OSFI has disgraced itself yet again with its response to the International Association of Insurance Supervisors’ 2016 Insurance Capital Standard Consultation.

The question is:

Q70 Section 5.3.1: Should Tier 1 Limited financial instruments be required to have a principal loss absorbency mechanism?

OSFI’s answer, found in the document “Section 5 Capital resources (Public)” that is linked on the above page, is “No”.

The follow-up question is:

Q70.1 Section 5.3.1 If “no” to Q70, should the principal be considered to provide loss absorbency on a going concern basis? Please explain how the instrument demonstrates loss absorbency on a going concern basis.

OSFI answers “Yes”, with the explanation:

Tier 1 Limited and Unlimited instruments provide loss absorbency on a going concern basis through the discretion the issuer has to not pay or cancel coupons on the instrument and the non-cumulative nature of such payments. The principal amount of such claims is only extinguished in resolution (regardless of accounting).

OSFI does not support principal loss absorbency mechanisms whereby instruments can be written down or converted into equity under going concern/early triggers (and that are not at the discretion of the supervisory authority) due to concerns that such triggers can lead to financial instability and adverse signalling regarding the issuer’s financial condition (as observed with CoCos issued by European banks earlier this year, for example). OSFI would only support such mechanisms where they result in a full and permanent write-off of the instrument at the point of non-viability where the IAIG has entered into resolution.

Note: What is an “IAIG”?:

An IAIG is a term under ComFrame for insurance groups or financial conglomerates that exceed thresholds on international activity and size. The IAIS defines an IAIG as a large, internationally active group that includes at least one sizeable insurance entity. There are two criteria for an insurance group to be identified as an IAIG: 1) International Activity — premiums are written in not fewer than three jurisdictions, and percentage of gross premiums written outside the home jurisdiction is not less than 10% of the group’s total gross written premium; and 2) Size —based on a rolling three-year average, total assets of not less than USD 50 Billion, or gross written premiums of not less than USD 10 Billion.

However, it is heartening to observe that the other four IAIS full members who provided public answers (European Insurance and Occupational Pensions Authority (Europe; the developers of the “Solvency 2” regime), BaFin (Germany), Financial Supervisory Service (Korea) and the National Association of Insurance Commissioners (USA)) all answered question 70 with “Yes”.

So I continue to believe that “Deemed Retractions” will eventually apply to Insurers and Insurance Holding Companies; I believe that while OSFI may well continue its ridiculous insistence on “low-trigger” conversions, it will adopt a global standard once the rest of the world agrees on conversion.

I will also note that in Canada, forcible conversion of Tier 1 capital for banks is also low-trigger, but this did not stop OSFI from demanding NVCC compliance for bank preferred share issues, which in turn led to “Deemed Retraction” for bank issues.

Now, is all that clear as mud? Sorry, but I’ve got PrefLetter to get out and don’t have much time for linking to previous material on this issue.

Update, 2017-4-19: As noted above, OSFI’s response included:

such triggers can lead to financial instability and adverse signalling regarding the issuer’s financial condition (as observed with CoCos issued by European banks earlier this year, for example).

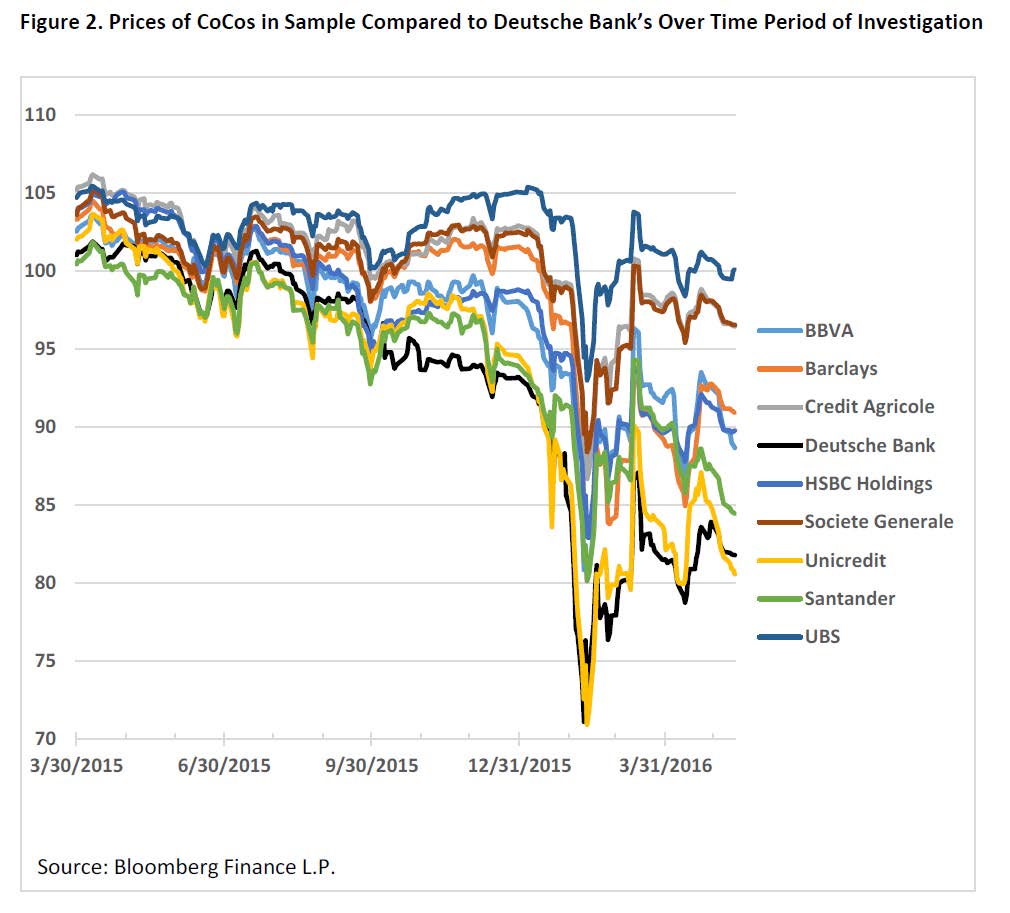

For a review of the performance – and reasons behind this performance of European CoCos, see Europe’s CoCos Provide a Lesson on Uncertainty:

Contingent convertible bonds (CoCos) issued by European global systemically important banks (G-SIBs) as part of their total loss-absorbing capacity (TLAC) are meant to enhance financial stability by forcing investors to absorb losses when a bank is under stress. Coupon payments are made at issuers’ discretion while loss absorption can be triggered at regulators’ discretion. This study investigates price effects of four press releases by Deutsche Bank AG in February 2016 related to the bank’s willingness and ability to make its upcoming CoCo coupon payments. Expected cash flow models capture changes in CoCo default risk, while event dates capture uncertainty effects. The price of a European G-SIB peer group portfolio declined a statistically significant 2.0-2.5 percent over two days in response to Deutsche Bank’s first press release. Deutsche Bank’s efforts to allay its own CoCo investors’ concerns appeared to increase concerns among CoCo investors generally. The results show potential negative effects of regulatory discretion.

Click for Big