DBRS has announced:

that the ratings of Element Fleet Management Corp. (Element or the Company), including its Long-Term Issuer Rating of BBB (high) are not impacted by the quarterly loss reported for 4Q17, or by the underlying drivers for the loss. For 4Q17, Element reported, on an IFRS basis, a net loss of $1.5 million in 4Q17, down from net income of $67.2 million in the prior quarter. While DBRS sees no impact to the current ratings from the quarter’s results, DBRS would view unfavorably additional material losses at 19th Capital. Also, DBRS would view negatively a sustained deterioration in origination volume growth or should customer retention rates not return to their historically strong levels, indicating that management efforts to address customer related issues from the integration have not been successful.

Results were impacted by charges related to ongoing challenges at the Company’s 19th Capital Group LLC joint venture (19th Capital or the JV), as well as an elevated level of operating expenses. Also, the Company’s results were impacted by $11.9 million of strategic review related costs that are not expected to reoccur.

For the quarter, Element’s results were impacted by a $60.8 million share of loss and equity charge related to its 19th Capital JV. Within the share of loss charge is operational losses of $14.1 million, as well as a $17.8 million loss on the disposition of certain assets in the JV. These losses were primarily driven by the JV’s ongoing execution of its strategic plan to improve operating performance. The strategic plan includes the shifting of the customer base to smaller corporate fleets from riskier owner-operators, optimizing the fleet mix, and accelerating the trade-in or sale of certain out of favor older truck models.

Also, included in the overall loss and charges related to 19th Capital was a $29.0 million provision for impairment by Element against its investment in the JV. While the overall U.S. trucking industry has begun to recover from the down cycle that began in 2015, Element considered it prudent to take a charge against the value of the investment given the expectations that an improvement in the JV’s operating performance may not be visible until late 2018 and with execution risks in the strategic plan still present. DBRS views the impairment provision as a conservative action by management, but is concerned about the ongoing losses at the JV, as well as the potential for the investment to be a distraction to Element’s management at a time when operational issues at the core fleet management business need to be addressed.

During 4Q17, Element experienced a higher than normal degree of customer attrition that included three large customers. The attrition was attributable to IT integration issues experienced during 1H17. The Company expects actions taken to address these customer concerns to return the retention rate to the historical level of approximately 97% in 2018. DBRS notes that volumes in the quarter were up slightly on a sequential basis and that management noted a good pipeline of new customers for 2018, suggesting that the issues from 1H17 are being addressed. DBRS will closely monitor volumes and customer retention in 2018.

Adjusted operating expenses were 6.1% higher sequentially in the quarter to $127.1 million. This resulted in the Company’s net efficiency ratio to weaken to 55.3% from 50.7% in the prior quarter and 48.6% in the comparable period a year ago. Element announced that it has initiated cost reduction actions during the current quarter, including headcount reduction, office space optimization, and the limiting of discretionary expenses. Thus, the Company expects to incur a charge of approximately $40 million in 1Q18 related to these actions. The actions are anticipated to produce an annual run rate savings of approximately $20 million. DBRS views the actions favorably should the savings be fully realized and result in an improved operating efficiency.

While total net revenues were 2.7% lower quarter-on-quarter in 4Q17 at $229.8 million, DBRS sees positives in the continuing strengthening of service and other related revenue. On a sequential basis, core fleet service and other revenue improved 4.5% to $141.0 million, and comprises 64% of total net revenue.

Element’s balance sheet fundamentals remain acceptable. The asset quality of the core fleet business remains sound and supportive of the ratings. Impaired finance receivables at December 31, 2017, were stable at a very low 0.04%. Tangible leverage was higher at 7.7x at quarter-end, which is slightly above management’s target range of 7.0x to 7.5x. Importantly, tangible leverage remains inside the bank facility covenant. Meanwhile, Element continues to maintain sufficient available liquidity. At December 31, 2017, the Company had total available liquidity of $4.7 billion, which is more than sufficient to meet debt maturities and expected new originations over the next 12 months.

Affected issues are EFN.PR.A, EFN.PR.C, EFN.PR.E, EFN.PR.G and EFN.PR.I, which haven’t been doing too well lately:

| EFN Preferreds Plunge | |||

| Ticker | Quote 2018-02-05 |

Quote 2018-03-19 |

Total Return (bid/bid) |

| EFN.PR.A | 24.85-97 | 18.23-38 | -25.03% |

| EFN.PR.C | 24.47-05 | 18.07-22 | -24.54% |

| EFN.PR.E | 24.51-65 | 17.12-42 | -28.57% |

| EFN.PR.G | 25.00-06 | 17.91-00 | -26.79% |

| EFN.PR.I | 24.35-50 | 16.67-90 | -30.14% |

As global markets gyrate, shares of Element Fleet Management Corp., the brainchild of company founder and Bay Street financier Steve Hudson, plummeted 29 per cent in a single day after it announced the departure of its chief executive officer and the loss of a crucial customer.

It is a stunning fall for what was, until recently, a high-flying company. The newly revealed woes have also changed the narrative around Mr. Hudson’s comeback, a long march to regain investors’ trust after the downfall of his previous venture.

Element has not named a new chief to replace outgoing CEO Brad Nullmeyer, who is one of Mr. Hudson’s closest associates, and the company is now conducting an external search. But the board did reveal that it expects earnings from its core fleet business to fall by three to five per cent in fiscal 2018 after losing the servicing business of a large client, which the company didn’t name, in recent months.

… and the other shoe dropped March 15:

Shares of Element Fleet Management Corp. plummeted for the second time in five weeks as the struggling Bay Street finance company said it will take a restructuring charge, cut staff and close offices as part of a recovery plan that will take the rest of 2018 to implement.

The Toronto-based company, founded by financier Steve Hudson, who is one of its largest individual shareholders, warned that earnings will fall short of investor expectations. The stock dropped by as much as 36 per cent on Thursday morning before closing down 24 per cent. Element has lost more than $3.5-billion in stock market value in the past year.

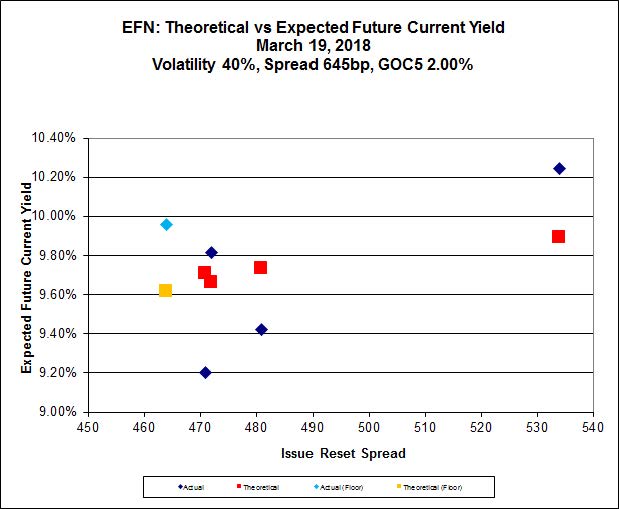

And, for what it’s worth, here’s the Implied Volatility Analysis:

Click for Big

EFN has had a good run (5+ years). Current situation may turnaround and I expect it shall. EFN.PR.I seems to me to have some consideration to weather the headwinds with some upside beyond divies.

No cheap wine tonight. Picking up a friend tonight at YYZ (03/20).