Royal Bank of Canada has announced:

a domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BD.

Royal Bank of Canada will issue 12 million Preferred Shares Series BD priced at $25 per share to raise gross proceeds of $300 million. The bank has granted the Underwriters an option, exercisable in whole or in part, to purchase up to an additional 2 million Preferred Shares Series BD at the same offering price.

The Preferred Shares Series BD will yield 3.60 per cent annually, payable quarterly, as and when declared by the Board of Directors of Royal Bank of Canada, for the initial period ending May 24, 2020. Thereafter, the dividend rate will reset every five years at a rate equal to 2.74 per cent over the 5-year Government of Canada bond yield.

Subject to regulatory approval, on or after May 24, 2020, the bank may redeem the Preferred Shares Series BD in whole or in part at par. Holders of Preferred Shares Series BD will, subject to certain conditions, have the right to convert all or any part of their shares to Non-Cumulative Floating Rate Preferred Shares Series BE on May 24, 2020 and on May 24 every five years thereafter.

Holders of the Preferred Shares Series BE will be entitled to receive a non-cumulative quarterly floating dividend, as and when declared by the Board of Directors of Royal Bank of Canada, at a rate equal to the 3-month Government of Canada Treasury Bill yield plus 2.74 per cent. Holders of Preferred Shares Series BE will, subject to certain conditions, have the right to convert all or any part of their shares to Preferred Shares Series BD on May 24, 2025 and on May 24 every five years thereafter.

The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is January 30, 2015.

We routinely undertake funding transactions to maintain strong capital ratios and a cost effective capital structure. Net proceeds from this transaction will be used for general business purposes.

They later announced:

that as a result of strong investor demand for its previously announced domestic public offering of Non-Cumulative, 5-Year Rate Reset Preferred Shares Series BD, the size of the offering has been increased to 24 million shares. The gross proceeds of the offering will now be $600 million. The offering will be underwritten by a syndicate led by RBC Capital Markets. The expected closing date is January 30, 2015.

Monster issue!

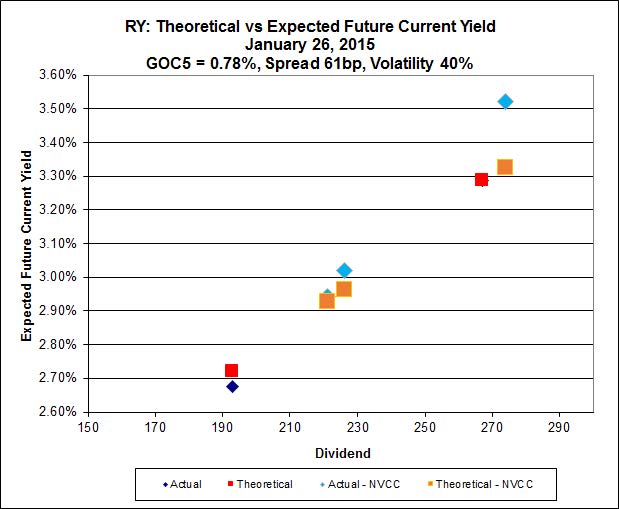

It doesn’t happen very often, but this issue actually looks cheap to its peers! The new issue looks a whopping $1.47 cheap, while the most expensive issue is RY.PR.I, bid at 25.31 and – according to Implied Volatility theory – is $0.40 rich. RY.PR.I resets at +193 on 2019-02-24 … and has a good chance of being called then because it’s not NVCC-compliant.

Click for Big

When the 5 year GOC inevitably goes negative will these be reset at less than 274 or is 274 a floor?

I looked at some definitions in the prospectus for RY.PR.H, which was announced 2014-5-23. I assume that the prospectus for the forthcoming issue will be copy-pasted, but it’s always worthwhile to check!

***********************

“Annual Fixed Dividend Rate” means, for any Subsequent Fixed Rate Period, the rate (expressed as a percentage rounded to the nearest one hundred–thousandth of one percent (with 0.000005% being rounded up)) equal to the Government of Canada Yield on the applicable Fixed Rate Calculation Date plus 2.26%.

“Government of Canada Yield” on any date means the yield to maturity on such date (assuming semi-annual compounding) of a Canadian dollar denominated non-callable Government of Canada bond with a term to maturity of five years as quoted as of 10:00 a.m. (Toronto time) on such date and which appears on the Bloomberg Screen GCAN5YR Page on such date; provided that, if such rate does not appear on the Bloomberg Screen GCAN5YR Page on such date, the Government of Canada Yield will mean the arithmetic average of the yields quoted to the Bank by two registered Canadian investment dealers selected by the Bank as being the annual yield to maturity on such date, compounded semi-annually, which a noncallable Government of Canada bond would carry if issued, in Canadian dollars in Canada, at 100% of its principal amount on such date with a term to maturity of five years.

**********************

I don’t see any reference to a floor or cap!

If you feel that a negative 5-year GOC rate is inevitable, you have no reason to be fooling around with FixedResets – or preferred shares of any kind, for that matter. You can make good money in derivatives … provided, of course, that the inevitable does in fact happen.

Not too many months ago, a rise in market yields was not just inevitable, but imminent…

As it happens, I received a similar inquiry from Assiduous Reader DL via email:

As noted above, I don’t see any reference in the prospectus to a floor or cap, so in theory the rate could go negative.

But that reminds me of a question I asked a bond dealer many moons ago. As you may know, there is a securities lending market for bonds. You can borrow bonds and lend cash, or vice versa, and the amount of cash lent or borrowed is basically fixed at a small percentage over the market value of the bonds.

The borrower of the bonds has to pay the owner the coupon on the bond, if, as and when received, and the borrower of the cash pays the cash lender a rate agreed to at the beginning of the borrow. This will most often happen at the “General Collateral” rate, which will normally be just a bit above the Fed Funds rate in the States, or the Overnight Rate in Canada, although this will not necessarily always be the case.

Sometimes, though, securities go “Special”. They’re hard to borrow, so anybody willing to lend them has a host of eager borrowers clamouring for his attention. There is room for a fair bit of chicanery here, but the basis is legitimate. “I won’t lend you this wonderful security if I have to pay 0.80% on your loan of cash to me! I will only pay 0.50%”.

Sometimes things can get basically impossible to borrow, so it becomes a fail to deliver situation. If you fail to deliver, you don’t get paid and (if it’s your fault) you don’t get any interest on the agreed amount. If I sell you $1-million Canadas at par and then fail to deliver for a day, you don’t have to pay me any interest on the $1-million cash you had all ready for me. You just give me the agreed upon cash when I give you the agreed upon securities, and in the interim any money you make investing that cash overnight is yours.

Now here’s where it gets hairy. Say I don’t deliver and you get nervous. You can buy me in. If I fail to deliver, you can tell me you need those securities and you need them now (to meet your other commitments) and if I don’t deliver tout suite, you’re going to buy them at whatever price you need to pay, and you’re going to charge me for the loss.

Again, this is all entirely normal, although regulators have kept themselves busy trying to eliminate fails in recent years.

But, back when I was a Canada bond guy, there was once an incredible squeeze on a low-coupon short-term issue (I forget the details. Sue me.). There was one dealer who owned an enormous chunk of this Canada issue and was squeezing the market to hell ‘n’ gone. The issue was ridiculously high priced, but you wouldn’t want to short it because you’d be taking a big hit on the borrowing and the price might go up anyway. It was a nasty, nasty situation for those dealers who had innocently shorted the issue as part of their normal market making activities.

So the repo rate on these things was a big fat zero. And I asked one of the dealers … ‘OK. Why just zero? Why can’t it go negative? Why can’t the cornering dealer say “You lend me cash AND pay me interest on it, or I’ll buy you in at … um …. whatever price it takes on the market.”

My guy didn’t have an answer for me. All he could say was … ‘I think the Bank of Canada might step in at that point.’

And that is the best I can do for you when asked what will happen if something is supposed to reset at what is supposed to be a negative rate. I don’t know. The big boys will have to argue over it when the time comes. You may remember that installment receipts for Husky Energy had a negative value at one point ($10 due on a stock trading at $8, if I remember correctly) and the brokerages got burned big-time, with guys buying 1,000 shares at -2.00, pocketing their $2,000 and disappearing.

I disagree. There are still opportunities in the preferred share market for people who think interest rates will go negative. Perpetuals should perform quite well when rates go negative, at least until they are called away at par. That’s why I wonder if issues like GWO.PR.S, which can’t be called for quite some time, deserve more of a premium.

Note the exceptional run ups in perpetual discounts in particular EMA.PR.E, CU.PR.G, F last week as the market revalues these issues for a new rate environment.

I will certainly agree that one can make good money in the preferred share market by applying a probability distribution of future market conditions to current prices and capitalizing on the differences. To the extent that your projected probability distribution is better over time than what the market is accounting for, you’ll do quite well.

But when this is applied on a macro scale, it is market timing. I don’t think anybody can do it well over time.

And if you take the view that negative interest rates are a foregone conclusion, then you can get better leverage on that certainty with derivatives than boring old preferred shares, which have to be margined at 35%.

But I certainly wouldn’t advise an investment strategy based on foregone conclusions, because they tend to be gone before you know it.