Barry Critchley was kind enough to quote me in his article TransAlta plays the Grinch with its preferred share holders:

James Hymas, who runs Hymas Investment Management and who also publishes the PrefBlog, wrote “all of this analysis leads to the conclusion that this is a rotten deal for the preferred shareholders, so rotten that we may call it a sleazy attempt by the company to pull the wool over the eyes of unsophisticated retail investors. As the company admits, they look forward to reducing the corporation’s notional capital balance of preferred shares by approximately $300 million.”

After noting that an analysis based on implied volatility would require an even higher dividend than the 6.50 per cent TransAlta is offering, Hymas said the $300-million “is money that currently can potentially be earned by the current shareholders.”

That $300 million could occur with price increases on the extant issues; from an increase in the five-year government of Canada yield, or “from straightforward spread narrowing. The company is giving up nothing – NOTHING! – in order to capture this entire amount for themselves,” he wrote.

Assiduous Readers will remember that my views on the proposed Exchange (which will be voted on as a Plan of Arrangement) were published in the post TA Proposes Sleazy Exchange Offer.

Update, 2016-12-24 I was perplexed by a comment on Financial Wisdom Forum:

More on the TransAlta exchange.

http://business.financialpost.com/news/ … picks=true

FWIW, I am quite satisfied with the offer because I’m a trader and am more than happy to bail on these PF-3 issues because I really believe that one would have to be wearing super sized rose coloured glasses to think that they would someday trade or be redeemed at par, especially with a company like TA that has slashed the dividend on the common to 4 cents/quarter.

The case for the “No” vote does not depend on the hope that the shares will “someday trade or be redeemed at par”, and demonstrating this should actually make the argument more clear for those who have difficulty with the concept of Implied Volatility.

Let us examine the specific case of TA.PR.D; the following analysis framework may be applied to the other series with changes in numbers.

TA.PR.D:

- pays $0.67725 p.a. until the next Exchange Date

- will reset to GOC-5 + 203bp (paid on par value of $25) on each Exchange Date

- This is equal to (25 * GOC-5) + (25 * 203bp)

- which is equal to (25 * GOC-5) + $0.5075

- may be redeemed at $25 on each Exchange Date

- Exchange Dates are 2021-3-31 and every five years thereafter

The company proposes to exchange each share of this for 0.503 of a New Preferred Share; each New Preferred Share will

- Pay 6.50% of $25.00 = 1.625 until the next Exchange Date

- will reset to GOC-5 + 529bp (paid on par value of $25) on each Exchange Date

- may be redeemed at $25 on each Exchange Date

- Exchange Dates are 2021-12-31 and every five years thereafter

The fact that holders will be getting only 0.503 New Preferred Shares for each share of TA.PR.D makes the changes a little more complex for many investors, so as a thought experiment, let’s design a Notional Share which we will assume will be offered 1 for 1 for TA.PR.D, with the new holdings, in total, having exactly the same characteristics as the proposed new holdings of the New Preferred Shares.

A Notional Preferred Share:

- pays $0.817375 until the next Exchange Date

- will reset to 0.503 (GOC-5 + 529bp) * 25 on each Exchange Date

- This is equal to (0.503 * 25 * GOC-5) + (0.503 * 25 * 529bp)

- which is equal to 12.575 * GOC-5 + $0.6652175

- subject to a minimum rate of $0.817375

- may be redeemed at $12.575 on each Exchange Date

- Exchange Dates are 2021-12-31 and every five years thereafter

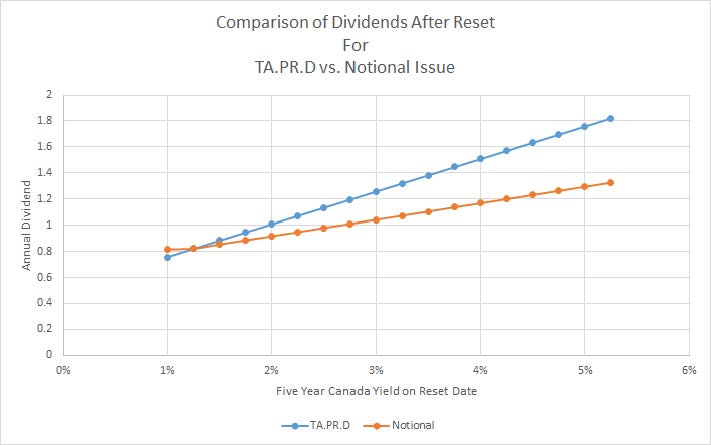

So when we compare the currently held TA.PR.D to the Notional Share we see that:

- The Notional Share will pay an extra $0.14 annually for each of the next five years (approximately), for a total of $0.70.

- The redemption price will drop from $25 to $12.575

- The dividends after the next Exchange Date (if it is left outstanding) will depend on the GOC-5 yield, as indicated on the following chart

Click for Big

The big problem, of course, is the change in redemption price – holders lose out on a lot of potential capital gains if the market improves, either through increases in the GOC-5 yield (which should increase the trading price of the preferreds) or through a narrowing of spreads (which may occur because the market improves, or TA’s credit improves, or both). In addition, we see that increases in the GOC-5 rate greatly improve the dividend payout from TA.PR.D and the much higher redemption price means these potential increases will not be called away unless for a gigantic premium over the current price.

Why does your chart stop at 1% on the left? Why do the lines not continue on? If they did, the Orange line would be well above the Blue line as we get down to 5-yr rates around 0.5%, no?. Are you suggesting that 5yr rates can never be below 1%?…..or are you purposely trying to make the deal look worse than it is in an effort to support your argument? If it is the former, I think clearly you are wrong. If it is the latter, well that would be a pretty sleazy thing to do wouldn’t it? If you want to be the guru of Canadian pref shares, I think you have a responsibility to be even-handed in your analysis and not try and trick people into supporting your view. Anyway, just my two cents on how to run your free blog….it is your blog so I guess you can draw the lines however you want.

Sounds like madequota!

Anyway, I believe the likelihood of five-year Canadas going below 1% again in five years time are very low, given the apparent recovery of the US economy and signs of life in Europe. This point was made and addressed in the comments to the original post.

If you disagree with my conclusions, go ahead. But it would aid your credibility if you put some numbers on your assumptions.

I do not have the time or the expertise to say whether this is a good deal for pref holders to accept. I see all five prefs rallied upon announcement and continue to trade above where they would had no proposal been announced, for me that is good enough as I am more of a trader than a long-term holder. You are the one doing the analysis, analysis that you are providing for free, and that I appreciate. However, it seems to me you built your chart in a deceptive way. The 5yr strip starting 5yrs out is barely above 2%, 5yr rates have been below 1% for virtually all of 2016. Rates could very easily be below 1% in five years time. You are often called the guru of Canadian pref shares, and rightly so, but I do think that also bestows a responsibility on you to be even-handed in your analysis. I think you should run the chart further to the left to show that in low interest rate environments, the New Pref actually is quite a bit better. I want the deal to go through because my prefs rallied upon announcement, they will fall (in the short-term) if the deal is blocked and likely rally further if it approved. Even if you think rates are going higher, can’t we just vote the deal through and take the extra money we make to buy even more lower-priced prefs from a different issuer that still have the upside you are looking for. I am not as smart as you to know if this is a good deal long-term, but I can very clearly see that I will lose money on my TA prefs I own if you and your army of followers block this deal. You block the deal, the prefs puke. It is as simple as that. What is so special about TA prefs? Just take the bonus 15-20% capital gain and roll into the prefs of another issuer. Smarter than tanking the free 20% gain we get from having the deal go through no?

Two different gmail addresses in the space of two posts?

You’re banned again, buddy. If you have problems with this, eMail me from an identifiable address using your real name and information that will allow confirmation of your identity.

It’s regrettable that preftrader2016 was accusatory (and anonymous?) in his post, but I actually agree with the basic content of what he said.

I have a large holding of TA.PR.H since, as you know, it was the best relative value among the TA rate reset preferreds. It is up 11% since the deal was announced. If someone offered me an 11% premium for ALL of my liquid investments tomorrow, I’d take it in a heartbeat and call it a year.

I have a large holding of TA.PR.H since, as you know, it was the best relative value among the TA rate reset preferreds.

There is certainly some temptation to celebrate the 11% price increase since the deal was announced, but nothing’s ever simple. I mentioned the tension between mourners and celebrants in a reply to comments on my main post on this topic.

So my first reaction is that since you say you “have a large holding” is: why do you still have it? Presumably you still hold it because you expect that this holding will give you some amount of excess return over time relative to other potential investments, so my question to you is: where is this extra return going to come from? Any capital appreciation due to spread narrowing and GOC-5 increases will be capped by the new issue’s call price; these two factors will have a greater effect on the extant issues (although of course the extant issues will have to overcome the 11% hurdle before we can firmly shift the marker into “Vote No” territory).

Extra income? There’s some amount of extra income being offered, but the Implied Volatility analysis shows quite clearly that this extra income does not compensate for sharp increase in call risk that will be borne by holders if the deal goes through.

And finally – 11% isn’t so great. You may be familiar with the valuation element I call “Disparity”, which is discussed as part of the explanation of my software; calculation of Disparity requires the calculation of a fair price for the security, when all of its projected cash flows are valued in the same way as the cash flows of comparable instruments – all adjusted for the characteristics of the issue, e.g., its credit quality, whether or not it’s a Floating Rate instrument, all that stuff.

TA.PR.H was 16.97 on December 16, the day before the announcement. On December 19, announcement date, it closed with a bid of 19.07. On December 30, after a 1.73% run-up in the broad TXPR index, it closed with a bid of 18.75 (which I call a 10.5% increase, but never mind).

On December 30, I calculate a fair value of TA.PR.H of 22.12. And, I will emphasize, this fair value contains no assumptions about the future course of spreads or the GOC-5. This compares the instrument on December 30 to all other liquid instruments trading on December 30. So I say the current bid of 18.75 is pretty damn low (when evaluated according to the attributes of the extant issue) and the only thing that can be said in favour of it is that it’s a little better than before.

So why would anybody vote in favour of this appalling plan? According to me, (and assuming the new issue trades at a price reflecting the 18.75 on TA.PR.H), the only thing you’re accomplishing is selling your shares at more than three bucks less than fair value. This is not good business.

Now, before anybody goes mortgaging their house so they can buy more TA preferreds based on fair value, I should emphasize that it’s only one of the elements that comprise my valuation of preferred shares; it’s not always right; and, like any other quantitative measure, it can be made to look pretty foolish if the environment changes (e.g., bankruptcy, or even just a credit downgrade). But I think it’s pretty good!

I agree with your calculations! In fact I sold 1/3 of my TA.PR.H post-announcement. I continue to hold TA.PR.H because I find 6.50%+529M650 attractive given the credit risk. The market also seems to have a long standing bias towards high spread vs low spread preferreds at least until and if it has a mini-Minksy moment. I assume the new TA preferred will be less volatile as a result. And, like with RON.PR.A&B maybe the deal will be sweetened in the end after all!

I continue to hold TA.PR.H because I find 6.50%+529M650 attractive given the credit risk.

OK, but the question at issue is not whether the new issue is attractive relative to the preferred share universe, but whether the new issue is attractive relative to TA.PR.H.

The market also seems to have a long standing bias towards high spread vs low spread preferreds at least until and if it has a mini-Minksy moment.

I’m not sure what this means. What bias and how do you measure it?

I assume the new TA preferred will be less volatile as a result.

Well, it’s possible. There are a number of reasons to suppose it will be less volatile:

I) Price changes as a result of spread changes will be dampened because downward price movement will be mitigated by a reduction of the negative value of the embedded call option, while upward movement will be reduced as the value of this option will become more negative.

I claim that the reduction of downward volatility is of no net value, since it is coming out of option value that will be produced by the deal; in other words, the money you save in an adverse market has come out of your pocket in the first place!

And reduction of upward volatility is a Bad Thing.

ii) Price Changes as a result of GOC-5 changes will be reduced by

a) the minimum reset guarantee, and

b) the reduced leverage to GOC-5 due to the higher price relative to par.

I claim that downward moves in GOC-5 over a five year time horizon are not a major threat; and that given the potential for a sharp upward move in this yield over the period, one wants increased leverage.

As with everything else in the investment business, you can put any numbers you like on this stuff to support the answer that you want to get. But I sure would like to see details of yours!

And, like with RON.PR.A&B maybe the deal will be sweetened in the end after all!

It might. But right now there’s only one deal on the table and I think it stinks.

[JH] On an unrelated thread, Assiduous Reader BarleyandHops posted:

Been catching up on reading..

But existing holders aren’t pleased. “This exchange, if successful, will effectively take away the potential capital gain associated with the current shareholders including myself who bought the shares at a deep discount. This is extremely unfair in my mind,” said one, who asked not to be named

http://business.financialpost.com/news/fp-street/transalta-plays-the-grinch-with-its-preferred-share-holders

If this is a trend, there will be many unhappy people. Let the lawyers hash thru it. Then again, in the long term the actual cost of borrowing in the pref market will rise as the lack of clarity will need to shore up the interest of buy and hold investors.

There’s an interesting article on ‘soliciting dealer fees’ titled Agrium Proxy Contest Leads to Scrutiny of Soliciting Dealer Fees in Canada.

It’s scandalous how sleazy companies are permitted to corrupt the proxy-voting process. Voting mechanics should be strictly separate from voting solicitation!

Mea culpa, mea culpa, mea maxima culpa.

Earlier in this thread I banned preftrader2016, under the false impression that this was just another alias for that old nuisance madequota.

I was wrong. I have spoken to preftrader2016 and he is not madequota.

I was led astray by the somewhat combative tone of preftrader2016‘s posts, his change of eMail between posts, and the fact that “preftrader” is an old alias of madequota‘s, which he used when he went so far as to create a rather idiotic attack site which for posterity has been preserved here and here. madequota has been banned from the site under a variety of identities, most recently here.

preftrader2016 has now been un-banned; I apologize for my incorrect identification.

Agreed that this deal is terrible. It’ll be especially bad when TA issues new prefs with a wider spread on top of the exchanged ones.

I want to see the information circular however and it’s not been posted on SEDAR. I don’t hold any TA so am not expecting to see one. Does anyone know if it has been received yet or be kind enough to post it someplace? Thanks

It should be on SEDAR immediately after mailing, but it’s not there yet! They’ll have to get cracking if they’re going to get it out well before the planned February 16 meeting date.

The Information Circular has been published.