 3.42 | 5 | 0.5069 % | 3,773.4 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5069 % | 2,944.1 |

| Perpetual-Premium | 5.36 % | -0.25 % | 51,446 | 0.09 | 18 | 0.0433 % | 2,862.1 |

| Perpetual-Discount | 5.28 % | 5.24 % | 71,755 | 15.10 | 16 | -0.2390 % | 3,011.9 |

| FixedReset | 4.16 % | 4.07 % | 140,785 | 3.82 | 98 | 0.4426 % | 2,550.6 |

| Deemed-Retractible | 5.04 % | 5.39 % | 82,593 | 5.87 | 28 | -0.0412 % | 2,957.9 |

| FloatingReset | 2.97 % | 2.50 % | 39,397 | 0.80 | 10 | 0.4624 % | 2,757.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.J | FixedReset | -2.64 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.42 Bid-YTW : 4.42 % |

| IFC.PR.A | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.50 Bid-YTW : 6.77 % |

| BAM.PF.C | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 21.72 Evaluated at bid price : 22.06 Bid-YTW : 5.52 % |

| CCS.PR.C | Deemed-Retractible | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 5.68 % |

| BAM.PF.D | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 22.22 Evaluated at bid price : 22.51 Bid-YTW : 5.47 % |

| MFC.PR.M | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.08 Bid-YTW : 4.90 % |

| BAM.PF.G | FixedReset | 1.01 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-06-30 Maturity Price : 25.00 Evaluated at bid price : 24.91 Bid-YTW : 4.73 % |

| IFC.PR.C | FixedReset | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.81 Bid-YTW : 4.77 % |

| MFC.PR.L | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.65 Bid-YTW : 5.07 % |

| BNS.PR.Y | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.79 Bid-YTW : 3.58 % |

| CM.PR.O | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.87 Evaluated at bid price : 24.24 Bid-YTW : 4.38 % |

| TRP.PR.F | FloatingReset | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 20.17 Evaluated at bid price : 20.17 Bid-YTW : 3.78 % |

| TRP.PR.A | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 20.84 Evaluated at bid price : 20.84 Bid-YTW : 4.63 % |

| PWF.PR.T | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 24.42 Evaluated at bid price : 24.80 Bid-YTW : 4.36 % |

| IAG.PR.G | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-06-30 Maturity Price : 25.00 Evaluated at bid price : 24.49 Bid-YTW : 4.33 % |

| BAM.PR.X | FixedReset | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 18.11 Evaluated at bid price : 18.11 Bid-YTW : 4.90 % |

| CU.PR.C | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 22.18 Evaluated at bid price : 22.78 Bid-YTW : 4.57 % |

| MFC.PR.K | FixedReset | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.59 Bid-YTW : 5.19 % |

| BAM.PR.C | Floater | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 16.50 Evaluated at bid price : 16.50 Bid-YTW : 3.41 % |

| EIT.PR.A | SplitShare | 1.47 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 25.49 Bid-YTW : 4.52 % |

| IAG.PR.A | Deemed-Retractible | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.99 Bid-YTW : 6.07 % |

| BMO.PR.Q | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.21 Bid-YTW : 3.95 % |

| BMO.PR.T | FixedReset | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.71 Evaluated at bid price : 24.09 Bid-YTW : 4.38 % |

| BAM.PR.B | Floater | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 16.53 Evaluated at bid price : 16.53 Bid-YTW : 3.41 % |

| BAM.PF.F | FixedReset | 1.67 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-09-30 Maturity Price : 25.00 Evaluated at bid price : 24.97 Bid-YTW : 4.67 % |

| TRP.PR.G | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-11-30 Maturity Price : 25.00 Evaluated at bid price : 24.76 Bid-YTW : 4.32 % |

| TRP.PR.E | FixedReset | 1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.40 Evaluated at bid price : 24.42 Bid-YTW : 4.37 % |

| TRP.PR.D | FixedReset | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.50 Evaluated at bid price : 23.96 Bid-YTW : 4.50 % |

| HSE.PR.G | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-06-30 Maturity Price : 25.00 Evaluated at bid price : 25.63 Bid-YTW : 3.59 % |

| TRP.PR.B | FixedReset | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 17.17 Evaluated at bid price : 17.17 Bid-YTW : 4.57 % |

| TRP.PR.H | FloatingReset | 3.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 16.92 Evaluated at bid price : 16.92 Bid-YTW : 3.55 % |

| MFC.PR.F | FixedReset | 3.75 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.10 Bid-YTW : 7.11 % |

| TRP.PR.C | FixedReset | 4.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.50 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.K | FixedReset | 314,386 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-05-31 Maturity Price : 25.00 Evaluated at bid price : 26.17 Bid-YTW : 3.88 % |

| RY.PR.Q | FixedReset | 203,403 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 26.92 Bid-YTW : 3.31 % |

| BNS.PR.Q | FixedReset | 171,194 | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-10-25 Maturity Price : 25.00 Evaluated at bid price : 25.03 Bid-YTW : 3.26 % |

| BNS.PR.R | FixedReset | 87,383 | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-01-26 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 3.28 % |

| NA.PR.W | FixedReset | 86,980 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.59 Evaluated at bid price : 23.90 Bid-YTW : 4.37 % |

| CM.PR.P | FixedReset | 84,640 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-01-09 Maturity Price : 23.41 Evaluated at bid price : 23.73 Bid-YTW : 4.38 % |

| There were 46 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.H | FloatingReset | Clearly a bogus quote (a spread of over $9 !), since the low for the day was 16.94 and the high 17.10 on what the bank-owned brokerages would possibly describe as overwhelming volume of 4,250 shares. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

Quote: 16.92 – 26.01 YTW SCENARIO |

| TD.PR.T | FloatingReset | Quote: 24.95 – 25.59 Spot Rate : 0.6400 Average : 0.3845 YTW SCENARIO |

| SLF.PR.G | FixedReset | Quote: 19.08 – 19.75 Spot Rate : 0.6700 Average : 0.4411 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 23.81 – 24.69 Spot Rate : 0.8800 Average : 0.6887 YTW SCENARIO |

| PWF.PR.F | Perpetual-Discount | Quote: 24.40 – 24.86 Spot Rate : 0.4600 Average : 0.2725 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 25.01 – 25.43 Spot Rate : 0.4200 Average : 0.2689 YTW SCENARIO |