DBRS has announced that it:

has today taken rating actions on 11 issuers following a full review of the oil and gas portfolio. This review covered 19 issuers and was undertaken in light of the recent price crude oil price declines and the outlook for a continued weak pricing environment. The rating actions are highlighted in the table below. As a result of the announced actions today, all issuers within DBRS’s oil and gas portfolio (with the exception of Suncor Energy Inc., rated A (low), and Canadian Oil Sands Limited (COS), rated BBB (low), which are both Under Review with Developing Implications) now have a Negative trend.

…

The weak pricing environment has created material, near-term financial challenges for oil and gas issuers that has been reflected today by DBRS’s rating and trend changes. Companies have responded to the lower pricing environment by cutting capital expenditure (capex) programs, undertaking asset sales and implementing cost-saving measures. However the sharp contraction in cash flows from oil- and gas-producing activities has been far greater, resulting in cash flow deficits, a drain on liquidity and escalating debt/cash flow ratios. The integrated oil companies and multinational oil companies rated by DBRS (which have downstream exposure) have weathered the pricing storm better but have also experienced weakening financial risk profiles. With expectations for continued weak pricing, the key credit metrics of issuers will remain under pressure. DBRS anticipates companies will announce additional significant capex cuts, cost-saving measures and possible dividend cuts to preserve liquidity and balance sheet strength. As such, DBRS will monitor each issuer closely as more information becomes available. A lack of concrete action by issuers to respond to a period of lower pricing and/or prevent their financial profiles from eroding further could lead to further negative rating actions by DBRS.

…

With the weak pricing outlook for both oil and natural gas, DBRS-rated oil and gas companies were all stress tested under various crude oil and natural gas pricing scenarios over a two-year forecast period. As a base case scenario DBRS used a forecast in line with the forward oil and gas price curves. The base case price forecast incorporated a West Texas Intermediate (WTI) oil price of USD 32 per barrel (bbl) in 2016 and USD 37/bbl in 2017. The natural gas price base case incorporated a forecast of USD 2.25 and CDN 2.25 per thousand cubic feet for NYMEX and AECO natural gas, respectively, in 2016. For 2017 the forecast was USD 2.75 and CDN 2.75 for NYMEX and AECO natural gas, respectively. A CDN/USD $0.70 exchange rate was assumed in the base case. DBRS also considered stressed pricing scenarios as low as USD 25/bbl for WTI in 2016, USD 30/bbl in 2017 and a CDN/USD exchange rate of $0.68. The stress tests focused on the effect that oil and gas prices would have on: (1) internally generated cash flow, (2) discretionary versus committed capex, (3) dividend flexibility, (4) planned asset dispositions, (5) covenant tests, (6) available liquidity, (7) key credit metrics and (8) a recovery rate analysis for high yield credits. Moreover, for non-investment-grade issuers borrowing bases were stress tested, at reductions of 20%, 25%, and 30% of current levels given the uncertainty with the upcoming borrowing base reviews.

Affected issues are HSE.PR.A, HSE.PR.C, HSE.PR.E and HSE.PR.G.

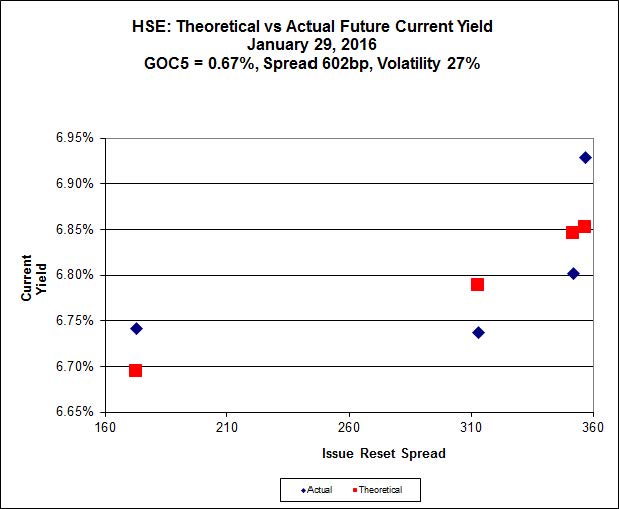

Implied Volatility analysis shows a high level of Implied Volatility (implying a certain amount of directionality in expected pricing is contradicting an assumption of the Black-Scholes analysis) and a very high spread.

Click for Big

According to this analysis, HSE.PR.E, resetting at +357bp on 2020-3-31, is $0.17 cheap, while HSE.PR.C, resetting at +313 on 2019-12-31 is $0.11 rich.

Update, 2016-2-19: Moody’s has affirmed HSE at Baa2:

Husky’s Baa2 senior unsecured rating reflects favorably priced contracts for its natural gas production offshore China, integrated upstream and refining operations that provide diversity and lessen cash flow volatility, and strong cash flow-based leverage and interest coverage metrics. These positive attributes are mitigated by the company’s exposure to weak commodity prices in its North American conventional business and risks associated with the ramp up of in-situ oil sands production at Sunrise.

Husky will have good liquidity through 2016. At September 30, 2015 the company had approximately C$2.6 billion available under its C$4 billion revolving credit facilities (C$2 billion of which matures in December 2016 and C$2 billion of which matures in June 2018). We expect the facility maturing in December 2016 to be renewed and extended. We expect negative free cash flow of about C$250 million through December 2016. We expect proceeds from asset sales of approximately C$1.5 billion to be used to fund the negative free cash flow and reduce short term debt. Husky has a US$200 million note maturity in November 2016. The company has numerous assets that could be sold to enhance liquidity.

The stable outlook reflects improving financial metrics in the current low oil price environment.

The rating could be upgraded when RCF/D appears likely to approach 30% after taking into account the reinstatement of a normalized long term dividend.

The rating could be downgraded if it appears that the RCF/D is likely to fall towards 20%.

Husky Energy Inc., headquartered in Calgary, Alberta, is a diversified independent E&P company with principal assets in North America and Southeast Asia. While Husky is a publicly traded company, approximately 69% is owned by entities controlled by Mr. Li Ka-shing of Hong Kong.