Markets are forecasting no changes in the Canadian policy rate:

The bond market is starting to believe Bank of Canada Governor Stephen Poloz’s newfound optimism in the Canadian economy, resetting borrowing costs back to the day of his shock rate cut.

Traders have almost completely priced out another rate cut in banker’s acceptances contracts, a predictor of interest rates. Contracts due December, 2015, reached 1 per cent this month for the first time since Jan. 21, the day the Bank of Canada lowered its overnight rate to 0.75 per cent to contend with the collapse in the price of oil, the nation’s biggest export.

So-called Bax contracts have settled about 20 basis points above the central bank’s target rate on average since 1992, data compiled by Bloomberg show. The yield has averaged 0.91 per cent this year.

It was another violently mixed day for the Canadian preferred share market, with PerpetualDiscounts down 58bp, FixedResets gaining 18bp and DeemedRetractibles off 6bp. A lengthy Performance Highlights table is dominated by FixedResets, particularly on the good side. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.24 to be $0.98 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.90 cheap at its bid price of 24.95.

Click for Big

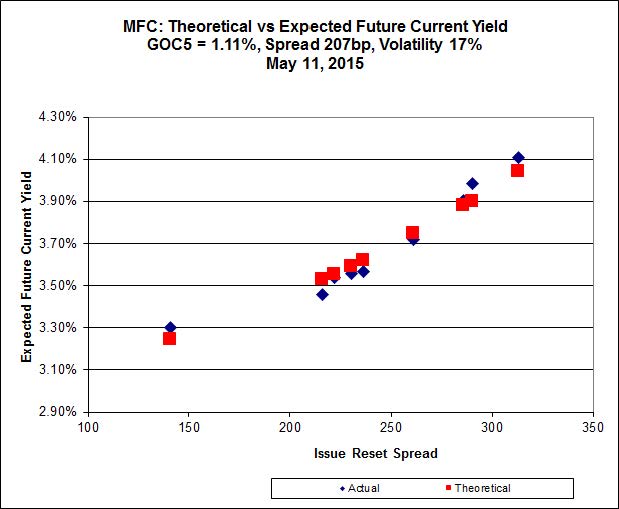

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 23.65 to be $0.49 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.16 to be $0.55 cheap.

Click for Big

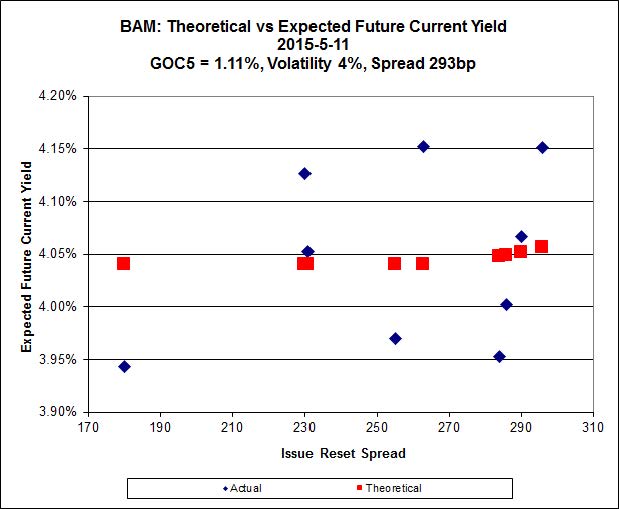

The cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.52 to be $0.62 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.98 and appears to be $0.58 rich.

Click for Big

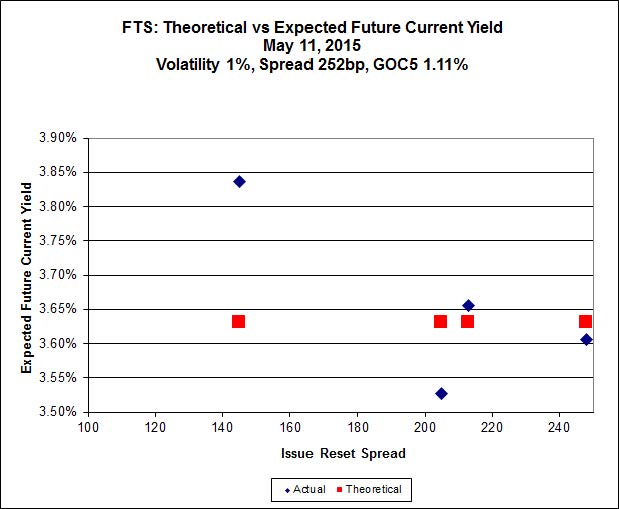

FTS.PR.H, with a spread of +145bp, and bid at 16.68, looks $0.95 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 22.40 and is $0.64 rich.

Click for Big

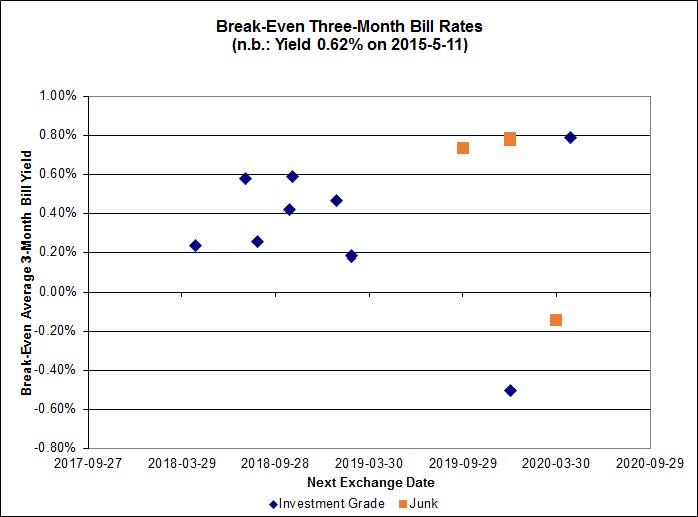

Investment-grade pairs now predict an average over the next five years of about 0.40%, but TRP.PR.A / TRP.PR.F is an outlier at -0.51% and BNS.PR.Y / BNS.PR.D is at +0.78%. On the junk side, the FFH.PR.E / FFH.PR.F pair is at -1.03% while BRF.PR.A / BRF.PR.B is at +1.03%.

Click for Big

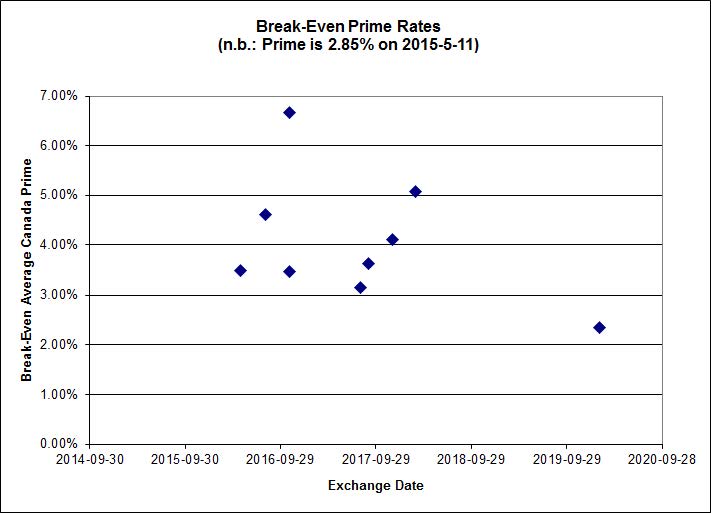

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.9378 % | 2,306.5 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.9378 % | 4,032.9 |

| Floater | 3.15 % | 3.26 % | 55,736 | 19.05 | 4 | -0.9378 % | 2,452.0 |

| OpRet | 4.42 % | -2.04 % | 38,273 | 0.14 | 2 | -0.0785 % | 2,768.6 |

| SplitShare | 4.56 % | 4.66 % | 59,622 | 3.35 | 3 | 0.1600 % | 3,233.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0785 % | 2,531.6 |

| Perpetual-Premium | 5.45 % | 2.00 % | 66,427 | 0.08 | 18 | -0.0697 % | 2,520.5 |

| Perpetual-Discount | 5.04 % | 5.03 % | 119,119 | 15.36 | 15 | -0.5779 % | 2,789.5 |

| FixedReset | 4.38 % | 3.72 % | 270,070 | 16.39 | 86 | 0.1805 % | 2,425.6 |

| Deemed-Retractible | 4.91 % | 3.22 % | 110,721 | 0.53 | 35 | -0.0569 % | 2,647.4 |

| FloatingReset | 2.58 % | 2.92 % | 62,894 | 6.19 | 7 | 0.2251 % | 2,338.7 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.C | Floater | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 3.33 % |

| CU.PR.F | Perpetual-Discount | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 22.46 Evaluated at bid price : 22.85 Bid-YTW : 4.91 % |

| CIU.PR.C | FixedReset | -1.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 16.02 Evaluated at bid price : 16.02 Bid-YTW : 3.80 % |

| RY.PR.Z | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 23.08 Evaluated at bid price : 24.54 Bid-YTW : 3.32 % |

| TRP.PR.D | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 22.71 Evaluated at bid price : 23.69 Bid-YTW : 3.65 % |

| PWF.PR.S | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 24.21 Evaluated at bid price : 24.62 Bid-YTW : 4.89 % |

| TRP.PR.A | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 20.88 Evaluated at bid price : 20.88 Bid-YTW : 3.64 % |

| CU.PR.G | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 22.55 Evaluated at bid price : 22.95 Bid-YTW : 4.89 % |

| BAM.PR.B | Floater | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 15.41 Evaluated at bid price : 15.41 Bid-YTW : 3.26 % |

| ENB.PR.F | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 20.23 Evaluated at bid price : 20.23 Bid-YTW : 4.53 % |

| FTS.PR.M | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 23.16 Evaluated at bid price : 24.89 Bid-YTW : 3.57 % |

| BMO.PR.T | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 22.96 Evaluated at bid price : 24.30 Bid-YTW : 3.38 % |

| MFC.PR.N | FixedReset | 1.10 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.96 Bid-YTW : 4.18 % |

| FTS.PR.K | FixedReset | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 21.98 Evaluated at bid price : 22.40 Bid-YTW : 3.64 % |

| MFC.PR.M | FixedReset | 1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 4.07 % |

| BNS.PR.Z | FixedReset | 1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.60 Bid-YTW : 3.48 % |

| TRP.PR.C | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 18.30 Evaluated at bid price : 18.30 Bid-YTW : 3.57 % |

| GWO.PR.N | FixedReset | 1.97 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.15 Bid-YTW : 6.27 % |

| SLF.PR.G | FixedReset | 2.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.03 Bid-YTW : 6.38 % |

| FTS.PR.G | FixedReset | 2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 21.85 Evaluated at bid price : 22.16 Bid-YTW : 3.72 % |

| RY.PR.H | FixedReset | 2.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 23.11 Evaluated at bid price : 24.70 Bid-YTW : 3.32 % |

| MFC.PR.L | FixedReset | 2.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.65 Bid-YTW : 4.28 % |

| TD.PF.B | FixedReset | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 23.12 Evaluated at bid price : 24.69 Bid-YTW : 3.33 % |

| HSE.PR.A | FixedReset | 2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 17.92 Evaluated at bid price : 17.92 Bid-YTW : 3.97 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.B | FixedReset | 122,714 | TD crossed four blocks: 35,000 shares, 17,500 shares, 30,000 and 29,500, all at 15.91. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 3.67 % |

| RY.PR.I | FixedReset | 85,880 | Nesbitt crossed two blocks of 35,000 each and one of 15,000, all at 25.35. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.41 Bid-YTW : 2.99 % |

| TRP.PR.G | FixedReset | 68,982 | TD crossed 20,000 at 25.07. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 23.11 Evaluated at bid price : 24.95 Bid-YTW : 3.81 % |

| BNS.PR.O | Deemed-Retractible | 63,250 | RBC crossed 61,100 at 26.00. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-06-10 Maturity Price : 25.50 Evaluated at bid price : 25.82 Bid-YTW : -7.56 % |

| TRP.PR.A | FixedReset | 58,801 | TD crossed 35,000 at 21.40 and 15,000 at 21.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-05-11 Maturity Price : 20.88 Evaluated at bid price : 20.88 Bid-YTW : 3.64 % |

| BMO.PR.M | FixedReset | 45,800 | RBC crossed 45,200 at 25.23. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 2.85 % |

| There were 31 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.K | FixedReset | Quote: 22.40 – 22.98 Spot Rate : 0.5800 Average : 0.3664 YTW SCENARIO |

| MFC.PR.H | FixedReset | Quote: 25.79 – 26.24 Spot Rate : 0.4500 Average : 0.2931 YTW SCENARIO |

| RY.PR.Z | FixedReset | Quote: 24.54 – 24.88 Spot Rate : 0.3400 Average : 0.2403 YTW SCENARIO |

| MFC.PR.C | Deemed-Retractible | Quote: 23.78 – 24.05 Spot Rate : 0.2700 Average : 0.1733 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 23.99 – 24.31 Spot Rate : 0.3200 Average : 0.2254 YTW SCENARIO |

| BMO.PR.K | Deemed-Retractible | Quote: 25.60 – 25.84 Spot Rate : 0.2400 Average : 0.1504 YTW SCENARIO |

I’m a little unclear as to what the negative predicted interest rate for the FFH.PR.E / F pair means. Is the simplest explanation that there is a market mispricing, and that all holders of the E series should swap into the F series?

Or something else (maybe they have different risk profiles, or are not inter-convertible in 5 years, or…)

Is the simplest explanation that there is a market mispricing

Yes

and that all holders of the E series should swap into the F series?

There might be some with high transaction costs and small holdings who might feel that the potential profit is too small to be worth the bother.

And there might be others who feel that a prediction of an average 3-month bill rate over the next few years of -1.03% is bang on the money.

In cases in which the breakeven rate is considered ‘too high’ there might even be some – perhaps levered up to hell ‘n’ gone – who will be so adversely affected by a rise in policy yields that they really need to own the FloatingReset; they’re not concerned with the ‘expected return’ of all scenarios, they’re concerned with the 10% of the scenarios that will kill them.

But yeah, assuming that you an execute swaps at prices reasonably approximating those used to calculate the break-even rate (I have used bid prices for all issues in this series of calculations), then basically a swap is indicated. Or, at the very least, if you have decided that FFH.PR.E is the FixedReset you want to own, put a bid in on FFH.PR.F instead.

Or something else (maybe they have different risk profiles, or are not inter-convertible in 5 years, or…)

Well, if that’s the case then I’ve made a mistake and FFH.PR.E / FFH.PR.F does not constitute a Strong Pair. I don’t think I have, but I’m willing to listen to contrary arguments.