Brookfield Office Properties Inc. has announced:

the completion of its previously announced Preferred Shares, Series II issue. The offering was underwritten by a syndicate of underwriters led by Scotiabank, CIBC Capital Markets, RBC Capital Markets and TD Securities Inc. On November 29, 2017, the syndicate agreed to purchase 10,000,000 Preferred Shares, Series II at C$25.00 per share.

The Preferred Shares, Series II will yield 4.85% annually for the initial period ending December 31, 2022. The net proceeds of the issue will be used by Brookfield Office Properties for general corporate purposes.

The Preferred Shares, Series II will commence trading today on the Toronto Stock Exchange under the ticker symbol BPO.PR.I.

BPO.PR.I is a FixedReset, 4.85%+323M485, announced 2017-11-29. The issue will be tracked by HIMIPref™ but has been relegated to the Scraps subindex on credit concerns.

The issue traded 398,681 shares today in a range of 24.40-70 before closing at 24.55-65. Vital statistics are:

| BPO.PR.I | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-12-07 Maturity Price : 23.00 Evaluated at bid price : 24.55 Bid-YTW : 4.95 % |

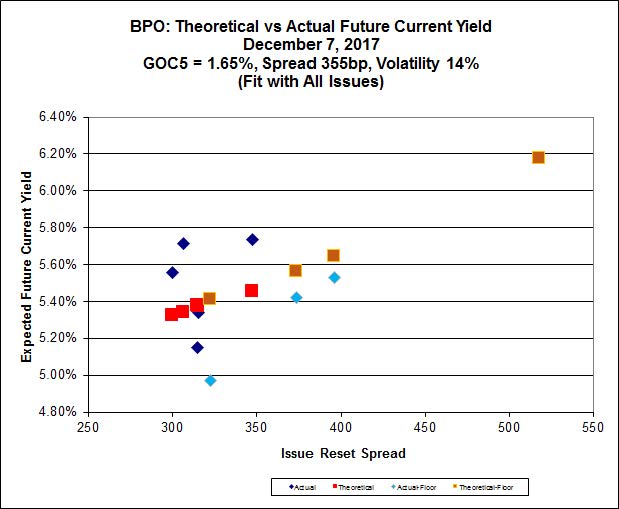

This issue looks extraordinarily expensive to me! According to Implied Volatility analysis:

Click for Big

With the parameters shown, the theoretical value of the new issue is a mere 22.56, down over fifty cents from announcement day. Critics will be quick to point out that in this calculation there is zero value assigned to the minimum rate guarantee … but I’d say that’s about right!

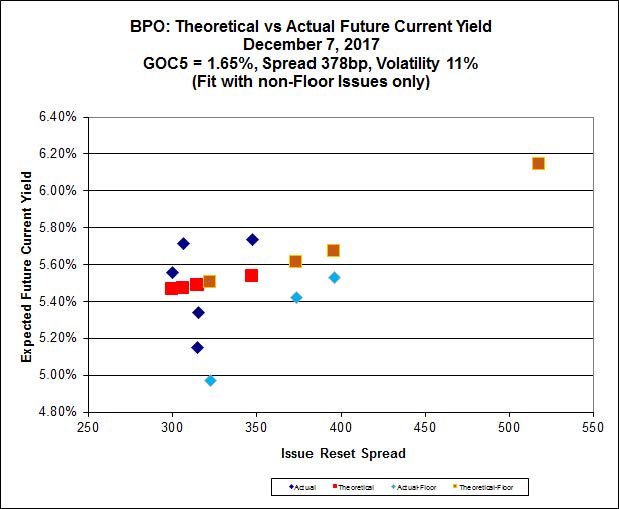

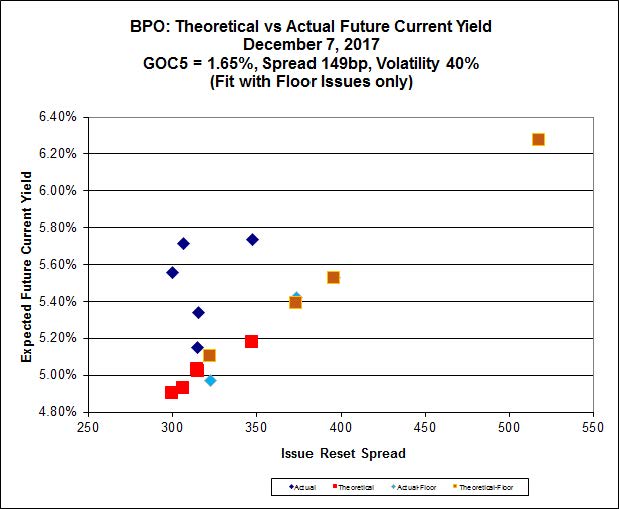

However, when the graph is examined more closely, it does look as if the Floor issues are on a different line with a steeper slope than the non-Floor issues. So let’s try disaggregating the data again:

Click for Big

Click for Big

It’s an interesting idea that bears watching in the future. The Implied Volatility of the “Floor” series is extremely high, indicating that the Black-Scholes assumptions do not hold, which I usually take to mean implies a strong belief in the directionality of future prices, e.g., that all issues will be called and hence are all expected to gravitate towards par. Regretably, all extant ‘floor’ issues (BPO.PR.C, BPO.PR.E, BPO.PR.G) have relatively high spreads (518, 396 and 374bp, respectively) and are trading above or only slightly below par, which may be contaminating the data.

[…] was issued as a FixedReset, 4.85%+323M485, that commenced trading 2017-12-7 after being announced 2017-11-29. The issue has been tracked by HIMIPref™ but has been relegated […]

[…] will reset at 6.359% effective 2023-1-1. BPO.PR.I was issued as a FixedReset, 4.85%+323M485, that commenced trading 2017-12-7 after being announced […]

[…] was issued as a FixedReset, 4.85%+323M485, that commenced trading 2017-12-7 after being announced 2017-11-29. BPO.PR.I will reset at 6.359% effective 2023-1-1; I recommended […]